UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the

Securities Exchange Act of 1934

(Amendment No. )

_________________

Filed by the Registrant c Filed

by a Party other than the Registrant £

Check the appropriate box:

c Preliminary

Proxy Statement

c Confidential,

for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

c Definitive

Proxy Statement

c Definitive

Additional Materials

£ Soliciting

Material Under §240.14a-12

Airgas, Inc.

(Name of Registrant as Specified in

its Charter)

L’Air Liquide, S.A.

(Name of Person(s) Filing Proxy Statement,

if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

£ No fee

required.

c Fee computed

on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

| (1) | Title of each class of securities to which transaction applies: |

________________________________________________________________________________________________

| (2) | Aggregate number of securities to which transaction applies: |

________________________________________________________________________________________________

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on

which the filing fee is calculated and state how it was determined): |

________________________________________________________________________________________________

| (4) | Proposed maximum aggregate value of transaction: |

________________________________________________________________________________________________

________________________________________________________________________________________________

c Fee paid previously

with preliminary materials.

| c | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the

offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and

the date of its filing. |

(1) Amount previously paid:

________________________________________________________________________________________________

| (2) | Form, Schedule or Registration Statement No.: |

________________________________________________________________________________________________

________________________________________________________________________________________________

________________________________________________________________________________________________

On November 18, 2015, L’Air Liquide, S.A. (“Air

Liquide”) posted an Investor Presentation slide deck to its website. A copy of the slide deck is attached as Exhibit 1.

On November 18, 2015, Air Liquide held a conference

call at 8:30 a.m. (CET) and posted a webcast of the call to its website. A transcript from the call is attached as Exhibit 2.

Exhibit 1

Strengthening Air Liquide’s leadership and building a new growth platform in North America A g ame - changing a cquisition November 18, 2015

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Legal disclaimer 2 CAUTIONARY STATEMENT REGARDING FORWARD - LOOKING STATEMENTS This press release contains certain statements that are “forward - looking statements” within the meaning of Section 27 A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934 , as amended . L’Air Liquide S . A . (“Air Liquide”) and Airgas have identified some of these forward - looking statements with words like “believe,” “may,” “could,” “would,” “might,” “possible,” “will,” “should,” “expect,” “intend,” “plan,” “anticipate,” or “continue,” the negative of these words, other terms of similar meaning or the use of future dates . Forward - looking statements in this release include without limitation statements regarding the expected timing of the completion of the transactions described in this press release, Air Liquide’s operation of Airgas’s business following completion of the contemplated transactions, and statements regarding the future operation, direction and success of Airgas’s businesses . Such statements are qualified by the inherent risks and uncertainties surrounding future expectations generally, and actual results could differ materially from those currently anticipated due to a number of risks and uncertainties . Risks and uncertainties that could cause results to differ from expectations include : uncertainties as to the timing of the contemplated transactions ; uncertainties as to the approval of Airgas’s stockholders required in connection with the contemplated transactions ; the possibility that a competing proposal will be made ; the possibility that the closing conditions to the contemplated transactions may not be satisfied or waived, including that a governmental entity may prohibit, delay or refuse to grant a necessary regulatory approval ; the effects of disruption caused by the announcement of the contemplated transactions making it more difficult to maintain relationships with employees, customers, vendors and other business partners ; the risk that stockholder litigation in connection with the contemplated transactions may affect the timing or occurrence of the contemplated transactions or result in significant costs of defense, indemnification and liability ; other business effects, including the effects of industry, economic or political conditions outside of the control of the parties to the contemplated transactions ; transactions costs ; actual or contingent liabilities ; and other risks and uncertainties discussed in Airgas’s filings with the U . S . Securities and Exchange Commission (the “ SEC ”), including the “Risk Factors” sections of Sangria’s most recent annual report on Form 10 - K . You can obtain copies of Airgas’s filings with the SEC for free at the SEC’s website (www . sec . gov) . Neither Air Liquide nor Airgas undertakes any obligation to update any forward - looking statements as a result of new information, future developments or otherwise, except as expressly required by law . All forward - looking statements in this announcement are qualified in their entirety by this cautionary statement . Additional Information and Where to Find it Airgas intends to file with the SEC a proxy statement in connection with the contemplated transactions . The definitive proxy statement will be sent or given to Airgas stockholders and will contain important information about the contemplated transactions . INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE PROXY STATEMENT CAREFULLY AND IN ITS ENTIRETY WHEN IT BECOMES AVAILABLE . Investors and security holders may obtain a free copy of the proxy statement (when it is available) and other documents filed with the SEC at the SEC’s website at www . sec . gov . Certain Information Concerning Participants Airgas and its directors and executive officers may be deemed to be participants in the solicitation of proxies from Airgas investors and security holders in connection with the contemplated transactions . Information about Airgas’s directors and executive officers is set forth in its proxy statement for its 2015 Annual Meeting of Stockholders and its most recent annual report on Form 10 - K . These documents may be obtained for free at the SEC’s website at www . sec . gov . Additional information regarding the interests of participants in the solicitation of proxies in connection with the contemplated transactions will be included in the proxy statement that Airgas intends to file with the SEC .

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas A new step in Air Liquide’s growth strategy Invest in growth markets North America, fastest growing advanced economy Enhance competitiveness Supply chain integration and multiple distribution channels Leverage innovation Wider customer base for advanced technologies deployment Deliver profitable growth over the long - term 3

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Leading national player Multi - channel distribution network Innovation platform A game - changing combination 4

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Undisputed global leadership #1 in North America #1 in Europe Middle East Africa #1 in Asia Pacific Source: Company estimates, global rankings for key segments #1 #1 Co #1 Industrial Merchant Large Industries Electronics Ideally positioned for growth over the long - term ...across geographies ...and business segments 5

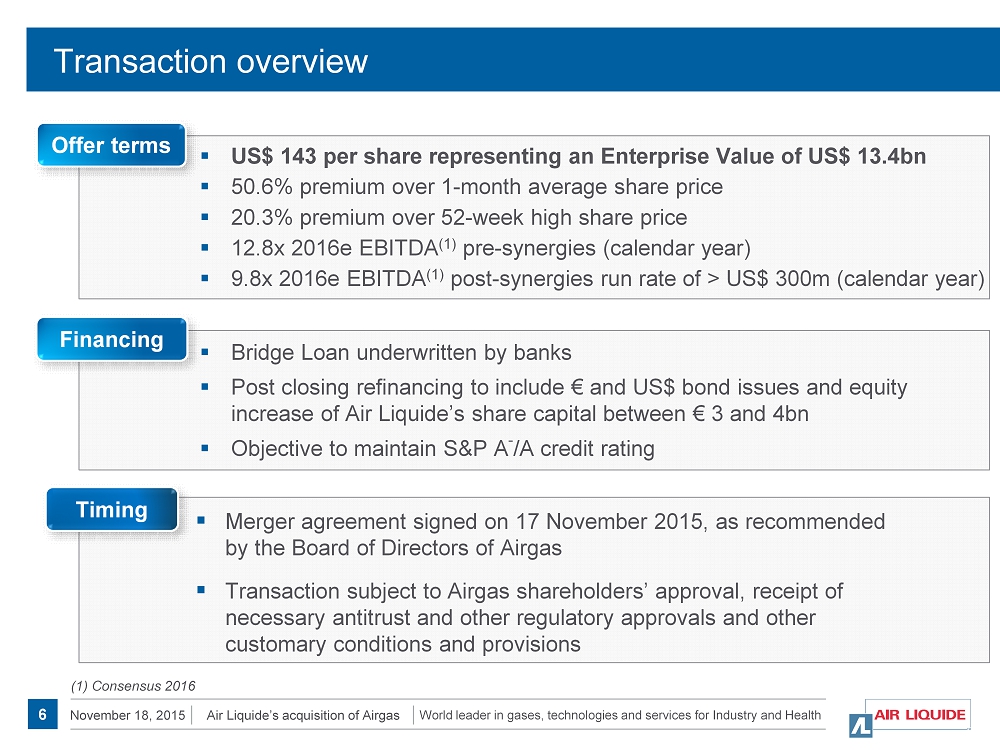

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Transaction overview ▪ Bridge Loan underwritten by banks ▪ Post closing refinancing to include € and US$ bond issues and equity increase of Air Liquide’s share capital between € 3 and 4bn ▪ Objective to maintain S&P A - /A credit rating ▪ Merger agreement signed on 17 November 2015, as recommended by the Board of Directors of Airgas ▪ Transaction subject to Airgas shareholders’ approval, receipt of necessary antitrust and other regulatory approvals and other customary conditions and provisions ▪ US$ 143 per share representing an Enterprise Value of US$ 13.4bn ▪ 50.6% premium over 1 - month average share price ▪ 20.3% premium over 52 - week high share price ▪ 12.8x 2016e EBITDA (1) pre - synergies (calendar year) ▪ 9.8x 2016e EBITDA (1) post - synergies run rate of > US$ 300m (calendar year) (1) Consensus 2016 Offer terms Financing Timing 6

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Agenda 1 3 2 4 Conclusion Strong financial fundamentals A game - changing acquisition Airgas, U.S. leader in packaged gas 7

1. Airgas, U.S. leader in packaged gas

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Proven success story Airgas, the unique partner to capture the North American growth ▪ Leader in packaged gas ▪ Major supplier of h ardgoods ▪ Largest footprint and asset base in the U.S. ▪ Coupled with best - in - class e - commerce platform ▪ 1 million+ customers ▪ Resilient profile with diversified customer segments ▪ Proximity to customers ▪ Unparalleled growth since 1982 ▪ Proven operational excellence ▪ Strong shareholder value creation 9 Major player in the U.S. market Multi - channel distribution network with unmatched reach Unrivalled customer base Solid track record of value creation

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Hardgoods Industrial gas Major player in the U.S. market Broadest offering of p ackaged g as and h ardgoods 10 63% 37% #1 in packaged gas Major supplier of hardgoods Full range of gases and delivery modes “One - stop - shop” model meeting U.S. customers’ expectations

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Multi - channel distribution network with unmatched reach 1,100 locations >900 branches and retail stores Source: Airgas company information Unparalleled distribution network… …coupled with expanding e - commerce platform 11

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Unrivalled US customer base 1 million+ customers Served by 17,000 professionals & industry specialists Customer proximity and strong focus on service Balanced portfolio of end markets Sales mix (FY2015) Source: Airgas company information, Fiscal Year 2015 ending 31 March 2015 Resilient profile with diverse customer base 12 US$5.3bn Energy & Chemical 12% Basic Materials 12 % Government 6% Food 13 % Healthcare 14% Non - Res. Construction 14 % Metal Fabrication 29 %

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Solid track record of value creation Source: Airgas company information, FY2015 ending 31 March 2015 High value creation for shareholders 0.00 1.00 2.00 3.00 4.00 5.00 6.00 1986 2005 2010 2015 Published EPS (US$) 0.03 1.19 4.85 Long history of solid growth 0.0 1.0 2.0 3.0 4.0 5.0 6.0 1986 2005 2010 2015 Net Sales ( US$bn ) 0.1 2.4 5.3 13

2. A game - changing acquisition

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas The U.S.: an attractive gas market ▪ Low energy prices driving investment and manufacturing ▪ Raising environmental awareness ▪ Innovation ecosystem and digital edge ▪ Healthcare and aging population 20 - 25% Source: Air Liquide estimates The U.S. will be a key driver of global growth & innovation U.S., the largest gas market worldwide... … set for growth in the long - term 15 2014 2020E US$ 22bn US$ 17bn

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Further acquisition opportunities boosting growth Source: Air Liquide estimates Independents Major players U.S. packaged gas market ~ 50% of market composed of independent producers Large potential for bolt - on acquisitions Airgas experience of integrating small players 16

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Unique US business combination Market coverage Cost synergies Improved customer service Leading position in new digital channels Liquid bulk Fill plant Direct delivery Retail Telesales e - commerce Large Industries Merchant bulk Packaged gas Liquid bulk Pipeline & on - sites Bulk deliveries Fill plant Fill plant 17 Primary production Primary production

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Highly complementary U.S. market reach Source: Air Liquide estimates (1) Calendar year 2014 Gas & Services sales Results in the most comprehensive product offering U.S. U.S. 18 Large industries Merchant bulk Packaged gas Electronics Sales US$ 2.7bn (1) US$ 5.3bn (1) US$ 8.0bn

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas A unique platform for growth 19 Innovation capabilities Unique distribution Worldwide #1 customer base ▪ Branch - based field stores ▪ eBusiness ▪ Telesales ▪ Strategic accounts ▪ … ▪ Market applications ▪ Advanced cylinders ▪ Efficient production ▪ … Leverage on innovation and multi - channel distribution

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Well - balanced global footprint Americas 42% Europe 37% Asia Pacific 19% Middle East & Africa 2% Americas 24% Europe 48% Asia Pacific 25% Middle East & Africa 3% € 13.9bn € 17 .8bn + 20 Gas & Services 2014 s ales (1) (1) Calendar year 2014 c onverted from USD to EUR at 2014 average exchange rate of 1.326

3. Strong financial fundamentals

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas > $ 300m of highly executable synergies ▪ Cross - selling ▪ Roll - out of Air Liquide’s innovative product offering in the U.S. ▪ Gas sourcing & procurement ▪ Plant loading ▪ Distribution efficiencies ▪ Optimization of sites & admin. >70% 22 Cost & Efficiency synergies Volume growth synergies 2 to 3 years 4 years

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Value accretive transaction Pro - forma Pro - forma 15.4 4.0 (1) 19.3 2.6 0.5 (1) 3.1 17.1% 12.2% 16.1% in € bn in € bn and % margin 23 Expected EPS accretion from Year 1 Objective: return to double - digit ROCE in 5 - 6 years Pro - forma Group sales 2014 Pro - forma Group OIR 2014 (1) Calendar year 2014 c onverted from USD to EUR at 2014 average exchange rate of 1.326

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Refinancing objective to maintain S&P A - /A credit rating Equity € 3 - 4bn USD & EUR bonds Enterprise value Re - financing 24 Closing Bridge loan Signing Bank commitment Assumed debt

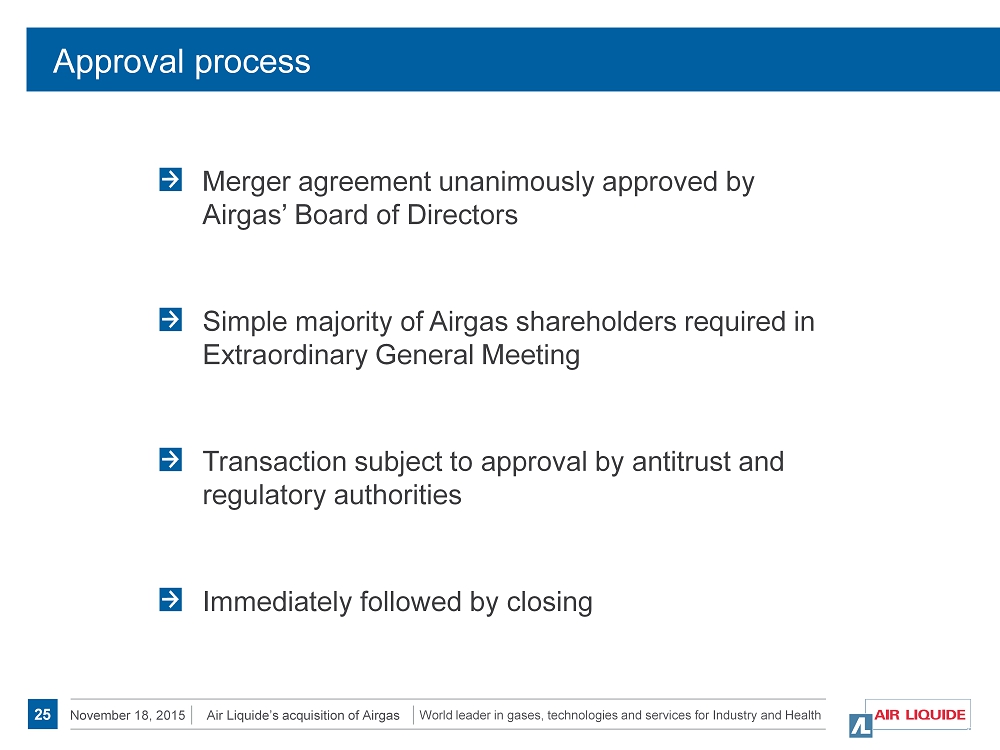

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Approval process Merger agreement unanimously approved by Airgas’ Board of Directors Simple majority of Airgas shareholders required in Extraordinary General Meeting Transaction subject to approval by antitrust and regulatory authorities Immediately followed by closing 25

Creating a unique business combination in North America Strengthening Air Liquide’s ability to grow in North America and beyond World leader in gases, technologies and services for Industry and Health 4. Conclusion +

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas Sales distribution by WBL € 13.9bn € 17.8bn + 28 Gas & Services 2014 Sales (1) Large Industries 36% Industrial Merchant 37% Healthcare 18% Electronics 9% Large Industries 28% Industrial Merchant 49% Healthcare 16% Electronics 7% (1) Calendar year 2014 c onverted from USD to EUR at 2014 average exchange rate of 1.326

World leader in gases, technologies and services for Industry and Health November 18, 2015 Air Liquide’s acquisition of Airgas 29 For further information, please contact: Investor Relations Aude Rodriguez + 33 (0)1 40 62 57 08 Erin Sarret + 33 (0)1 40 62 57 37 Louis Laffont + 33 (0)1 40 62 57 18 Jérôme Zaman + 33 (0)1 40 62 59 38 L’Air Liquide S.A. Corporation for the study and application of processes developed by Georges Claude with registered capital of 1,897 ,386,986.00 euros Corporate headquarters : 75, Quai d’Orsay 75321 Paris Cedex 07 Tel : +33 (0)1 40 62 55 55 RCS Paris 552 096 281 www.airliquide.com Follow us on Twitter @AirLiquideGroup Communications Anne Bardot + 33 (0)1 40 62 50 93 Annie Fournier + 33 (0)1 40 62 51 31

Exhibit

2

Air Liquide

announces agreement to acquire Airgas

Transcript – 18/11/2015

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING

STATEMENTS

This press release contains certain statements

that are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E

of the Securities Exchange Act of 1934, as amended. L’Air Liquide S.A. (“Air Liquide”) and Airgas have identified

some of these forward-looking statements with words like “believe,” “may,” “could,” “would,”

“might,” “possible,” “will,” “should,” “expect,” “intend,”

“plan,” “anticipate,” or “continue,” the negative of these words, other terms of similar meaning

or the use of future dates. Forward-looking statements in this release include without limitation statements regarding the expected

timing of the completion of the transactions described in this press release, Air Liquide’s operation of Airgas’s business

following completion of the contemplated transactions, and statements regarding the future operation, direction and success of

Airgas’s businesses. Such statements are qualified by the inherent risks and uncertainties surrounding future expectations

generally, and actual results could differ materially from those currently anticipated due to a number of risks and uncertainties.

Risks and uncertainties that could cause results to differ from expectations include: uncertainties as to the timing of the contemplated

transactions; uncertainties as to the approval of Airgas’s stockholders required in connection with the contemplated transactions;

the possibility that a competing proposal will be made; the possibility that the closing conditions to the contemplated transactions

may not be satisfied or waived, including that a governmental entity may prohibit, delay or refuse to grant a necessary regulatory

approval; the effects of disruption caused by the announcement of the contemplated transactions making it more difficult to maintain

relationships with employees, customers, vendors and other business partners; the risk that stockholder litigation in connection

with the contemplated transactions may affect the timing or occurrence of the contemplated transactions or result in significant

costs of defense, indemnification and liability; other business effects, including the effects of industry, economic or political

conditions outside of the control of the parties to the contemplated transactions; transactions costs; actual or contingent liabilities;

and other risks and uncertainties discussed in Airgas’s filings with the U.S. Securities and Exchange Commission (the “SEC”),

including the “Risk Factors” sections of Airgas’s most recent annual report on Form 10-K. You can obtain copies

of Airgas’s filings with the SEC for free at the SEC’s website (www.sec.gov). Neither Air Liquide nor Airgas undertakes

any obligation to update any forward-looking statements as a result of new information, future developments or otherwise, except

as expressly required by law. All forward-looking statements in this announcement are qualified in their entirety by this cautionary

statement.

Additional Information and Where to Find

it

Airgas intends to file with the SEC a proxy

statement in connection with the contemplated transactions. The definitive proxy statement will be sent or given to Airgas stockholders

and will contain important information about the contemplated transactions. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE

PROXY STATEMENT CAREFULLY AND IN ITS ENTIRETY WHEN IT BECOMES AVAILABLE. Investors and security holders may obtain a free copy

of the proxy statement (when it is available) and other documents filed with the SEC at the SEC’s website at www.sec.gov.

Certain Information Concerning Participants

Airgas and its directors and executive officers

may be deemed to be participants in the solicitation of proxies from Airgas investors and security holders in connection with the

contemplated transactions. Information about Airgas’s directors and executive officers is set forth in its proxy statement

for its 2015 Annual Meeting of Stockholders and its most recent annual report on Form 10-K. These documents may be obtained for

free at the SEC’s website at www.sec.gov. Additional information regarding the interests of participants in the solicitation

of proxies in connection with the contemplated transactions will be included in the proxy statement that Airgas intends to file

with the SEC.

KEY: Unable to decipher = (inaudible

+ timecode), Phonetic spelling = (ph + timecode), Missed word = (? + timecode). For respondents M: Male, F: Female.

(TC: 00:00:00)

Aude Rodriguez: Good morning, everyone. This

is Aude Rodriguez, head of investor relations. Welcome to our conference call regarding the Air Liquide, Airgas deal. Benoît

Potier will first introduce the presentation and will present the strategic rationale of the acquisition, after Pierre Dufour has

taken you through Airgas. Fabienne Lecorvaisier will highlight the financial fundamentals. Benoît, Pierre and Fabienne will

then be available to answer your questions. I remind you that the next announcement of our full year, 2015 results will be on 16

February 2016. Thank you, and I hand it over to Benoît.

Benoît Potier: Thank you all, good morning

to everyone. I’m very pleased to be with you for this announcement this morning. This is undoubtedly a game changing acquisition

for Air Liquide, and a major step, definitely, in the overall strategy of Air Liquide to deliver profitable growth in the long-term.

This growth will be, in this case, in America, North America, which, as we all know, is the largest industrial gas market. It’s

also the fastest growing market among advanced economies, about 4% growth on the average, and this is a market expected to deliver

about 20% to 25% of the global industrial gas mid-term growth, and the market that might reach $22 billion in 2020. This is really

a game changing acquisition that will enhance our competitiveness, first of all by a fully integrated supply chain. I think that’s

one of the major characteristics of this acquisition, the complementing of the two businesses, and also it will give us a full

market coverage, with multiple distribution channels that will include telesales and e-business, and I’m sure we’ll

have occasions to talk about that. In a nutshell, this is a unique platform to deploy Air Liquide’s most innovative products

and technologies in North America. We don’t have, today, the base that is required for that, and it would be with a strong

digital content or value service, and in particular thinking about the smart, easy to use cylinders.

This is a game changing combination also because

the businesses are highly complementary businesses. Airgas is a recognised leading national player in package gases, with about

25% combined market share. Over the years, I would say, it builds a multichannel distribution network and is now the most advanced

industrial gas company in terms of ecommerce. This will give us an exceptional innovation platform for advanced products and business

models of the two companies. Page six, there’s just an overview of the transaction. I think you had all the terms in the

press release. The price per share offered is $143 per share. It represents an equity value of 10.3 billion and a total enterprise

value of 13.4 billion. In terms of statistics, it’s a premium of more than 50% over the one month average share price. A

premium of 20%, 20.3% over the 52 week high share price, and a multiple of 2016 estimated EBITDA of 9.8, including the few synergies

that will be over $300 million pre-tax. In terms of financing, we have two steps. The first step is going to be a bridge loan,

which has been underwritten by banks. Then, the second step will be refinancing through euro and dollar bond issues, and a capital

increase between €3 and €4 billion, with of course an objective to maintain, A S&P credit rating, A minus.

For the timing, the merger agreement recommended

by the board of Airgas was signed yesterday, November 17th. This transaction is, of course, subject to approval by both Airgas

shareholders meeting and customary authorities which include antitrust. On page five, we just have a very broad view of the positions.

We will become clearly an undisputed global leader. It will reinforce our leadership of the industry. We’re already number

one in Asia Pacific, in Europe, Middle East and Africa in industrial gas. We have complete coverage of the full market through

various business

segments, and when we look at the business

segments, we will also be number one in industrial merchant large industries and electronics. So, we will be, definitely, ideally

positioned for growth over the long term. That’s, in a nutshell, the content of this fantastic acquisition. I would like

now to hand over to Pierre, who is going to give you more insight about Airgas as a company. Pierre?

Pierre Dufour: Thank you, Benoît. So, what

is Airgas? Airgas is a company that was born in the early 1980s, 1982-ish. It started by being an aggregator of small distributors

in the US market. So, over the years, they have aggregated or made about 450 acquisitions of mostly small to medium-sized companies,

to become what they are today. After they attained a certain critical mass, about four, five years ago, they transformed their

company, to make the company a real operational company, and not only a grow by acquisition type company. So, today we have a company

that has a real operating philosophy, a real operating culture. Still doing some acquisitions, but was growing mostly through an

operating strategy. So, Airgas is the major player in the US market today for package gas. It is the leader in that market. It

has a very unique customer base, with more than one million customers. They touch these customers in just about every channel that

can be used. They touch them with direct salesmen, they touch them with industry specialists. They touch them through telemarketing,

they touch them through ecommerce.

They touch them through stores with over

1,000 such stores in the country. So, they’re really the big specialist and by far the leading company in distribution

channels for their gas and services. So, this is what is attractive to us, is to acquire this platform which will allow us to

leverage the advantage of Air Liquide, which are technology-based, new offer-based and the like. So, having more than a

million customers, being in a very diversified market, I’ll touch on that a little bit in a few minutes, and the

remarkable multichannel distribution system, but this is what, in a nutshell, Airgas is. Now on slide 10, Airgas is a gas

company. Almost two thirds of their sales, 63% at last count is in package gas, in all ranges, and all delivery modes. They

also have hardgoods, because they believe in the one-stop shop model in the US, it’s a model that is prevalent, and

this model basically makes them a leader in the hardgoods supply as well, but the hardgoods is not an end in itself. The

hardgoods is a complementary business to their gas business.

On slide eleven, getting back to this multichannel

distribution network, the many ways in which they’re able to reach their customers, again, 1,100 locations, 900 branches

and retail stores with a lot of people on the ground, a lot of salespeople on the ground, contacting customers. Together, coupled

with an e-commerce platform which is leading our industry, which is very efficient, and again, with a lot of growth in that channel,

compared to the traditional channels, that gives us a very good way to leverage the digital age. Also, telemarketing, telecommerce,

which is, again, another very efficient way to touch or to reach a certain segment of customers. So, very strong in the distribution

(TC: 00:10:00) channels. On slide twelve, their customer base is unique, over a million customers, as you can see on the chart.

Very, very balanced presence in most of the markets that are available in the US economy, which gives them a lot of resilience

and gives them, basically, access to all of the growth segments of the US economy. So, it’s very balanced from an in-market

perspective. It’s very balanced on customer size segmentation, and it’s a company that has 17,000 people who are-,

whose culture is really a client-first culture, which is a very nice culture that we-, that sits with our own strategy on that

issue. So, a very balanced portfolio. Their company has been very successful. They’ve grown for a long time, since their

inception, very long history of growth. A growth about 8% over the last ten years or so, and also, a high value creation, because

they’re able, when they grow the company, to enhance the gas component of their sales, and hence increase their earnings,

which is something, of course, we also try to do. So, a very strong company from an operational perspective. A very strong company

in their

presence in the market, and a very strong company

in their ability to develop sales and profit from those sales. Benoît, back to you.

BP: Thank you, Pierre. So, why is it a game

changing acquisition? We need to start from the US market. This is on page fifteen. The US is undoubtedly a very attractive gas

market. If we just look at the world market, many developing economies today have reached a sort of phase of transition, with slower

growth perspectives, and we see the progressive convergence of global growth rates. This is why, in this context, the US is a very

attractive gas market. This is the largest industrial gas market worldwide. This is the fastest growing market among advanced economies.

As I said earlier, this is expected to deliver about 20% to 25% of global mid-term growth, and the average compounded annual growth

rate is expected to be about 4% to 4.5% over 2014 to 2020, and this market is also supported by the structural strength of the

US economy in the long term. Clearly, what has changed in the past five years is the competitive nature of the natural gas heat

stock and energy situation with prices being very competitive, and it’s driving investment and manufacturing in the US. There’s

also, sort of, raising environmental awareness, that may trigger new markets in the US. There are strong society drivers, such

as healthcare and aging population. There are drivers that we find everywhere else also, but the US is also at the heart of this

transformation, and finally, Airgas provides a, sort of, unique access to the US, high-tech and innovation prone environment.

So, the US market will be a key driver of global

growth and innovation. Now, if we just zoom a little bit more on the package gas, page sixteen, approximately half of the US package

gas market is composed of independent producers, but this provides further opportunities to continue to boost future growth and

we will pursue this successful historical strategy both Airgas and Air Liquide having significant experience in integrating small

players. Now, if we look at the distribution pattern, the slide seventeen illustrates the strong complementarities of Air Liquide

and Airgas businesses in the US. Starting with Air Liquide on the left, the main presence upstream is on primary production both

in large industry, with over 3,500km, or 2,200 miles of pipeline network in America. It’s mainly in the gulf coast, and in

bulk business, also, in the US. We also supply large and medium-sized customers, mainly. Airgas, on their side, on the right, is

more present in the downstream distribution, with 300 filling stations across the US, package gas being delivered through 900 branches

and retail stores, whereas Air Liquide goes about 80% through distributors.

They also have telesales, e-commerce, or next

day UPS direct deliveries from national warehouses. So, Air Liquide and Airgas are really quite complementary, and together offer

the most complete market coverage and offering to customers. The integration, upstream and downstream will generate synergies and

improve customer service. When we look at the future pattern of the combined entities, page eighteen, we see that the combined

company will have approximately $8 billion in sales in the US. Air Liquide will have strong positions in large industry and electronic

business. That will remain, and Airgas’ merchant book will reinforce Air Liquide’s existing position, whereas Air Liquide

will benefit from Airgas’ strong position in package gases. So, it will result in the most comprehensive product offering

in the US. On slide nineteen, we just see that by combining, one, Air Liquide and Airgas innovation capabilities, two, distribution

channels, the completion of two distribution channels, and number three, a worldwide number one customer base. The two of us together

are creating a unique platform that will deliver significant mid-term growth. We will be able to deploy the innovation, the Air

Liquide innovation more effectively in the US, but also to replicate Airgas’ successful product and business models outside

of the US, and it will enable the development of innovative and new digital offers, bringing value and new services worldwide to

package gas customers and beyond.

There’s one thing I’d like just

to mention as well, that we have already done such a combination of base and innovation in Canada, where Air Liquide has successfully

introduced most of the advanced technologies from Europe on a very successful way. When we look now on page twenty, on the new

combination and the new Air Liquide footprint, America will be the largest weight with 42% of the new group sales instead of 24%

currently. Europe will come down from 48% to 37%, and Asia Pacific from 25% to 19%. So, we will rebalance Air Liquide towards North

America. That will enable us to leverage the dynamic economic environment of the US, in terms of growth but also innovation and

talents, and overall position Air Liquide even better for growth in the mid to long term. I’m thinking about those drivers

that we have identified recently for the future years. I’m talking about energy and climate change transition. I’m

also talking, or thinking about the digital revolution, but also the healthcare transformations. All those drivers will help, together

with the new footprint, and the excellent national base that we will get to really develop growth in this continent. Thank you,

and I’ll now hand over to Fabienne.

Fabienne Lecorvaisier: Well, thank you Benoît.

As mentioned in the introduction, this deal is supported by strong financials, given the strategic seat and the strength of our

complementary product offerings, a combination of the two businesses, we generate synergies and efficiencies. If you look at page

22, we have quantified the cost and the volume growth synergies, and our estimate after full ramp up is above $300 million pre-tax.

The efficiency and cost synergies, which rely on sourcing optimisation, permitting a better loading of both parties’ associated

distribution efficiencies and reorganisation, (TC: 00:20:00) we’ll ramp up, in a two to three year period, and represent

above 70% of the total. The volume growth synergies will result from cross-selling and extension of the customer reach, as well

as from the roll-out of the Air Liquide current innovative offer, through the Airgas different distribution channels over the next

four years. They will present the rest of the total. We also believe that we’ll be able, over time, to create additional

value to the use of the Airgas platform to deploy the Air Liquide most advanced technologies, including connecting cylinders of

hydrogen energy, and also through the replication of the Airgas offering and model in other countries. The additional strategy

synergies are not, of course, included in this $300 million.

In terms of impact on the Air Liquide group,

on page 23, you have performance based on the 2014 calendar year published numbers, and 2014 average foreign exchange rate. Combined

sales would have been above €90 million, and operating income recurring would have been above €3 billion. More broadly,

this acquisition is going to boost our average yearly growth by approximately 5% over the next five years, while only initially

reducing the group operating margin by 100 by this point. It is also important to note that the impact on earnings per share is

expected to be positive from the first full year of ownership. Of course, due to the good will associated with the transaction,

the return on capital employed is going to be impacted in the early years, but the objective is clearly to return to double digits

after five or six years. A few words about the financing of the transaction. Our primary objective is to keep our A credit rating

from Standard and Poor’s, even if it is reduced to A minus initially, and the financing of the transaction will be designed as such.

Our offer, which has been unanimously approved by the board of Airgas is supported by bank underwriting for a bridge loan, equal

to the full cash amount of the equity value and of the Airgas debt to be refinanced at closing.

The bridge loan will be drawn at closing and

refinanced as soon as possible thereafter, through an equity increase of Air Liquide, S.A. in an amount between €3 billion

and €4 billion and through a mix of euro and US dollar bond issues. The approval process includes the approval of the Airgas

board of directors, which, as you know, was obtained last night. After the confirmation of the SEC clearance, the vote of Airgas

shareholders would be required, with another 50% majority in an extraordinary general shareholder meeting, and in parallel, the

transaction will be submitted to the various regulatory

authorities and in particular to the antitrust

authorities. There, the closing will immediately follow the obtaining of those various approvals. Benoît, for the conclusion?

BP: Yes. The conclusion is very simple. We

believe that the Air Liquide, Airgas transaction will allow the creation of a unique business combination in North America, and

it will significantly strengthen our ability to grow in this region, but also beyond. It will confirm also our leadership, our

world leadership in gases, technology and services for industry and earth, and will offer to our customers, I think, a unique player,

not just in North America but all across the world. Thank you, and we can now start the Q and A session.

F: Thank you. If you would like to ask a question

over the telephone, please press star one. Please ensure the mute button on your telephone is switched off to allow your signal

to reach our equipment. Again, please press star one to ask a question. We’ll take the first question from the telephone

from Paul Walsh from Morgan Stanley.

Paul Walsh: Thanks very much guys. It’s

Paul, from Morgan Stanley. Three questions, if I can, to kick off. My first question around EPS accretion in year one. Can you

give me the assumptions you’ve made behind that, as it relates to the rights discount, the cost of debt, the remedy packages

and the synergies? My second question is, you talk about returning to double digit returns for the group, I guess that is, but

over what period do you think you can get the returns on the acquisition back up over your hurdle rate, given the price that’s

been paid? My final question, just on the Airgas business, it was interesting to me that we’ve seen material earnings downgrade

at Airgas this year, when you look at consensus numbers. So, I was wondering if you could talk a little bit about some of the headwinds

their business has been facing this year, and the extent to which that’s impacted growth in the Airgas business. Thanks very

much.

BP: Right, thank you. I think Fabienne will

answer the first, and I’ll take the second, Pierre the third.

FL: So, as I explained, the design of the refinancing,

including the level of the equity increase will be fine-tuned after our discussion with the rating agencies, so, we have made several

scenarios, and in those several scenarios, we see a first year earning per share equation, which is between 2% and 5%. No synergies

have been included, or very small synergies in the first year calculation, as those synergies will take a little time to ramp up.

So, it is what we have at the time being, so more range than precise number, because we still need to fine-tune the structure of

the refinements.

PW: Sorry, just one quickly on that, no remedy

packages have been assumed in that 2% to 5% accretion, I guess?

FL: Yes, there are several scenarios as well,

in terms of remedy packages, and that will depend, as you know, on our discussion with the antitrust authorities, but this has

been taken into account, of course.

PW: Okay, thank you.

BP: The second question is, of course, related

to the return on capital, Paul, yes, the double digit will be a group double digit in five, six years. The immediate effect on

the business of this acquisition, I’m talking the Airgas impact, will be what it is for the immediate impact, but very soon

we’ll have the cost synergies that will be factored in. So, we think that very early in the period, we’ll be able to

be above the whack for this acquisition only. Of course, we will remain far above whack for the group, even with this acquisition,

and we plan, overall, for the group to be back to double digits in five, six years.

We think we have a very reasonable and achievable

synergy plan. This is well-identified. There was tremendous work made by our teams to asses those synergies, so we are confident

that we have a very good plan to actually achieve this objective of double digit return ROCE by five, six years. Pierre?

PD: Yes. The headwinds that were faced by Airgas

in the last year or two are the same headwinds that the whole industry has suffered through. The drop in oil prices has created

a shock in all of the industries that support oil and gas exploration and production. Not only the direct industry, the drilling

industry, and so on and so forth, but also the industries that support those industries. So, these are the headwinds that have

hit the whole industry, including our business in the US, and everybody else’s. The business of Airgas, as ours, is actually

growing outside of these industries. So, the US economy, apart from the different segments affected by oil and gas are not so-,

are not doing so badly, but of course, the weight of the oil and gas segments, and then the support segments to that industry have

pulled-, have created the headwinds that Airgas has been suffering through. So, we don’t think that this is a permanent state

of affairs in the US. We think that, as the low energy cost environment continues to take hold, that the US industry is going to

grow at rates that have been known historically, starting I don’t know when, but starting reasonably soon. So, we’re

not at all down on the US current headwinds, we just have to go through them, as an industry, and then business will be more, I

would say, balanced between the different segments.

PW: Thanks very much, guys, thank you.

BP: Thank you, next question.

F: We’ll now take the next question from

Laurence Alexander, from Jefferies.

Laurence Alexander: (TC: 00:30:00) Good morning.

Just a couple. First, would your plan be to just maintain the ERP system that Airgas has in place, or would you put in place your

own systems? Secondly, can you give your view on the strategy of adding merchant capacity at a fairly consistent clip, that Airgas

has been pursuing, or would you adopt a different strategy for that, for those assets, and third, can you speak a little bit to

the non-traditional businesses within the Airgas portfolio? I’m thinking the chemical distribution, like the Urea or the

CO2 businesses, your perspective on whether those are core or not?

BP: Okay, Pierre, you can just take the questions.

PD: Yes. The ERP system that Airgas has invested

in is perfectly tailored to the business that they have, and the business that they have is going to be the bulk of the business

that we have. I mean, they have five billion sales. We have one billion sales. So, basically, the ERP system has to be that Airgas

has to be kept, in order to make sure that we don’t destroy the value of their distribution system. So, we will keep their

ERP system for our merchant business. As to production capacity, basically, Airgas of course has not been a production capacity-driven

player through the years. They’ve had capacity when they could not easily buy the product from the market, so, they’re

still in a structural deficit of production for their business, so, they are buying and they are producing. Whereas, Air Liquide

has always been driven by the production side, as we rely on piggyback from large industries quite a bit. So I think the mix is

going to be able to rebalance the supply portfolio, I would say, more towards production than buying, although they’ll be

some buying left. So we don’t see, at this stage, major production capacity increases. I think we’ll rebalance theirs

with ours, and that way make it a more balanced system. As to what we tend to call the other businesses, chemicals, ammonia, that

sort of thing, it’s the same strategy. Airgas has the same strategy for those that they have for hardgoods, in

that their aim is to touch the customers in

as many ways as they can, and a lot of their customers have asked them to see if they can help them with those business lines,

which are reasonably small. They have. So basically, what we need to look at it the stability of these links between getting these

businesses into the customer channel, distribution channel, versus what they bring to the overall profitability. So the strategy

is not to be in those businesses, per se, the strategy is to be in those businesses as a way to satisfy customer demand, for those

customers that have gas needs at the end.

M: Thank you.

Benoît Poitier: Thank you, next question.

F: The next question will come from Neil Tyler,

from Redburn.

Neil Tyler: Good morning, thank you. A couple

from me, please. Just wonder if you could share with us what thoughts or discussions you’ve had already on the regional density

and overlap, and how that’s likely to be perceived by the antitrust authorities. If you could help us through your thought

process there? Secondly, with regards to the asset consolidation and efficiency, I suppose asking Laurence’s question another

way, do you expect the combination to lead to a reduced need for future capex in the combined business? Then thirdly, you mentioned

the blueprint that you talked about in Canada, for pushing the technology services through the business. I wonder if you could

help us understand how that has impacted the growth of your business, relative to the market. Thank you.

BP: Okay, I’ll take the first, and Pierre

will take the two others. In terms of the rules normally applied by the antitrust authority in the US, we are quite familiar, of

course, with the history and what is normally required, so we have prepared ourselves quite well for that. In a nutshell, the bulk

business as such is all about density in a certain region, with the HHI index, in other words, producing assets in the region and

the potential overlap of plants from two competitors. So, we know quite well what the rules are, and we’re rather clear about

what we should expect from the antitrust authority, and it’s something that we’ve gone through several times in our

history. The cylinder business is normally different, because it’s a very local business, so the way the relevant markets

are defined is quite different, because over 50 or 100 miles, there’s absolutely no influence between two different markets.

So, we’ve made this sort of analysis already, and we are well-prepared to start the discussions with the antitrust authorities,

but it’s based on our own experience but also all the previous cases that have been made and decided in the US. Overall,

I would say we are confident with two separate markets, bulk on the one side, and cylinder on the other side. Hardgoods is very

different, because hardgoods is a totally different market. Asset efficiency and blueprint, and the example of Canada, Pierre?

PD: Thanks for the question, Neil. Yes, we

expect the capex of the joint merchant business of Airgas and everything in the US to be slightly less than what it is today individually.

What we don’t know yet, because the markets are evolving very fast, is the amount of investment that will be required for

the digital part of the business, but as far as everything to do with production, with the maintenance and broad capex in production,

with the cylinder investments and all of these kinds of things, we expect the combined capex to be less than the sum of the parts

we have today.

As far as Canada goes, Canada is structured

slightly differently than Airgas, but has the same overall, I would say, strategic positioning in the market. We touch the customers

directly, on the small customers as much as the medium and large ones. We touch them with the one-stop shop strategy, and because

we touch them directly and have a high density of facilities in Canada to touch those customers, every time we have a new offer

that we develop in the group, it’s very directly deployed in

Canada, because we are basically on top of

what the distribution channels are. Whether it’s a new technology in distribution efficiency, or it’s a new technology

in applications, in Canada we’re able to deploy that extremely fast and extremely effectively. If you look at the historical

growth rates of our business in Canada in IM, it has been very good. So there’s no question that this model of touching,

in a North American context, it might be different in other places, being able to touch the customers in all segments and sizes

directly has a big advantage when you’re trying to deploy anything new.

NT: Thank you. Are you able to, sort of, quantify

the growth differential that you described there, in terms of basis points versus the market, or just broadly speaking?

PD: Well, I could make the calculations. I

don’t have those numbers at the top of my head, but clearly the performance of Canada from growth and margin increase has

been superior to the IM business in the US for a long time, so clearly there is an impact, but I cannot tell you exactly how much.

To include this in your model, we’ll have to wait a few weeks until we figure it out. (TC: 00:40:00) Thank you, Neil.

NT: Bye.

BP: Okay, thank you. Next question.

F: The next question comes from Andrew Benson,

from Citi.

Andrew Benson: Thanks very much. A few questions,

number one, can you define how you go about campaigning accretion in terms of EPS? Is it before amortisation charges, as opposed

to post-amortisation, just to understand your thought processes, given the bandwidth of the share issue, and the timing of the

share issue, as well? Secondly, is this a platform for getting into US home care? Thirdly, can you talk about your aspirations

for cash generation over the next few years, in order to pay down the debt? Lastly, a little bit philosophical, you’ve always

fought shy of cylinder business in North America. I think in the distant past you may have been sold some assets, to Airgas, your

principle focus has been on the development of tonnage. I’m just wondering, why this quite substantial change in strategic

direction, away from growth through large industries and tonnage on a global basis through to regionalised, localised cylinder

activities?

BP: I think Fabienne will take the first two

questions, and I’ll take the third one.

Fabienne Lecorvaisier: When we talk about accretion

on an earning per share assumption, it’s of course a performer based on the 12-month ownership, based on the refinancing

they want. Meaning, having the equity increase on day one, of course it’s not going to happen like that, but this is what

we have in our assumptions. It’s, of course, after amortisation charges, after purchase price account and whatever. It’s

a full-year performer accretion that we have forecasted. Cash generation, of course, this combined group will be very strong in

generating cash flow, and as we said, we are determined to keep an A rating, A-A, of course, we lose A+, no question. We will be

managing the groups so that the debt is progressively reduced over years. We expect the gearing to be under 100%, if not day one,

very rapidly.

BP: Just before I go to the strategy, we’ve

been very, very careful in the way we’ve planned the cash generation for the overall acquisition, to make sure that rather

soon, we were in a position not only to pay the interest of the debt and pay all the dividends, but also to generate additional

cash to start reimbursing the date, nearly on day one. I think we have quite a solid plan to actually generate these

cash flows to reduce the capital employed.

Interesting question about strategy and tonnage, you’re right that in the US, we’ve been rather shy in the development

of our cylinder business, but this is mainly due to the history of early key development in the US. Fundamentally, the cylinder

business is a good cash generation unit within early key. This is the case in Europe, and this is the case everywhere where we

have the density that is required for really doing good business and selling well to our customers. The history of early key in

the US has been such that just about half a century ago, we had to sell all businesses that were not majority-owned businesses,

just after the war. This is why in the US, we were organised to sell. When we came back about ten, fifteen years later, we had

to actually make a certain number of acquisitions in different places, but we never had the sort of scale and density that was

required in the US to be really successful.

We had this density in Canada, and this is

why the metal fab business in Canada is doing well, and we have, overnight, this sort of technology transfer from Europe to Canada,

to really make it even more successful. The problem in the US was a scale problem, a density problem, and this is why we decided

to sell this business a few years ago. Now, in parallel, about 30 years ago, we had this opportunity to buy big three industries,

and really started a significant tonnage business, which is now successful. The same applies to tonnage, this is a successful business

in the whole world, and we have the density that is required to make reasonable and good margins in this business. Now, this opportunity

with Airgas is giving us, really, the density, the distribution channels and the access to customers that is required to be successful.

That's why we think it’s not a change in the strategy, it’s just an opportunity, which is unique, in our eyes, to take

a position to give us what we need to be successful.

Now, if we look at the way the Airgas has been

built over time, it has been built through acquisition, so it was more a conglomerate of acquisitions in the past, but we consider,

today, through the diligence process, it was really proven that, Pierre mentioned that earlier, that this is really an operating

company. A company that has really, in particular in the past five years, created the good base required in the cylinder business

to be successful. So, it’s not really a change in strategy. It’s an opportunity to have the base which is required

to be successful, and that’s why we think it is a fantastic opportunity for us.

AB: That’s extremely helpful. Just one

point, is this a base for being able to get into home care?

BP: To healthcare, you mean?

AB: To the home care franchise.

BP: No, it’s a different business. Of

course, the presence will be there. In other words, we’ll have gas available in stores, but the home health care is more

a service business. So, it’s not the idea behind. The idea is really to develop the cylinder business. Now, through the presence

that we’re going to have, we mentioned 1,100 locations, there will be plenty of new opportunities. We are really confident

that we can develop the US market a little bit differently, but to start with, home health care and cylinder business are quite

different.

AB: That’s very clear. Thank you very

much.

BP: Thank you. Next question?

F: The next question comes from Gunther Zechmann

from Goldman Sachs.

Gunther Zechmann: Hi, good morning. Thanks

for taking my questions. I have three, if I may. Firstly, what’s the strategic mission in hardgoods, the 37% of sales? Quite

sizeable, and to that point, is it fair to assume that the synergies you want to harvest are mainly in the gas distribution? Secondly,

also to Andrew’s point with the health care, what’s the competition to that (inaudible 48.33)? You partly answered

it already, but if you could just outline the strengths of Airgas’s business. Lastly, more a numbers, technical question

on the hedging of the bridge loan, if you could just share with us what instruments you’ve used there, at what levels you’ve

hedged the currency exposure? Thank you.

BP: Pierre, do you want to take the first?

I’ll take the second, and Fabienne the third.

PD: Yes, the Airgas strategy on hardgoods is

really to make it complementary to the gas sales, gas sales being the priority. A lot of customers, especially in the smaller segments,

a lot of the customers require a one-stop shop for their cylinders and hardgoods, so if you’re not in the hardgoods, you

have a gap in your service offering to those customers. So it’s completely integrated, as is the safety business, which is

on the same wavelength. So strategically, it’s important to maintain the hardgoods strategy that has been successful for

years in the business that we are going to be integrated. Part of the reason why we were shy on that market in the US in previous

years is that we just did not have (TC: 00:50:00) the ability to do this joint one-stop shop thing very effectively. If you need

just one KPI to demonstrate that, most of the businesses that Airgas has been buying over the years, the small distributors, are

roughly averaging about 50/50 between gas and hardgoods. Airgas has been able to transform this into an almost 2/3, 1/3 mix. So

it’s proved that they are not optimising on hardgoods, from a sales perspective. They’re optimising on gas, but they’re

optimising the hardgoods from a supply chain perspective, to make sure that the contribution margin of hardgoods is okay. So this

is the strategy, and we’re going to keep that strategy. You’re right on the synergies. Since we don’t have any

hardgoods businesses in the US, the cost synergies are going to be mostly on the gas side, and the volume synergies, also mostly

on the gas side.

BP: Right, the health care thing, I answered.

The only synergy that we could think about between the cylinder gas and the healthcare, home care, would be related to the long-term

oxygen therapy, in other words, the delivery of oxygen to COPD patients. It’s a product synergy, but again, I think to start

with, we don’t need to dream too much about huge synergies. I think we are doing this acquisition to really have a critical

mass in cylinders. It will give us presence everywhere, we might use this presence in the future to develop other businesses, but

we are going to be highly focused, to start with, to generate all the synergies that are planned, and if there are other opportunities,

they will come in due time. Hedging and bridge loans, Fabienne?

FL: The bridge loan is underwritten in US dollars

and will be drawn in US dollars. We are considering contingent hedging, but we think for the Airgas shareholder meeting, we need

to improve the deal before implementing that.

BP: Thank you. We still have a certain number

of questions, so we are not going to be able to answer all those questions now, but you have to know that there will be another

presence of Air Liquide in London today, Fabienne, today and tomorrow. We will be in New York and Boston, as well, so if some of

you can also have access to Fabienne or ourselves in the US, we can go on with the discussion. So for the time left, I would suggest

that you just limit yourself to one question, and we can take two or three questions maximum. So next one, please. (Pause 53.07-53.17)

Next question?

F: We now take the next question from Patrick

Lambert from Raymond James.

Patrick Lambert: Hi, good morning. Just one

question, then. Can you describe a little bit more the 210 million cost synergies that you expect, in terms of where you see them,

in which buckets you put them, G&A, distribution, etc? Thanks.

BP: Right. Thank you. Pierre?

PD: Yes, the synergies, the buckets, as you

call them, as described, at least, in overall buckets on slide 22. We will have a number of sourcing benefits. We will have a reduction

in distribution costs, as we optimise the distribution with plans that are located slightly differently. We have some G&A reduction,

of course, at two levels. At the level of Airgas no longer operating as a publicly listed companies, and in corporate functions,

where we integrate ours with theirs, within the framework of the SAP system that they’ve built. So all of those are the key

cost synergies that we have. We’ve done this analysis in minute detail. Of course, we don’t have all the information

about Airgas that we will need to finalise everything, but I mean, being in the same market we know them well enough that we know,

and with the due diligence, we pretty much know, I would say, the first actions from cost synergies. So basically, it’s a

good part of efficiency, mostly, in bulk production and distribution, and then together with distribution efficiency and lots of

G&A, given the fact that we don’t need two accounting departments, two procurement departments, two of everything else

within the merchant business anymore.

PL: Great, thanks.

BP: Thank you. Next question.

F: We’ll now take the next question from

Stephen Kippett (ph 55.49) from Commerzbank.

Stephen Kippet: Thank you. Just a quick one,

with regards to the rating environment. I assume that you’ve probably had some tentative conversations with S&P before.

Is the variability that you have in the equity component of the whole deal something that you would use to avoid a two-notch downgrade?

Or would you, at least for an intermediate period of time, also be happy with being an A- company, as opposed to maybe an A flat

company, in terms of S&P rating.

BP: Fabienne?

FL: Well, the discussion is just starting with

the rating agencies. It’s obviously an arbitrage to be found. The objective is really to keep the A category, and to be back

to at least A very rapidly. As I said in the beginning, it could be A- for a short period of time. That’s clearly why we’ve

kept some flexibility and said that the equity bucket will be from two to three billion, but it’s really a little bit early

to be more precise than that. Three to four, sorry.

SK: Alright, thank you very much.

BP: Thank you. Next question?

F: We’ll now take the next question from

Peter McKay from Exxon (ph 57.17).

Peter McKay: Morning, thank you. Yes, I’m

just thinking, obviously your strategic focus has shifted a bit since the last time this business was in play, you know, and at

that stage your focus was very much towards Asia. You’re talking about a rebalancing and a convergence of growth rates globally,

now,

how should we think about this impacting your

portfolio of opportunities, which are still fairly substantial, and your attitude towards the, sort of, product bidding environment

at the moment? Do you feel in any way restricted by this deal, in terms of potential products that you can bid on, or are you shifting

your focus to regions outside Asia?

BP: Well, thank you. This is of course a very

important question. We’ve made all the assumptions in the business plan that we would keep the same pace of development in

the other businesses, that is to say the large industry, electronics and healthcare, but we also know that independently from this

acquisition, we have to be highly selective in the deals we sign in the world. If we look at the experience over the past five

years of China, where a lot of deals were signed in the steel market in the past, and then the chemical market was probably the

most active one, now it’s even more different. We have more core diversification and energy markets, so we’ve been

going through this transformation in the market. We think that the key is really to be selective in terms of market segments, quality

of bases (ph 59.17) and customers. Also, competitiveness of sites. So, it will just reinforce the selectivity of our deals, but

our main assumption is going to be, we go on with the strategy where we think there are sound projects to be developed. So, it

won’t really affect, fundamentally, the other businesses, but we are going to be more sensitive to cash generation, and of

course the returns are not going to change. We have this objective of going back to double-digit returns in five, six years, and

we are going to manage the company to achieve that objective.

PM: If I can (TC: 01:00:00) just follow up

there with a suggestion of the round table in London earlier this year, that the competitive environment for projects has perhaps

eased a little bit with Air Products and Linde taking a bit more of a selective view. The feeling was that hurdle rates or target

rates might have been going up on projects, but you still feel the need to be more selective about those portfolio opportunities,

do you?

PD: Well, of course if we can we will try to

get better returns from our deals. This is a mix of customers’ view, but also our ability to really be innovative and competitive

in our solutions. I mean, returns are important. We have always said that, and we reaffirm it today. In all our businesses, we

are trying to get the maximum returns that we can from the business in a given time. So, we have the same type of spirit. In all

businesses, we’re trying to get the best out of the assets we invest. I can take the very last question, and then we close.

F: We’ll take the last question now from

Thomas Gilbert from UBS.

Thomas Gilbert: Thank you very much for taking

my question. Two small ones. Can you quantify integration costs in the P&L, so exceptional items, cash cost for integration

and timing, and can you also say whether there is any type of break fee arrangement in place if either of you is walking away from

the deal? Thank you.

PD: Okay, Fabienne, take the first. I’ll

take the second.

FL: Yes, the integration costs are taken into

account in the P&L, and what we present to you as the synergies are synergies net of implementation cost. Break-up fee?

PD: Well, break-up fee, we have negotiated

break-up fees, but they are really customary break-up fees, and they are always a certainty in deals like that, so it was part

of our discussions. They are balanced and well in line with the market practices. So, I mean, in that regard, this is a normal

deal, and probably the most sensitive one is the antitrust one. We are highly confident that we have, already on

the table, what should be normally accepted

by the authorities, but of course we need to start the discussions with them. In terms of break-up fees, this is just market practice.

BP: Thank you very much, again. We will be

available in different places. Fabienne will be in London, I will be with Pierre in New York, first today, at the end of this day,

and then Pierre will stay in New York, I will be in Boston. So, you will have other opportunities to join us, and of course, we

will be back into Paris on Friday with Fabienne. Thank you very much, and again, very good acquisition, game-changing, and hopefully

it will be approved through the approval process. Thank you very much, have a good day. Bye.

15

Airgas (NYSE:ARG)

Historical Stock Chart

From Mar 2024 to Apr 2024

Airgas (NYSE:ARG)

Historical Stock Chart

From Apr 2023 to Apr 2024