| Village Bank and Trust Financial Corp. (Nasdaq: VBFC)

Market Areas

(1) Source: S&P Global, Data as of the 6/30/2023 FDIC Summary of Deposits for the Richmond, VA MSA.

(2) Source: Greater Richmond Partnership.

(3) Source: Williamsburgva.gov

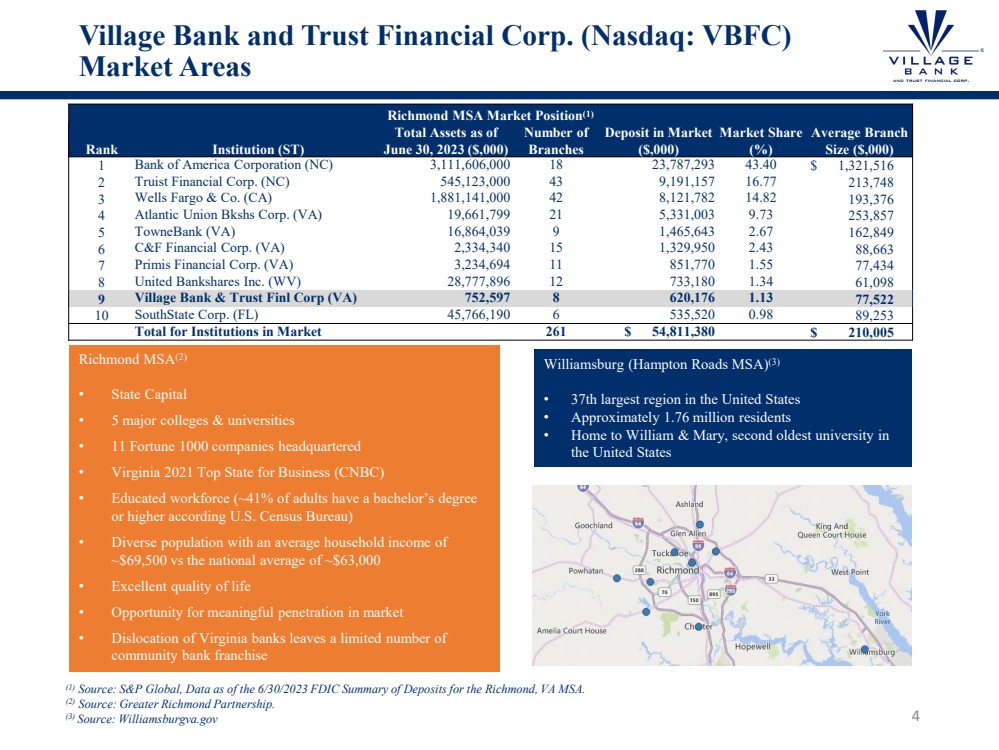

Richmond MSA(2)

• State Capital

• 5 major colleges & universities

• 11 Fortune 1000 companies headquartered

• Virginia 2021 Top State for Business (CNBC)

• Educated workforce (~41% of adults have a bachelor’s degree

or higher according U.S. Census Bureau)

• Diverse population with an average household income of

~$69,500 vs the national average of ~$63,000

• Excellent quality of life

• Opportunity for meaningful penetration in market

• Dislocation of Virginia banks leaves a limited number of

community bank franchise

Williamsburg (Hampton Roads MSA)(3)

• 37th largest region in the United States

• Approximately 1.76 million residents

• Home to William & Mary, second oldest university in

the United States

Richmond MSA Market Position(1)

Rank Institution (ST)

Total Assets as of

June 30, 2023 ($,000)

Number of

Branches

Deposit in Market

($,000)

Market Share

(%)

Average Branch

Size ($,000)

1 Bank of America Corporation (NC) 3,111,606,000 18 23,787,293 43.40 $ 1,321,516

2 Truist Financial Corp. (NC) 545,123,000 43 9,191,157 16.77 213,748

3 Wells Fargo & Co. (CA) 1,881,141,000 42 8,121,782 14.82 193,376

4 Atlantic Union Bkshs Corp. (VA) 19,661,799 21 5,331,003 9.73 253,857

5 TowneBank (VA) 16,864,039 9 1,465,643 2.67 162,849

6 C&F Financial Corp. (VA) 2,334,340 15 1,329,950 2.43 88,663

7 Primis Financial Corp. (VA) 3,234,694 11 851,770 1.55 77,434

8 United Bankshares Inc. (WV) 28,777,896 12 733,180 1.34 61,098

9 Village Bank & Trust Finl Corp (VA) 752,597 8 620,176 1.13 77,522

10 SouthState Corp. (FL) 45,766,190 6 535,520 0.98 89,253

Total for Institutions in Market 261 $ 54,811,380 $ 210,005

4 |