UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

PURSUANT

TO SECTION 13 OR 15(d) OF THE

SECURITIES

EXCHANGE ACT OF 1934

Date

of Report (Date of earliest event reported)

February

3, 2016

Annaly

Capital Management, Inc.

(Exact

Name of Registrant as Specified in its Charter)

|

Maryland

|

|

1-13447

|

|

22-3479661

|

|

(State

or Other Jurisdiction

Of

Incorporation)

|

|

(Commission

File

Number)

|

|

(I.R.S.

Employer

Identification

No.)

|

|

1211

Avenue of the Americas

New

York, New York

|

|

10036

|

|

(Address

of Principal

Executive

Offices)

|

|

(Zip

Code)

|

Registrant’s

telephone number, including area code: (212) 696-0100

(Former

Name or Former Address, if Changed Since Last Report)

Check the

appropriate box below if the Form 8-K filing is intended to

simultaneously satisfy the filing obligation of the registrant under any

of the following provisions:

⃞

Written

communications pursuant to Rule 425 under the Securities Act (17 CFR

230.425)

⃞

Soliciting

material pursuant to Rule 14a-12 under the Exchange Act (17 CFR

240.14a-12)

⃞

Pre-commencement

communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR

240.14d-2(b))

⃞

Pre-commencement

communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR

240.13e-4(c))

Item 7.01. Regulation FD Disclosure

Annaly Capital Management, Inc. (the “Company”) hereby furnishes the

information set forth in the presentation (the “Presentation”) attached

hereto as Exhibit 99.1, which is incorporated herein by reference.

The

Presentation is being furnished pursuant to Item 7.01, and the

information contained therein shall not be deemed “filed” for the

purposes of Section 18 of the Securities Exchange Act of 1934, as

amended (the “Exchange Act”), or otherwise subject to the liabilities of

that section, nor shall it be deemed incorporated by reference in any

filing under the Securities Act of 1933, as amended, or the Exchange

Act, except as shall be expressly set forth by specific reference in

such filing.

The Presentation contains statements that, to the

extent they are not recitations of historical fact, constitute

“forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995 (the “Reform Act”). All such

forward-looking statements are intended to be subject to the safe harbor

protection provided by the Reform Act. Actual outcomes and results could

differ materially from those forecast due to the impact of many factors

beyond the control of the Company. All forward looking statements

included in the Presentation are made only as of the date of the

Presentation and are subject to change without notice. Certain factors

that could cause actual results to differ materially from those

contained in the forward-looking statements are included in the

Company’s periodic reports filed with the SEC. Copies are available on

the SEC’s website at www.sec.gov. The Company disclaims any obligation

to update its forward looking statements unless required by law.

Item

9.01 Financial Statements and Exhibits

(d) Exhibits

99.1 Presentation

by Annaly Capital Management, Inc.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the

Registrant has duly caused this report to be signed on its behalf by the

undersigned hereunto duly authorized.

|

|

|

ANNALY CAPITAL MANAGEMENT, INC.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

By:

|

/s/ Glenn A. Votek

|

|

|

|

|

|

Name:

|

Glenn A. Votek

|

|

|

|

|

Title:

|

Chief Financial Officer

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dated:

|

February 3, 2016

|

|

|

|

|

February 2016 Investor

Presentation

1 Safe Harbor This

Presentation contains statements that, to the extent they are not

recitations of historical fact, constitute “forward-looking statements”

within the meaning of the Private Securities Litigation Reform Act of

1995 (the “Reform Act”). All such forward-looking statements are

intended to be subject to the safe harbor protection provided by the

Reform Act. Actual outcomes and results could differ materially from

those forecast due to the impact of many factors beyond the control of

the Company. All forward looking statements included in this

Presentation are made only as of the date of this Presentation and are

subject to change without notice. Certain factors that could cause

actual results to differ materially from those contained in the

forward-looking statements are included in the Company’s periodic

reports filed with the SEC. Copies are available on the SEC’s website at

www.sec.gov. The Company disclaims any obligation to update its forward

looking statements unless required by law.

2 Introduction & Macro

Overview

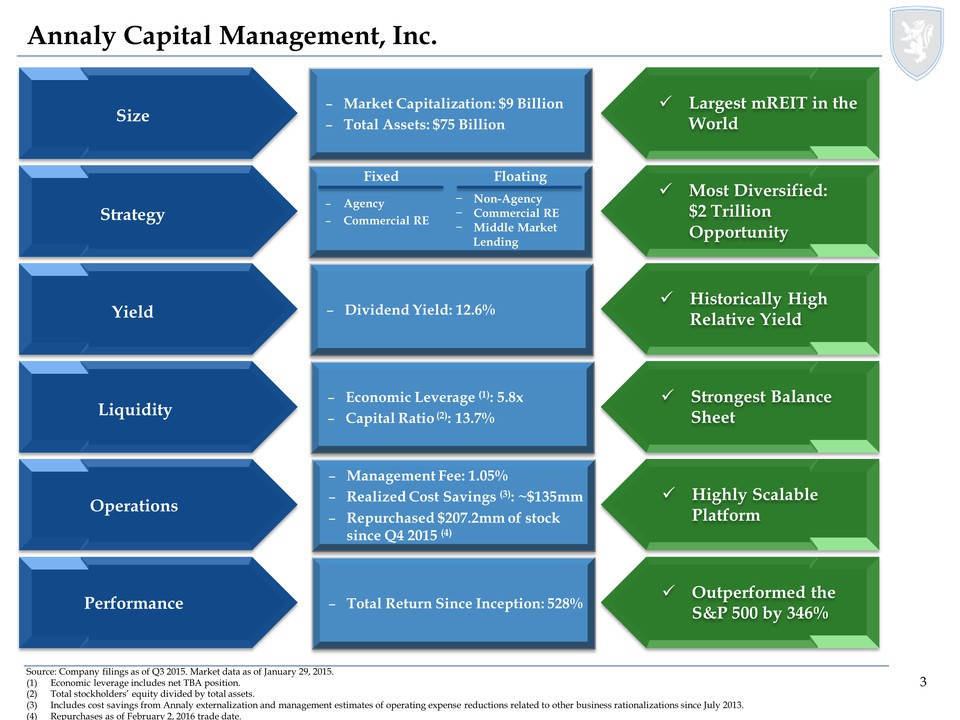

3 Historically High

Relative Yield Strongest Balance Sheet Highly Scalable Platform

Outperformed the S&P 500 by 346% Most Diversified: $2 Trillion

Opportunity Largest mREIT in the World Annaly Capital Management, Inc.

Size Strategy Yield Liquidity Operations Performance Source: Company

filings as of Q3 2015. Market data as of January 29, 2015. (1)Economic

leverage includes net TBA position. (2)Total stockholders’ equity

divided by total assets. (3)Includes cost savings from Annaly

externalization and management estimates of operating expense reductions

related to other business rationalizations since July 2013.

(4)Repurchases as of February 2, 2016 trade date. –Dividend Yield: 12.6%

–Economic Leverage (1): 5.8x –Capital Ratio (2): 13.7% –Management Fee:

1.05% –Realized Cost Savings (3): ~$135mm –Repurchased $207.2mm of stock

since Q4 2015 (4) –Total Return Since Inception: 528% –Agency

–Commercial RE –Market Capitalization: $9 Billion –Total Assets: $75

Billion −Non-Agency −Commercial RE −Middle Market Lending Fixed Floating

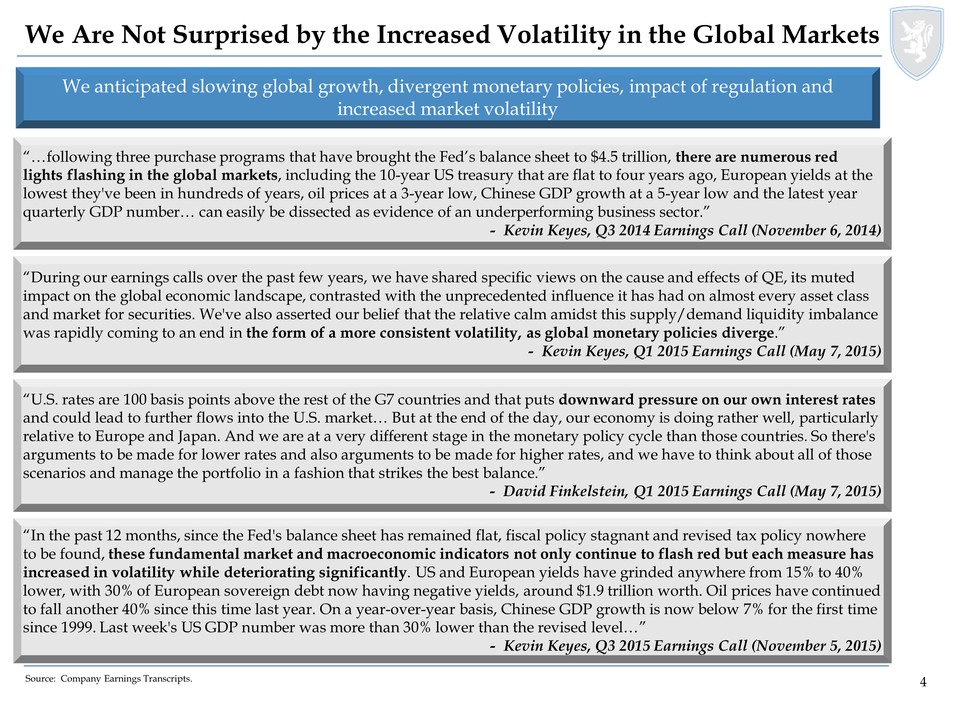

4 We Are Not Surprised by

the Increased Volatility in the Global Markets We anticipated slowing

global growth, divergent monetary policies, impact of regulation and

increased market volatility “In the past 12 months, since the Fed's

balance sheet has remained flat, fiscal policy stagnant and revised tax

policy nowhere to be found, these fundamental market and macroeconomic

indicators not only continue to flash red but each measure has increased

in volatility while deteriorating significantly. US and European yields

have grinded anywhere from 15% to 40% lower, with 30% of European

sovereign debt now having negative yields, around $1.9 trillion worth.

Oil prices have continued to fall another 40% since this time last year.

On a year-over-year basis, Chinese GDP growth is now below 7% for the

first time since 1999. Last week's US GDP number was more than 30% lower

than the revised level…” - Kevin Keyes, Q3 2015 Earnings Call (November

5, 2015) “…following three purchase programs that have brought the Fed’s

balance sheet to $4.5 trillion, there are numerous red lights flashing

in the global markets, including the 10-year US treasury that are flat

to four years ago, European yields at the lowest they've been in

hundreds of years, oil prices at a 3-year low, Chinese GDP growth at a

5-year low and the latest year quarterly GDP number… can easily be

dissected as evidence of an underperforming business sector.” - Kevin

Keyes, Q3 2014 Earnings Call (November 6, 2014) “U.S. rates are 100

basis points above the rest of the G7 countries and that puts downward

pressure on our own interest rates and could lead to further flows into

the U.S. market… But at the end of the day, our economy is doing rather

well, particularly relative to Europe and Japan. And we are at a very

different stage in the monetary policy cycle than those countries. So

there's arguments to be made for lower rates and also arguments to be

made for higher rates, and we have to think about all of those scenarios

and manage the portfolio in a fashion that strikes the best balance.” -

David Finkelstein, Q1 2015 Earnings Call (May 7, 2015) “During our

earnings calls over the past few years, we have shared specific views on

the cause and effects of QE, its muted impact on the global economic

landscape, contrasted with the unprecedented influence it has had on

almost every asset class and market for securities. We've also asserted

our belief that the relative calm amidst this supply/demand liquidity

imbalance was rapidly coming to an end in the form of a more consistent

volatility, as global monetary policies diverge.” - Kevin Keyes, Q1 2015

Earnings Call (May 7, 2015) Source: Company Earnings Transcripts.

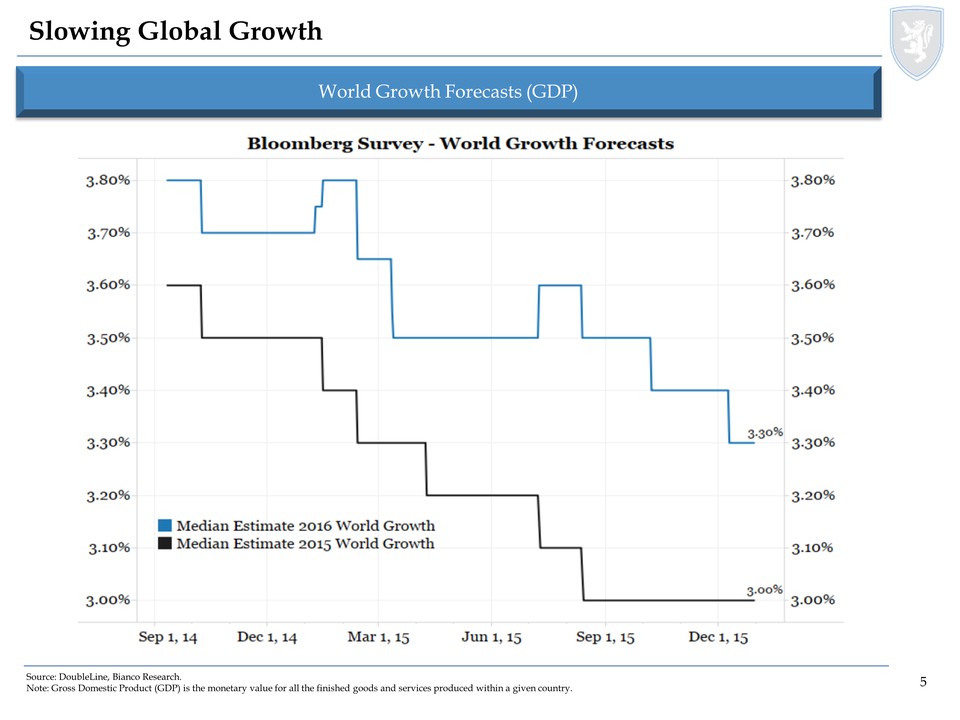

5 Source: DoubleLine,

Bianco Research. Note: Gross Domestic Product (GDP) is the monetary

value for all the finished goods and services produced within a given

country. Slowing Global Growth World Growth Forecasts (GDP) 3.80% 3.70%

3.60% 3.50% 3.40% 3.30% 3.20% 3.10% 3.00% Sep 1, 14 Dec 1, 14 Mar 1, 15

Jun 1, 15 Sep 1, 15 Dec 1, 15

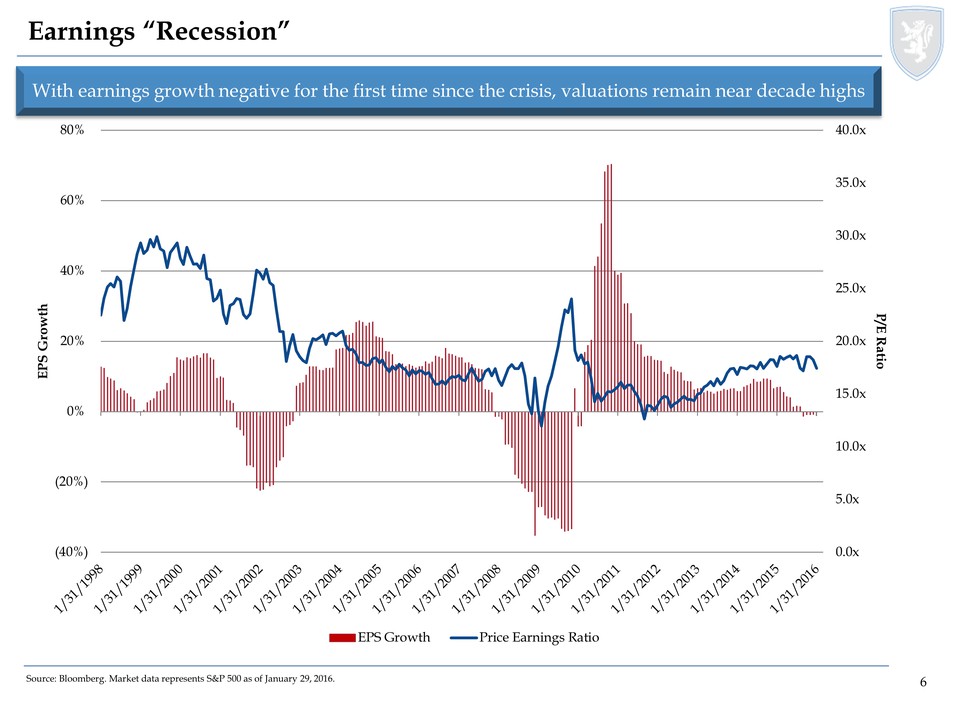

6 Source: Bloomberg. Market

data represents S&P 500 as of January 29, 2016. With earnings growth

negative for the first time since the crisis, valuations remain near

decade highs Earnings “Recession” 0.0x 5.0x 10.0x 15.0x 20.0x 25.0x

30.0x 35.0x 40.0x (40%) (20%) 0% 20% 40% 60% 80% P/E Ratio EPS Growth

EPS Growth Price Earnings Ratio 1/31/1998 1/31/1999 1/31/2000 1/31/2001

1/31/2002 1/31/2003 1/31/2004 1/31/2005 1/31/2006 1/31/2007 1/31/2008

1/31/2009 1/31/2010 1/31/2011 1/31/2012 1/31/2013 1/31/2014 1/31/2015

1/31/2016

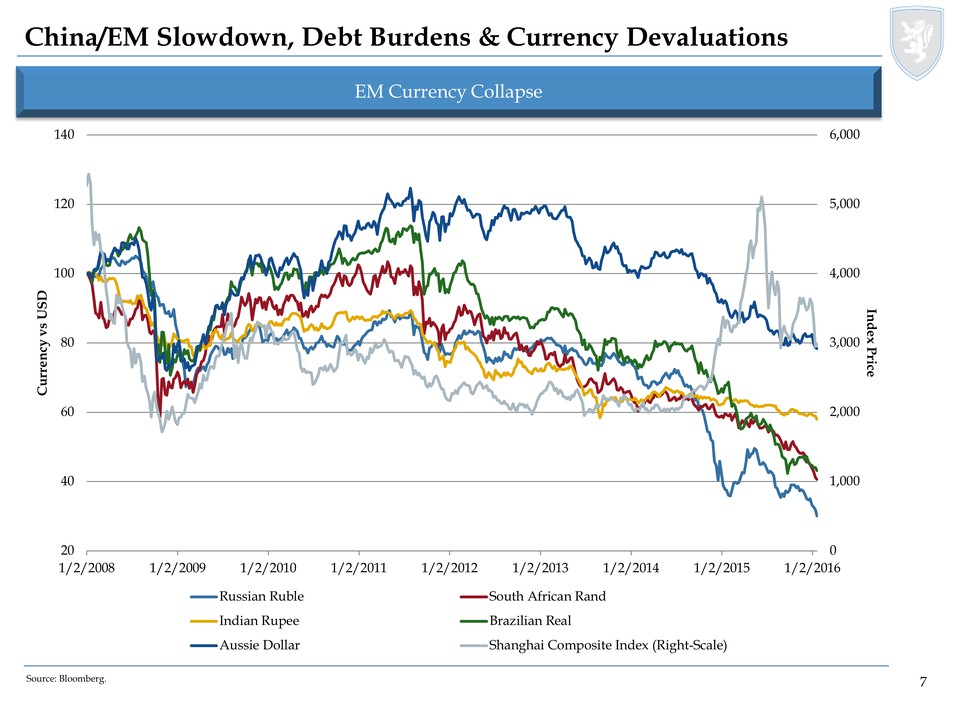

7 China/EM Slowdown, Debt

Burdens & Currency Devaluations EM Currency Collapse Source: Bloomberg.

0 1,000 2,000 3,000 4,000 5,000 6,000 20 40 60 80 100 120 140 1/2/2008

1/2/2009 1/2/2010 1/2/2011 1/2/2012 1/2/2013 1/2/2014 1/2/2015 1/2/2016

Index Price Currency vs USD Russian Ruble South African Rand Indian

Rupee Brazilian Real Aussie Dollar Shanghai Composite Index (Right-Scale)

8 Oil and Commodity

Collapse Signal Weakening Global Demand Commodity Prices (January 9,

1996 to January 11, 2016) Source: Bloomberg. Note: BCOM Commodity Index

is calculated on an excess return basis and reflects commodity futures

price movements with monthly rebalancing. You cannot invest directly in

an index. 240 220 200 180 160 140 120 100 60 ‘96’97 ’98 ’99 ’00 02 03 04

05 06 07 08 09 10 11 12 13 14 15 75.8560 237.9531 129.2791 74.2411 Last

Price High on 07/02/08 Average Low on 02/26/99

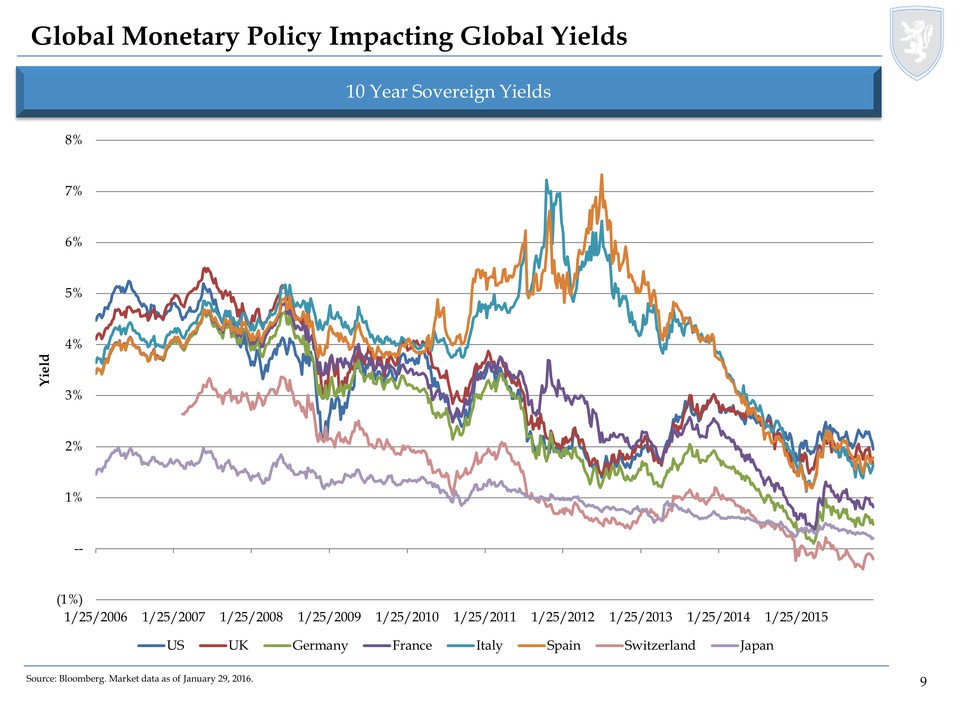

9 Global Monetary Policy

Impacting Global Yields 10 Year Sovereign Yields Source: Bloomberg.

Market data as of January 29, 2016. (1%) -- 1% 2% 3% 4% 5% 6% 7% 8%

1/25/2006 1/25/2007 1/25/2008 1/25/2009 1/25/2010 1/25/2011 1/25/2012

1/25/2013 1/25/2014 1/25/2015 Yield US UK Germany France Italy Spain

Switzerland Japan

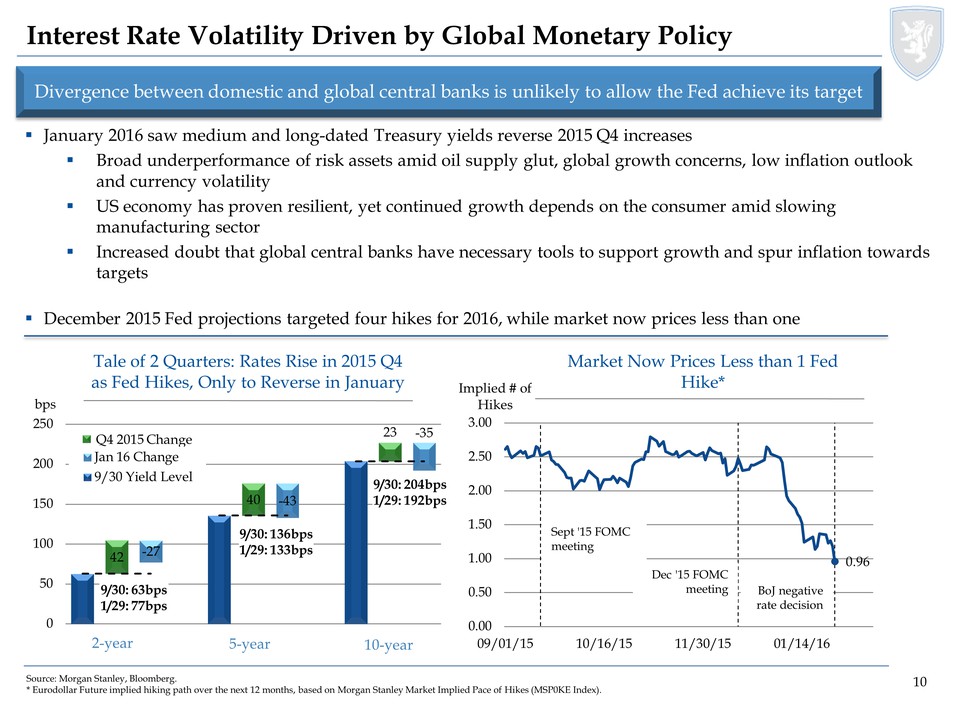

10 Source: Morgan Stanley,

Bloomberg. * Eurodollar Future implied hiking path over the next 12

months, based on Morgan Stanley Market Implied Pace of Hikes (MSP0KE

Index). Interest Rate Volatility Driven by Global Monetary Policy

January 2016 saw medium and long-dated Treasury yields reverse 2015 Q4

increases Broad underperformance of risk assets amid oil supply glut,

global growth concerns, low inflation outlook and currency volatility US

economy has proven resilient, yet continued growth depends on the

consumer amid slowing manufacturing sector Increased doubt that global

central banks have necessary tools to support growth and spur inflation

towards targets December 2015 Fed projections targeted four hikes for

2016, while market now prices less than one 0.96 0.00 0.50 1.00 1.50

2.00 2.50 3.00 09/01/15 10/16/15 11/30/15 01/14/16 Implied # of Hikes

Sept '15 FOMC meeting Dec '15 FOMC meeting BoJ negative rate decision 42

-27 40 -43 23 -35 0 50 100 150 200 250 bps Jan 16 Change 9/30 Yield

Level 2-year 5-year 10-year 9/30: 63bps 1/29: 77bps 9/30: 136bps 1/29:

133bps 9/30: 204bps 1/29: 192bps Q4 2015 Change Tale of 2 Quarters:

Rates Rise in 2015 Q4 as Fed Hikes, Only to Reverse in January Market

Now Prices Less than 1 Fed Hike* Divergence between domestic and global

central banks is unlikely to allow the Fed achieve its target

11 Annaly’s Positioning

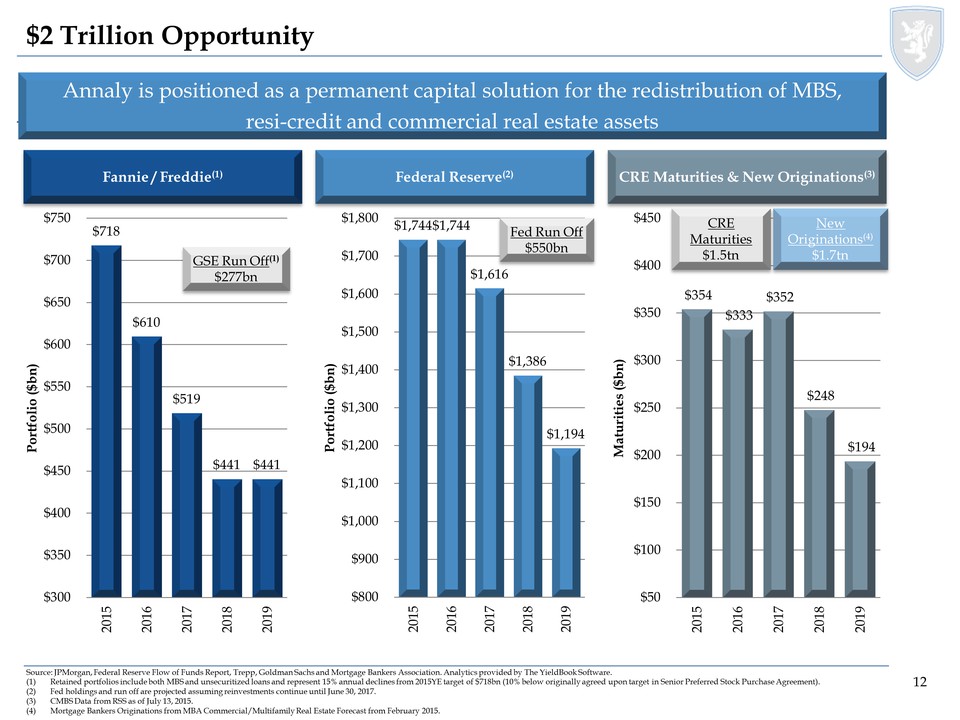

12 $1,744 $1,744 $1,616

$1,386 $1,194 $800 $900 $1,000 $1,100 $1,200 $1,300 $1,400 $1,500 $1,600

$1,700 $1,800 2015 2016 2017 2018 2019 Portfolio ($bn) $718 $610 $519

$441 $441 $300 $350 $400 $450 $500 $550 $600 $650 $700 $750 2015 2016

2017 2018 2019 Portfolio ($bn) $2 Trillion Opportunity Annaly is

positioned as a permanent capital solution for the redistribution of

MBS, resi-credit and commercial real estate assets Federal Reserve(2)

Fannie / Freddie(1) CRE Maturities & New Originations(3) Source:

JPMorgan, Federal Reserve Flow of Funds Report, Trepp, Goldman Sachs and

Mortgage Bankers Association. Analytics provided by The YieldBook

Software. (1)Retained portfolios include both MBS and unsecuritized

loans and represent 15% annual declines from 2015YE target of $718bn

(10% below originally agreed upon target in Senior Preferred Stock

Purchase Agreement). (2)Fed holdings and run off are projected assuming

reinvestments continue until June 30, 2017. (3)CMBS Data from RSS as of

July 13, 2015. (4)Mortgage Bankers Originations from MBA

Commercial/Multifamily Real Estate Forecast from February 2015. GSE Run

Off(1) $277bn Fed Run Off $550bn $354 $333 $352 $248 $194 $50 $100 $150

$200 $250 $300 $350 $400 $450 2015 2016 2017 2018 2019 Maturities ($bn)

CRE Maturities $1.5tn New Originations(4) $1.7tn

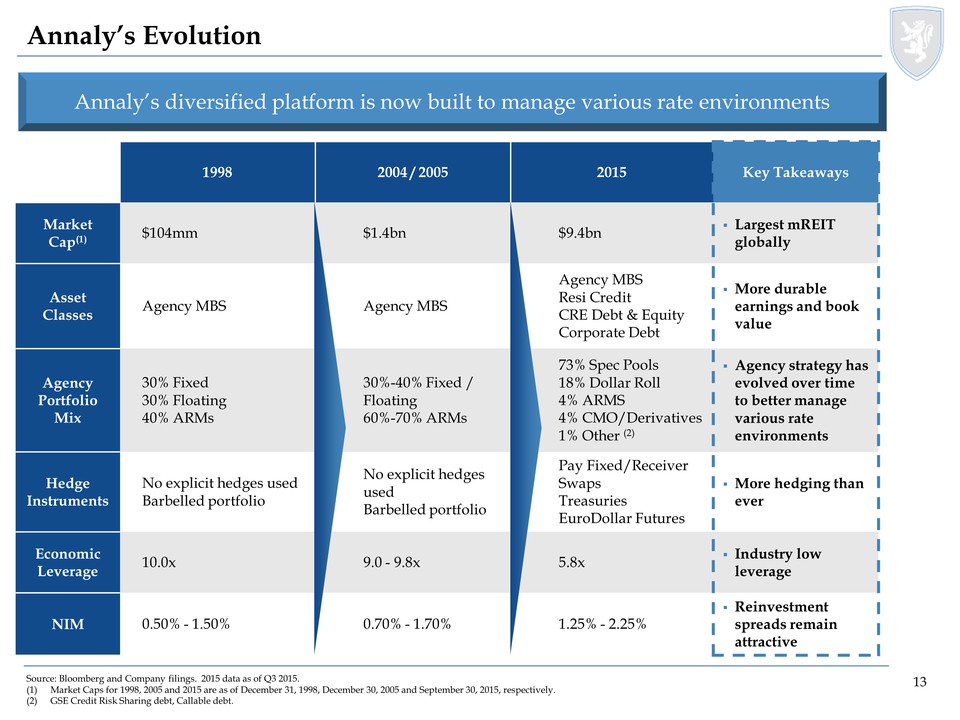

13 Source: Bloomberg and

Company filings. 2015 data as of Q3 2015. (1)Market Caps for 1998, 2005

and 2015 are as of December 31, 1998, December 30, 2005 and September

30, 2015, respectively. (2)GSE Credit Risk Sharing debt, Callable debt.

1998 2004 / 2005 2015 Key Takeaways Market Cap(1) $104mm $1.4bn $9.4bn

Largest mREIT globally Asset Classes Agency MBS Agency MBS Agency MBS

Resi Credit CRE Debt & Equity Corporate Debt More durable earnings and

book value Agency Portfolio Mix 30% Fixed 30% Floating 40% ARMs 30%-40%

Fixed / Floating 60%-70% ARMs 73% Spec Pools 18% Dollar Roll 4% ARMS 4%

CMO/Derivatives 1% Other (2) Agency strategy has evolved over time to

better manage various rate environments Hedge Instruments No explicit

hedges used Barbelled portfolio No explicit hedges used Barbelled

portfolio Pay Fixed/Receiver Swaps Treasuries EuroDollar Futures More

hedging than ever Economic Leverage 10.0x 9.0 - 9.8x 5.8x Industry low

leverage NIM 0.50% - 1.50% 0.70% - 1.70% 1.25% - 2.25% Reinvestment

spreads remain attractive Annaly’s Evolution Annaly’s diversified

platform is now built to manage various rate environments

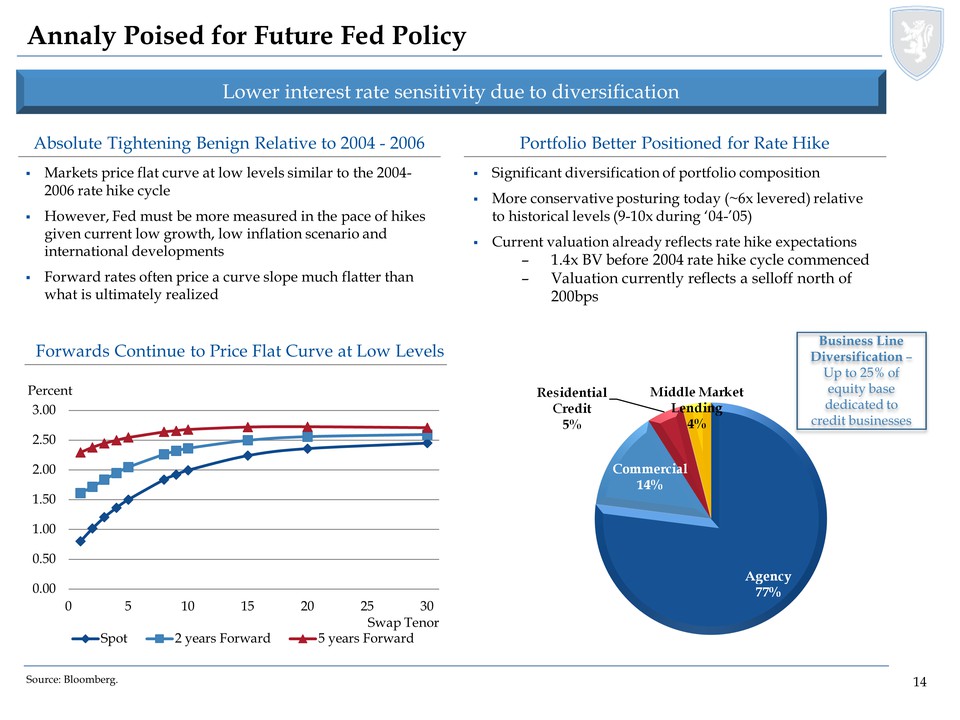

14 Absolute Tightening

Benign Relative to 2004 - 2006 Lower interest rate sensitivity due to

diversification Markets price flat curve at low levels similar to the

2004- 2006 rate hike cycle However, Fed must be more measured in the

pace of hikes given current low growth, low inflation scenario and

international developments Forward rates often price a curve slope much

flatter than what is ultimately realized Significant diversification of

portfolio composition More conservative posturing today (~6x levered)

relative to historical levels (9-10x during ‘04-’05) Current valuation

already reflects rate hike expectations – 1.4x BV before 2004 rate hike

cycle commenced – Valuation currently reflects a selloff north of 200bps

Agency 77% Commercial 14% Residential Credit 5% Middle Market Lending 4%

Portfolio Better Positioned for Rate Hike Annaly Poised for Future Fed

Policy Business Line Diversification – Up to 25% of equity base

dedicated to credit businesses 0.00 0.50 1.00 1.50 2.00 2.50 3.00 0 5 10

15 20 25 30 Percent Swap Tenor Spot 2 years Forward 5 years Forward

Forwards Continue to Price Flat Curve at Low Levels Source: Bloomberg.

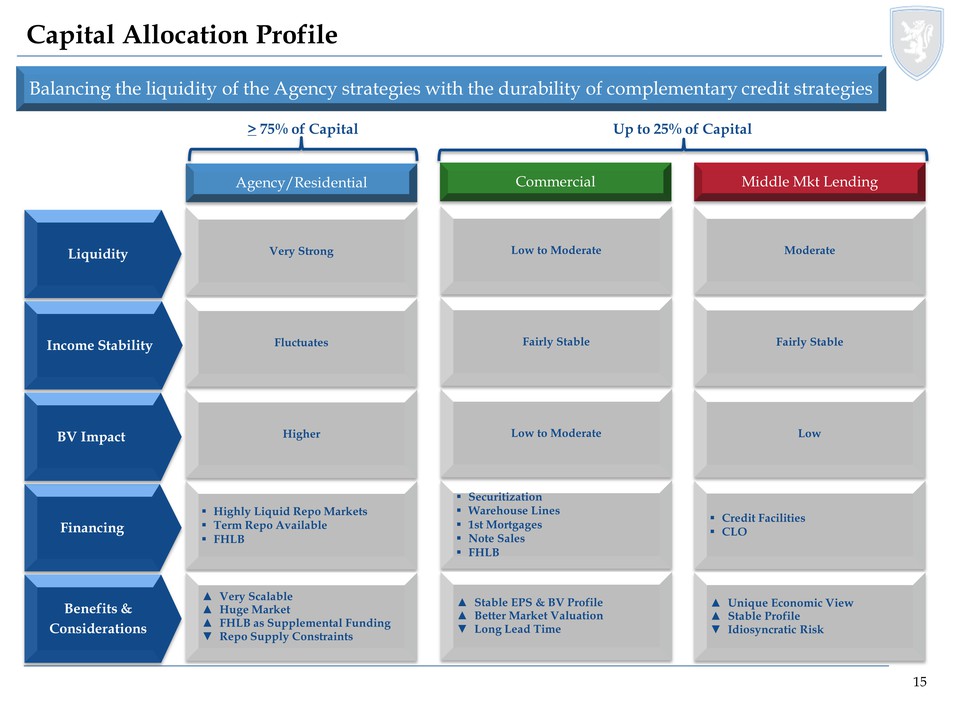

15 Agency/Residential

Commercial Middle Mkt Lending Financing Benefits &

Considerations Highly Liquid Repo Markets Term Repo Available FHLB Very

Scalable Huge Market FHLB as Supplemental Funding Repo Supply

Constraints Securitization Warehouse Lines 1st Mortgages Note

Sales FHLB Stable EPS & BV Profile Better Market Valuation Long Lead

Time Credit Facilities CLO Unique Economic View Stable Profile

Idiosyncratic Risk Liquidity Very Strong Low to Moderate Moderate

Benefits Higher Low to Moderate Low Fluctuates Fairly Stable Fairly

Stable Income Stability BV Impact Capital Allocation Profile > 75% of

Capital Up to 25% of Capital Balancing the liquidity of the Agency

strategies with the durability of complementary credit strategies

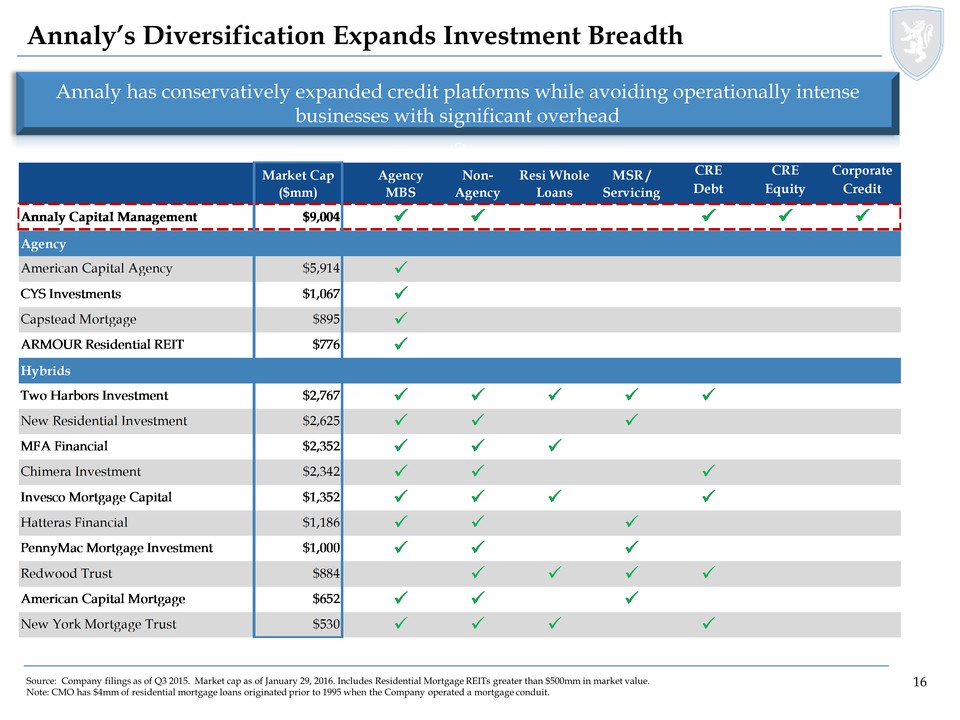

16 Annaly’s Diversification

Expands Investment Breadth Source: Company filings as of Q3 2015. Market

cap as of January 29, 2016. Includes Residential Mortgage REITs greater

than $500mm in market value. Note: CMO has $4mm of residential mortgage

loans originated prior to 1995 when the Company operated a mortgage

conduit. Annaly has conservatively expanded credit platforms while

avoiding operationally intense businesses with significant overhead

CRECRECorporateDebtEquityCreditAnnaly Capital Management$9,004

AgencyAmerican Capital Agency$5,914 CYS Investments$1,067 Capstead

Mortgage$895 ARMOUR Residential REIT$776 HybridsTwo Harbors

Investment$2,767 New Residential Investment$2,625 MFA Financial$2,352

Chimera Investment$2,342 Invesco Mortgage Capital$1,352 Hatteras

Financial$1,186 PennyMac Mortgage Investment$1,000 Redwood Trust$884

American Capital Mortgage$652 New York Mortgage Trust$530 Market Cap

($mm)MSR / ServicingAgency MBSNon-AgencyResi Whole Loans

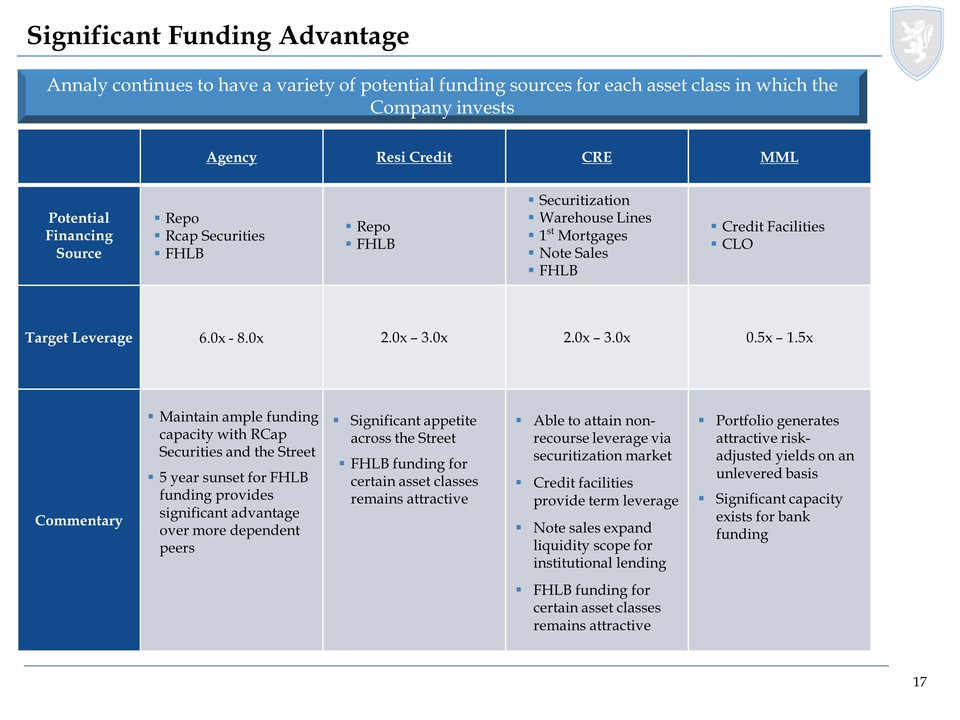

17 Significant Funding

Advantage Agency Resi Credit CRE MML Potential Financing

Source Repo Rcap

Securities FHLB Repo FHLB Securitization Warehouse Lines 1st

Mortgages Note Sales FHLB Credit Facilities CLO Target Leverage 6.0x

- 8.0x 2.0x – 3.0x 2.0x – 3.0x 0.5x – 1.5x Commentary Maintain ample

funding capacity with RCap Securities and the Street 5 year sunset for

FHLB funding provides significant advantage over more dependent

peers Significant appetite across the Street FHLB funding for certain

asset classes remains attractive Able to attain non-recourse leverage

via securitization market Credit facilities provide term leverage Note

sales expand liquidity scope for institutional lending FHLB funding for

certain asset classes remains attractive Portfolio generates attractive

risk-adjusted yields on an unlevered basis Significant capacity exists

for bank funding Annaly continues to have a variety of potential funding

sources for each asset class in which the Company invests

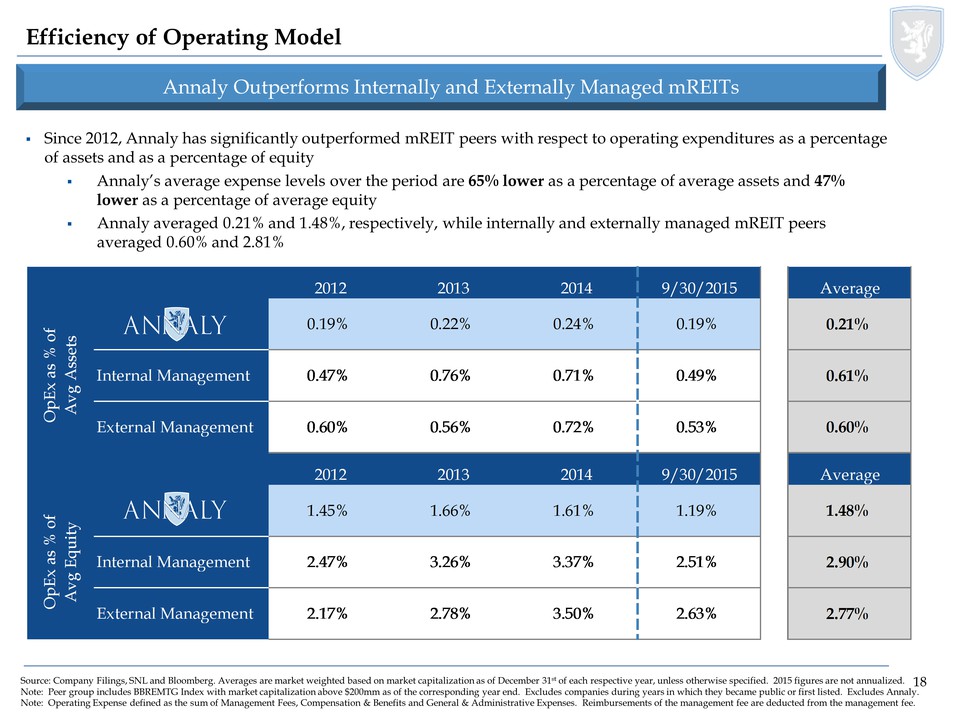

18 2012 2013 2014 9/30/2015

Average 0.19% 0.22% 0.24% 0.19% 0.21% Internal Management 0.47% 0.76%

0.71% 0.49% 0.61% External Management 0.60% 0.56% 0.72% 0.53% 0.60% 2012

2013 2014 9/30/2015 Average 1.45% 1.66% 1.61% 1.19% 1.48% Internal

Management 2.47% 3.26% 3.37% 2.51% 2.90% External Management 2.17% 2.78%

3.50% 2.63% 2.77% OpEx as % of Avg Equity OpEx as % of Avg Assets

Efficiency of Operating Model Since 2012, Annaly has significantly

outperformed mREIT peers with respect to operating expenditures as a

percentage of assets and as a percentage of equity Annaly’s average

expense levels over the period are 65% lower as a percentage of average

assets and 47% lower as a percentage of average equity Annaly averaged

0.21% and 1.48%, respectively, while internally and externally managed

mREIT peers averaged 0.60% and 2.81% Source: Company Filings, SNL and

Bloomberg. Averages are market weighted based on market capitalization

as of December 31st of each respective year, unless otherwise specified.

2015 figures are not annualized. Note: Peer group includes BBREMTG Index

with market capitalization above $200mm as of the corresponding year

end. Excludes companies during years in which they became public or

first listed. Excludes Annaly. Note: Operating Expense defined as the

sum of Management Fees, Compensation & Benefits and General &

Administrative Expenses. Reimbursements of the management fee are

deducted from the management fee. Annaly Outperforms Internally and

Externally Managed mREITs

19 Industry Landscape &

Performance

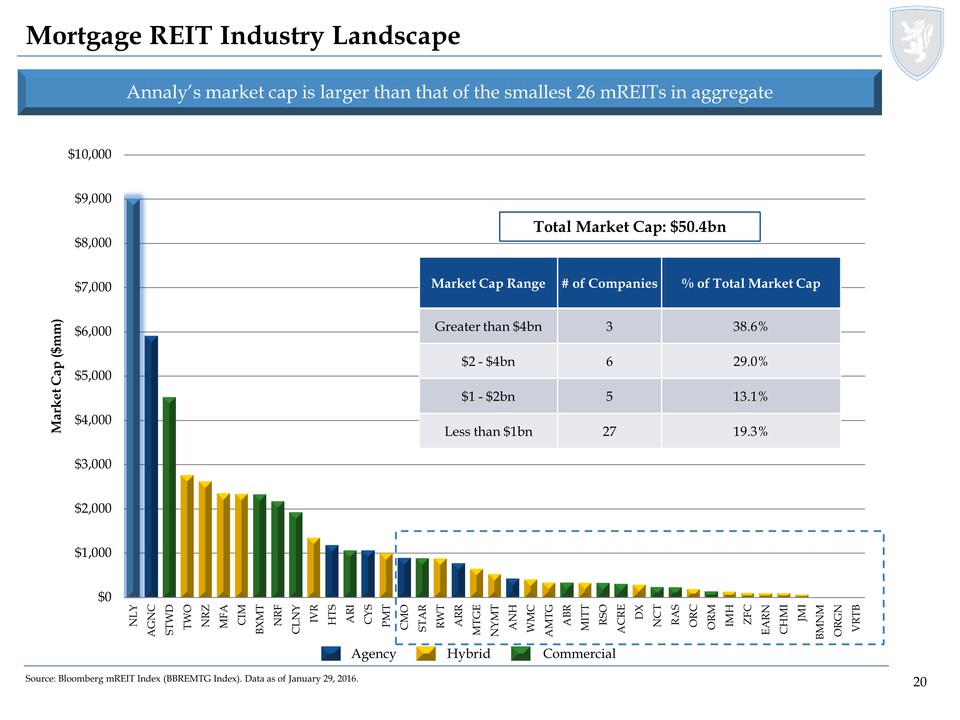

20 $0 $1,000 $2,000 $3,000

$4,000 $5,000 $6,000 $7,000 $8,000 $9,000 $10,000 NLY AGNC STWD TWO NRZ

MFA CIM BXMT NRF CLNY IVR HTS ARI CYS PMT CMO STAR RWT ARR MTGE NYMT ANH

WMC AMTG ABR MITT RSO ACRE DX NCT RAS ORC ORM IMH ZFC EARN CHMI JMI BMNM

ORGN VRTB Market Cap ($mm) Agency Hybrid Commercial Source: Bloomberg

mREIT Index (BBREMTG Index). Data as of January 29, 2016. Total Market

Cap: $50.4bn Market Cap Range # of Companies % of Total Market Cap

Greater than $4bn 3 38.6% $2 - $4bn 6 29.0% $1 - $2bn 5 13.1% Less than

$1bn 27 19.3% Annaly’s market cap is larger than that of the smallest 26

mREITs in aggregate Mortgage REIT Industry Landscape

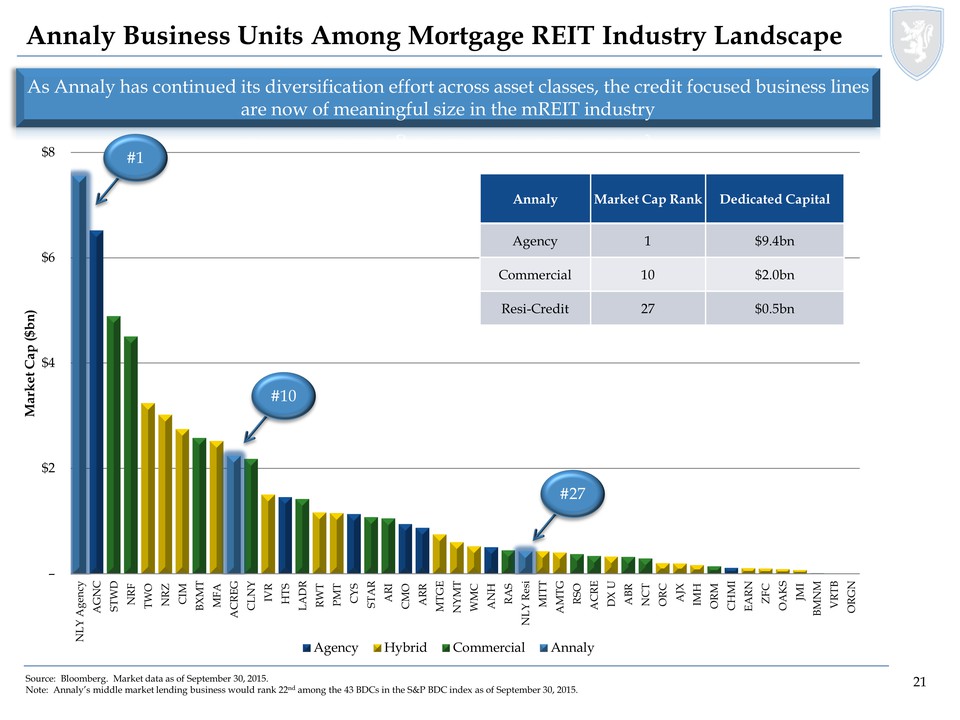

21 – $2 $4 $6 $8 NLY Agency

AGNC STWD NRF TWO NRZ CIM BXMT MFA ACREG CLNY IVR HTS LADR RWT PMT CYS

STAR ARI CMO ARR MTGE NYMT WMC ANH RAS NLY Resi MITT AMTG RSO ACRE DX U

ABR NCT ORC AJX IMH ORM CHMI EARN ZFC OAKS JMI BMNM VRTB ORGN Market Cap

($bn) Agency Hybrid Commercial Annaly Source: Bloomberg. Market data as

of September 30, 2015. Note: Annaly’s middle market lending business

would rank 22nd among the 43 BDCs in the S&P BDC index as of September

30, 2015. As Annaly has continued its diversification effort across

asset classes, the credit focused business lines are now of meaningful

size in the mREIT industry Annaly Market Cap Rank Dedicated Capital

Agency 1 $9.4bn Commercial 10 $2.0bn Resi-Credit 27 $0.5bn #1 #10 #27

Annaly Business Units Among Mortgage REIT Industry Landscape

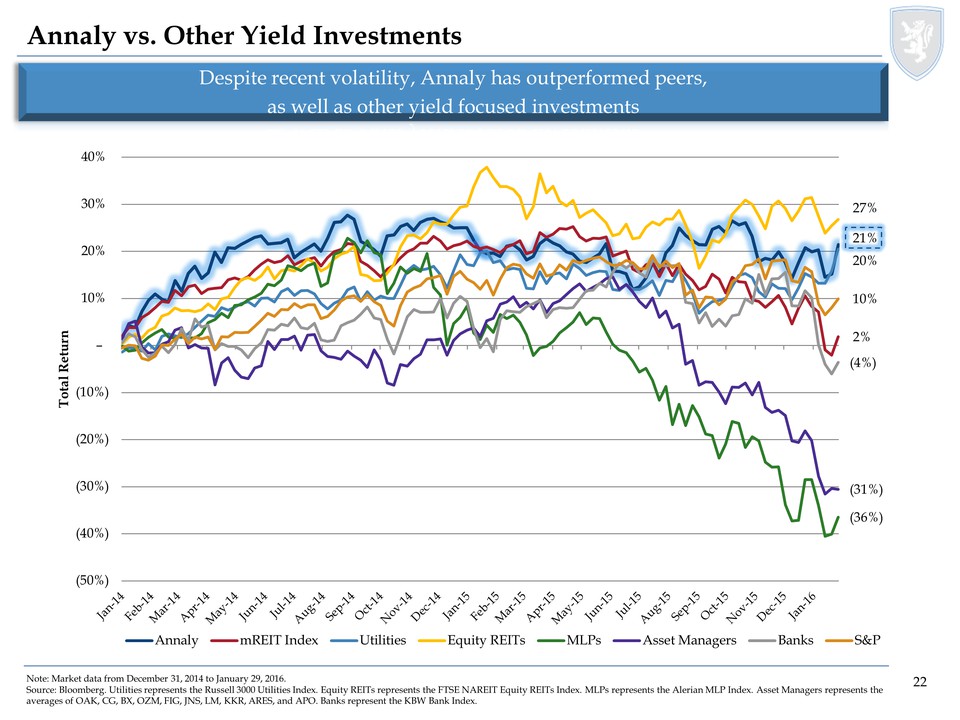

22 Annaly vs. Other Yield

Investments Note: Market data from December 31, 2014 to January 29,

2016. Source: Bloomberg. Utilities represents the Russell 3000 Utilities

Index. Equity REITs represents the FTSE NAREIT Equity REITs Index. MLPs

represents the Alerian MLP Index. Asset Managers represents the averages

of OAK, CG, BX, OZM, FIG, JNS, LM, KKR, ARES, and APO. Banks represent

the KBW Bank Index. Despite recent volatility, Annaly has outperformed

peers, as well as other yield focused investments 21% 2% 20% 27% (36%)

(31%) (4%) 10% (50%) (40%) (30%) (20%) (10%) – 10% 20% 30% 40% Total

Return Annaly mREIT Index Utilities Equity REITs MLPs Asset Managers

Banks S&P

23 Utilities Equity REITs

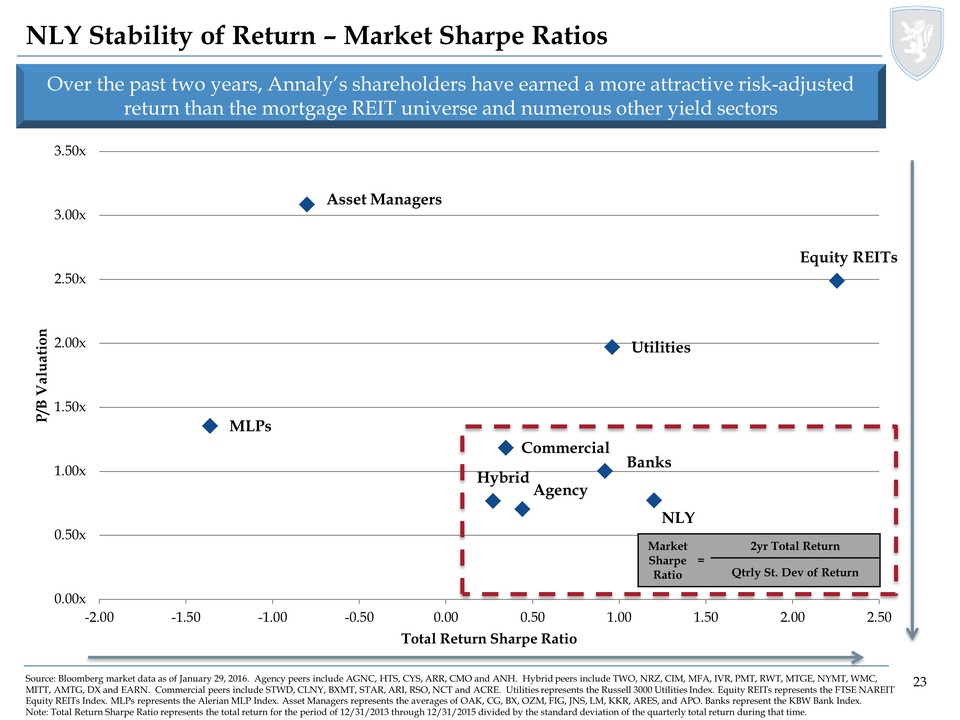

MLPs Asset Managers Banks NLY Agency Commercial Hybrid 0.00x 0.50x 1.00x

1.50x 2.00x 2.50x 3.00x 3.50x -2.00 -1.50 -1.00 -0.50 0.00 0.50 1.00

1.50 2.00 2.50 P/B Valuation Total Return Sharpe Ratio Over the past two

years, Annaly’s shareholders have earned a more attractive risk-adjusted

return than the mortgage REIT universe and numerous other yield sectors

Source: Bloomberg market data as of January 29, 2016. Agency peers

include AGNC, HTS, CYS, ARR, CMO and ANH. Hybrid peers include TWO, NRZ,

CIM, MFA, IVR, PMT, RWT, MTGE, NYMT, WMC, MITT, AMTG, DX and EARN.

Commercial peers include STWD, CLNY, BXMT, STAR, ARI, RSO, NCT and ACRE.

Utilities represents the Russell 3000 Utilities Index. Equity REITs

represents the FTSE NAREIT Equity REITs Index. MLPs represents the

Alerian MLP Index. Asset Managers represents the averages of OAK, CG,

BX, OZM, FIG, JNS, LM, KKR, ARES, and APO. Banks represent the KBW Bank

Index. Note: Total Return Sharpe Ratio represents the total return for

the period of 12/31/2013 through 12/31/2015 divided by the standard

deviation of the quarterly total return during that time. NLY Stability

of Return – Market Sharpe Ratios Market Sharpe Ratio = 2yr Total Return

Qtrly St. Dev of Return

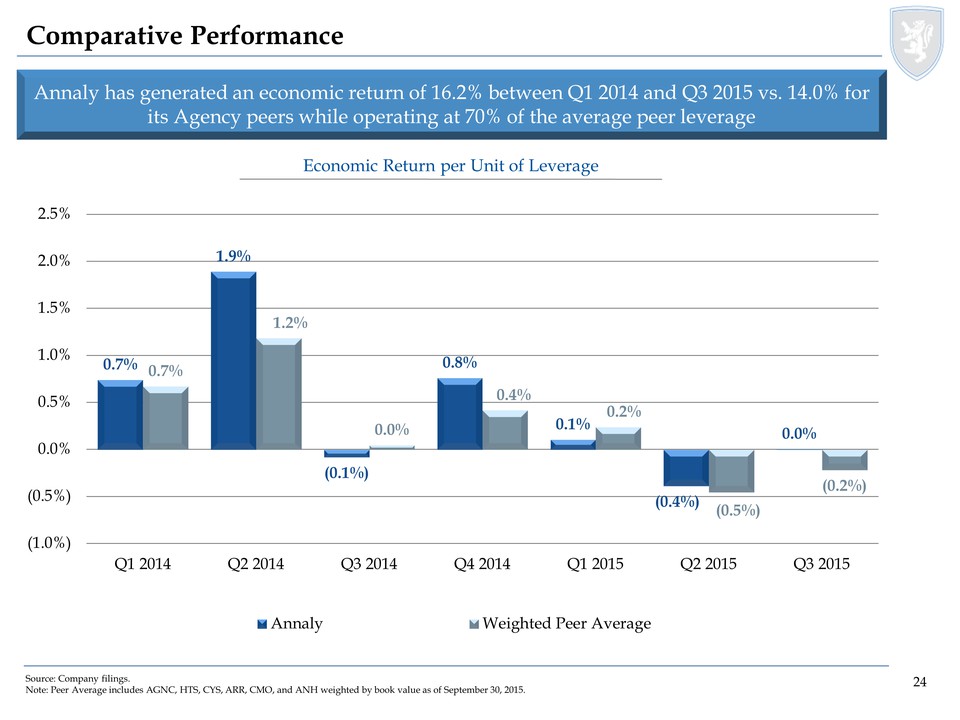

24 0.7% 1.9% (0.1%) 0.8%

0.1% (0.4%) 0.0% 0.7% 1.2% 0.0% 0.4% 0.2% (0.5%) (0.2%) (1.0%) (0.5%)

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2

2015 Q3 2015 Annaly Weighted Peer Average Comparative Performance Annaly

has generated an economic return of 16.2% between Q1 2014 and Q3 2015

vs. 14.0% for its Agency peers while operating at 70% of the average

peer leverage Source: Company filings. Note: Peer Average includes AGNC,

HTS, CYS, ARR, CMO, and ANH weighted by book value as of September 30,

2015. Economic Return per Unit of Leverage

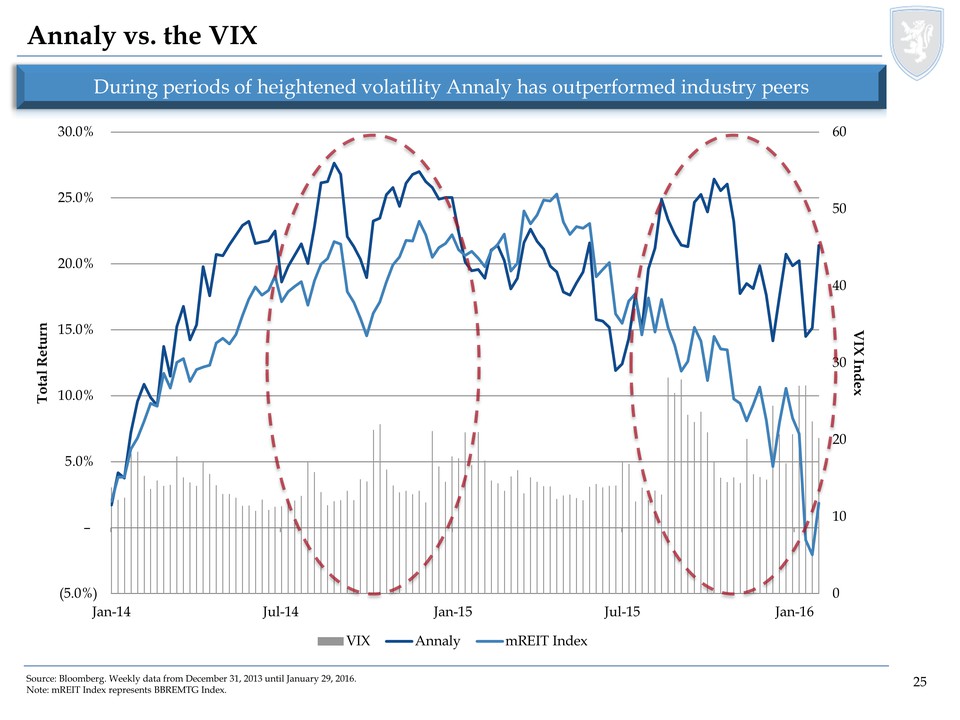

25 0 10 20 30 40 50 60

(5.0%) – 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% Jan-14 Jul-14 Jan-15 Jul-15

Jan-16 VIX Index Total Return VIX Annaly mREIT Index Annaly vs. the VIX

Source: Bloomberg. Weekly data from December 31, 2013 until January 29,

2016. Note: mREIT Index represents BBREMTG Index. During periods of

heightened volatility Annaly has outperformed industry peers

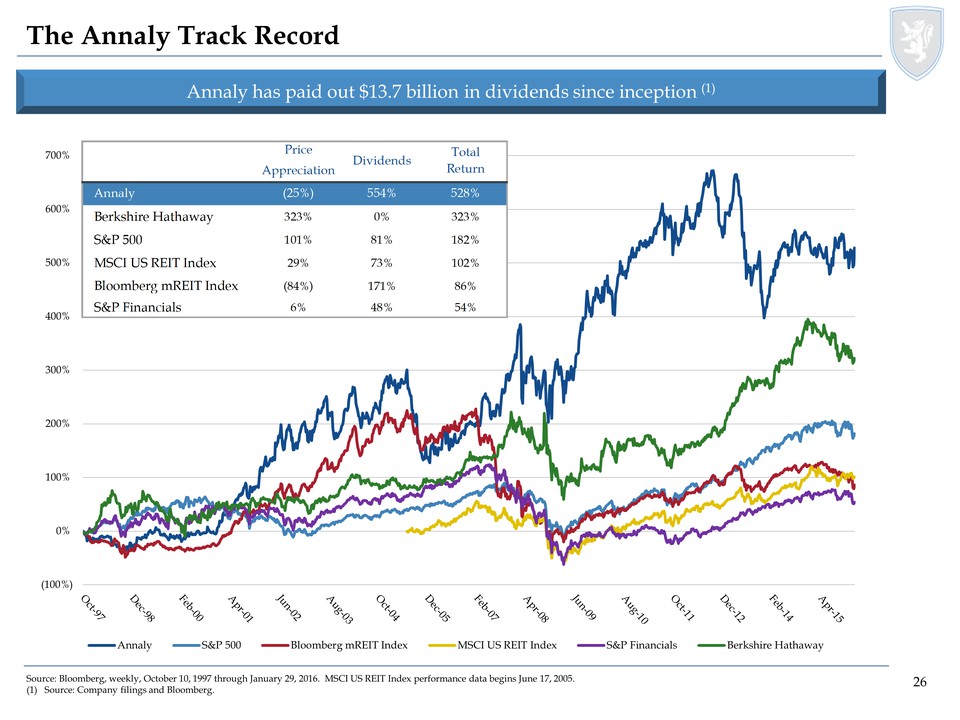

26 The Annaly Track Record

Annaly has paid out $13.7 billion in dividends since inception (1)

Source: Bloomberg, weekly, October 10, 1997 through January 29, 2016.

MSCI US REIT Index performance data begins June 17, 2005. (1) Source:

Company filings and Bloomberg. (100%) 0% 100% 200% 300% 400% 500% 600%

700% Annaly S&P 500 Bloomberg mREIT Index MSCI US REIT Index S&P

Financials Berkshire Hathaway Price AppreciationAnnaly(25%)554% 528%

Berkshire Hathaway323% 0% 323% S&P 500101% 81% 182% MSCI US REIT

Index29% 73% 102% Bloomberg mREIT Index(84%)171% 86% S&P Financials6%

48% 54% DividendsTotalReturn

Annaly Capital Management (NYSE:NLY)

Historical Stock Chart

From Aug 2024 to Sep 2024

Annaly Capital Management (NYSE:NLY)

Historical Stock Chart

From Sep 2023 to Sep 2024