UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities

Exchange Act of 1934

Filed by the Registrant x Filed by a Party other than the

Registrant ¨

Check the appropriate box:

| ¨ |

Preliminary Proxy Statement |

| ¨ |

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x |

Definitive Proxy Statement |

| ¨ |

Definitive Additional Materials |

| ¨ |

Soliciting Material Pursuant to Rule 14a-12 |

TRANSDIGM GROUP INCORPORATED

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy

Statement, if Other Than Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ |

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11 |

| |

(1) |

Title of each class of securities to which transaction applies: |

| |

(2) |

Aggregate number of securities to which transaction applies: |

| |

(3) |

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and

state how it was determined): |

| |

(4) |

Proposed maximum aggregate value of transaction: |

| ¨ |

Fee paid previously with preliminary materials. |

| ¨ |

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously.

Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| |

(1) |

Amount Previously Paid: |

| |

(2) |

Form, Schedule or Registration Statement No.: |

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

Notice is hereby given that the Annual Meeting of Stockholders of TransDigm Group Incorporated, a Delaware corporation (the “Company”), will

be held at 1301 East Ninth Street, 4th Floor, Cleveland, Ohio 44114, on Wednesday, March 2, 2016, at 9:00 a.m., Eastern time, for the following purposes:

1. To elect six directors, each to serve a one-year term and until a successor has been duly elected and qualified;

2. To conduct an advisory vote on compensation paid to the Company’s named executive officers;

3. To ratify the selection of Ernst & Young LLP as the Company’s independent accountants for the Company’s fiscal year

ending September 30, 2016; and

4. To transact such other business as may properly come before the meeting.

Only stockholders of record at the close of business on January 4, 2016 will be entitled to notice of and to vote at the meeting or

any adjournment of the meeting. Stockholders are urged to complete, date and sign the enclosed proxy and return it in the enclosed envelope.

By order of the Board of Directors,

Halle Fine Terrion

Secretary

Dated: January 21, 2016

YOUR VOTE IS IMPORTANT. PLEASE SIGN, DATE AND RETURN YOUR PROXY.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE STOCKHOLDERS MEETING TO BE HELD ON MARCH 2, 2016.

The Proxy Statement and Proxy Card are available at

http://www.transdigm.com/phoenix.zhtml?c=196053&p=proxy

TABLE OF CONTENTS

PROXY STATEMENT

The Company’s Board of Directors is sending you this proxy statement to ask for your vote as a stockholder of TransDigm Group Incorporated (the

“Company”) on matters to be voted on at the upcoming annual meeting of stockholders. The meeting will be held at 1301 East Ninth Street, 4th Floor, Cleveland, Ohio 44114, on

Wednesday, March 2, 2016, at 9:00 a.m., Eastern time. The Company is mailing this proxy statement and the accompanying notice of meeting and proxy form, along with the Company’s Annual Report to Stockholders, on or about

January 21, 2016.

ABOUT THE MEETING

What is the purpose of the annual meeting of stockholders?

The purpose of the annual meeting of stockholders is to vote on matters outlined in the accompanying notice of meeting, including the election of six

directors, an advisory vote on executive compensation and the ratification of the Company’s selection of its independent accountants. We are not aware of any other matter that will be presented for your vote at the meeting.

Who is entitled to vote?

Only stockholders of record at the close of business on the record date, January 4, 2016, are entitled to receive notice of the meeting and to vote

the shares of common stock that they held on the record date at the meeting, or any postponement or adjournment of the meeting. Each outstanding share of common stock entitles its holder to cast one vote on each matter to be voted on. As of the

record date, the Company had outstanding 53,592,306 shares of common stock.

Who can attend the meeting?

Only stockholders as of the record date, or their duly appointed proxies, may attend the meeting. If you hold your shares in “street name”

(that is, through a broker or other nominee), your name does not appear in the Company’s records, so you will need to bring a copy of your brokerage statement reflecting your ownership of shares of common stock as of the record date.

When and where is the meeting?

The meeting will be held at 1301 East Ninth Street, 4th Floor, Cleveland, Ohio 44114, on Wednesday,

March 2, 2016, at 9:00 a.m., Eastern time. For directions to the meeting, call Investor Relations at (216) 706-2945.

Who

is soliciting my proxy?

This solicitation of proxies is made by and on behalf of the Company’s Board of Directors. The Company

will bear the cost of the solicitation of proxies. In addition to the solicitation of proxies by mail, regular employees of the Company and its subsidiaries may solicit proxies by telephone, facsimile or email. In addition, we have retained Alliance

Advisors, LLC, 200 Broadacres Drive, 3rd Floor, Bloomfield, NJ 07003, at an estimated cost of $15,000, plus customary costs and expenses, to aid in the solicitation of proxies from brokers, institutional holders and individuals who own a large

number of shares of common stock. The Company’s employees will not receive any additional compensation for their participation in the solicitation.

1

How do I vote by proxy?

Whether or not you plan to attend the annual meeting, we urge you to complete, sign and date the enclosed proxy form and to return it in the envelope

provided. Returning the proxy form will not affect your right to attend the annual meeting.

If you properly complete your proxy form and send it to

the Company in time to vote, your proxy (one of the individuals named in the proxy form) will vote your shares as you have directed. If you sign the proxy form but do not make specific choices, your proxy will vote your shares as recommended by the

Board of Directors to elect the director nominees listed in “Election of Directors,” in favor of the proposal to approve the compensation paid to the Company’s named executive officers, and in favor of ratification of the selection of

Ernst & Young as the Company’s independent accountants.

If any other matter is presented, your proxy will vote in accordance

with his best judgment. As of the date of this proxy statement, we are not aware of other matters to be acted on at the annual meeting other than those matters described in this proxy statement.

May I revoke my proxy?

If you give a proxy, you may revoke it at any time before it is exercised by giving written notice to the Company at its principal executive offices

located at 1301 East Ninth Street, Suite 3000, Cleveland, Ohio 44114, or by giving notice to the Company in open meeting. Your presence at the annual meeting, without any further action on your part, will not revoke your previously granted proxy.

What constitutes a quorum?

The presence at the annual meeting, either in person or by proxy, of the holders of a majority of the shares of common stock outstanding on the record

date will represent a quorum permitting the conduct of business at the meeting. Proxies received by the Company marked as abstentions or broker non-votes will be included in the calculation of the number of shares considered to be present at the

meeting.

What vote is required to approve each proposal assuming that a quorum is present at the Annual Meeting?

The six nominees receiving the greatest number of votes ‘FOR’ election will be elected as directors. If you do not vote for a particular

director nominee, or if you indicate ‘WITHHOLD AUTHORITY’ for a particular nominee on your proxy form, your vote will not count either for or against the nominee. If your shares are held in “street name” by a broker or nominee

indicating on a proxy that it does not have authority to vote on this or any other proposal, this will result in a “broker non-vote,” which will not count as a vote for or a vote against any of the nominees.

The approval of executive compensation is an advisory vote; however, the Board of Directors and the Compensation Committee will consider the affirmative

vote of a majority of the shares present in person or by proxy and entitled to vote on the proposal as approval of the compensation paid to the Company’s named executive officers. Broker non-votes will not have a positive or negative effect on

the outcome of this proposal. Abstentions will have the same effect as a vote against the proposal.

Although the Audit Committee may select the

Company’s independent accountants without stockholder approval, the Audit Committee will consider the affirmative vote of a majority of the shares present in person or by proxy and entitled to vote on the proposal to be a ratification by the

stockholders of the selection of Ernst & Young LLP as the Company’s independent accountants. Broker non-votes will not have a positive or negative effect on the outcome of this proposal. Abstentions will have the same effect as a vote

against the proposal.

2

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND

MANAGEMENT

The following table sets forth information regarding the beneficial ownership of Company common stock as of December 18,

2015 with respect to each person known to be a beneficial owner of more than five percent of the outstanding common stock.

|

|

|

|

|

|

|

| Name and Address of Beneficial Holder |

|

Amount and Nature of

Beneficial Ownership |

|

|

Percentage

of Class |

|

|

|

| FMR LLC(1)

245 Summer Street

Boston, MA 02210 |

|

|

4,569,533 |

|

|

8.50% |

|

|

|

| Vanguard Group, Inc.(2)

100 Vanguard Blvd.

Malvern, PA 19355 |

|

|

3,430,934 |

|

|

6.38% |

|

|

|

| Capital World

Investors(3) 333 South Hope Street, 55th Floor Los Angeles, CA 90071 |

|

|

3,305,000 |

|

|

6.15% |

|

|

|

| Berkshire Partners LLC(4)

200 Clarendon Street, 35th floor

Boston, MA 02116 |

|

|

2,711,047 |

|

|

5.04% |

| (1) |

Information obtained from a Schedule 13G/A filed by FMR LLC, Edward C. Johnson III and Abigail P. Johnson on February 13, 2015 and a Form 13F-HR filed by FMR LLC on November 10, 2015

reporting holdings as of September 30, 2015. According to FMR LLC’s 13F-HR filing, FMR LLC has voting power over 77,734 shares. Mr. Johnson is Chairman of FMR LLC. Ms. Johnson is Vice Chairman, Chief Executive Officer and President of

FMR, LLC. Members of the family of Mr. Johnson, including Ms. Johnson, are the predominant owners, directly or through trusts, of Series B voting common shares of FMR LLC, representing 49% of the voting power of FMR LLC. The Johnson family and

all other Series B shareholders have entered into a shareholders’ voting agreement under which all Series B voting common shares will be voted in accordance with the majority vote of the Series B voting common shares. Accordingly, through their

ownership of voting common shares and the shareholders’ voting agreement, members of the Johnson family may be deemed to form a controlling group with respect to FMR LLC. Neither FMR LLC nor Mr. Johnson nor Ms. Johnson has the sole power

to vote or direct the voting of the shares owned directly by the various investment companies registered under the Investment Company Act (the “Fidelity Funds”) advised by Fidelity Management & Research Company (“FMR Co.”), a

wholly owned subsidiary of FMR LLC, which power resides with the Fidelity Funds’ Boards of Trustees. FMR Co. carries out the voting of the shares under written guidelines established by the Fidelity Funds’ Boards of Trustees.

|

| (2) |

Information obtained from a Schedule 13G filed by The Vanguard Group on February 10, 2015 and a Form 13F-HR filed by Vanguard Group, Inc. on November 12, 2015 reporting holdings as of

September 30, 2015. Vanguard Group, Inc. has voting power over 52,314 shares. |

| (3) |

Information obtained from a Schedule 13G filed by Capital World Investors on February 13, 2015 and a Form 13F-HR filed by Capital World Investors on November 16, 2015 reporting holdings

as of September 30, 2015. |

| (4) |

Information obtained from a Schedule 13D/A filed by Berkshire Fund VII, L.P. (“Fund VII”), Berkshire Fund VII-A, L.P. (“Fund VII-A”), Berkshire Investors LLC

(“Investors”), Berkshire Investors III LLC (“Investors III”), Stockbridge Fund, L.P. (“SF”), Stockbridge Partners LLC (“SP”), Stockbridge Fund M, L.P. (“SFM”), Stockbridge Absolute Return Fund, L.P.

(“SARF”) and Stockbridge Master Fund (OS), L.P. (“SOS”) on March 10, 2014 and from information obtained from Berkshire Partners LLC. The shares are beneficially owned by or through certain affiliated investment entities,

including direct ownership by Fund VII, Fund VII-A, Investors, Investors III, SF, SOS, SARF, and SP (collectively, the “Berkshire Entities”). Each of the Berkshire Entities beneficially owns the shares. Seventh Berkshire Associates LLC, a

Massachusetts limited liability company (“7BA”), is the general partner of Fund VII and Fund VII-A. Stockbridge Associates LLC, a Delaware limited liability company (“SA”), is the general partner of SF, SARF and SOS. As of

December 31, 2015, the managing members of 7BA are Michael C. Ascione, Bradley M. Bloom, David C. Bordeau, Kenneth S. Bring, Jane Brock-Wilson, Kevin T. Callaghan, Christopher J. Hadley, Sharlyn C. Heslam, Elizabeth L. Hoffman, Matthew A.

Janchar, Ross M. Jones, Lawrence S. Hamelsky, Richard K. Lubin, Joshua A. Lutzker, Jonathan J. Meyer, Greg Pappas, Marni F. Payne, David R. Peeler, Anil Seetharam, Raleigh A. Shoemaker, Robert J. Small and Edward J. Whelan, Jr. (the

“Berkshire Principals”). Mr. Small is a director of the Company. Certain of the Berkshire Principals are also the managing members of Investors, Investors III and SA. The Berkshire Entities often make acquisitions in, and dispose of,

securities of an issuer on the same terms and conditions and at the same time. Berkshire Partners LLC, a Massachusetts limited liability company, is the investment adviser to Fund VII and Fund VII-A. |

The following table sets forth information regarding the beneficial ownership of Company common stock as of December 18, 2015 with respect to each

director and named executive officer of the Company and all directors and executive officers as a group. Except as indicated in the footnotes to this table and subject to applicable community property laws, the persons named in the table have sole

voting and investment power with respect to all shares of common stock listed as beneficially owned by them. None of the shares held by directors or executive officers are pledged. Unless

3

otherwise indicated in a footnote, the address for each individual listed below is c/o TransDigm Group Incorporated, 1301 East Ninth Street, Suite 3000, Cleveland, Ohio 44114.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Amount and Nature of Beneficially

Ownership(1) |

|

| Beneficial Owner |

|

Shares |

|

|

Shares Subject

to Options

Currently

Exercisable or

Exercisable

within 60 Days |

|

|

Total

Number

of

Shares |

|

|

Percentage

of Class |

|

| William Dries |

|

|

1,013 |

|

|

|

4,790 |

|

|

|

5,803 |

|

|

|

* |

|

| Mervin Dunn |

|

|

2,143 |

|

|

|

17,690 |

|

|

|

19,833 |

|

|

|

* |

|

| Michael Graff(2) |

|

|

28,087 |

|

|

|

1,790 |

|

|

|

29,877 |

|

|

|

* |

|

| Sean P. Hennessy |

|

|

15,717 |

|

|

|

17,690 |

|

|

|

33,407 |

|

|

|

* |

|

| W. Nicholas Howley(3) |

|

|

26,735 |

|

|

|

786,700 |

|

|

|

813,435 |

|

|

|

1.49 |

% |

| Raymond F. Laubenthal(4) |

|

|

166,938 |

|

|

|

215,000 |

|

|

|

381,938 |

|

|

|

* |

|

| Douglas W. Peacock(5) |

|

|

3,787 |

|

|

|

17,690 |

|

|

|

21,477 |

|

|

|

* |

|

| Robert J. Small(6) |

|

|

2,771,100 |

|

|

|

7,292 |

|

|

|

2,778,392 |

|

|

|

5.17 |

% |

| John Staer |

|

|

91 |

|

|

|

3,390 |

|

|

|

3,481 |

|

|

|

* |

|

| Terrance Paradie(7) |

|

|

5,000 |

|

|

|

22,400 |

|

|

|

27,400 |

|

|

|

* |

|

| Robert Henderson |

|

|

15,000 |

|

|

|

206,400 |

|

|

|

221,400 |

|

|

|

* |

|

| Kevin Stein(8) |

|

|

13,000 |

|

|

|

39,600 |

|

|

|

52,600 |

|

|

|

* |

|

| Gregory Rufus |

|

|

11,000 |

|

|

|

140,000 |

|

|

|

151,000 |

|

|

|

* |

|

| All directors and executive officers as a group (20 persons)(9) |

|

|

3,109,459 |

|

|

|

2,086,807 |

|

|

|

5,196,266 |

|

|

|

9.30 |

% |

| (1) |

Includes shares of which the listed beneficial owner is deemed to have the right to acquire beneficial ownership under Rule 13d-3 under the Securities Exchange Act, as amended (the “Exchange

Act”), within 60 days of December 18, 2015. The number of shares outstanding used in calculating the percentage of beneficial ownership for each person listed below includes the shares underlying options held by such persons that are

exercisable within 60 days of December 18, 2015, but excludes shares underlying options held by any other person. Percentage of ownership is based on 53,758,120 shares of common stock of the Company outstanding as of December 18, 2015.

|

| (2) |

Includes 3,382 shares held by Mr. Graff as the trustee of certain trusts created for the benefit of his minor children and 16,096 shares held by a trustee of a trust created by

Mr. Graff’s wife for the benefit of their children. Also includes 269 shares which are beneficially owned by Warburg Pincus and as to which Mr. Graff disclaims beneficial interest, except to the extent of his pecuniary interest therein.

|

| (3) |

Includes options to purchase 18,924 shares that are held by Bratenahl Capital Partners, Ltd (“Bratenahl”). By virtue of his indirect ownership interest in Bratenahl, Mr. Howley may

be deemed to be the beneficial owner (within the meaning of Rule 13d-3 under Exchange Act) of the options that are owned by Bratenahl. Mr. Howley disclaims beneficial ownership of all options owned by Bratenahl and reported herein as

beneficially owned except to the extent of any pecuniary interest therein. |

| (4) |

Includes 36,669 shares held in trust for the benefit of Mr. Laubenthal’s children. Mr. Laubenthal does not have any direct voting or dispositive power over the trust or economic

interest therein and therefore, disclaims beneficial ownership. |

| (5) |

Includes 3,000 shares held in trust by Mr. Peacock’s wife as trustee. Mr. Peacock does not have any direct voting or dispositive power over the trust or economic interest therein,

and, therefore, disclaims beneficial ownership. |

| (6) |

Includes 2,711,047 held by entities related to Berkshire Partners LLC (see footnote (5) above). Mr. Small disclaims beneficial ownership of all shares owned or controlled by the Berkshire

entities except to the extent of any pecuniary interest therein. Also includes 6,113 shares held by Mr. Small as trustee over which he has voting power but does not have any economic interest. |

| (7) |

Includes 4,700 shares of restricted stock, subject to forfeiture if Mr. Paradie is no longer employed by the Company. The risk of forfeiture will lapse (i.e., the stock will “vest”) as to

1,566 shares on April 22, 2016, as to 1,566 shares on April 22, 2017 and as to 1,567 shares on April 22, 2018. |

| (8) |

Includes 13,000 shares of restricted stock, subject to forfeiture if Mr. Stein is no longer employed by the Company. The risk of forfeiture will lapse (i.e., the stock will “vest”) as to

4,333 shares on December 31, 2015, as to 4,333 shares on December 31, 2016 and as to 4,334 shares on December 31, 2017. |

| (9) |

Includes shares subject to options exercisable within 60 days of December 18, 2015. Includes (i) 3,382 shares held by Mr. Graff as trustee and 16,096 held by a trustee of a trust created

by Mr. Graff’s wife and 269 shares which are beneficially owned by Warburg Pincus and as to which Mr. Graff disclaims beneficial interest, except to the extent of his pecuniary interest therein (see footnote (2)), (ii) 18,924 options

to purchase shares of common stock, which Mr. Howley may be deemed to beneficially own by virtue of his indirect ownership interest in Bratenahl (see footnote (3)), (iii) 36,669 shares held in trust for the benefit of

Mr. Laubenthal’s children (see footnote (4)), (iv) 3,000 shares held by Mr. Peacock’s wife as trustee of a trust (see footnote (5)), (v) shares held by entities related to Berkshire Partners LLC and 6,113 shares held by

Mr. Small as trustee (see footnote (6)), (vi) 4,700 shares of restricted stock held by Mr. Paradie, which are subject to forfeiture (see footnote (7)), (vii) 13,000 shares of restricted stock held by Mr. Stein, which are subject to forfeiture

(see footnote (8)), (viii) 26,578 shares held in trust for the benefit of the children of James Skulina, Executive Vice President. |

4

PROPOSAL ONE: ELECTION OF DIRECTORS

The total number of directors is fixed at nine. The Board of Directors was formerly divided into three classes of directors, with each class elected to

a three-year term. However, at the 2014 annual stockholders’ meeting, the Board was declassified, such that directors whose terms are expiring are now elected for one-year terms. The Board will be fully declassified by the 2017 annual

stockholders’ meeting. At this annual meeting, the terms of six directors are expiring. Unless you specify otherwise, the shares of common stock represented by your proxy will be voted to re-elect Messrs. Dries, Dunn, Graff, Howley, Small and

Laubenthal. The six nominees receiving the most votes will be elected as directors. If elected, each nominee will serve as a director for a one-year term and until his successor is duly elected and qualified.

If for any reason any of the nominees is not a candidate when the election occurs (which is not expected), the Board intends that proxies will be voted

for the election of a substitute nominee designated by the Board as recommended by the Nominating and Corporate Governance Committee. The following information is furnished with respect to each director (including the six nominees).

|

|

|

|

|

| Name and Basic Information |

|

Business Experience |

|

Qualifications |

| WILLIAM DRIES, age 64 Director 2016 Director Nominee

Director Since:

2011 Other Public Company

Director Positions: NN Inc. –

Nasdaq listed manufacturer of precision bearing

and metal components (serves as audit committee

chair)

Formerly a director of Polypore International, Inc. –

NYSE listed manufacturer of polymer-based

membranes (through August 2015) |

|

Retired Senior Vice President and Chief Financial Officer of EnPro Industries, Inc., a manufacturer of

engineered industrial products (2002-2011) Formerly with United Dominion Industries, Inc. and

Ernst & Young Licensed as a certified public accountant (currently on inactive

status). |

|

As a certified public accountant and the former chief financial officer of two public companies, both engaged in manufacturing highly engineered industrial

products, and as director and audit committee member of another public company, Mr. Dries’ finance background and public company experience is valuable to the Company and provides additional financial depth to the audit committee.

Mr. Dries’ acquisitions and international experience is also beneficial to the Company. |

| MERVIN DUNN, age 62 Director 2016 Director

Nominee Director

Since: 2007 Other

Pubic Company Director Positions: Not currently a director of any public company

Formerly director of Commercial Vehicle Group,

Inc. – NASDAQ-listed supplier of systems for the

commercial vehicle market (through May 2013) |

|

President and Chief Executive Officer of

Merv Dunn Management & Consulting, LLC, a private management consulting company since 2013

Co-Chairman of the Board of Futuris Group of Companies Ltd, a privately-held Australian automotive supplier since 2013

Retired Chief Executive Officer of Commercial Vehicle Group, Inc., a NASDAQ-listed supplier of

systems for the commercial vehicle market (1999 – 2013) |

|

As former CEO of Commercial Vehicle Group,

Mr. Dunn brings to the Board his extensive acquisition experience and experience with domestic and international management of an engineered product business, as well as his experience being the chief executive officer of a public company, all

of which are useful to the Board. |

5

|

|

|

|

|

| Name and Basic Information |

|

Business Experience |

|

Qualifications |

| MICHAEL GRAFF, age 64 Director 2016 Director

Nominee Director

Since: 2003 Other

Public Company Director Positions: Builders FirstSource, Inc. - NASDAQ-listed

manufacturer and distributor

Formerly a director of Polypore International, Inc. –

NYSE-listed manufacturer of polymer-based

membranes (through August 2015) |

|

Member and Managing Director of Warburg Pincus LLC and General Partner of

Warburg Pincus & Co., a private equity firm, since 2003 Formerly President and Chief

Operating Officer of Bombardier Aerospace, an aerospace manufacturer |

|

Mr. Graff brings to the Board a knowledge of acquisitions and capital market transactions and significant public company board experience, both acquired through his positions with Warburg

Pincus. Additionally, with his aerospace industry experience, and his previous management consulting background at McKinsey, Mr. Graff’s industry and management perspective is valuable to the Company. |

| SEAN HENNESSY, age 58 Director

Director Since: 2006

Other Public Company Director Positions:

None |

|

Chief

Financial Officer of The Sherwin Williams Company, a manufacturer and distributor of coatings and related products, since 2001

Certified public accountant |

|

As a certified public accountant and CFO of

a public company engaged in manufacturing, Mr. Hennessy’s finance background and public company experience is valuable to the Company and critical for his service on the Company’s Board and as chair of the Audit

Committee. |

| W. NICHOLAS HOWLEY, age 63 Chief Executive Officer, President and Chairman of the Board

2016 Director Nominee

Director Since:

2003 Other Public Company

Director Positions: Not currently a director of any public company

Formerly director of Polypore International, Inc.

- NYSE-listed manufacturer of polymer-based

membranes (through November 2012)

Formerly director of Satair A/S, a Danish public

company that is an aerospace distributor, including

a distributor of the Company’s products (through

October 2011) |

|

Chairman of

the Board of Directors since 2003 Co-founder of TransDigm Inc. and President and/or Chief

Executive Officer of the Company since its inception in 2003 and of TransDigm Inc. since December 1998 |

|

As a cofounder of the Company,

Mr. Howley brings to the Board an extensive understanding of the Company’s business. As the long-standing President and/or CEO of the Company and TransDigm Inc., Mr. Howley has played an integral role in the Company’s

establishment and implementation of its core value drivers on an ongoing basis and in its rapid and strategic growth. |

| RAYMOND LAUBENTHAL, age 54 Director 2016

Director Nominee

Director Since: 2015

Other Public Company Director Positions:

None |

|

Retired

President and COO of the Company (2005-2014) Formerly an employee of TransDigm Inc. or its

subsidiaries since its inception in 1993 |

|

As a long-time management employee of the

Company, Mr. Laubenthal brings to the Board an intimate knowledge of the company and industry. In addition, Mr. Laubenthal’s continued involvement with the Company through Board service will benefit the Company if it has a need for

his expertise on any special projects (none of which are anticipated at this time). |

6

|

|

|

|

|

| Name and Basic Information |

|

Business Experience |

|

Qualifications |

| DOUGLAS PEACOCK, age 77

Director

Director Since:

2003 Other Public

Company Director Positions: None |

|

Co-founder of TransDigm Inc.

Chairman of TransDigm Inc., 1993 - 2003

CEO of TransDigm Inc., 1993 - 2001

President of TransDigm Inc., 1993 - 1998 |

|

As a cofounder of the Company and retired CEO and Chairman of TransDigm Inc., with prior diverse and lengthy experience as senior management at a broad range of engineered products companies,

Mr. Peacock brings to the Board an extensive understanding of the Company’s business. |

| ROBERT SMALL, age 49 Director 2016 Director

Nominee Director

Since: 2010 Other

Public Company Director Positions: None |

|

Managing

Director of Berkshire Partners LLC, a private equity investment firm, since 2000 (having joined the firm in 1992)

Managing Director of Stockbridge Partners LLC, a specialized investment group affiliated with Berkshire focused on marketable securities, since its inception in

2007 |

|

Mr. Small brings to the Board a

knowledge of acquisitions and capital market transactions, based on more than 20 years of experience in the private equity industry, as well as a breadth of board experience. Mr. Small is or has been a director of several of Berkshire’s

portfolio companies, including having previously served as director of Hexcel Corporation, a composite materials producer primarily for aerospace applications, which is publicly traded on the NYSE. |

| JOHN STAER, age 64 Director

Director Since: 2012

Other Public Company Director Positions:

Dalhoff Larsen & Horneman A/S, a Danish public

company that is a supplier of timber and wood

products

Ambu A/S, a Danish public company that is a

manufacturer of hospital and rescue service

equipment (through December 2015) |

|

Retired

Chief Executive Officer of Satair A/S, a subsidiary of Airbus (“Satair”), and a distributor of aerospace products, including parts manufactured by subsidiaries of the Company, from 1993 - 2013 |

|

Through 2013, Mr. Staer was CEO of

Satair A/S when it was a public company in Denmark and then as a subsidiary of Airbus. Satair is a distributor of aerospace products, including parts manufactured by subsidiaries of the Company. In addition, Mr. Staer has prior experience has a

CFO. Mr. Staer is a valuable addition to the board of directors because of his industry experience, international experience (including extensively in Europe and the Pacific Rim), mergers and acquisitions experience and finance background and

experience as a public company board member. |

|

| |

|

The Board of Directors recommends that the stockholders vote FOR the

nominees for election set forth above. Proxies will be voted FOR election of the

nominees unless otherwise specified.

|

The Nominating and Corporate Governance Committee recommends

potential director candidates to the Board. In making its recommendations, consistent with the Committee charter, the Committee considers independence, as well as diversity, age, strategic and financial skills and experience, in the context of the

needs of the Board as a whole. The Committee’s charter requires the selection of prospective Board members with personal and professional integrity who have

7

demonstrated appropriate ability and judgment and whom the Committee believes will be effective, in conjunction with the other Board members, in collectively serving the long-term interests of

the Company and its stockholders. There are no other stated criteria for director nominees, and the Committee considers other factors as it deems appropriate in the best interests of the Company and its stockholders. Other than the consideration of

diversity as one factor to be considered in recommending a nominee consistent with the Committee’s charter, the Committee does not have a policy specifically focused on diversity.

The Committee identifies nominees by first evaluating current Board members willing to continue in service. If any Board member does not wish to

continue to serve or if the Committee or Board decides not to nominate a member for re-election, then the Committee identifies the desired skills and experience in light of the criteria outlined above. The Committee then establishes potential

director candidates from recommendations from the Board, senior management, stockholders and third parties. The Committee may retain a search consultant to supplement potential Board candidates if it deems it advisable.

As reflected on the previous pages, each Board member was chosen to be a director nominee because the Board and Committee believe that he demonstrated

leadership experience, specific industry or manufacturing experience and experience with capital market transactions. Every director holds or has held executive positions in organizations that have provided him with experience in management and

leadership development. The Board and the Committee believe that these skills and qualifications, combined with each director’s diverse background and ability to work in a positive and collegial fashion, benefit the Company and its stockholders

by creating a strong and effective Board.

The Committee will consider stockholder suggestions concerning qualified candidates for election as

directors. To recommend a prospective nominee for the Committee’s consideration for the 2017 annual meeting, a stockholder must submit the candidate’s name and qualifications to the Company’s Secretary, Halle Fine Terrion, at the

following address: TransDigm Group Incorporated, 1301 East Ninth Street, Suite 3000, Cleveland, Ohio 44114 between November 5, 2016 and December 5, 2016. The Committee has not established specific minimum qualifications a candidate must

have in order to be recommended to the Board. However, in determining qualifications for new directors, the Committee will consider potential members’ independence, as well as diversity, age, skill and experience in the context of the

Board’s needs.

DIRECTOR COMPENSATION

Mr. Howley, the only director who is also an employee of the Company, does not receive any director fees.

Compensation for non-employee directors was as follows:

| |

• |

|

An annual retainer fee of $60,000, with such fee being paid, at the option of each director, either in cash or shares of the Company’s common stock, paid semi-annually in arrears. No additional Board or committee

meeting fees will be paid. |

| |

• |

|

An additional retainer of $15,000 to the chairman of the Audit Committee, paid semi-annually in arrears. |

| |

• |

|

An additional retainer of $5,000 to the chairmen of the Compensation and Nominating and Governance Committees, paid semi-annually in arrears. |

In addition, in 2014, the Company made a grant of stock options to each director valued at $300,000 on a Black Scholes basis covering compensation for

fiscal 2014 and fiscal 2015, granted on the same

8

terms and conditions as those granted to Company employees, which vests over five years. The terms of the options are discussed in greater detail under “Executive Compensation – Equity

Based Incentives – Options.” Directors must maintain equity in the Company (i.e., stock or vested in-the-money options) equal to at least $150,000.

In addition, pursuant to an agreement entered into in 1999 between TransDigm Inc. and Mr. Peacock, TransDigm Inc. is obligated to provide

Mr. Peacock and his wife with medical and dental insurance coverage comparable to what they were receiving at the time of Mr. Peacock’s retirement. In light of the Company’s transition to self-insurance, in 2007, TransDigm Inc.

and Mr. Peacock agreed that TransDigm Inc. would satisfy its obligations under the 1999 agreement by paying for Mr. Peacock’s Medicare and dental insurance coverage, Mrs. Peacock’s medical and dental insurance coverage, and

supplemental medical reimbursement coverage for both Mr. and Mrs. Peacock, less the amount of any Company employee portion of the premium under the Company’s self-insurance program as if Mr. and Mrs. Peacock were covered

under those benefit plans. TransDigm Inc. also agreed to retain a health insurance consultant to assist Mr. and Mrs. Peacock in evaluating coverage and handling the administrative burden of the Medicare and insurance enrollment process at

the outset and thereafter managing claims issues. These payments are made on a “grossed-up” basis for federal income tax purposes, but no gross-up payment related to fiscal 2015 has yet been made. The cost of coverage and related services

under these arrangements in fiscal 2015 was $12,914 and the cost of the gross-up payment for 2014, paid in January 2015, was $9,124.

The following

table sets forth the compensation paid to the Company’s non-employee directors during 2015:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Name |

|

Fees Earned or Paid in

Cash

($)(2) |

|

|

Stock Awards ($)(2) |

|

|

Option Awards ($) |

|

|

All Other

Compensation ($)(3) |

|

|

Total ($) |

|

| William Dries |

|

|

314 |

|

|

|

59,686 |

|

|

|

-- |

|

|

|

22,400 |

|

|

|

82,400 |

|

| Mervin Dunn |

|

|

314 |

|

|

|

59,686 |

|

|

|

-- |

|

|

|

22,400 |

|

|

|

82,400 |

|

| Michael S. Graff |

|

|

5,314 |

|

|

|

59,686 |

|

|

|

-- |

|

|

|

22,400 |

|

|

|

87,400 |

|

| Sean P. Hennessy |

|

|

15,314 |

|

|

|

59,686 |

|

|

|

-- |

|

|

|

22,400 |

|

|

|

97,400 |

|

| Raymond Laubenthal(1) |

|

|

314 |

|

|

|

59,686 |

|

|

|

-- |

|

|

|

-- |

|

|

|

60,000 |

|

| Douglas W. Peacock |

|

|

65,000 |

|

|

|

— |

|

|

|

-- |

|

|

|

44,438 |

|

|

|

109,438 |

|

| Robert J. Small |

|

|

60,000 |

|

|

|

— |

|

|

|

-- |

|

|

|

22,400 |

|

|

|

82,400 |

|

| John Staer |

|

|

60,000 |

|

|

|

— |

|

|

|

-- |

|

|

|

22,400 |

|

|

|

82,400 |

|

| (1) |

Mr. Laubenthal does not receive any equity compensation for his service. In connection with his retirement, Mr. Laubenthal retained a portion of options previously granted to him in November 2012

with vesting scheduled in 2016 and 2017. |

| (2) |

Messrs. Dries, Dunn, Graff, Hennessy and Laubenthal elected to receive their semi-annual board retainer fees as stock. The shares were issued based on a value established on March 15, 2015 and

September 15, 2015, on which dates the last closing prices of the common stock on the New York Stock Exchange were $214.82 and $229.43, respectively. |

| (3) |

Represents amounts paid under the Company’s dividend equivalent plans described on pages 20 and 21. Also includes $22,038 for Mr. Peacock, constituting the net amounts paid to or on

behalf of Mr. Peacock or his wife for medical insurance coverage or medical claims pursuant to the agreement between Mr. Peacock and TransDigm Inc. described above. |

CORPORATE GOVERNANCE

Corporate Governance Guidelines

The Board of Directors has adopted Corporate Governance Guidelines, which guide it in the performance of its responsibilities to serve the best interests

of the Company and its stockholders. A copy of the Corporate Governance Guidelines is posted on the Company’s website, www.transdigm.com, under “Investor Relations—Corporate Governance” and is available to any stockholder

in writing upon request to the Company. The Board reviews the Corporate Governance Guidelines periodically.

9

Codes of Ethics & Whistleblower Policy

We are committed to integrity and ethical behavior and have adopted a Code of Ethics for Senior Financial Officers, a Code of Business Conduct and Ethics

and a Whistleblower Policy. Each of these documents is posted on the Company’s website, www.transdigm.com, under “Investor Relations—Corporate Governance” and is available to any stockholder in writing upon request to the

Company.

Code of Ethics for Senior Financial Officers. We have a Code of Ethics for Senior Financial Officers that applies to the chief

executive officer, chief operating officer, chief financial officer, division presidents, controllers, treasurer and manager of internal audit (collectively, “Senior Financial Officers”). This code requires Senior Financial Officers

to: act with honesty and integrity; endeavor to provide information that is full, fair, accurate, timely and understandable in all reports and documents that the Company files with, or submits to, the SEC and other public filings or communications

made by the Company; endeavor to comply with all laws, rules and regulations of federal, state and local governments and all applicable private or public regulatory agencies; not knowingly or recklessly misrepresent material facts or allow their

independent judgment to be compromised; not use for personal advantage confidential information acquired in the course of their employment; proactively promote ethical behavior among peers and subordinates in the workplace; and promptly report any

violation or suspected violation of the code to the Audit Committee. Only the Audit Committee or the Board may waive a provision of the code with respect to a Senior Financial Officer. Any such waiver, or any amendment to the code, will be promptly

disclosed on the Company’s website and as otherwise required by rule or regulation. There were no such waivers in 2015.

Code of Business

Conduct and Ethics. We also have a Code of Business Conduct and Ethics that reflects the Company’s commitment to honesty, integrity and the ethical behavior of Company employees, officers and directors. The code governs the actions,

interactions and working relationships of Company employees, officers and directors with customers, fellow employees, competitors, government and self-regulatory agencies, investors, the public, the media, and anyone else with whom the Company has

contact. The code sets forth the expectation that employees, officers and directors will conduct business legally and addresses conflict of interest situations, protection and use of Company assets, corporate opportunities, fair dealing,

confidentiality and reporting of illegal or unethical behavior. Only the Board or the Nominating and Corporate Governance Committee may waive a provision of the code with respect to an executive officer or director. Any such waiver will be promptly

disclosed on the Company’s website and as otherwise required by rule or regulation. There were no such waivers in 2015.

Whistleblower

Policy. The purpose of the Whistleblower Policy is to encourage employees to disclose alleged wrongdoing that may adversely impact the Company, its customers or stockholders, fellow employees or the public, without fear of retaliation. The

policy sets forth procedures for reporting alleged financial and non-financial wrongdoing on a confidential and anonymous basis, a process for investigating reported acts of alleged wrongdoing and a policy of non-retaliation. Reports may be made

directly to the CFO, Audit Committee or Convercent, a third party service retained on behalf of the Audit Committee. The Audit Committee chair receives notices of complaints and oversees investigation of complaints of financial wrongdoing.

Board Composition

The Board of

Directors was formerly divided into three classes, but was declassified in 2014. Directors appointed or elected after March 2014 were not and will not be put into a class and will serve until the next annual election of directors. The directors who

are standing for election this year will be elected for one-year terms. The entire Board will be declassified as of the 2017 annual meeting, at which all director will be elected for one-year terms.

10

The Company’s amended and restated certificate of incorporation and bylaws provide that the number of

directors shall be fixed from time to time by a resolution of the majority of its Board of Directors. The number of directors is currently fixed at nine.

Independence of Directors

Currently, all of the directors, other than Messrs. Howley and Laubenthal, are

“independent directors” within the meaning of the NYSE’s listing standards. In determining that Mr. Staer is independent, the Board considered Mr. Staer’s relationship with Satair and Satair’s relationship to the

Company, as well as the former relationship between Mr. Howley and Satair. In determining that Mr. Peacock is independent, the Board considered the insurance arrangement between Mr. Peacock and the Company described in this proxy

statement under “Director Compensation.” We do not have separate criteria for determining independence, different from the NYSE listing standards. The Board of Directors reviews periodically the relationships that each director or nominee

has with the Company (either directly or as a partner, stockholder or officer of an organization that has a relationship with the Company). Those directors or nominees whom the Board affirmatively determines have no material relationship with the

Company (either directly or as a partner, stockholder or officer of an organization that has a relationship with the Company) that would preclude independence as specified in the listing standards of the NYSE will be considered independent.

Board Leadership Structure

The

Board leadership structure is comprised of a combined Chief Executive Officer and Chairman of the Board. The Board believes that combining the function of CEO and Chairman is appropriate for the Company because it ensures that the Board focuses on

important strategic objectives and understands challenges facing the Company in its day-to-day operations. This combined role is balanced by the independence of the other directors and the role of the presiding director described below.

The Board uses a presiding director, who is an independent director that leads executive sessions of the non-management directors. The Board designates

the presiding director at each meeting on a rotating basis.

Board Self-Evaluation

The Board and each of the Audit Committee, Compensation Committee and Nominating and Corporate Governance Committee conducts a self-evaluation annually.

Board’s Role in Risk Management Oversight

The Board oversees the process of risk management. Management regularly communicates with the Board regarding the Company’s risk exposure and its

efforts to monitor and mitigate such risks. Specifically, the Company’s executive officers meet annually to discuss the material risks facing the Company and ways to mitigate those risks. Management then provides a summary of its findings to

the Board and the Board reviews and discusses such risks at a regularly scheduled Board meeting.

Board Meetings

The Board held four meetings in fiscal 2015. Each director attended more than 75% of the aggregate number of meetings of the Board and committees on

which he served in fiscal 2015. The Board does not hold a meeting on the date of the Company’s annual stockholder meeting and the

11

Company has not established a policy regarding director attendance at the stockholder meeting. One director attended the 2015 annual stockholder meeting; no stockholders attended the meeting in

person. After each meeting of the Board, non-management directors meet independently of the CEO and Chairman. In fiscal 2015, non-management directors met in executive session after each regularly scheduled Board meeting. The independent directors

met in executive session three times.

Board Committees

The Board of Directors has an Executive Committee, a Nominating and Corporate Governance Committee, an Audit Committee and a Compensation Committee. The

members of the committees are as set forth in the following table:

The Executive Committee possesses the power of the Board of Directors in the management of the Company’s

business and affairs during intervals between Board meetings. The Executive Committee

12

held no formal meetings during fiscal 2015, although it did act by unanimous written consent. Details regarding the responsibilities and meetings of the other committees are set forth below.

|

|

|

|

|

NOMINATING &

CORPORATE GOVERNANCE

COMMITTEE |

|

AUDIT COMMITTEE |

|

COMPENSATION

COMMITTEE |

| Committee

Responsibilities: The Committee:

• oversees & assists the Board in identifying

& recommending nominees for election as directors;

• recommends to the Board qualifications for committee membership, structure & operation;

• recommends to the Board directors to service on

each committee; • develops & recommends to

the Board corporate governance policies & procedures;

• provides oversight with respect to corporate governance & ethical conduct;

• leads the Board in its annual performance

review; • oversees the Company’s

succession planning. |

|

Committee

Responsibilities: The Committee:

• oversees issues regarding accounting &

financial reporting processes & audits of the Company’s financial statements.

• assists the Board in monitoring the integrity of the Company’s financial statements, compliance with legal &

regulatory requirements, independent auditor’s qualifications & independence, & the performance of the Company’s internal audit function & independent auditors;

• assumes direct responsibility for the

appointment, compensation, retention & oversight of the work of the Company’s independent auditors;

• provides a venue for consideration of matters relating to audit issues. |

|

Committee Responsibilities:

The Committee:

• discharges the Board’s responsibilities relating to compensation of Company executives;

• oversees the Company’s compensation &

employee benefit plans and practices; • has

sole discretion concerning administration of the Company’s stock option plans, including selection of individuals to receive awards, types of awards, the terms & conditions of the awards & the time at which awards will be granted, other

than awards to directors, which are approved by the full Board. |

| Committee

Independence: Each Committee member is

independent under NYSE listing

standards |

|

Committee

Independence: Each Committee member is independent under NYSE listing standards and as

such term is defined in Rule 10A-3(b)(1). |

|

Committee Independence:

Each Committee member is independent under NYSE listing standards, a “non-employee director” as defined in Section 16(b) of the Securities Exchange Act of 1934

and an “outside director” as defined in Section 162(m) of the Internal Reveue Code. In determining independence, the Board affirmatively determined that none of the Committee members has a relationship with the Company that is material to

his ability to be independent from management in connection with his duties on the Committee. |

| Number of meetings in

FY’15: |

|

Number of meetings in FY’15: |

|

Number of meetings in FY’15: |

|

4 |

|

8

|

|

7

|

13

Stockholder Communication with Board of Directors

Any stockholder or other interested party who desires to communicate with any of the members of the Board of Directors may do so electronically by

sending an email to ir@transdigm.com. Alternatively, an individual may communicate with the members of the Board by writing to the Company, c/o Investor Relations, TransDigm Group Incorporated, 1301 East Ninth Street, Suite 3000, Cleveland,

Ohio 44114. Communications may be addressed to an individual director, a Board committee, the independent directors or the full Board of Directors. Communications received by Investor Relations will be distributed to the appropriate directors.

Solicitations for the sale of merchandise, publications or services of any kind will not be forwarded to the directors.

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS

The Board of Directors reviews and must approve all related party transactions.

Proposed transactions between the Company and related persons (as defined in Regulation S-K Item 404 under the Securities Act of 1933) are submitted to the full Board for consideration. The relationship of the parties and the terms of the

proposed transaction are reviewed and discussed by the Board and the Board may approve or disapprove the Company entering into the transaction. All related party transactions, whether or not those transactions must be disclosed under Regulation S-K

Item 404, are approved by the Board pursuant to the policy.

EXECUTIVE COMPENSATION

Executive Compensation Discussion and Analysis

The Compensation Committee determines compensation of the Company’s executive officers. The primary goal in determining executive compensation is to

provide a competitive total compensation package that enables the Company to attract and retain qualified executives and create a strong incentive to increase the Company’s equity value. In light of this goal, the Committee compensates

executive officers based on their responsibilities and the Company’s performance. The primary components of the Company’s executive compensation program are base salaries, bonuses and performance-based options and related dividend

equivalent payments, although the program is heavily weighted towards performance-based options and related dividend equivalents.

The Company has

its roots as a private equity portfolio company. As such, management’s cash compensation was typically set below the median of relevant peer groups but management had an opportunity to earn significant additional performance-based compensation

based on options/equity ownership in the Company. We believe this ownership mentality contributes significantly to incentivize and motivate management to create stockholder value. Therefore, we have continued to focus on compensation through

performance-based options targeted to vest upon attainment of financial and investment metrics at or above those of high-performing private equity funds. Specifically, this compensation philosophy aligns management and stockholders, with management

focused on creation of value through increasing EBITDA and cash generation and return of capital to stockholders. Because of the opportunity to realize a significant appreciation in the Company’s equity value via growth or special dividends, we

have historically provided, and intend to continue to provide, executives with cash compensation below the median cash compensation in the marketplace, based on our knowledge of compensation practices within the industry and publicly available

information.

The Committee has overall responsibility for establishing, implementing, and monitoring the executive compensation program for

executive officers. Mr. Howley recommends to the Committee, for its approval, salary and bonus amounts and option awards for all officers other than himself. The Committee reviews Mr. Howley’s recommendations and ultimately determines

the salary, bonus and option award, if applicable. The Committee has historically determined Mr. Howley’s salary and bonus amounts without his input. Generally, individual performance, company performance, market conditions and other

factors are considered in determining compensation. The Committee generally does not consider the tax or accounting treatment of items of compensation in structuring its compensation packages, except that it makes an effort to ensure that any

deferred compensation is compliant with Section 409A of the Internal Revenue Code.

14

Financial Performance and Highlights*

As background, fiscal 2015 was another good year for the Company. Set forth below are highlights of 2015 performance that impacted the Compensation

Committee’s decisions. It was this performance that was considered in making compensation decisions, including bonuses, relating to 2015 performance.

| |

• |

|

Acquisitions. We acquired six operating units in four different transactions for a total purchase price of approximately $1.6 billion, the biggest year for acquisitions to date.

|

| |

• |

|

Increase in net sales. Fiscal 2015 net sales rose 14.1% to $2.7 billion. |

| |

• |

|

Increase in adjusted net income. Fiscal 2015 adjusted net income, excluding expenses related to acquisitions, non-cash stock compensation, refinancing and other non-recurring charges

rose 15.2% to $510 million, or $9.01 per share. |

| |

• |

|

Increase in EBITDA as defined. Fiscal 2015 “EBITDA As Defined” rose 15% to $1.23 billion. “EBITDA As Defined” as a percentage of net sales was approximately 46%

for the year. This “EBITDA As Defined” margin excluding the dilutive impact from the acquisitions purchased in fiscal 2014 and 2015 was 48%, up 1.5 percentage points on a year over year basis. |

| |

• |

|

Effective capital allocation. We generated significant cash flow from operating activities, and also raised approximately $2 billion in new debt, using about half of the proceeds to

fund the acquisitions and the balance to extend maturities and lower interest rates on existing debt. |

| |

• |

|

Strong operating strategy. This strong financial performance was achieved due to management’s continued focus on our value-based operating strategy despite continuing to

integrate the three operating units purchased in fiscal 2014 and beginning the integration of the six operating units purchased in fiscal 2015. |

| |

• |

|

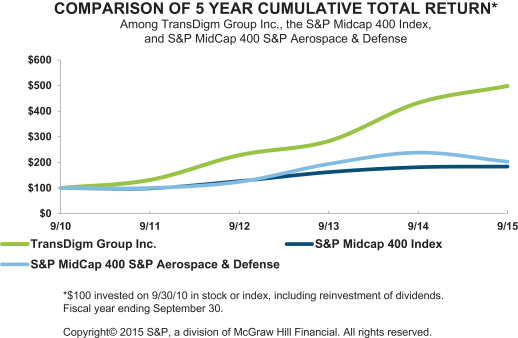

Exceptional stock performance. In addition, in fiscal 2015, the Company significantly outperformed the S&P Midcap 400 and the S&P Midcap 400 S&P Aerospace &

Defense indices over fiscal 2015, as well as over a five-year period, as demonstrated in the graph below. Total stockholder return over the five-year period was 439%. Total return to stockholders in last twelve months was 15%. |

| * |

Adjusted net income, EBITDA and EBITDA As Defined are non-GAAP measures. For a reconciliation of net income to adjusted net income, EBITDA and EBITDA As Defined, please see our Report on Form 10-K.

|

15

Our long-term performance has been excellent and has resulted in outstanding returns to stockholders. As

shown in the graph above, our five-year total stockholder return significantly exceeds its peers. Part of this return reflects the payment to its stockholders of $59.85 per share in dividend payments to stockholders over the five-year period, for an

aggregate $3.2 billion return of capital to stockholders over the five-year period. Dividends are just one example of how we create value for stockholders. With few acquisition opportunities that met our strategic and value-creation criteria in

2014, we returned about $1.6 billion to shareholders in the form of a large special dividend and also a modest share buyback. In contrast, in 2015, we allocated about $1.6 billion to acquisitions as highlighted above. The comparison of capital

allocation in the last two years highlights our flexible value-focused strategy.

The Board commended the management team’s leadership in

connection with the Company’s performance as compared to its peers in a recovering market and especially while continuing to aggressively pursue the Company’s long-term value drivers. The Committee believes that the Company’s

activities in 2015 created significant value for Company stockholders during 2015 and in the long-term.

Executive Summary

2015 Compensation Committee Actions

The Committee took routine actions during 2015, including granting options and approving annual salaries and bonuses, consistent with past practices.

Additionally, the Committee granted restricted stock in order to attract Messrs. Stein and Paradie to employment with the Company and the Committee approved some immaterial amendments to employment agreements for executive officers, primarily to

abolish the executives’ entitlement to subsidized COBRA payments following employment. See “Employment Agreements” beginning on page 32 for further information.

Recent Developments Following Fiscal Year End

On December 10, 2015, the Committee approved, and the Company and Mr. Howley entered into, a Fourth Amended and Restated Employment Agreement.

The Employment Agreement replaced Mr. Howley’s Third Amended and Restated Employment Agreement dated August 28, 2014, as amended in October 2015. The primary purpose of the amendments contained in the Employment Agreement as compared

to the prior employment agreement was to provide Mr. Howley with equity compensation in lieu of cash compensation for salary and bonus. Mr. Howley will receive $7,000 in cash annually to pay for his employee co-premium for health benefits,

however his annual salary and incentive award, traditionally paid in cash, will be converted to grants of performance-based options.

Mr. Howley initially expressed his willingness and desire to enter into such an arrangement based on his confidence in the Company’s long-term

business plan and the increased alignment that would result between himself and Company stockholders. The Committee engaged Veritas Executive Compensation Consultants to help it consider such an arrangement. Veritas provided information regarding

other companies whose executives have forgone cash compensation and noted the advantages to the Company would be that it would replace guaranteed compensation with at-risk performance-based equity, that it would show an increased commitment to and

alignment with Company stockholders and that it would improve the Company’s cash flow. Veritas advised that it would be appropriate to have an equity risk premium in the range of 15-50% added to the compensation because of the additional risk

associated with equity as opposed to cash. The Committee and Mr. Howley agreed that in determining the amount of Mr. Howley’s award, which is

16

calculated based on a Black Scholes valuation with contractually fixed assumptions as described under “Employment Agreements”, the Company would use a 37.5% equity risk premium, which

was at the higher end of the Veritas range because Mr. Howley would be receiving performance vested options as opposed to stock or time vested options.

See “Employment Agreements – Employment Agreement with Mr. Howley, Chief Executive Officer” on pages 32-35 for further information

and a more complete description of the equity compensation arrangement.

Elements of the Executive

Compensation Program

Equity Based Incentives

Performance-Based Stock Options

We intend that the largest portion of management’s potential earnings be based on total stockholder return. We believe that performance-based stock

option grants are, and will continue to be, a valuable motivating tool and provide a long-term incentive to management. Performance-based stock option grants reinforce the long-term goal of increasing stockholder value and yielding returns

comparable to or higher than well-performing private equity funds by aligning the interests of the Company’s stockholders and management. We only grant options that vest upon performance targets and do not grant options that merely vest based

on the passage of time.

Other than to the CEO, who gets annual grants pursuant to his employment agreement, the Committee does not make annual

grants of options to employees. Rather, it grants options that vest over five years in connection with hirings, promotions and the assumption of increased responsibilities. Thereafter, unless there has been an intervening five year award because of

a promotion, for management other than the CEO, the Company grants biennial extension awards that vest in the fourth and fifth year following the award. These grants are generally made in the third year of vesting under the initial award so that the

employee always has four or five years of future option vesting in order to promote maximizing long-term value. Because of proxy advisory firms’ difficulty in analyzing the swings in CEO compensation related to biennial awards, in 2014, for

ease of understanding, the Committee determined that the CEO would receive annual option awards commencing in fiscal 2015. However, for the other named executive officers (and historically for the CEO), the pattern of option awards means that the

annual compensation in the Summary Compensation Table increases and decreases biennially.

Company stock options vest based on the achievement of

specific performance-based targets. Initial options vest annually over five years based on the achievement of annual targets and two-year extension options vest up to 50% in the fourth fiscal year after the grant and up to 50% in the fifth year

after the grant based on the achievement of performance targets. Commencing with options awarded in fiscal 2015, options awarded to Mr. Howley in fiscal 2015 will vest at the end of the fifth fiscal year following the date of grant; options

awarded to Mr. Howley in fiscal 2016 and 2017 will vest at the end of the fourth fiscal year following the date of grant; and options awarded to Mr. Howley in fiscal 2018 and 2019 will vest at the end of the third fiscal year following the

date of grant.

All options vest based on the achievement of an annual performance target. In all cases, the targets are set to require cumulative

growth over the applicable multi-year period. Through these performance-based options with five year performance periods, we believe we have optimized management incentive to drive stockholder value creation over the long term and appropriately

linked compensation with Company performance.

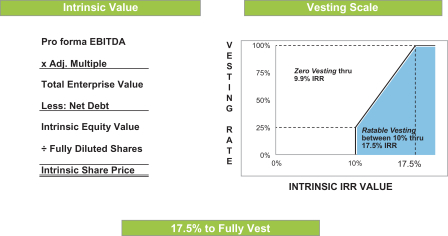

At the time of grant, per share targets representing an intrinsic share price, as described below,

are set by taking the prior year’s annual operational performance and increasing such amount by 10% and 17.5%, respectively, to establish the minimum and maximum targets. In other words, as

17

demonstrated in the chart on the following page, the intrinsic share price must grow at a compound annual growth rate of 10% for any vesting to even occur at all; for 100% vesting,

the intrinsic share price must grow at a compound annual growth rate of 17.5%. Targets are thus robust, requiring 17.5% compound annual growth from the most recently completed year for maximum vesting. Targets were set with a 17.5%

compound annual growth rate in an effort to achieve growth at or above the long-term returns of top performing private equity funds, with the hope that market growth will reflect the Company’s intrinsic growth. This is consistent with our

objective of providing stockholders with returns at or above those of well-performing private equity funds. If these returns are achieved, both investors and management benefit significantly.

Annual targets are calculated based on a ratio of (a) the excess of (i) the product of EBITDA (as defined in the Company’s credit agreement) and an

acquisition-weighted market multiple over (ii) net debt to (b) the Company’s number of diluted shares as of such date based on the treasury stock method of accounting (the “operational performance per diluted share”). The

targets are adjusted for dividends. To simplify, option targets and vesting are basically calculated as follows:

Annual operating performance, as reflected above, takes into consideration the following:

| |

• |

|

management of capital structure; |

| |

• |

|

acquisition performance, including the acquisition price paid; and |

| |

• |

|

the impact of option dilution on common shares outstanding. |

We use growth in intrinsic value of its equity as the

performance-based metric for a number of reasons:

| |

• |

|

It focuses management on the fundamentals of stockholder value creation— i.e., EBITDA, cash generation, capital structure management and return of capital, as appropriate. |

| |

• |

|

This is the basic private equity formula for value that the senior and operational management team has focused on achieving since its inception since 1993. |

| |

• |

|

Over the long term, we believe that market value will generally follow intrinsic value. |

As described above, our

long-term objective is to give its stockholders well performing, private equity-like returns. We believe that this metric aligns management with that goal. In order to get to 17.5%

18

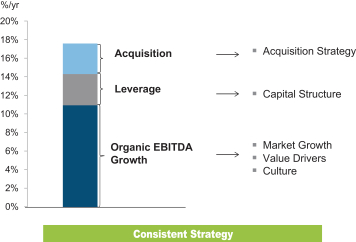

growth, we must focus on underlying business operations, capital structure and utilization and growth through acquisitions. Generally, and on average, we plan to achieve our growth target as

follows:

We believe this option target performance criteria, taking into account many aspects of the Company’s

performance without focusing on a single measure, is unique—eliminating the need for several different metrics—and achieves an unusually high level of pay-for-performance alignment by emphasizing long-term stockholder value.

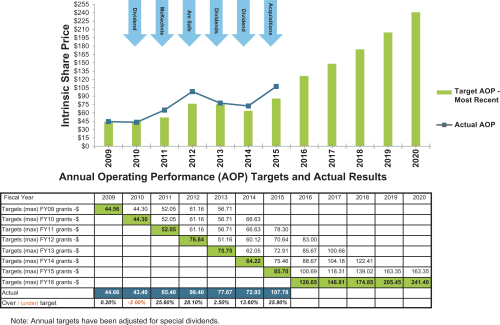

Specifically, historical and future targets under the option plan, and actual performance through fiscal 2015, are set forth in the table below.

Targets are set, and options vest, over five year periods. The few years in which our actual performance has far exceeded our option targets followed significant well-performing acquisitions, such as our acquisitions of McKechnie for $1.3 billion in

the beginning of fiscal 2011 and of AmSafe for $750 million in the middle of fiscal 2012 (in addition to the other $382 million of acquisitions in fiscal 2011 and $118 million of acquisitions in fiscal 2012) and our four acquisitions totaling $1.6

billion in 2015.

19

Targets have been adjusted for the $3.6 billion aggregate ($67.50 per share) dividends paid to stockholders over the

performance periods. The Committee believes the adjustments were appropriate and necessary to account for the early return to stockholders because if a portion of the investment is returned early via special dividend or return of capital, the

subsequent years’ targets must be adjusted to reflect the revised capital structure and maintain the same IRR-based performance requirements. Adjustment of the targets did not make the targets any easier to achieve but rather maintained the IRR

targets.

Because we view our performance on a long-term basis and the targets are set to achieve long-term compound annual and cumulative growth,

if the annual performance per share exceeds the maximum target in an applicable year, such excess may be treated as having been achieved in the following two fiscal years and/or the prior two fiscal years (without duplication) if less than the full

amount of options would otherwise have vested for such years. This allows management to focus on long-term value without having to make short-term decisions to maximize vesting in a particular year. We believe this feature acts similarly to

long-term incentive plans that take into account performance over a multi-year period. We also believe this plan feature mitigates compensation risk, because if performance were measured in only one-year “snap-shot” increments, management

could be incentivized to sacrifice longer term goals to achieve vesting in the short term.

Our long-term performance has been outstanding. Over

five years, the Company has exceeded its goal to achieve an intrinsic compound annual growth rate of 17.5% and has met or exceeded its option targets in four of the last five years. In that same period, total stockholder return has been 439%.

In addition to vesting based on operational targets, in the event of a change in control, performance vesting options become fully vested. No option

agreements provide for any gross up to any payments that would be deemed to be “excess parachute payments” under Section 280G of the Internal Revenue Code in connection with the acceleration of options upon a change in control.

The options also have an alternate market-based performance measurement, such that if, beginning in the second fiscal year following the date of grant,

the price of the Company’s common stock on the NYSE exceeds two times the exercise price of the options less dividends paid since the date of grant, then, to the extent that the options did not otherwise vest in accordance with their terms, the

options may vest 50% in the fourth fiscal year from the date of grant and 50% in the fifth fiscal year from the date of grant (or if such market price is achieved in the fifth year, 100% may vest in the fifth fiscal year); but vesting of the options

will not accelerate as compared to their original vesting schedule.

Option agreements for executive officers provide that if the officer’s