UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

FORM 10-K/A

(Amendment No. 2)

☒ ANNUAL REPORT PURSUANT TO SECTION

13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2022

or

☐ TRANSITION REPORT PURSUANT TO SECTION

13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________to____________

Commission file number: 000-56013

JRSIS HEALTH CARE CORPORATION

(Exact name of registrant as specified in its charter)

| Florida | | 46-4562047 |

| State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization | | Identification No.) |

3/F Building A, De Run Yuan

No. 19 Chang Yi Road, Chang Ming Shui

Wu Gui Shan, Zhong Shan City 528458

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including

area code: +86-760-88963658

Securities registered pursuant to Section 12(b)

of the Act:

| Title of Each Class |

|

Name of Each Exchange on Which Registered |

| None |

|

Not Applicable |

Securities registered pursuant to Section 12(g)

of the Act:

Title of Each Class

Common Stock, $0.001 par value

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the prece$786,559ing

12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant

has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No

☐

Indicate by check mark if disclosure of delinquent

filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to

the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this

Form10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant

is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report. ☐

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error

corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive

officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule12 b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s

voting common stock held by non-affiliates computed by reference to the closing price as of the last business day of the quarterly period

ended June 30, 2022 was $786,560.

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each

of the registrant’s classes of common stock, as of the latest practicable date.

As of the date of filing of this report, there

were 58,366,569 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

AMENDMENT NO. 2

This Amendment No. 2 to the Annual Report

of JRSIS Health Care Corporation for the year ended December 31, 2022 has been filed to provide additional disclosure in Item 1: Business

and Item 1A: Risk Factors pertaining to the operations of Laidian Technology (Zhongshan) Co., Ltd. within the People’s Republic

of China. No other Items within the Report have been amended, nor has the disclosure in the Report been updated. Investors should refer

to the filings in the SEC’s EDGAR system after the Annual Report for more current information about JRSIS Health Care Corporation.

Table of Contents

PART I

Cautionary Statement Regarding Forward Looking

Statements

The discussion contained in this Annual Report

on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the United States Securities Act of

1933, as amended, and Section 21E of the United States Securities Exchange Act of 1934, as amended. Any statements about our expectations,

beliefs, plans, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. These statements

are often, but not always, made through the use of words or phrases like “anticipate,” “estimate,” “plans,”

“projects,” “continuing,” “ongoing,” “target,” “expects,” “management

believes,” “we believe,” “we intend,” “we may,” “we will,” “we should,”

“we seek,” “we plan,” the negative of those terms, and similar words or phrases. We base these forward-looking

statements on our expectations, assumptions, estimates and projections about our business and the industry in which we operate as of the

date of this Form 10-K. These forward-looking statements are subject to a number of risks and uncertainties that cannot be predicted,

quantified or controlled and that could cause actual results to differ materially from those set forth in, contemplated by, or underlying

the forward-looking statements. Statements in this Form 10-K describe factors, among others, that could contribute to or cause these

differences. Actual results may vary materially from those anticipated, estimated, projected or expected should one or more of these risks

or uncertainties materialize, or should underlying assumptions prove incorrect. Because the factors discussed in this Form 10-K could

cause actual results or outcomes to differ materially from those expressed in any forward-looking statement made by us or on our behalf,

you should not place undue reliance on any such forward-looking statement. New factors emerge from time to time, and it is not possible

for us to predict which will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any

factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement.

Except as required by law, we undertake no obligation to publicly revise our forward-looking statements to reflect events or circumstances

that arise after the date of this Form 10-K.

ITEM 1. BUSINESS

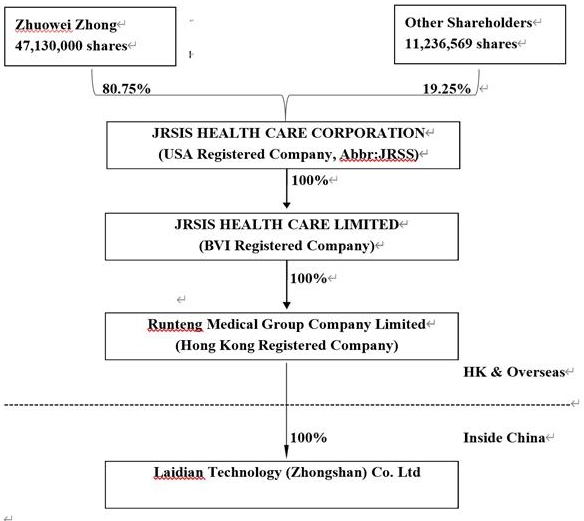

Identification of Consolidated Entities

JRSIS Health Care Corporation is a Florida corporation

whose business operations are carried out in the People’s Republic of China (“China” or the “PRC”) by Laidian

Technology (Zhongshan) Co., Ltd. JRSIS Health Care Corporation owns 100% of the equity in Laidian Technology (Zhongshan) Co., Ltd. through

two wholly owned subsidiaries: JRSIS Health Care Limited and Runteng Medical Group Company Limited.

In this Report, JRSIS Health Care Corporation

and its subsidiaries are identified as follows:

| ● | “JRSIS” identifies JRSIS Health Care

Corporation, a Florida corporation. |

| ● | “JRSIS–BVI” identifies JRSIS

Health Care Limited, a wholly-owned subsidiary of JRSIS that is organized in the British Virgin Islands (“BVI”). |

| ● | “Runteng” identifies Runteng Medical

Group Company Limited, a wholly-owned subsidiary of JRSIS-BVI that is organized in Hong Kong. |

| ● | “Laidian” identifies Laidian Technology

(Zhongshan) Co., Ltd., a wholly-owned subsidiary of Runteng that is organized in the PRC. |

| ● | “Company” identifies JRSIS, JRSIS-BVI,

Runteng and Laidian as an entity consolidated for financial reporting purposes. |

Corporate Structure; Related Risks

JRSIS IS A HOLDING COMPANY INCORPORATED IN

THE STATE OF FLORIDA. IT HAS NO OPERATIONS. JRSIS IS THE DIRECT OWNER OF ONE SUBSIDIARY, JRSIS-BVI, WHICH HAS NO OPERATIONS BUT IS THE

DIRECT OWNER OF ONE SUBSIDIARY, RUNTENG, RUNTENG HAS NO OPERATIONS BUT IS THE DIRECT OWNER OF LAIDIAN. LAIDIAN IS ORGANIZED IN THE PRC

AND CARRIES OUT ALL OF ITS OPERATIONS IN THE PRC. ACCORDINGLY, INVESTORS IN JRSIS ARE NOT THE OWNERS OF A FLORIDA CORPORATION WITH OPERATIONS

IN CHINA, BUT RATHER ARE OWNERS OF A FLORIDA HOLDING COMPANY WHOSE PROSPERITY WILL DEPEND ON ITS INDIRECT OWNERSHIP THROUGH OFFSHORE ENTITIES

OF AN ENTITY ORGANIZED UNDER CHINESE LAW THAT CARRIES ON OPERATIONS IN THE PRC.

Our present corporate structure is as follows:

WE FACE VARIOUS LEGAL

AND OPERATIONAL RISKS AND UNCERTAINTIES RELATED TO HAVING OUR OPERATIONS IN CHINA. THE PRC GOVERNMENT HAS SIGNIFICANT AUTHORITY TO REGULATE

A COMPANY, SUCH AS LAIDIAN, THAT IS ORGANIZED IN CHINA. FOR EXAMPLE, WE FACE RISKS ASSOCIATED WITH ANTI-MONOPOLY REGULATORY ACTIONS, AS

WELL AS OVERSIGHT ON CYBERSECURITY AND DATA PRIVACY. IN ADDITION, THE PRC GOVERNMENT HAS SIGNIFICANT OVERSIGHT AND DISCRETION OVER THE

CONDUCT OF LAIDIAN’S BUSINESS AND MAY INTERVENE WITH OR INFLUENCE THE OPERATIONS OF OUR BUSINESS AS THE GOVERNMENT DEEMS APPROPRIATE

TO FURTHER REGULATORY, POLITICAL AND SOCIETAL GOALS. THE PRC GOVERNMENT HAS RECENTLY PUBLISHED NEW POLICIES THAT SIGNIFICANTLY AFFECTED

CERTAIN INDUSTRIES SUCH AS THE EDUCATION AND INTERNET INDUSTRIES, AND WE CANNOT RULE OUT THE POSSIBILITY THAT IT WILL IN THE FUTURE RELEASE

REGULATIONS OR POLICIES REGARDING LAIDIAN’S INDUSTRY THAT COULD ADVERSELY AFFECT ITS BUSINESS, FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.

MOREOVER, THE PRC

GOVERNMENT, BY ITS AUTHORITY OVER LAIDIAN, HAS THE ABILITY TO EXERT INFLUENCE ON THE ABILITY OF JRSIS, TO ACCEPT FOREIGN INVESTMENTS OR

LIST ON U.S. OR OTHER FOREIGN EXCHANGES. SUCH RISKS COULD RESULT IN A MATERIAL CHANGE IN OUR OPERATIONS AND/OR THE VALUE OF JRSIS COMMON

STOCK OR COULD SIGNIFICANTLY LIMIT OR COMPLETELY HINDER OUR ABILITY TO OFFER, OR CONTINUE TO OFFER, OUR COMMON STOCK AND/OR OTHER SECURITIES

TO INVESTORS AND CAUSE THE VALUE OF SUCH SECURITIES TO SIGNIFICANTLY DECLINE OR BE WORTHLESS. FOR EXAMPLE, ON FEBRUARY 17, 2023, THE CHINA

SECURITIES REGULATORY COMMISSION, OR CSRC, ISSUED THE TRIAL ADMINISTRATIVE MEASURES OF OVERSEAS SECURITIES OFFERING AND LISTING BY DOMESTIC

COMPANIES, OR THE “TRIAL MEASURES”, WHICH BECAME EFFECTIVE ON MARCH 31, 2023. PURSUANT TO THE TRIAL MEASURES, COMPANIES ORGANIZED

IN CHINA THAT SEEK TO OFFER OR LIST SECURITIES OVERSEAS, BOTH DIRECTLY OR INDIRECTLY THROUGH A PARENT COMPANY, MUST FULFILL A FILING PROCEDURE

AND REPORT RELEVANT INFORMATION TO THE CSRC. TO DATE, WE HAVE NOT RECEIVED ANY INQUIRY, NOTICE, WARNING OR SANCTIONS FROM THE CSRC OR

ANY OTHER PRC GOVERNMENTAL AUTHORITIES RELATING TO THE LISTING OF JRSIS COMMON STOCK ON THE OTC PINK MARKET. AS THE TRIAL MEASURES ARE

NEWLY PUBLISHED AND THERE IS UNCERTAINTY WITH RESPECT TO THE FILING REQUIREMENTS AND THE IMPLEMENTATION, IF WE ARE REQUIRED TO SUBMIT

TO THE CSRC AND COMPLETE THE FILING PROCEDURES IN CONNECTION WITH ANY FUTURE SECURITIES OFFERING BY JRSIS, WE CANNOT BE SURE THAT WE WILL

BE ABLE TO COMPLETE SUCH FILINGS IN A TIMELY MANNER. ANY FAILURE OR PERCEIVED FAILURE BY US TO COMPLY WITH SUCH FILING REQUIREMENTS UNDER

THE TRIAL MEASURES MAY RESULT IN FORCED CORRECTIONS, WARNINGS AND FINES AGAINST US AND COULD MATERIALLY HINDER OUR ABILITY TO OFFER JRSIS

SECURITIES.

IN ADDITION, CHANGES IN THE LEGAL, POLITICAL

AND ECONOMIC POLICIES OF THE CHINESE GOVERNMENT, THE RELATIONS BETWEEN CHINA AND THE UNITED STATES, OR CHINESE OR U.S. REGULATIONS MAY

MATERIALLY AND ADVERSELY AFFECT OUR BUSINESS, FINANCIAL CONDITION AND RESULTS OF OPERATIONS. ANY SUCH CHANGES COULD SIGNIFICANTLY LIMIT

OR COMPLETELY HINDER OUR ABILITY TO OFFER OR CONTINUE TO OFFER JRSIS SECURITIES TO INVESTORS AND COULD CAUSE THE VALUE OF OUR SECURITIES

TO SIGNIFICANTLY DECLINE OR BECOME WORTHLESS. FOR EXAMPLE, ON DECEMBER 28, 2021, THE CYBERSPACE ADMINISTRATION OF CHINA (THE “CAC”)

JOINTLY WITH THE RELEVANT AUTHORITIES FORMALLY PUBLISHED MEASURES FOR CYBERSECURITY REVIEW (2021) WHICH TOOK EFFECT ON FEBRUARY 15, 2022

AND REPLACED THE FORMER MEASURES FOR CYBERSECURITY REVIEW (2020). MEASURES FOR CYBERSECURITY REVIEW (2021) STIPULATES THAT OPERATORS

OF CRITICAL INFORMATION INFRASTRUCTURE PURCHASING NETWORK PRODUCTS AND SERVICES AND ANY ONLINE PLATFORM OPERATOR WHO CONTROLS MORE THAN

ONE MILLION USERS’ PERSONAL INFORMATION MUST GO THROUGH A CYBERSECURITY REVIEW BY THE CYBERSECURITY REVIEW OFFICE IF IT SEEKS TO

HAVE ITS SECURITIES LISTED IN A FOREIGN COUNTRY. GIVEN THAT: (I) WE DO NOT POSSESS PERSONAL INFORMATION ON MORE THAN ONE MILLION USERS

IN OUR BUSINESS OPERATIONS; AND (II) DATA PROCESSED IN OUR BUSINESS DOES NOT HAVE A BEARING ON NATIONAL SECURITY AND THUS MAY NOT BE

CLASSIFIED AS CORE OR IMPORTANT DATA BY THE AUTHORITIES, WE DO NOT BELIEVE AN OFFERING OF SECURITIES BY JRSIS WOULD NECESSITATE AN APPLICATION

FOR A CYBERSECURITY REVIEW UNDER THE MEASURES FOR CYBERSECURITY REVIEW (2021). WE HAVE NOT, HOWEVER, ENGAGED PRC LEGAL COUNSEL TO PROVIDE

ANY OPINION OR ASSURANCE AS TO OUR UNDERSTANDING OF THE IMPLICATIONS OF THE CRSC OR CAC REGULATIONS FOR OUR FUTURE OPERATIONS. OUR STATEMENTS

IN THIS REPORT ARE BASED SOLELY ON OUR REVIEW OF THE REGULATIONS AND PUBLICLY AVAILABLE ANALYSES.

HOWEVER, SINCE THESE STATEMENTS AND REGULATORY

ACTIONS BY THE PRC GOVERNMENT AUTHORITIES ARE NEWLY PUBLISHED AND THE OFFICIAL GUIDANCE AND RELATED IMPLEMENTATION RULES HAVE NOT BEEN

ISSUED, IT IS HIGHLY UNCERTAIN WHAT THE POTENTIAL IMPACT SUCH MODIFIED OR NEW LAWS AND REGULATIONS WILL HAVE ON OPERATIONS OF LAIDIAN,

ITS ABILITY TO ACCEPT FOREIGN INVESTMENTS AND THE ABILITY OF JRSIS TO MAINTAIN A LISTING IN THE U.S. WITHOUT RECRIMINATION BY THE PRC

AUTHORITIES. IF THE CSRC, CAC OR OTHER REGULATORY AGENCIES IN THE FUTURE PROMULGATE LAWS, REGULATIONS OR IMPLEMENTING RULES REQUIRING

THAT WE OBTAIN THEIR APPROVALS FOR A SECURITIES OFFERING, THERE IS NO ASSURANCE THAT WE CAN OBTAIN THE APPROVAL, AUTHORIZATIONS, OR COMPLETE

REQUIRED PROCEDURES OR OTHER REQUIREMENTS IN A TIMELY MANNER, OR AT ALL. IN THE EVENT THAT LAIDIAN (I) DOES NOT RECEIVE OR MAINTAIN ANY

REQUISITE PERMISSIONS OR APPROVALS, (II) INADVERTENTLY CONCLUDES THAT SUCH PERMISSIONS OR APPROVALS ARE NOT REQUIRED, OR (III) APPLICABLE

LAWS, REGULATIONS, OR INTERPRETATIONS CHANGE AND LAIDIAN IS REQUIRED TO OBTAIN SUCH PERMISSIONS OR APPROVALS IN THE FUTURE, LAIDIAN MAY

BE SUBJECT TO SANCTIONS IMPOSED BY THE RELEVANT PRC REGULATORY AUTHORITY, INCLUDING FINES AND PENALTIES, REVOCATION OF THE LICENSES AND

SUSPENSION OF ITS BUSINESS, RESTRICTIONS OR LIMITATIONS ON THE ABILITY OF JRSIS TO PAY DIVIDENDS OUTSIDE OF CHINA, REGULATORY ORDERS,

INCLUDING INJUNCTIONS REQUIRING LAIDIAN TO CEASE BUSINESS OPERATION, LITIGATION OR ADVERSE PUBLICITY, AND OTHER FORMS OF SANCTIONS, WHICH

MAY RESULT IN A MATERIAL CHANGE IN THE OPERATIONS OF LAIDIAN, SIGNIFICANTLY LIMIT OR COMPLETELY HINDER THE ABILITY OF JRSIS TO OFFER SECURITIES

TO INVESTORS, AND THE MARKET PRICE OF JRSIS COMMON STOCK MAY SUBSTANTIALLY DECLINE OR BECOME WORTHLESS.

Prior Business Operations

JRSIS was incorporated on November 20, 2013 under

the laws of the State of Florida. In December 2013, JRSIS acquired 100% of the equity in JRSIS-BVIJRSIS-BVI, which is a privately held

Limited Liability Company registered in “BVI on February 25, 2013. JRSIS-BVI owns 100% of the equity in Runteng Medical Group Co.,

Ltd (“Runteng”), a limited liability company registered in Hong Kong on September 17, 2012. Until March 31, 2022, Runteng

owned 70% of the equity in Harbin Jiarun Hospital Co., Ltd (“Jiarun”). a for-profit hospital incorporated in Harbin City of

Heilongjiang, China in February 2006. The remaining 30% equity in Jiarun was owned by Junsheng Zhang, who is the Chairman of the Board

of JRSIS until April 28, 2022. Jiarun operates a private hospital serving patients on a municipal and county level and providing both

Western and Chinese medical practices to the residents of Harbin.

On April 12, 2022, Runteng organized and acquired

100% of the equity in Laidian, a wholly foreign-owned enterprise (“WFOE”) subsidiary. JRSIS established Laidian to engage

in the business of providing charging services to electric vehicles with the headquarter in Zhongshan City of Guangdong, China.

On April 28, 2022 JRSIS completed the spin-off

of its subsidiary Jiarun. as Runteng transferred its 70% equity interest in Jiarun to Zhang Junsheng (the “Spin-Off”). In

exchange for the 70% equity interest in Jiarun, Zhang Junsheng transferred 5,392,000 shares of JRSIS’ common stock to Runteng, which

surrendered the shares to the JRSIS treasury.

After the Spin-Off, JRSIS does not beneficially

own any equity interest in Jiarun. According to spin-off agreement on April 28, 2022, the effective date of spin-off was April 1, 2022.

Our Present Business

Until April 28, 2022, we operated Jiarun Hospital

and its two branch hospitals, collectively being a private hospital with 950 beds located in Harbin, the capital of Heilongjiang Province

in northeastern China. Jiarun Hospital offers patients care and pharmaceuticals in the areas of both Western and Chinese medical practices.

On April 28, 2022 JRSIS completed the spin-off

of its subsidiary Jiarun. On April 12, 2022, Runteng organized and acquired 100% of the equity in Laidian Technology (Zhongshan) Co.,

Ltd (“Laidian”), a wholly foreign-owned enterprise (“WFOE”) subsidiary. JRSIS established Laidian to engage in

the business of providing charging services to electric vehicles with the headquarter in Zhongshan City of Guangdong, China.

Laidian was organized in 2022 to engage in the

business of constructing and operating charging stations for electric vehicles (“EV”). JRSIS’s Board of Directors appointed

Zhuowei Zhong as JRSIS’s Chief Executive Officer primarily because he has extensive experience in the business of distributing and

operating EV charging stations. Our ambition is to build Laidian into a central participant in this growing industry.

In this, our first year of operation, we are focusing

our efforts on building a group of consulting clients who are themselves distributors of charging stations. We are undertaking this top-down

approach to the industry in part because we lack sufficient financial resources to compete directly with the major participant in the

industry. But of equal importance is the opportunity for market impact that we will gain by positioning ourselves as leaders in the charging

station industry. As those to whom we provide our services and guidance spread throughout the EV world, they will advertise our brand

as their authoritative source for technological and commercial knowledge about the charging station industry, and so our brand will gain

value among the relevant participants in the EV world. Our goal is that, when we have secured the financing necessary to compete in the

charging station community, we will already be known and identified with quality and know-how related to charging stations.

Our main business at this time, therefore, is

to provide consulting services relating to the planning and design of new energy charging piles to customer in Guangzhou City, the capital

of Guangdong Province of the PRC. Our customers are enterprises that are either initiating their participation in this industry in general

or expanding their operations to Guangzhou. In either case, a customer who engages Laidian, will receive, among other things:

| |

● |

a survey report on the distribution of new energy charging piles that have been built and are under construction in the district of Guangzhou City in which the customer intends to distribute its stations;, |

| |

● |

a business plan based upon an analysis of the existing distribution of charging piles in the target market; |

| |

● |

a site selection plan identifying prospective locations where charging piles can be built; |

| |

● |

a plan of the electric equipment design plus the type of charging piles to be used; |

| |

● |

a plan of the construction and the construction method; as well as |

| |

● |

the design and sample drawings of the foundation for the piles, |

Customers

At present, Laidian’s primary customer is Zhongke

Kuaichong (Guangzhou) New Energy Co., Ltd. Laidian is increasing its marketing efforts and is negotiating consulting agreements with a

number of customers. Laidian’s professional services have won high praise from existing and potential customers.

The Charging Station Industry in China

In recent decades, China’s rapid economic

growth has enabled more and more consumers to buy their own cars. The result has been the creation of the largest automotive market in

the world—but also serious urban air pollution, high greenhouse gas emissions, and growing dependence on oil imports. To counteract

those troubling trends, the Chinese government has imposed policies to encourage the adoption of plug-in electric vehicles (EVs). Since

buying an EV costs more than buying a conventional internal combustion engine vehicle, in 2009 the government began to provide generous

subsidies for EV purchases. As a result, China became the world’s largest market for EV’s, accounting for approximately 50%

of global sales. In 2020 1.1 million EVs were produced and sold in China. The central government’s “New Energy Vehicle Industry

Development Plan (2021 - 2035) predicted that sales of new energy vehicles would account for 20% of car sales in China in 2025. In fact,

during 2022, EV sales represented 22% of new car sales.

As the number of EV purchases grew, paying for

the subsidies became extremely costly for the government. As a result, beginning in 2020, China’s government began to phase out

the subsidies and instead rely on a mandate imposed on car manufacturers. The mandate requires that a certain percent of all vehicles

sold by a manufacturer each year must be battery-powered. To avoid financial penalties, every year manufacturers must earn a stipulated

number of points, which are awarded for each EV produced based on a complex formula that takes into account range, energy efficiency,

performance, and more. The requirements get tougher over time, with a goal of having EVs make up 40% of all car sales in China by 2030.

The mandate on vehicle manufacturers to produce

EVs is supplemented by a number of Chinese government policies:

| ● | Tax

exemptions. The Chinese government exempts electric vehicles from consumption and sales taxes, which can save purchasers tens of thousands

of RMB (equivalent to thousands of dollars). It also waives 50% of vehicle registration fees for electric vehicles. |

| ● | Procurement.

The Chinese government also uses its procurement power to promote electric vehicles. A May 2016 order required that half of new vehicles

purchased by China’s central government be new energy vehicles within five years. |

| ● | New

auto factory requirements. Chinese regulations strongly discourage the construction of factories for manufacturing internal combustion

engine vehicles only. Subject to exceptions that are difficult to satisfy, any new vehicle factory is required to include capacity for

the construction of electric vehicles. |

Since EVs will be useless without charging stations,

the Chinese central government has promoted the development of EV charging infrastructure as a matter of national policy. As the central

government has withdrawn subsidies for purchase of EVs, it has redirected a significant portion of those funds to support the development

of EV infrastructure, primarily charging stations. In November 2020, the General Office of the State Council promulgated its “Development

Plan of the New Energy Vehicle Industry (2021 - 2035), in which it mandated financial support for the construction of charging stations

and proposed preferential policies with respect to allocation of space in parking lots to charging stations. China State Grid and China

Southern Grid, China’s two state-owned electric utilities, both have programs to promote the development of electric vehicle charging

infrastructure.

Guangdong Province has also been aggressive in

support of EVs and EV infrastructure. During 2022 the number of EVs sold in Guangdong Province doubled compared to sales in 2021, and

now one-eighth of the EVs manufactured in the PRC are manufactured in Guangdong Province. To support this push toward EVs, Guangdong Province

now has more charging stations than any other province in China – and three times as many charging facilities as are located in

the entire United States. The Province subsidizes certain purchases of EVs, and encourages insurance companies to provide preferential

premiums for EVs. The government of Guangdong Province gives every indication that it will continue to support the expansion of the charging

station network indefinitely, with an ultimate goal of maximizing the conversion of vehicular traffic to electric.

Competition

Laidian is operating in the growing market of

new energy charging piles, which is becoming increasingly competitive due to the growing demand for electric vehicles and the government’s

push towards cleaner energy. The competition Laidian is facing can be broadly categorized into the following:

| 1. | Established

players: The new energy charging pile market is already populated with a number of established players such as State Grid, Southern Power

Grid, and other major energy companies. These companies have a strong brand presence, financial resources, and expertise in the energy

sector. They also have established relationships with customers and are likely to be strong competitors for Laidian. |

| 2. | New

entrants: The market for new energy charging piles is attracting a growing number of new entrants, ranging from start-ups to established

companies diversifying into the market. These competitors are also likely to be aggressive in pursuing market share and have the potential

to disrupt the market. |

| 3. | Technological

changes: The charging technology for electric vehicles is constantly evolving, and competitors are investing heavily in developing new

charging technologies such as wireless charging, fast charging, and ultra-fast charging. These technological changes could lead to new

entrants and disrupt existing market players. |

| 4. | Regulatory

environment: The regulatory environment for the new energy charging pile market is evolving rapidly, and competitors are likely to be

affected by changes in regulations and policies related to the development of the new energy industry. These changes could favor some

players and disadvantage others. |

In summary, Laidian is operating in a highly competitive

market, facing competition from established players, new entrants, technological changes, and regulatory environment changes. Laidian

is developing a strong value proposition and endeavoring to build a competitive advantage to succeed in the market.

Marketing

Laidian is developing a brand identity that reflects

Laidian’s values and mission. This includes developing a unique logo, website, and marketing materials that are visually appealing and

clearly communicate Laidian’s value proposition. Laidian also plans to further strengthen our marketing efforts and improve our brand

awareness through the following actions:

| 1. | Leverage

social media: Social media platforms such as WeChat, Weibo, and LinkedIn can be used to build awareness of our brand, share Company news

and updates, and engage with potential customers. Laidian can also consider partnering with influencers in the electric vehicle or sustainability

space to reach a wider audience. |

| 2. | Attend

industry events: Laidian will attend industry events such as trade shows, conferences, and seminars to network with potential customers

and partners. These events can also provide valuable insights into industry trends and customer needs. |

| 3. | Foster

partnerships: Laidian is seeking out partnerships with property developers, government agencies, and other companies in the new energy

space. By partnering with these organizations, Laidian can expand its reach and access new customer segments. |

| 4. | Overall,

by developing a brand identity, leveraging social media, attending industry events, and fostering partnerships, Laidian can build awareness

of its brand and generate leads in the highly competitive market. |

Intra-Company Transfer of Funds

In the Spring of 2022 JRSIS spun-off Jiarun Hospital,

the PRC entity that had been JRSIS’ sole operating company, and organized Laidian to serve as its sole operating company for the

immediate future. Since that restructuring, no funds have been transferred from JRSIS (or its subsidiaries) to Laidian or from Laidian

to JRSIS (or its subsidiaries), nor has any attempt been made to effect such a transfer of funds. JRSIS has paid no dividends or distributions

to its shareholders.

The business plan of Laidian aims for a significant

position in the Chinese market for charging stations. Accomplishment of that goal will depend, in large part, on the availability of capital

to finance operations, marketing and new installations. Our expectation, therefore, is that for the foreseeable future the net income

generated by the operations of Laidian will be needed to fund the expansion of those operations. Only when the market for charging stations

has matured and only if Laidian is then enjoying cash reserves in excess of that useful for growth, will Laidian be likely to distribute

earnings to JRSIS.

If it should occur that the cash reserves

of Laidian are sufficient to warrant a distribution of cash by Laidian, the funds will be distributed as a dividend payable to Runteng,

which would then pay a dividend or make a return of capital to JRSIS-BVI, which would then pay a dividend or return of capital, as appropriate,

to JRSIS. JRSIS could then dividend the cash to its shareholders or utilize the cash to expand its investments. We expect that JRSIS

will rely primarily on dividends paid in this manner for its cash needs, which will include administrative expenses and may, under appropriate

circumstances, include funds necessary to pay dividends and other cash distributions, if any, to our shareholders. However, because we

do not foresee any distribution by Laidian occurring in the foreseeable future, we have not developed formal cash management policies

with respect to inter-company transfers. We have made no such distributions to date and intend that the net cash generated by Laidian

will be used to expand that entity’s operations for the foreseeable future.

All dividends declared and payable upon the

equity interests in Laidian may be converted into foreign currency and be freely transferred out of the PRC, provided that (i) the declaration

and payment of such dividends complies with applicable PRC Laws and the constitutional documents of Laidian, and (ii) the remittance

of such dividends out of the PRC complies with the procedures required by the relevant PRC Laws relating to foreign exchange administration.

Even when circumstances would make it reasonable for Laidian to make

distributions to JRSIS (via its subsidiaries), it is not certain that government regulations will permit Laidian to make such distributions.

In general, the People’s Bank of China and the State Administration of Foreign Exchange, or SAFE, implement capital control measures

that severely restrict the flow of cash into and out of China. The primary measures restricting inflow and outflow of cash are the restrictions

on conversion of Renminbi into foreign currencies, such as the U.S. Dollar. Under existing PRC foreign exchange regulations, payments

of current account items, such as distributions of profits, interest payments, and trade and service-related transactions, can be made

by a Chinese enterprise in foreign currencies without approval by SAFE, provided certain registration procedures are completed. Therefore,

under current regulations, profits generated by the operations of Laidian could be distributed upstream to JRSIS, subject to the following

limitations:

| ● | Pursuant

to the Implementation Rules for the PRC Enterprise Income Tax Law, effective on January 1, 2008, dividends payable by a foreign

invested enterprise (“FIE”) to its foreign investors are subject to a withholding tax of up to 10%. |

| ● | Pursuant

to Article 10 of the Arrangement Between the Mainland of China and the Hong Kong Special Administration Region for the Avoidance of Double

Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income, effective December 8, 2006, dividends payable by

a FIE (such as Laidian) to its Hong Kong investor which owns 25% or more of the equity of the FIE is subject to a withholding tax of

up to 5%. |

| ● | PRC

regulations require that a FIE fund a statutory reserve fund by setting aside at least 10% of its after tax profits until the amount

of the fund reaches 50% of its registered capital. That reserve would necessarily reduce dividends payable. The transfer to this reserve

must be made before distribution of any dividend to shareholders. The surplus reserve fund is non-distributable other than during liquidation,

can be used to fund previous years’ losses, if any, and may be utilized for business expansion or converted into share capital

by issuing new shares to existing shareholders in proportion to their shareholding or by increasing the par value of the shares currently

held by them, provided that the remaining reserve balance after such issue is not less than 25% of the registered capital. |

| ● | The

PRC government may continue to strengthen its capital controls, and more restrictions and vetting procedures may be introduced by SAFE

for cross-border transactions. Any or all of these enhanced restrictions could limit the ability of Laidian to transfer funds upstream. |

These and any other limitations on the ability

of our PRC operating subsidiary to distribute dividends or other payments to its shareholder for transfer to JRSIS could materially and

adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends or otherwise

fund and conduct any business other than that carried on by Laidian.

In 2016, when the value of the Renminbi against

other currencies weakened, significant capital outflows from China occurred, which led the PRC government to impose more restrictive foreign

exchange policies. These included more thorough scrutiny of cross-border transactions classified as current account transactions. It would

not be surprising if the PRC government in the future further restricts the current accounts transaction window for outflows of cash.

Any such further restrictions would increase our difficulty in funding dividends paid from China to JRSIS.

JRSIS will be permitted

under PRC laws and regulations to provide funding to Laidian only through loans or capital contributions, and only if it satisfies the

applicable government registration and approval requirements. Any loans to Laidian will be subject to PRC regulations and foreign exchange

loan registrations. For example, loans by JRSIS to Laidian cannot exceed statutory limits and must be registered with the local counterpart

of the State Administration on Foreign Exchange (“SAFE”), or filed with SAFE in its information system. According to the Notice

of the People’s Bank of China and the State Administration of Foreign Exchange on Adjustments to Comprehensive Macro-prudential

Regulation Parameters for Cross-border Financing issued by the People’s Bank of China and the State Administration of Foreign Exchange

in March 2020, the limit for the total amount of foreign debt is 2.5 times its net assets. Moreover, any medium or long-term loan to be

provided by us to Laidian must also be filed and registered with the NDRC. We may also decide to finance our PRC subsidiary by means of

capital contributions. These capital contributions must be reported to the Ministry of Commerce, or MOFCOM, or its local counterpart.

In addition, a foreign invested enterprise is required to use its capital pursuant to the principle of authenticity and self-use within

its business scope.

PRC Laws and Regulations Requiring Laidian

to Secure Government Approval

Each aspect of the business operations of Laidian

and each aspect of the relationship of JRSIS and its subsidiary holding companies with Laidian is the subject of one or more regulations

imposed by the government of the PRC or the PRC Provincial governments. The risks of non-compliance are several: we could be denied a

necessary license or permission; we could inadvertently overlook the requirement to obtain a license or permission; we could obtain the

necessary license or permission but fail to comply with the regulations governing the regulated activity; or the regulations could change

in a way that interferes with our ability to carry out our business plan. Any of these situations could prevent us from carrying out our

business plan and result in loss to our investors.

The consequences of failure or inability to conform

our conduct to government policy will vary: the significance of the consequence will tend to reflect the level of concern that the government

holds for the subject of the regulation. If, when Laidian commences installation of charging stations, Laidian fails to comply with government

regulation of the operation of charging stations, the penalties could range from a fine to a revocation of its license to carry on the

charging station business. If we fail to comply with regulations regarding financial matters (securities offerings, cash flows, the corporate

structure itself), the penalties could range from significant civil penalties (e.g. revocation of business licensee) to criminal penalties.

Our business plan contemplates that we will use our access to U.S. capital markets to secure the capital we will need in order to grow

Laidian into a leading participant in the Chinese market for charging stations. If the CSRC or the CAC or any other government entity

were to restrict our ability to finance Laidian from the proceeds of security sales in the U.S., we would be forced to either secure an

alternative source of funds (which could result in significant dilution of our existing shareholders) or to severely reduce the pace of

our growth (which could doom our efforts at competitive strength).

We have tried to be scrupulous in ascertaining

the obligations that Chinese government regulations impose on us. In connection with the regulations that will be applicable to Laidian’s

charging station business, Laidian will primarily rely on the expertise of its Chairman, Zhuowei Zhong, who has many years of executive

experience in the charging station business. We have not, however, engaged PRC legal counsel to provide any opinion or assurance as to

our understanding of the implications of the CRSC or CAC regulations for our future operations. Our statements in this report are based

solely on our review of the regulations and publicly available analyses.

The following paragraphs classify the principal

regulations with which we must comply by reference to the aspect of our business to which they apply:

The Charging Station Business. At

the present time, Laidian serves only as a consultant to enterprises entering the charging station business. There are no government regulations

that apply to the consulting business, and so Laidian needs no government approvals to carry on this business. Our plan, however, is that

Laidian will in the future initiate its own implementation and operation of charging stations. The business of installing and operating

charging stations will require the involvement of the government at four points:

| ● | To

initiate the business of providing EV charging services, Laidian will be required to register with, and obtain approval from, the Development

and Reform Commission of each Province in which Laidian intends to do business; |

| ● | Prior

to each installation of a charging station, Laidian will be required to register the construction and operation plan for the charging

station with the Province or County and receive approval of the plan; |

| ● | Each

installation of a charging station requires a construction permit: if the charging station is being installed on an existing parking

lot or other commercial location, Laidian will require a construction permit from the local Land Reserve and Development Department;

if the installation will be made on raw land, Laidian will also require a zoning permit from the Residential Construction and Planning

Department of the local township. |

| ● | Prior

to placing any charging station into service, inspection and approval must be obtained from the local township, the construction department,

and the relevant electric utility. |

Securities Offering by JRSIS. JRSIS

has no immediate plan to make a securities offering. In the future, however, JRSIS anticipates that it will offer its securities to the

public in order to raise capital and fund the operations of Laidian. At that time, Laidian will be required to comply with the permission

requirements of the China Securities Regulatory Commission (the “CSRC”) and the Cyberspace Administration of China (the “CAC”)

in order for JRSIS to sell securities in the U.S. or elsewhere.

On February 17, 2023, the CSRC promulgated the

Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Administrative Measures”),

which took effect on March 31, 2023. The Trial Administrative Measures mandate that an issuer will be required to go through the filing

procedures under the Trial Administrative Measures if 50% or more of the issuer’s operating revenue, total profit, total assets

or net assets as documented in its audited consolidated financial statements for the most recent accounting year is accounted for by PRC

domestic companies and the main parts of the issuer’s business activities are conducted in mainland China, or its main places of

business are located in mainland China, or the senior managers in charge of its business operation and management are mostly Chinese citizens

or domiciled in mainland China. Accordingly, if and when JRSIS undertakes to make a public offering of its securities, Laidian will be

required to file with CRSC such information as CRSC shall require. Since the filing processes are currently being developed, we cannot

predict the difficulty of compliance or the extent to which compliance with CRSC regulations may hinder the ability of JRSIS to raise

money in the capital markets.

Securities Listing by JRSIS. The

common stock of JRSIS is currently quoted on the OTC Pink Market. JRSIS plans, at an undetermined future date when it is eligible, to

apply for an “uplist” to the OTCQB, NASDAQ or an exchange.

On December 28, 2021 the CAC and 12 other Chinese

government departments issued “New Measures for Cybersecurity Review.” According to Article 7 of the New Measures, network

platform operators holding personal information of more than one million users are required to apply to the Network Security Review Office

for a cybersecurity review before listing their securities in a foreign country. The cybersecurity reviewers will have broad discretion

to determine whether the offshore listing may affect China’s national security. In the event that Laidian, in the course of implementing

its plan to participate in the charging station industry, accumulates personal information from more than one million users of its charging

stations, it will be necessary for it to undergo the mandated security review before uplisting to an exchange. We cannot predict whether,

at that time, a listing of JRSIS common stock on a U.S. exchange will be considered to pose a threat to China’s national security.

We have not engaged PRC legal counsel to provide

any opinion or assurance as to our understanding of the implications of the CRSC or CAC regulations for our future operations. Our statements

in this report are based solely on our review of the regulations and publicly available analyses.

PRC Policies Regarding PCAOB Inspection of

Auditors

Pursuant to the Holding Foreign Companies Accountable

Act (“HFCAA”), as adopted by the United States Congress, the Public Company Accounting Oversight Board (the “PCAOB”)

issued a Determination Report on December 16, 2021 which found that the PCAOB was unable to inspect or investigate completely registered

public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one

or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position

taken by one or more authorities in Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting

firms which are subject to these determinations. Our registered public accounting firm, Centurion ZD CPA & Co. is headquartered in

Hong Kong and was identified in this report as a firm subject to the PCAOB’s determination. As a result, on May 13, 2022, the SEC

listed JRSIS as a Commission-Identified Issuer under the HFCAA, which made JRSIS subject to sanctions if the Hong Kong authorities continued

to prevent the PCAOB from inspecting our auditor. Under the HFCAA (as amended by the Consolidated Appropriations Act – 2023), JRSIS

securities may be prohibited from trading on a U.S. stock exchange or facility if our auditor is not inspected by the PCAOB for two consecutive

years, and this ultimately could result in JRSIS common stock being removed from the OTC Pink Market.

On August 26, 2022, the China Securities Regulatory

Commission (“CSRC”), the Ministry of Finance of China, and the PCAOB signed a protocol governing inspections and investigations

of audit firms based in China and Hong Kong. On December 15, 2022, the PCAOB issued

a new Determination Report which: (1) vacated the December 16, 2021 Determination Report; and (2) concluded that the PCAOB had been able

to conduct inspections and investigations completely in Hong Kong in 2022. The December 15, 2022 Determination Report cautions, however,

that authorities in Hong Kong might take positions at any time that would prevent the PCAOB from continuing to inspect or investigate

completely. As required by the HFCAA, if in the future the PCAOB determines it no longer can inspect or investigate completely because

of a position taken by an authority in Hong Kong, the PCAOB will act expeditiously to consider whether it should issue a new determination.

If the PCAOB is not able to fully conduct inspections of our auditor’s work papers in China, you may be deprived of the benefits

of such inspection which could result in limitation or restriction to our access to the U.S. capital markets and trading of JRSIS securities

may be prohibited under the HFCAA.

Enforceability of Civil Liabilities

At present, JRSIS has only three members of its

management team: Zhuowei Zhong, Zhifei Huang and Zhuowen Chen, each of whom is a member of the JRSIS Board of Directors and an executive

officer of JRSIS. As our operations expand, we expect to increase the numbers of our managers, both directors and officers. It is likely,

however, that all or most of our executives will also be residents of the PRC.

Shareholder claims that are common in the United

States, including securities law class actions and fraud claims, generally are difficult to pursue as a matter of law or practicality

in China. For example, in China, there are significant legal and other obstacles to obtaining information needed for shareholder investigations

or litigation outside China or otherwise with respect to foreign entities. Although the local authorities in China may establish a regulatory

cooperation mechanism with the securities regulatory authorities of another country or region to implement cross-border supervision and

administration, such regulatory cooperation with the securities regulatory authorities in the Unities States has not been efficient in

the absence of a mutual and practical cooperation mechanism.

Efforts by shareholders of JRSIS to obtain recourse

against the management of JRSIS in U.S. courts will likely also be unavailing. It will be difficult for the shareholders of JRSIS to effect

service of process upon members of our management who reside in China – in general, Chinese authorities will not assist in performing

the service. In addition, China does not have treaties providing for the reciprocal recognition and enforcement of judgments of courts

with the United States. In addition, according to the PRC Civil Procedures Law, courts in China will not enforce a foreign judgment against

us or our directors and officers if they decide that the judgment violates the basic principles of PRC law or national sovereignty, security

or public interest. Therefore, even if a shareholder were successful in obtaining judgment against an officer or director of JRSIS in

a U.S. court, recognition and enforcement in China of judgments of a court in the U.S. in relation to any matter not subject to a binding

arbitration provision may be difficult or impossible.

Taxes

Enterprise income tax is defined under the Provisional

Regulations of PRC Concerning Income Tax on Enterprises promulgated by the PRC. Income tax is payable by enterprises at a rate of 25%

of their taxable income.

Employees

As of December 31, 2022, we had 3 employees,

None of our employees are represented by a labor union or similar collective bargaining organization.

ITEM 1A. RISK FACTORS.

An investment in our common stock involves a high

degree of risk. You should carefully consider the following risk factors and other information in this 10K before deciding to invest in

our Company. If any of the following risks actually occur, our business, financial condition and results of operations could be seriously

harmed. As a result, the trading price of our common stock could decline and you could lose all or part of your investment.

Risks Related to Doing Business in China

The Company (i.e. JRSIS and its subsidiaries on

a consolidated financial basis) has a single source of revenue: Laidian, a limited company organized and operating in the PRC. This arrangement

imposes specific risks on investors in JRSIS:

Changes in China’s

economic, political or social conditions or government policies could have a material adverse effect on our business and operations. The

PRC government has recently indicated an intent to exert more oversight and control over overseas securities offerings and other capital

markets activities and foreign investment in China-based companies like us. Any such action, once taken by the PRC government, could significantly

limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to

significantly decline or,in extreme cases, become worthless.

All of our assets and

operations are located in China. Accordingly, our business, financial condition, results of operations and prospects may be influenced

to a significant degree by political, economic, and social conditions in China. The Chinese economy differs from the economies of most

developed countries in many respects, including the level of government involvement, level of development, growth rate, control of foreign

exchange and allocation of resources. Although the Chinese government has implemented measures emphasizing the utilization of market forces

for economic reform, the reduction of state ownership of productive assets, and the establishment of improved corporate governance in

business enterprises, a substantial portion of productive assets in China is still owned by the government. In addition, the Chinese government

continues to play a significant role in regulating the development of industry by imposing industrial policies.

The PRC government has

significant authority to exert influence on the ability of a China-based company, such as Laidian, to conduct its business and accept

foreign investments. Through exercise of its control over the China-bases subsidiary, the PRC government can also exercise significant

control over the decision of an offshore holding company, such as JRSIS, to list its securities on an U.S. or other foreign exchanges.

For example, JRSIS faces risks associated with regulatory approvals of securities offerings outside of China as well as oversight on cybersecurity

and data privacy. Such risks or any actions by the PRC government to exert more oversight and control over offerings that are conducted

overseas and/or foreign investment in China-based issuers could result in a material change in our operations and/or the value of our

common stock or could significantly limit or completely hinder our ability to offer or continue to offer our common stock and/or other

securities to investors and cause the value of such securities to significantly decline or be worthless.

The PRC government has

significant authority, oversight and discretion over the conduct of our business and may intervene with or influence our operations as

the government deems appropriate to further regulatory, political and societal goals. The PRC government has recently published new policies

that significantly affected certain industries such as the education and internet industries, and we cannot rule out the possibility that

it will in the future release regulations or policies regarding our industry that could adversely affect our business, financial condition

and results of operations. Furthermore, the PRC government has recently indicated an intent to exert more oversight and control over overseas

securities offerings and other capital markets activities and foreign investment in China-based companies like us. Any such action, once

taken by the PRC government, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors

and cause the value of such securities to significantly decline or in extreme cases, become worthless.

Recently, the PRC government

initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including

cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable

interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly

enforcement. Currently, we believe that these statements and regulatory actions have had no impact on Laidian’s daily business operations,

the ability of Laidian to accept foreign investments or the ability of JRSIS to list its securities on an U.S. or other foreign exchange.

Nevertheless, since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation

making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified

or promulgated, if any, and the potential impact of such modified or new laws and regulations.

Because all of our operations are in China,

our business is subject to the complex and rapidly evolving laws and regulations there. The Chinese government may exercise significant

oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time, which could result

in a material change in Laidian’s operations and/or the value of JRSIS’ common stock.

As a business operating in

China, Laidian is subject to the laws and regulations of the PRC, which can be complex and which evolve rapidly. The PRC government has

the power to exercise significant oversight and discretion over the conduct of Laidian’s business, and the regulations to which

Laidian is subject may change rapidly and with little notice to JRSIS or its shareholders. As a result, the application, interpretation,

and enforcement of new and existing laws and regulations in the PRC are often uncertain. In addition, these laws and regulations may be

interpreted and applied inconsistently by different agencies or authorities, and inconsistently with Laidian’s current policies

and practices. New laws, regulations, and other government directives in the PRC may also be costly to comply with, and such compliance

or any associated inquiries or investigations or any other government actions may:

| ● | Delay or impede our development, |

| ● | Result in negative publicity or increase our operating costs, |

| ● | Require significant management time and attention, and |

| ● | Subject Laidian to remedies, administrative penalties and

even criminal liabilities that may harm its business, including fines assessed for our current or historical operations, or demands or

orders that Laidian modify or even cease its business practices. |

The promulgation of new laws

or regulations, or the new interpretation of existing laws and regulations, that restrict or otherwise unfavorably impact the ability

or manner in which Laidian conducts its business could require Laidian to change certain aspects of its business to ensure compliance,

could decrease demand for Laidian’s products, reduce revenues, increase costs, require Laidian to obtain more licenses, permits,

approvals or certificates, or subject Laidian to additional liabilities. To the extent any new or more stringent measures are required

to be implemented, Laidian’s business, financial condition and results of operations could be adversely affected, which could materially

decrease the value of JRSIS common stock.

Increased regulation of offshore offerings

by the CSRC could restrict the ability of JRSIS to offer its securities to investors and could cause the value of our common stock to

significantly decline or become worthless.

On July 6, 2021, PRC government authorities

published the Opinions on Strictly Cracking Down Illegal Securities Activities in Accordance with the Law. These opinions call for strengthened

regulation over illegal securities activities and supervision on overseas listings by China-based companies. They propose to take effective

measures, such as promoting the construction of relevant regulatory systems, to deal with the risks faced by China-based overseas-listed

companies.

On December 24, 2021, the CSRC released the Draft

Rules Regarding Overseas Listing, which had a comment period that expired on January 23, 2022. The Draft Rules Regarding Overseas Listing

lay out the filing regulation arrangement for both direct and indirect overseas listing, and clarify the determination criteria for indirect

overseas listing in overseas markets. The Draft Rules stipulate that the Chinese-based companies, or the issuer, shall fulfill the filing

procedures within three working days after the issuer makes an application for initial public offering and listing in an overseas market.

The required filing materials for an initial public offering and listing should include at least the following: record-filing report and

related undertakings; regulatory opinions, record-filing, approval and other documents issued by competent regulatory authorities of relevant

industries (if applicable); and security assessment opinion issued by relevant regulatory authorities (if applicable); PRC legal opinion;

and prospectus.

In addition, an overseas offering and listing

is prohibited under any of the following circumstances: (1) if the intended securities offering and listing is specifically prohibited

by national laws and regulations and relevant provisions; (2) if the intended securities offering and listing may constitute a threat

to or endangers national security as reviewed and determined by competent authorities under the State Council in accordance with law;

(3) if there are material ownership disputes over the equity, major assets, and core technology, etc. of the issuer; (4) if, in the past

three years, the domestic enterprise or its controlling shareholders or actual controllers have committed corruption, bribery, embezzlement,

misappropriation of property, or other criminal offenses disruptive to the order of the socialist market economy, or are currently under

judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations; (5) if, in past

three years, directors, supervisors, or senior executives have been subject to administrative punishments for severe violations, or are

currently under judicial investigation for suspicion of criminal offenses, or are under investigation for suspicion of major violations;

(6) other circumstances as prescribed by the State Council. The Draft Administration Provisions defines the legal liabilities of breaches

such as failure in fulfilling filing obligations or fraudulent filing conducts, imposing a fine between RMB 1 million and RMB 10 million,

and in cases of severe violations, a parallel order to suspend relevant business or halt operation for rectification, revoke relevant

business permits or operational license.

On February 17, 2023, the CSRC promulgated the

Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Administrative Measures”),

which will take effect on March 31, 2023. Compared to the Draft Rules, the Trial Administrative Measures further clarified and emphasized

several aspects, including:

| i. | comprehensive determination of the “indirect overseas

offering and listing by PRC domestic companies” in compliance with the principle of “substance over form” and particularly,

an issuer will be required to go through the filing procedures under the Trial Administrative Measures if the following criteria are

met at the same time: a) 50% or more of the issuer’s operating revenue, total profit, total assets or net assets as documented

in its audited consolidated financial statements for the most recent accounting year is accounted for by PRC domestic companies, and

b) the main parts of the issuer’s business activities are conducted in mainland China, or its main places of business are located

in mainland China, or the senior managers in charge of its business operation and management are mostly Chinese citizens or domiciled

in mainland China; |

| ii. | exemptions from immediate filing requirements for issuers that

a) have already been listed or registered but not yet listed in foreign securities markets, including U.S. markets, prior to the effective

date of the Trial Administrative Measures, and b) are not required to re-perform the regulatory procedures with the relevant overseas

regulatory authority or the overseas stock exchange, c) whose such overseas securities offering or listing shall be completed before

September 30, 2023. However, such issuers shall carry out filing procedures as required if they conduct refinancing or are involved in

other circumstances that require filing with the CSRC; |

| iii. | a negative list of types of issuers banned from listing overseas,

such as issuers under investigation for bribery and corruption; |

| iv. | regulation of issuers in specific industries; |

| v. | issuers’ compliance with national security measures and

the personal data protection laws; and |

| vi. | certain other matters such as: an issuer must file with the

CSRC within three business days after it submits an application for initial public offering to competent overseas regulators; and subsequent

reports shall be filed with the CSRC on material events, including change of control or voluntary or forced delisting of the issuer(s)

who have completed overseas offerings and listings. |

We have not engaged PRC legal counsel to provide

any opinion or assurance as to our understanding of the implications of the CRSC regulations for our future operations. Our statements

in this report are based solely on our review of the regulations and publicly available analyses. The Draft Rules Regarding Overseas

Listing, if enacted, and the Trial Administrative Measures may subject us to additional compliance requirement in the future. If JRSIS

undertakes to raise capital through a securities offering, we cannot assure you that Laidian will be able to complete the filing processes

and secure the necessary clearance from the CSRC on a timely basis, or at all. Any failure by Laidian to fully comply with new regulatory

requirements may significantly limit or completely hinder the ability of JRSIS to offer its securities, cause significant disruption

to Laidian’s business operations, and severely damage Laidian’s reputation, which would materially and adversely affect our

financial condition and results of operations and cause JRSIS common stock to significantly decline in value or become worthless.

Rules recently

adopted by the Cyberspace Administration of China may restrict our ability to finance Laidian from the proceeds of securities offerings

by JRSIS.

On January 4, 2022 the

Cyberspace Administration of China (“CAC”) adopted rules mandating that an issuer who is a “critical information infrastructure

operator” or a “data processing operator” as defined therein and who possesses personal information of more than one

million users, and intends to have its securities listed for trading in a foreign country must complete a cybersecurity review by the

CAC. Alternatively, relevant governmental authorities in the PRC may initiate cyber security review if such governmental authorities determine

an operator’s cyber products or services, data processing or potential listing in a foreign country affect or may affect national

security. The rules became effective on February 15, 2022.

The new CAC rules do

not apply to Laidian at this time, as Laidian does not collect any personal information at this time. Nevertheless, the continued expansion

of business operations by Laidian could bring that company within the scope of authority of the CAC rules. CAC rules may also expand the

protections involved in collection of user information. Laidian may face challenges in addressing such enhanced regulatory requirements

and in making necessary changes to its internal policies and practices in data privacy and cybersecurity matters. If Laidian is unable

to develop the security structures required by the CAC, it may be prevented from collecting user data. In addition, if Laidian is unable

to satisfy the CAC’s cybersecurity review, it may be prevented by the CAC from accepting funds from JRSIS that arise from offshore

offerings of JRSIS common stock. In that event, our ability to finance the business of Laidian could be hindered, which could prevent

Laidian from achieving profitable operations.

We have not engaged PRC legal counsel to provide

any opinion or assurance as to our understanding of the implications of the CAC regulations for our future operations. Our statements

in this report are based solely on our review of the regulations and publicly available analyses.

If the Chinese government chooses to exert

more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, such action could

significantly limit or completely hinder the ability of JRSIS to offer or continue to offer securities to investors and cause the value

of such securities to significantly decline or be worthless.

The Chinese government has exercised, and continues

to exercise, substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Laidian’s

ability to operate in China may be harmed by changes in Chinese laws and regulations, including those relating to securities regulation,

data protection, cybersecurity and mergers and acquisitions and other matters. Central or local governments in the PRC may impose new,

stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on Laidian’s

part for compliance with such regulations or interpretations. Government actions in the future could significantly affect economic conditions

in China or particular regions thereof, and could require Laidian to materially change its operating activities. Laidian’s business

may be subject to various types of government and regulatory interference, such as requiring Laidian to gain approval from CSRC before

JRSIS makes a securities offfering and to conduct a cyber security review. Laidian may incur increased costs necessary to comply with

existing and newly adopted laws and regulations or penalties for any failure to comply. Laidian’s operations could be adversely

affected by existing or future laws and regulations.

Any of these events could result in a material

change in the operations of Laidian and the value of JRSIS common stock. The Chinese government has indicated an intent to exert more

oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers. Any such actions by

the Chinese government could significantly limit or completely hinder our ability to offer securities to investors and cause the value

of our securities to significantly decline or be worthless.

SAFE regulations relating to offshore investment

activities by PRC residents may increase our administrative burdens and restrict our overseas and cross-border investment activity. If

our shareholders and beneficial owners who are PRC residents fail to make any required applications, registrations, and filings under

such regulations, we may be unable to distribute profits and may become subject to liability under PRC laws.

China’s State Administration of Foreign

Exchange (“SAFE”) has promulgated several regulations, including Notice on Relevant Issues Concerning Foreign Exchange Administration

for PRC Residents to Engage in Financing and Inbound Investment via Oversea Special Purpose Vehicles, or “Circular No. 75,”

issued on October 21, 2005 and effective as of November 1, 2005 and certain implementation rules issued in subsequent years, requiring

registrations with, and approvals from, PRC government authorities in connection with direct or indirect offshore investment activities

by PRC residents and PRC corporate entities. These regulations apply to our shareholders and beneficial owners who are PRC residents,

and may affect any offshore acquisitions that we make in the future.

SAFE Circular No. 75 requires PRC residents, including

both PRC legal person residents and/or natural person residents to register with the local SAFE branch before establishing or controlling

any company outside of China for the purpose of equity financing with assets or equities of PRC companies, referred to in the notice as

an “offshore special purpose company.” In addition, any PRC resident who is a direct or indirect shareholder of an offshore

company is required to update his registration with the relevant SAFE branches, with respect to that offshore company, in connection with

any material change involving an increase or decrease of capital, transfer or swap of shares, merger, division, equity or debt investment

or creation of any security interest. Moreover, the PRC subsidiaries of that offshore company are required to coordinate and supervise

the filing of SAFE registrations by the offshore company’s shareholders who are PRC residents in a timely manner. If a PRC shareholder

with a direct or indirect stake in an offshore parent company fails to make the required SAFE registration, the PRC subsidiaries of such

offshore parent company may be prohibited from making distributions of profit to the offshore parent and from paying the offshore parent

proceeds from any reduction in capital, share transfer or liquidation in respect of the PRC subsidiaries, and the offshore parent company

may also be prohibited from injecting additional capital into its PRC subsidiaries. Furthermore, failure to comply with the various SAFE

registration requirements described above may result in liability for the PRC shareholders and the PRC subsidiaries under PRC law for

foreign exchange registration evasion.

Although we have requested our PRC shareholders

to complete the SAFE Circular No. 75 registration, we cannot be certain that all of our PRC resident beneficial owners will comply with

the SAFE regulations. The failure or inability of our PRC shareholders to receive any required approvals or make any required registrations

may subject us to fines and legal sanctions, restrict our overseas or cross-border investment activities, prevent us from making capital

injection into our PRC subsidiaries, limit our PRC subsidiaries’ ability to make distributions or pay dividends or affect our ownership

structure, as a result of which our acquisition strategy and business operations and our ability to distribute profits to you could be

materially and adversely affected.

Changes in current policies of the PRC government

could have a significant impact upon the business we conduct in the PRC and the profitability of our operations.

Current policies adopted by the PRC government

indicate that it seeks to encourage a market-oriented economy. We believe that the PRC government will continue to develop policies that

strengthen its economic and trading relationships with foreign countries and as a consequence, business development in the PRC will follow

current market forces. While we believe that this trend will continue, we cannot assure you that such beneficial policies will not change

in the future. A change in the current policies of the PRC government could result in confiscatory taxation, restrictions on currency

conversion, or the expropriation or nationalization of private enterprises, all of which would have a negative impact on our current corporate

structure and our operations. The PRC laws and regulations governing our current business operations are sometimes vague and uncertain.

Any changes in such PRC laws and regulations may have a material and adverse effect on our business.

There are substantial uncertainties regarding

the interpretation and application of PRC laws and regulations, including, but not limited to, those laws and regulations governing our