Prospectus Supplement

To Prospectus dated August 3, 2021,

as may be amended |

Registration Statement No.

333-258403

Dated August 3, 2021;

Rule 424(b)(2) |

Senior Debt Funding Notes, Series E

We, Deutsche Bank AG, may

offer and sell our senior debt funding notes (the “notes”) at one or more times. The specific terms of any notes that

we offer and sell will be included in a term sheet and/or pricing supplement. We refer to such term sheet and pricing supplement generally

as “pricing supplements.”

The notes will have the following

general terms:

| · | The notes may bear interest at any time at either

a fixed rate or a floating rate that varies during the term of the relevant notes, which, in either case, may be zero. Floating rates

will be based on one of the base rates specified herein or another base rate as specified in the applicable pricing supplement. |

| · | The notes will pay interest, if any, on the dates

stated in the applicable pricing supplement. |

| · | The notes will be held in global, book-entry form

by The Depository Trust Company, unless the pricing supplement provides otherwise. |

The pricing supplement may

also specify that the notes will have any additional terms, including whether they may be callable by us.

Investing in the

notes involves risks. See “Risk Factors” beginning on page PS–5 of this prospectus supplement as well as the applicable

pricing supplement and the documents incorporated herein by reference for a discussion of risks relating to each particular issuance of

notes.

Neither the Securities

and Exchange Commission nor any state securities commission has approved or disapproved of the notes or passed upon the accuracy or the

adequacy of this prospectus supplement, the accompanying prospectus or any related pricing supplement. Any representation to the contrary

is a criminal offense.

The notes will constitute

our unsecured and unsubordinated obligations and shall rank pari passu among themselves and pari passu with all of our other

unsecured and unsubordinated obligations, subject, however, to statutory priorities conferred upon certain unsecured and unsubordinated

obligations in the event of any Resolution Measures (as described in the accompanying prospectus) imposed on us or in the event of our

dissolution, liquidation, insolvency or composition, or if other proceedings are opened for the avoidance of the insolvency of, or against,

us; and in accordance with Section 46f(5) of the German Banking Act (Kreditwesengesetz), our obligations under the notes shall

rank in priority to our senior non-preferred obligations under any of our debt instruments (Schuldtitel) within the meaning of

Section 46f(6) sentence 1 of the German Banking Act (including the senior non-preferred obligations under any such debt instruments that

we issued before July 21, 2018 and that are subject to Section 46f(9) of the German Banking Act) or any successor provision;

this includes eligible liabilities within the meaning of Articles 72a and 72b(2) of Regulation (EU) No 575/2013 of the European Parliament

and of the Council, as amended, supplemented or replaced from time to time (the “CRR”).

The

notes are intended to qualify as eligible liabilities instruments within the meaning of Article 72b(2), with the exception of point (d),

CRR for the minimum requirement for own funds and eligible liabilities, as described and provided for in the bank regulatory capital provisions

to which we are subject, including restrictions on the aggregate amount of similar instruments that we may use for such purposes, but

do not constitute senior non-preferred debt instruments within the meaning of Section 46f(6) sentence 1 of the German Banking Act.

By acquiring the

notes, you will be bound by and will be deemed to consent to the imposition of any Resolution Measure by the competent resolution

authority, which may include the write down of all, or a portion, of any payment on the notes or the conversion of the notes into

ordinary shares or other instruments of ownership. If any Resolution Measure becomes applicable to us, you may lose some or all of

your investment in the notes. Please see the section “Risk Factors” beginning on page 20 in the

accompanying prospectus and the section “Resolution Measures” beginning on page 76 in the accompanying

prospectus for more information.

The notes are not deposits

or savings accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other U.S. or foreign governmental

agency or instrumentality.

Deutsche Bank Securities Inc.

(“DBSI”), which is our affiliate, has agreed to use reasonable efforts to solicit offers to purchase these notes as

our selling agent to the extent it is named in the applicable pricing supplement. DBSI may also act on a firm commitment basis, but only

if so specified in the applicable pricing supplement. Certain other selling agents to be named in the applicable pricing supplement may

also be used to solicit such offers on either a reasonable efforts or firm commitment basis. The agents may also purchase these notes

as principal at prices to be agreed upon at the time of sale. The agents may resell any notes they purchase as principal at prevailing

market prices, or at other prices, as the agents determine.

Because DBSI is both our affiliate

and a member of the Financial Industry Regulatory Authority, Inc. (“FINRA”), each offering of notes by DBSI must be

conducted in accordance with the applicable provisions of FINRA Rule 5121. For more information, see the “Plan of Distribution (Conflicts

of Interest)” section of this prospectus supplement.

The agents may use this prospectus

supplement and the accompanying prospectus, together with any pricing supplements, in connection with offers and sales of the notes in

market-making transactions.

The date of this prospectus

supplement is August 3, 2021.

TABLE OF CONTENTS

| |

Page

|

| Summary |

PS–3 |

| Risk Factors |

PS–5 |

| Description of Notes |

PS–9 |

| The Depositary |

PS–23 |

| Series E Notes Offered on a Global Basis |

PS–25 |

| United States Federal Income Taxation |

PS–31 |

| Taxation by Germany of Non-Resident Holders |

PS–37 |

| Benefit Plan Investor Considerations |

PS–39 |

| Plan of Distribution (Conflicts of Interest) |

PS–41 |

| Legal Matters |

PS–44 |

SUMMARY

The following summary describes

the notes we are offering under this program in general terms only. You should read the summary together with the more detailed information

contained in this prospectus supplement, in the accompanying prospectus and in the applicable pricing supplement. We refer to the notes

offered under this prospectus supplement as our “Series E notes” or “notes.” We refer

to the offering of the Series E notes as our “Series E program.”

As used in this prospectus

supplement, the “Bank,” “we,” “our,”

“us” or “Issuer” refers to Deutsche Bank AG, including,

as the context may require, acting through one of its branches.

| Issuer |

Deutsche Bank AG |

| Notes offered |

Senior Debt Funding Notes, Series E |

| Ranking |

The notes will constitute our unsecured and unsubordinated obligations and shall rank pari passu among themselves and pari passu with all of our other unsecured and unsubordinated obligations, subject, however, to statutory priorities conferred upon certain unsecured and unsubordinated obligations in the event of any Resolution Measures imposed on us or in the event of our dissolution, liquidation, insolvency or composition, or if other proceedings are opened for the avoidance of the insolvency of, or against, us; in accordance with Section 46f(5) of the German Banking Act (Kreditwesengesetz), our obligations under the notes shall rank in priority to our senior non-preferred obligations under any of our debt instruments (Schuldtitel) within the meaning of Section 46f(6) sentence 1 of the German Banking Act (including the senior non-preferred obligations under any such debt instruments that we issued before July 21, 2018 and that are subject to Section 46f(9) of the German Banking Act) or any successor provision, this includes eligible liabilities within the meaning of Articles 72a and 72b(2) CRR. |

| Resolution Measures |

By acquiring any notes, you will be bound by

and will be deemed to consent to the imposition of any Resolution Measure by the competent resolution authority, which may include

the write down of all, or a portion, of any payment on the notes or the conversion of the notes into ordinary shares or other

instruments of ownership. If any Resolution Measure becomes applicable to us, you may lose some or all of your investment in the

notes. Please see the section “Risk Factors” beginning on page 20 in the accompanying prospectus and the section

“Resolution Measures” beginning on page 76 in the accompanying prospectus for more information.

|

| Branches; Office Substitution |

We may act directly through our principal office in Frankfurt or through one of our branches, such as our London branch or New York branch, as specified in the applicable pricing supplement. If specified in the applicable pricing supplement, we may, without the consent of the holders or the trustee, designate our head office or another branch of ours (in this |

| |

paragraph, we refer to each of our head office or any of our branches as an “office”) as substitute for the office through which we have acted to issue such series with the same effect as if such substitute office had been originally named as the office through which we had acted to issue such series for all purposes under the Indenture (as defined below) and such series. |

| Interest features |

A note will pay interest, if any, on the dates specified in the applicable pricing supplement. A note may bear interest at any time at either a fixed rate or a floating rate that varies during the term of the relevant notes, which, in either case, may be zero. |

| Redemption features |

Subject to (i) receipt by the Bank of approval

of the competent authority and (ii) compliance with any other regulatory requirements. If the notes are redeemed by us without the approval

of such competent authority, then the amounts paid on the notes must be returned to us irrespective of any agreement to the contrary.

|

| Currency and denomination |

The notes will be issued in U.S. dollars in minimum denominations of $1,000 unless we specify otherwise in the applicable pricing supplement. |

| Listing |

The notes will not be listed on any securities exchange unless we specify otherwise in the applicable pricing supplement. |

| Form of notes |

The notes will be issued only in global form (i.e., in book-entry form) registered in the name of The Depository Trust Company, or its nominee, unless otherwise stated in the applicable pricing supplement. |

| Conflicts of Interest |

Because DBSI is both an affiliate of the Bank and a member of FINRA, any distribution of the notes by DBSI must be made in compliance with the applicable provisions of FINRA Rule 5121 regarding a FINRA member firm’s distribution of the securities of an affiliate and related conflicts of interest. In accordance with FINRA Rule 5121, DBSI may not make sales in offerings of the notes to any of its discretionary accounts without the prior written approval of the customer. For more information, see the “Plan of Distribution (Conflicts of Interest)” section of this prospectus supplement. |

| How to reach us |

You may contact us at Deutsche

Bank AG, Taunusanlage 12, 60325 Frankfurt am Main, Germany, Attention: Investor Relations (telephone: +49–800–910–8000, email: db.ir@db.com). |

RISK FACTORS

For a discussion of the

risk factors relating to Deutsche Bank AG and its business, see “Risk Factors” in Part I, Item 3

of our most recent annual report on Form 20-F and our other current and periodic reports filed with the Securities and Exchange

Commission that are incorporated by reference into this prospectus supplement.

In

addition, you should consider carefully the following discussion of risks, together with the section “Risk

Factors” beginning on page 20 in the accompanying prospectus and the risk information contained in the relevant

pricing supplement, before you decide that an investment in the notes is suitable for you.

Risks Relating to the Notes Generally

The notes are subject to the credit of Deutsche Bank AG.

The notes will constitute

unsecured and unsubordinated senior non-preferred obligations of Deutsche Bank AG and will not, either directly or indirectly, constitute

an obligation of any third party. Any interest payments to be made on the notes and the repayment of principal at maturity depend on the

ability of Deutsche Bank AG to satisfy its obligations as they become due. An actual or anticipated downgrade in Deutsche Bank AG’s

credit rating or increase in the credit spreads charged by the market for taking Deutsche Bank AG’s credit risk will likely have

an adverse effect on the value of the notes. As a result, the actual and perceived creditworthiness of Deutsche Bank AG will affect the

value of the notes. Any future downgrade could materially affect Deutsche Bank AG’s funding costs and cause the trading price of

the notes to decline significantly. Additionally, under many derivative contracts to which Deutsche Bank AG is a party, a downgrade could

require it to post additional collateral, lead to terminations of contracts with accompanying payment obligations or give counterparties

additional remedies. In the event Deutsche Bank AG were to default on its payment obligations or become subject to a Resolution Measure,

you might not receive interest and principal payments owed to you under the terms of the notes and you could lose your entire investment.

Senior debt funding securities,

including the notes offered herein, are intended to qualify as eligible liabilities within the meaning of Article 72(b)(2), with the exception

of point (d), CRR for the minimum requirement for own funds and eligible liabilities under the bank regulatory capital provisions applicable

to us. They are expected to constitute “senior preferred” debt securities and would, if insolvency proceedings are opened

against us or if resolution measures are imposed on us, bear losses after our “senior non-preferred” debt instruments but

before other liabilities with an even more senior rank, for example, covered deposits held by natural persons and micro, small and medium-sized

enterprises.

The notes are intended

to qualify as eligible liabilities instruments within the meaning of Article 72b(2), with the exception of point (d), CRR for the

minimum requirement for own funds and eligible liabilities of the Bank. The obligations under the notes constitute unsecured and

unsubordinated preferred obligations of the Bank ranking pari passu among themselves and with other unsecured and

unsubordinated obligations of the Bank, subject, however, to statutory priorities conferred to certain unsecured and unsubordinated

obligations in the event of resolution measures being imposed on the Bank or in the event of the dissolution, liquidation,

insolvency, composition or other proceedings for the avoidance of insolvency of, or against, the Bank. Pursuant to Section 46f(5) of

the German Banking Act (Kreditwesengesetz), the obligations under the notes rank in priority of those under our debt

instruments (Schuldtitel) within the meaning of Section 46f(6) sentence 1 of the German Banking Act (also in conjunction with

Section 46f(9) of the German Banking Act) or any successor provision.

You as holder of notes may

not set off or net your claims arising under the notes against any of our claims. No collateral or guarantee shall be provided at any

time to secure claims of a holder of notes under the notes; any collateral or guarantee already provided or granted in the future in connection

with our other liabilities may not be used for claims under the notes.

No subsequent agreement

may enhance the seniority of the obligations as described above or shorten the term of the notes or any applicable notice period.

Any redemption, repurchase or termination of the notes prior to their scheduled maturity is subject to the prior approval of the

competent resolution authority.

If insolvency proceedings

are opened against us or if Resolution Measures are imposed on us, our “senior preferred” debt securities (including the notes

offered herein) are expected to be among the unsecured

unsubordinated obligations that

would bear losses after our “senior non-preferred” debt instruments, including our non-structured senior debt securities issued

before July 21, 2018.

On the other hand, there are

liabilities with an even more senior rank, for example, covered deposits held by natural persons and micro, small and medium-sized enterprises.

Therefore, you may lose some or all of your investment in the notes offered herein if insolvency proceedings are opened against us or

a Resolution Measure becomes applicable to us.

The notes contain limited events of default,

and the remedies available thereunder are limited.

As described in “Description

of Debt Securities — Senior Debt Funding Securities — Events of Default” in the accompanying prospectus, the notes provide

for no event of default other than the opening of insolvency proceedings against us by a German court having jurisdiction over us. In

particular, the imposition of a Resolution Measure will not constitute an event of default with respect to the Indenture or the notes.

If an event of default occurs,

holders of the notes have only limited enforcement remedies. If an event of default with respect to the notes occurs or is continuing,

either the trustee or the holders of not less than 33⅓% in aggregate principal amount of all outstanding debt securities issued

under the Indenture, including the notes, voting as one class, may declare the principal amount of the notes and interest accrued thereon

to be due and payable immediately. We may issue further series of debt securities under the Indenture and these would be included in that

class of outstanding debt securities.

In particular, holders of

the notes will have no right of acceleration in the case of a default in the payment of principal of, interest on, or other amounts owing

under, the notes. If such a default occurs and is continuing with respect to the notes, the trustee and the holders of the notes could

take legal action against us, but they may not accelerate the maturity of the notes. Moreover, if we fail to make any payment because

of the imposition of a Resolution Measure, the trustee and the holders of the notes would not be permitted to take such action, and in

such a case you may permanently lose the right to the affected amounts.

Holders will also have no

rights of acceleration due to a default in the performance of any of our other covenants under the notes.

We may, without consent of the holders or the trustee, designate

another office of ours as the issuing office.

If specified in the applicable

pricing supplement, we may, without consent of the holders or the trustee, designate our head office or another branch of ours (in this

paragraph, we refer to each of our head office or any of our branches as “office”) as substitute for the office through

which we have acted to issue such series with the same effect as if such substitute office had been originally named as the office through

which we had acted to issue such series for all purposes under the Indenture and such series. This means that, with effect from the substitution

date, such substitute office will assume all of the obligations of the originally-named office as principal obligor under such series

of notes. If such series includes an “Office Substitution” right, as described above and in the Indenture, the applicable

pricing supplement may include disclosure about the possible tax consequences of such substitution. If applicable, you should review

such disclosure carefully and consult your tax adviser regarding the U.S. federal tax consequences of such substitution, as well as tax

consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

Risks Relating to Floating Rate Notes

Regulation, reform and the actual or potential

discontinuation of certain “benchmark” rates, including any base rate to which your notes may reference, may adversely affect

the value of, return on and trading market for floating rate notes that are based on these benchmarks.

Previously certain interest

rates which are deemed to be “benchmark” rates have been the subject of national, international and other regulatory guidance,

reform and other actions. This has resulted in regulatory reform and changes to existing benchmarks. Such reform of benchmarks includes

the Regulation (EU) 2016/1011 (as amended, the “EU Benchmarks Regulation”) of the European Parliament and of the Council

of 8 June 2016 on indices used as benchmarks in financial instruments and financial contracts or to measure the performance of investment

funds and amending Directives 2008/48/EC and 2014/17/EU and Regulation (EU) No 596/2014, and the EU Benchmarks Regulation as it forms

part of UK domestic law by virtue of the UK European Union

(Withdrawal) Act 2018 (the “UK

Benchmarks Regulation” and, together with the EU Benchmarks Regulation, the “Benchmarks Regulations”), which

apply to the provision of benchmarks, the contribution of input data to a benchmark and the use of a benchmark within the European Union

(the “EU”) and the United Kingdom (the “UK”), respectively.

Among other things, the Benchmarks

Regulations (i) require benchmark administrators to be authorized or registered (or, if non-EU-based or non-UK based, to be subject to

an equivalent regime or otherwise recognized or endorsed) and (ii) prevent certain uses by EU and UK supervised entities, as applicable,

of benchmarks of administrators that are not authorized or registered (or if non EU-based or UK-based, as applicable, not deemed equivalent

or recognized or endorsed).

The Benchmarks Regulations

could have a material impact on any floating rate notes, in particular, if the methodology or other terms of the relevant benchmark are

changed in order to comply with the requirements of the Benchmarks Regulations. Such changes could, amongst other things, have the effect

of reducing, increasing or otherwise affecting the volatility of the published rate or level of the relevant benchmark.

The Financial Conduct Authority

of the United Kingdom (the “FCA”) has indicated through a series of announcements that the continuation of the London

Interbank Offered Rate (“LIBOR”) cannot and will not be guaranteed after 2021. On March 5, 2021, the FCA and ICE Benchmark

Administration announced that all LIBOR setting either will cease to be provided by any administrator or will no longer be representative

(i) immediately after December 31, 2021 (for all sterling, euro, Swiss franc and Japanese yen settings, and the 1-week and 2-month U.S.

dollar settings) and (ii) immediately after June 30, 2023 (for the remaining U.S. dollar settings).

In June 2017, the New York

Federal Reserve’s Alternative Reference Rates Committee announced the Secured Overnight Financing Rate (“SOFR”)

as its recommended alternative to U.S. dollar LIBOR. However, the composition and characteristics of SOFR are not the same as those of

U.S. dollar LIBOR, SOFR is not be the economic equivalent of U.S. dollar LIBOR, there can be no assurance that SOFR will perform in the

same way as U.S. dollar LIBOR would have at any time and there is no guarantee that SOFR will be a comparable substitute for U.S. dollar

LIBOR. Any failure of SOFR to gain market acceptance could adversely affect the value of the notes linked to SOFR. The administrator of

SOFR may make changes that could change the value of SOFR or discontinue SOFR and has no obligation to consider your interests in doing

so.

In the future, “benchmark”

rates, including any base rate to which the notes may reference could be subject to further regulatory scrutiny, reform efforts and/or

other actions. Any such regulatory scrutiny, reform efforts and/or other actions could increase the costs and risks of administering or

otherwise participating in the setting of a “benchmark” and complying with applicable regulations or requirements. Such factors

may have the effect of discouraging market participants from continuing to administer or contribute to certain “benchmarks”,

trigger changes in the rules or methodologies used in certain “benchmarks” or lead to the elimination, discontinuance or obsolescence

of certain “benchmarks”. Following the implementation of reforms, the manner of administration of benchmarks may change, with

the result that they may perform differently than in the past, or the benchmark could be eliminated or discontinued entirely, or there

could be other consequences that cannot be predicted. Even prior to the implementation of any changes, uncertainty as to the nature of

potential alternative reference rates and as to the nature and effect of potential changes to such benchmark may adversely affect such

benchmark during the term of the relevant notes, as well as the value of, the return on and/or trading market for notes linked to such

benchmark. Any of the foregoing consequences could have a material adverse effect on the interest rate on, value of, return on and trading

market for any notes linked to such a “benchmark” rate.

Furthermore, if any base rate

is discontinued or ceases to be published, there can be no assurances that the Bank and other market participants will be adequately prepared

for such discontinuance or cessation, which may have an unpredictable impact on contractual mechanics (including, but not limited to,

the interest rate to be paid by the Bank with respect to specific notes), among other adverse consequences with respect to an applicable

series of notes.

The applicable base

rate may be modified or discontinued and a series of notes may bear interest by reference to a rate other than the original base rate,

which could adversely affect the value of such notes.

The base rates are published

by third-party administrators based on data received by such administrators from sources other than us, and we have no control over the

methods of calculation, publication schedule, rate revision practices or availability of such rates at any time. There can be no guarantee

that the applicable base rate will not be discontinued or fundamentally altered in a manner that is materially adverse to the interests

of

investors in the notes. If the

manner in which the applicable base rate is calculated is changed, that change may result in a reduction in the amount of interest payable

on a series of notes, and the trading prices of such series of notes. In addition, the administrator of the applicable base rate may withdraw,

modify or amend the published data with respect to the applicable base rate in the sole discretion of such administrator and without notice,

in which case the interest rate on such affected notes will not be adjusted for any modifications or amendments to such applicable base

rate data that the applicable administrator may publish after the interest rate for an applicable interest period has been determined.

If the applicable base rate

is eliminated or discontinued, or if certain other events occur with respect to such base rate, then the interest rate on a series of

notes will be calculated using an alternative base rate, which could require or result in adjustments to the interest determination and

other provisions of the notes, and, with respect to certain such rates, decisions or elections with respect to new interest determination

conventions and other provisions. Any such use, adjustment, decision or election may result in adverse consequences to holders of any

such series of notes.

Potential

conflicts of interest may arise if the relevant base rate for floating rate notes has been discontinued or is unavailable.

If the relevant base rate

for floating rate notes has been eliminated or discontinued, the terms of the notes provide for certain “fallback” arrangements

that the calculation agent will use to determine the applicable base rate, which may include the selection of an alternative reference

rate as well as certain adjustments to the terms of the notes. The terms that the calculation agent may adjust include, but are not limited

to, the base rate, the applicable currency and/or index maturity for such alternative reference rate, the spread or spread multiplier,

as well as the business day convention, the definition of business day, interest determination dates and related provisions and definitions.

This may require the exercise of discretion and the making of subjective judgments. In making these discretionary judgments, the fact

that we are acting as calculation agent for the notes may cause us to have economic interests that are adverse to your interests as an

investor in the notes. Any selection, adjustments or determinations by the calculation agent could adversely affect the interest rate

and the return on the notes. If a Benchmark Transition Event occurs, a U.S. Holder holding floating rate notes may be deemed to exchange

such Floating Rate Notes for new notes for U.S federal income tax purposes, which may be taxable to such U.S. Holder. Proposed U.S. Treasury

Regulations, which are not yet in effect but upon which taxpayers may rely, provide that in certain circumstances, the replacement of

the Benchmark with a qualifying reference rate would not result in a deemed exchange under the Code. U.S. Holders should consult with

their own tax advisers regarding the potential consequences of a Benchmark Transition Event.

DESCRIPTION OF NOTES

References in this prospectus

supplement to the “Bank,” “we,” “our” or “us”

refer to Deutsche Bank AG, including, as the context may require, acting through one of its branches. As

context may require, references to “you” or “ holders” mean either (a) those

who invest in the notes being offered, whether they are the direct holders or owners of beneficial interests in those notes or (b) those

who own notes registered in their own names, on the books that we or the registrar maintain for this purpose, and not those

who own beneficial interests in notes issued in book-entry form through The Depository Trust Company or another depositary or in

notes registered in street name. Owners of beneficial interests in the notes should read the section entitled “Description

of Notes — Form, Legal Ownership and Denomination of Notes.”

General Information Regarding Senior Debt Funding

Notes, Series E

We refer to the Senior Debt

Funding Notes, Series E offered under this prospectus supplement as our “Series E notes” or the “notes,”

which are a separate series of our debt securities. We refer to the offering of the Series E notes as our “Series E program.”

Investors should carefully read the general terms and provisions of our debt securities in “Description of Debt Securities —

Senior Debt Funding Securities” in the accompanying prospectus. This section supplements that description.

A pricing supplement to

this prospectus supplement will add specific terms for each issuance of notes and may modify or replace any of the information in this

section and in “Description of Debt Securities — Senior Debt Funding Securities” in the accompanying prospectus.

If the pricing supplement is inconsistent with this prospectus supplement or the accompanying prospectus, the terms in the pricing

supplement will control with regard to the note you purchase. Therefore, the statements made in this prospectus supplement

may not be the terms that apply to the note you purchase.

We Will Issue Notes

Under the Senior Debt Funding Indenture. The Series E notes issued under our Series E program will be governed by the amended

and restated senior debt funding indenture, dated as of August 3, 2021, among us, Delaware Trust Company, as trustee, and Deutsche Bank

Trust Company Americas, as paying agent, authenticating agent, issuing agent and registrar, as may be amended and supplemented from time

to time (the “Indenture”) (see “Description of Debt Securities — Senior Debt Funding Securities —

The Senior Debt Funding Indenture” in the accompanying prospectus). The notes issued under the Indenture will constitute a single

series under that Indenture, together with any notes we have issued in the past or that we issue in the future under that Indenture that

we designate as being part of that series. From time to time, we may create and issue additional notes with the same terms as previous

Series E notes, so that the additional notes will be considered as part of the same issuance as the earlier notes; provided that,

if any such additional notes are not fungible with the earlier notes for U.S. federal income tax purposes, they will be issued under a

separate CUSIP or other identifying number.

By acquiring any

notes, you will be bound by and will be deemed to consent to the imposition of any Resolution Measure by the competent

resolution authority, which may include the write down of all, or a portion, of any payment on the notes or the conversion of

the notes into ordinary shares or other instruments of ownership. If any Resolution Measure becomes applicable to us, you may

lose some or all of your investment in the notes. Please see the section “Risk Factors” beginning on page

20 in the accompanying prospectus and the section “Resolution Measures” beginning on page 76 in the

accompanying prospectus for more information.

Outstanding Indebtedness

of the Bank. The Indenture does not limit the amount of additional indebtedness that we may incur.

How the Notes Rank

Against Other Debt. The notes will constitute our unsecured and unsubordinated obligations and shall rank pari passu among

themselves and pari passu with all of our other unsecured and unsubordinated obligations, subject, however, to statutory priorities

conferred upon certain unsecured and unsubordinated obligations in the event of any Resolution Measures imposed on us or in the event

of our dissolution, liquidation, insolvency or composition, or if other proceedings are opened for the avoidance of the insolvency of,

or against, us; and in accordance with Section 46f(5) of the German Banking Act (Kreditwesengesetz), our obligations under the

notes shall rank in priority to our senior non-preferred obligations under any of our debt instruments (Schuldtitel) within the

meaning of Section 46f(6) sentence 1 of the German Banking Act (including the senior non-preferred obligations under any such debt instruments

that we issued

before July 21, 2018 and that are subject to Section

46f(9) of the German Banking Act) or any successor provision; this includes eligible liabilities

within the meaning of Articles 72a and 72b(2) CRR.

Qualification as

“Eligible Liabilities”. The notes are intended to qualify as eligible

liabilities instruments within the meaning of Article 72b(2), with the exception of point (d), CRR for the minimum requirement for

own funds and eligible liabilities, as described and provided for in the bank regulatory capital provisions to which we are subject,

including restrictions on the aggregate amount of similar instruments that we may use for such purposes, but do not constitute

senior non-preferred debt instruments within the meaning of Section 46f(6) sentence 1 of the German Banking Act.

Office Substitution.

If specified in the applicable pricing supplement, we may, without the consent of the holders or the trustee, designate our head office

or another branch of ours (in this paragraph, we refer to each of our head office or any of our branches as an “office”)

as substitute for the office through which we have acted to issue such series with the same effect as if such substitute office had been

originally named as the office through which we had acted to issue such series for all purposes under the Indenture and such series. In

order to give effect to such a substitution, we will give notice of the substitution to the trustee and the holders of such series of

notes. With effect from the substitution date, such substitute office will, without any amendment of such series of notes or entry into

any supplemental indenture, assume all of the obligations of the originally-named office as principal obligor under such series of notes.

The applicable pricing supplement will include a reference to office substitution if included as a term of a series of notes.

This Section Is Only

a Summary. The accompanying prospectus and this prospectus supplement provide only summaries of the Indenture’s material

terms. They do not, however, describe every aspect of the Indenture and the notes. The Indenture and its associated documents, including

the applicable note, contain the full legal text of the matters described in this section and in the accompanying prospectus. A copy of

the Indenture has been filed with the Securities and Exchange Commission (the “SEC”) as part of the registration statement

for the notes.

Some Frequently Used

Definitions. We have defined some of the terms that we use frequently in this prospectus supplement below:

A “business day”

means, unless otherwise stated in the applicable pricing supplement, for any note, any day other than a day that is (i) a Saturday or

Sunday, (ii) a day on which banking institutions generally in the City of New York are authorized or obligated by law, regulation or executive

order to close, (iii) a day on which transactions in U.S. dollars are not conducted in the City of New York or (iv) a day on which TARGET2

is not operating.

“Clearstream, Luxembourg”

means Clearstream Banking, société anonyme, Luxembourg.

“Depositary” means

The Depository Trust Company, New York, New York.

“Euroclear operator”

means Euroclear Bank SA/NV, as operator of the Euroclear System.

“Euro-zone” means the region comprising

member states of the European Union that have adopted a single currency in accordance with the relevant treaty of the European Union,

as amended.

An “interest payment date”

for any note means a date on which, under the terms of that note, regularly scheduled interest is payable.

A “New York Banking Day”

means, unless otherwise stated in the applicable pricing supplement, for any note, any day except a Saturday, Sunday or a legal holiday

in The City of New York or a day on which banking institutions in The City of New York are authorized or required by law or executive

order to close.

The “record date”

for any interest payment date is, (a) in the case of global notes, the date that is one New York Banking Day immediately preceding

the relevant date of payment with respect to such interest payment date and, (b) in the case of certificated notes, the date that

is 15 calendar days prior to that interest payment date, whether or not that day is a business day, unless otherwise specified in the

applicable pricing supplement. However, upon maturity or redemption, the paying agent will pay any interest due to the holder to whom

it pays the principal of the note.

The term “Reuters page”

means the display on Reuters 3000 Xtra, or any successor service, on the page or pages specified in this prospectus supplement or the

relevant pricing supplement, or any replacement page or pages on that service.

“TARGET2” means the

Trans-European Automated Real-time Gross Settlement Express Transfer System.

“TARGET Settlement Day”

means any day on which TARGET2 is operating.

References in this prospectus

supplement to “U.S. dollar,” “U.S.$” or “$” are to

the currency of the United States of America. References in this prospectus supplement to “euro” or “€”

are to the single currency introduced at the commencement of the third stage of the European Economic and Monetary Union pursuant to the

treaty establishing the European Community, as amended.

Types of Notes

We may issue the following

types of notes:

Fixed Rate Notes

A note of this type will bear

interest at a fixed rate described in the applicable pricing supplement. This type includes zero coupon notes, which bear no interest.

Floating Rate Notes

A note of this type will bear

interest at rates that are determined by reference to an interest rate or interest rate formula. In some cases, the rates may also be

adjusted by adding or subtracting a spread or multiplying by a spread multiplier. The various interest rate formulas and these other features

are described below under “— Interest Rates — Floating Rate Notes.” If the note you purchase is a floating rate

note, the formula and any adjustments that apply to the interest rate will be specified in the pricing supplement.

Terms Specified in Pricing Supplements

A pricing supplement generally

will specify the following terms of any issuance of our Series E notes to the extent applicable:

| · | the specific designation of the notes; |

| · | the issue price (price to public); |

| · | the aggregate principal amount, purchase price

and denomination; |

| · | the original issue date; |

| · | the stated maturity date and any terms related

to any postponing or shortening of the maturity date to account for days that are not business days; |

| · | whether the notes are fixed rate notes or floating

rate notes; |

| · | for fixed rate notes, the rate per year at which

the notes will bear interest, if any, or the method of calculating that rate and the dates on which interest will be payable; |

| · | for floating rate notes, the base rate, the index

maturity (if any), the spread, the spread multiplier, the initial interest rate, the interest reset periods, the interest payment dates

and any other terms relating to the particular method of calculating the interest rate for the note; |

| · | whether the notes may be redeemed, in whole or

in part, at our option prior to the stated maturity date, and the terms of any redemption; |

| · | the circumstances, if any, under which we will

pay additional amounts on the notes for any tax, assessment or governmental charge withheld or deducted and, if so, whether we will have

the option to redeem those notes rather than pay the additional amounts; and |

| · | any other terms on which we will issue the notes. |

Form, Legal Ownership and Denomination

of Notes

Form. We will

issue notes in fully registered, global (i.e., book-entry) form only, unless we specify otherwise in the applicable pricing

supplement. Notes in book-entry form will be represented by a global note registered in the name of the Depositary or its nominee, which

will be the sole registered owner and the holder of all the notes represented by the global note. An investor therefore will not be a

holder of the note, but will own only beneficial interests in a global note, which are held by means of an account with a broker, bank

or other financial institution that in turn has an account as a “participant” in the Depositary or with another institution

that does. The Depositary maintains a computerized, book-entry system that will reflect the interests in the global notes held by participants

in its book-entry system. An investor’s beneficial interest in the global notes will, in turn, be reflected only in the records

of the Depositary’s direct or indirect participants though an account maintained by the investor with such participant.

Except as set forth in the

accompanying prospectus under “Forms of Securities — Global Securities,” you may not exchange registered global notes

or interests in registered global notes for a certificate issued to you in definitive form (a “certificated note”).

A further description of the Depositary’s procedures for global notes representing book-entry notes is set forth below under “The

Depositary” and in the accompanying prospectus under “Forms of Securities — Global Securities.”

Legal Ownership.

The person or entity in whose name the notes are registered will be considered the holder and legal owner of the notes. Our obligations

under the Indenture, as well as the obligations of the trustee and those of any third parties employed by us or the trustee, run only

to the registered holders of the notes. We do not have obligations to investors who own beneficial interests in global notes, in street

name or by any other indirect means. For example, once we make a payment or give a notice to the registered holder, we have no further

responsibility for that payment or notice even if that holder is required, under agreements with depositary participants or customers

or by law, to pass it along to the indirect holders (e.g., owners of beneficial interests), but does not do so. Similarly,

if we need to ask the holders of the notes to vote on a proposed amendment to the notes, we would seek approval only from the registered

holders, and not the indirect holders, of the notes.

Special Considerations

for Indirect Holders. If you hold notes through a bank, broker or other financial institution, either in book-entry form or in

street name, you should check with your own institution to find out:

| · | how it handles securities payments and notices; |

| · | whether it imposes fees or charges; |

| · | how it would handle voting if it were ever required; |

| · | whether and how you can instruct it to send you

notes registered in your own name so you can be a direct holder, if that is permitted; and |

| · | how it would pursue rights under the notes if

there were a default or other event triggering the need for holders to act to protect their interests. |

Denominations.

Unless we provide otherwise in the applicable pricing supplement, we will issue the notes in denominations of $1,000 or any amount greater

than $1,000 that is an integral multiple of $1,000.

Governing Law.

The Indenture is, and the notes will be, governed by and construed in accordance with the laws of the State of New York, except as may

be otherwise required by mandatory provisions of law.

Interest Rates

Fixed Rate Notes

Each fixed rate note will

bear interest from the date of issuance at the annual rate specified in the applicable pricing supplement until the principal is paid

or made available for payment. Unless otherwise specified in the applicable pricing supplement, the following provisions will apply to

fixed rate notes offered pursuant to this prospectus supplement.

How Interest Is Calculated.

Interest on fixed rate notes will be computed on the basis of a 360-day year of twelve 30-day months.

How Interest Accrues.

Interest on fixed rate notes will accrue from, and including, the most recent interest payment date to which interest has been paid or

duly provided for, or, if no interest has been paid or duly provided for, from, and including, the issue date or any other date specified

in the applicable pricing supplement on which interest begins to accrue, to, but excluding, the next interest payment date, or, if earlier,

the date on which the principal has been paid or duly made available for payment, except as described below under “— If a

Payment Date is Not a Business Day” (each such period, an “interest period”).

When Interest Is Paid.

Payments of interest on fixed rate notes will be made on the interest payment dates specified in the applicable pricing supplement. However,

if the period of time between the issue date and the first interest payment date thereafter is less than the period of time between a

record date and an interest payment date, interest will not be paid on the first interest payment date, but will be paid on the second

interest payment date.

Amount of Interest Payable.

Interest payments for fixed rate notes will include accrued interest from, and including, the date of issue or from, and including, the

last interest payment date in respect of which interest has been paid, as the case may be, to, but excluding, the relevant interest payment

date or date of maturity or earlier redemption, as the case may be.

If a Payment Date is

Not a Business Day. If any scheduled interest payment date is not a business day, we will pay interest on the next business day,

but interest on that payment will not accrue during the period from and after the scheduled interest payment date. If the scheduled maturity

date or date of redemption is not a business day, we may pay interest, if any, and principal and premium, if any, on the next succeeding

business day, but interest on that payment will not accrue during the period from and after such scheduled maturity date or date of redemption.

Floating Rate Notes

Each floating rate note will

mature on the date specified in the applicable pricing supplement.

Each floating rate note will

bear interest at a floating rate determined by reference to an interest rate or interest rate formula, which we refer to as the “base

rate.” The base rate may be one or more of the following:

| · | any other reference interest rate specified in

the applicable pricing supplement. |

Formula for Interest

Rates. The interest rate on each floating rate note will be calculated by reference to:

| · | the specified base rate based on the index maturity,

if any, |

| · | plus or minus the spread, if any, and/or |

| · | multiplied by the spread multiplier, if any. |

For any floating rate note,

if applicable, “index maturity” means the period of maturity of the instrument or obligation from which the base rate

is calculated and will be specified in the applicable pricing supplement. The “spread” is the number of basis points

(one one-hundredth of a percentage point) specified in the applicable

pricing supplement to be added to, or subtracted

from, the base rate for a floating rate note. The “spread multiplier” is the percentage specified, if any, in the applicable

pricing supplement by which the base rate will be multiplied to determine the applicable interest rate for such floating rate note.

In addition, the interest

rate on a floating rate note may not be less than 0% per annum or higher than the maximum rate permitted by applicable New York law, as

that maximum rate may be modified by United States law of general application.

How Certain Floating

Interest Rates Are Reset.

The terms and provisions set

forth in this section will apply to any series of notes for which the specified base rate is EURIBOR or any other base rate that the applicable

pricing supplement specifies this section applies to, but will not apply to series of notes for which the specified base rate specified

is Compounded SOFR.

The interest rate in effect

from the date of issue to the first interest reset date for a floating rate note will be the initial interest rate specified in the applicable

pricing supplement. We refer to this rate as the “initial interest rate.” The interest rate on each floating rate note

may be reset daily, weekly, monthly, quarterly, semiannually or annually or on any other periodic basis described in the applicable pricing

supplement. We refer to this period as the “interest reset period.” The “interest reset date” in

respect of each interest reset period will be the first day of each interest reset period, unless otherwise specified in the applicable

pricing supplement.

If any interest reset date

for any floating rate note would otherwise be a day that is not a business day, such interest reset date, unless otherwise specified in

the applicable pricing supplement, will be postponed to the next succeeding day that is a business day; except that, in the case of a

EURIBOR note, if such business day is in the next succeeding calendar month, such interest reset date, unless otherwise specified in the

applicable pricing supplement, will be the immediately preceding business day.

The interest rate applicable

to each interest reset period commencing on an interest reset date will be the rate per annum determined by the calculation agent on the

interest determination date. The “interest determination date” with respect to EURIBOR will be the second TARGET Settlement

Day preceding the applicable interest reset date.

If the interest rate for a

floating rate note is determined by reference to two or more base rates, the interest determination date pertaining to such note will

be the most recent business day that is at least two business days prior to the applicable interest reset date for such floating rate

note on which each base rate is determinable. Each base rate will be determined as of such date, and the applicable interest rate will

take effect on the applicable interest reset date.

The interest rate in effect

for the ten calendar days immediately prior to maturity or redemption will be the one in effect on the tenth calendar day preceding the

maturity or redemption date.

In the detailed descriptions

of the various base rates which follow, the “calculation date” pertaining to an interest determination date means the

earlier of (1) the tenth calendar day after that interest determination date, or, if that day is not a business day, the next succeeding

business day, and (2) the business day immediately preceding the applicable interest payment date or maturity date or, for any principal

amount to be redeemed, any redemption date.

How Interest Is Calculated.

Interest on floating rate notes will accrue from, and including, the most recent interest payment date to which interest has been paid

or duly provided for, or, if no interest has been paid or duly provided for, from, and including, the issue date or any other date specified

in a pricing supplement on which interest begins to accrue. Interest will accrue to, but excluding, the next interest payment date or,

if earlier, the date on which the principal has been paid or duly made available for payment, except as described below under “—

If a Payment Date is Not a Business Day.”

Floating rate notes will have

a calculation agent, which will be Deutsche Bank AG, London Branch, unless otherwise specified in the applicable pricing supplement.

Upon the request of the holder

of any EURIBOR note, the calculation agent will provide the interest rate then in effect and, if determined, the interest rate that will

become effective on the next interest reset date for that floating rate note. Upon the request of the holder of any Compounded SOFR note,

the calculation agent will provide Compounded SOFR, the interest rate and the amount of interest accrued with respect to any interest

period for such note, after Compounded SOFR and

such interest rate and accrued interest have been determined.

The amount of accrued interest

on a floating-rate note for an interest period is calculated by multiplying the principal amount of such note by an accrued interest factor.

This accrued interest factor will be determined by multiplying the per annum floating interest rate determined by reference to the applicable

base rate, as determined for the applicable interest period, by a factor resulting from the day count convention that applies with respect

to such determination. The factor resulting from the day count convention will be, if so specified in the applicable pricing supplement,

one of the following, or may be any other convention set forth in the applicable pricing supplement:

| · | a factor based on a 360-day year of twelve 30-day

months if the day count convention specified in the applicable pricing supplement is “30/360”; |

| · | a factor equal to the actual number of days in

the relevant period divided by 360 if the day count convention specified in the applicable pricing supplement is “Actual/360”; |

| · | a factor equal to the actual number of days in

the relevant period divided by 365, or if any portion of that relevant period falls in a leap year, the sum of (A) the actual number of

days in that portion of the relevant period falling in a leap year divided by 366 and (B) the actual number of days in that portion of

the relevant period falling in a non-leap year divided by 365, if the day count convention specified in the applicable pricing supplement

is “Actual/Actual”; or |

| · | a factor equal to the actual number of days in

the relevant period divided by 365, if the day count convention specified in the applicable pricing supplement is “Actual/365 (Fixed).” |

If no day count convention

is specified in the applicable pricing supplement, the factor for EURIBOR notes and Compounded SOFR notes will be equal to the actual

number of days in the relevant period divided by 360.

All calculations with respect

to the amount of interest payable on the notes will be rounded to the nearest one hundred-thousandth, with five one-millionths rounded

upward (e.g., 0.876545 would be rounded to 0.87655); all U.S. dollar amounts related to determination of the payment per principal amount

of notes at maturity will be rounded to the nearest ten-thousandth, with five one hundred-thousandths rounded upward (e.g., 0.76545 would

be rounded up to 0.7655); and all U.S. dollar amounts paid on the aggregate principal amount of notes per holder will be rounded to the

nearest cent, with one-half cent rounded upward.

When Interest Is Paid.

We will pay interest on floating rate notes on the interest payment dates specified in the applicable pricing supplement. However, if

the period of time between the issue date and the first interest payment date thereafter is less than the period of time between a record

date and an interest payment date, interest will not be paid on the first interest payment date, but will be paid on the second interest

payment date.

If a Payment Date Is

Not a Business Day. If any scheduled interest payment date, other than the maturity date or any earlier redemption date, for any

floating rate note falls on a day that is not a business day, it will be postponed to the following business day; except that, in the

case of a EURIBOR note or a Compounded SOFR note, if that business day would fall in the next calendar month, the interest payment date

will be the immediately preceding business day. If the scheduled maturity date or any earlier redemption date of a floating rate note

falls on a day that is not a business day, the payment of principal, premium, if any, and interest, if any, will be made on the next succeeding

business day, but interest on that payment will not accrue during the period from and after such maturity or redemption date.

EURIBOR Notes

EURIBOR notes will bear interest

at an interest rate based on the Euro Interbank Offered Rate, which is commonly referred to as “EURIBOR,” and any spread and/or

spread multiplier and will be subject to the minimum interest rate and the maximum interest rate, if any.

EURIBOR, for any interest

determination date, will be the rate for interbank term deposits in euro, as sponsored, calculated and published jointly by the European

Money Markets Institute, having the index maturity

specified in the applicable pricing supplement,

as such rate appears on Reuters page EURIBOR01 (or any other page as may replace Reuters page EURIBOR01) as of 11:00 A.M., Brussels

time on such interest determination date.

The following procedures will

be followed if the rate cannot be determined as described above:

| · | If the calculation

agent determines that EURIBOR with the index maturity specified in the relevant pricing supplement has been discontinued or ceases to

be calculated or published, the calculation agent will, in its sole discretion, select an alternative reference rate as a substitute interest

rate for such EURIBOR notes; provided that if the calculation agent determines that there is an industry accepted successor interest

rate for the discontinued EURIBOR, the calculation agent shall use such successor interest rate as the substitute interest rate for such

EURIBOR notes. As part of any such substitution, the calculation agent may make adjustments to the terms of such EURIBOR notes, including,

but not limited to, the definition of the base rate (including the related fallback mechanism), the applicable currency and/or index maturity

for such alternative reference rate, the spread or spread multiplier, as well as the business day convention, the definition of

business day, interest determination dates and related provisions and definitions, in each case

consistent with accepted market practice for the use of such alternative reference rate for debt obligations such as the notes. |

| · | If the calculation

agent has not selected an alternative reference rate as a substitute interest rate for EURIBOR notes as provided above, the following

will apply: |

| o | If the rate described in the second paragraph of this subsection does not

appear on Reuters page EURIBOR01 (or any other page as may replace Reuters page EURIBOR01), or is not so published by 11:00 A.M., Brussels

Time, on the applicable interest determination date, EURIBOR for such interest determination date will be the rate calculated by the calculation

agent as the arithmetic mean of at least two quotations obtained by the calculation agent after requesting the principal Euro-zone offices

of four major banks in the Euro-zone interbank market, which may include us, as selected by the calculation agent, to provide the calculation

agent with its offered quotation for interbank term deposits in euro for the period of the index maturity designated in the applicable

pricing supplement, commencing on the applicable interest reset date, to prime banks in the Euro-zone interbank market at approximately

11:00 A.M., Brussels Time, on the applicable interest determination date and in a principal amount not less than the equivalent of U.S.$1,000,000

in euro that is representative for a single transaction in euro in such market at such time. |

| o | If fewer than two quotations are so provided, the rate on the applicable

interest determination date will be calculated by the calculation agent and will be the arithmetic mean of the rates quoted at approximately

11:00 A.M., Brussels Time, on such interest determination date by four major banks in the Euro-zone interbank market, as selected by the

calculation agent, for loans in euro to leading European banks, having the index maturity designated in the applicable pricing supplement,

commencing on the applicable interest reset date and in principal amount not less than the equivalent of U.S. $1,000,000 in euro that

is representative for a single transaction in euro in such market at such time. |

| o | If the banks so selected by the calculation agent are not providing quotations

as set forth above, then the calculation agent, after consulting such sources as it deems comparable to any of the foregoing quotations

or display page, or any such source as it deems reasonable from which to estimate EURIBOR with the relevant index maturity, will determine

EURIBOR for that interest determination date in its sole discretion. |

Secured Overnight Financing Rate (SOFR)

SOFR is published by the Federal

Reserve Bank of New York (the “New York Federal Reserve”) and is intended to be a broad measure of the cost of borrowing

cash overnight collateralized by U.S. Treasury securities. The New York Federal Reserve reports that SOFR includes all trades in the Broad

General Collateral Rate and bilateral Treasury repurchase agreement (repo) transactions cleared through the delivery-versus-payment service

offered by the Fixed Income Clearing Corporation (the “FICC”), a subsidiary of The Depository Trust & Clearing

Corporation (“DTCC”), and SOFR

is filtered by the New York Federal Reserve to remove some (but not all) of the foregoing transactions considered to be “specials.”

According to the New York Federal Reserve, “specials” are repos for specific-issue collateral, which take place at cash-lending

rates below those for general collateral repos because cash providers are willing to accept a lesser return on their cash in order to

obtain a particular security.

The New York Federal Reserve

reports that SOFR is calculated as a volume-weighted median of transaction-level tri-party repo data collected from The Bank of New York

Mellon as well as General Collateral Finance Repo transaction data and data on bilateral Treasury repo transactions cleared through the

FICC’s delivery-versus-payment service. The New York Federal Reserve also notes that it obtains information from DTCC Solutions

LLC, an affiliate of DTCC.

If data for a given market

segment were unavailable for any day, then the most recently available data for that segment would be utilized, with the rates on each

transaction from that day adjusted to account for any change in the level of market rates in that segment over the intervening period.

SOFR would be calculated from this adjusted prior day’s data for segments where current data were unavailable, and unadjusted data

for any segments where data were available. To determine the change in the level of market rates over the intervening period for the missing

market segment, the New York Federal Reserve would use information collected through a daily survey conducted by its Trading Desk of primary

dealers’ repo borrowing activity. Such daily survey would include information reported by Deutsche Bank AG, as a primary dealer,

or its affiliates.

The New York Federal Reserve

notes on its publication page for SOFR that use of SOFR is subject to important limitations, indemnification obligations and disclaimers,

including that the New York Federal Reserve may alter the methods of calculation, publication schedule, rate revision practices or availability

of SOFR at any time without notice.

Each U.S. Government Securities

Business Day, the New York Federal Reserve publishes SOFR on its website at approximately 8:00 a.m., New York City time. If errors are

discovered in the transaction data provided by The Bank of New York Mellon or DTCC Solutions LLC, or in the calculation process, subsequent

to the initial publication of SOFR but on that same day, SOFR and the accompanying summary statistics may be republished at approximately

2:30 p.m., New York City time. Additionally, if transaction data from The Bank of New York Mellon or DTCC Solutions LLC had previously

not been available in time for publication, but became available later in the day, the affected rate or rates may be republished at around

this time. Rate revisions will only be effected on the same day as initial publication and will only be republished if the change in the

rate exceeds one basis point. Any time a rate is revised, a footnote to the New York Federal Reserve’s publication would indicate

the revision. This revision threshold will be reviewed periodically by the New York Federal Reserve and may be changed based on market

conditions.

Because SOFR is published

by the New York Federal Reserve based on data received from other sources, we have no control over its determination, calculation or publication.

The information contained

in this section “Secured Overnight Financing Rate” is based upon the New York Federal Reserve’s Website and other U.S.

government sources.

Compounded SOFR Notes

Compounded SOFR notes will

bear interest at an interest rate based on a compounded average of the Secured Overnight Financing Rate (“SOFR”), and

any spread and/or spread multiplier and will be subject to the minimum interest rate and the maximum interest rate, if any.

The calculation agent will

determine Compounded SOFR, the interest rate and accrued interest for each interest period in arrears as soon as reasonably practicable

on or after the last day of the applicable observation period, and in any event on or prior to the business day immediately preceding

the relevant interest payment date, and will notify us of Compounded SOFR and such interest rate and accrued interest for each interest

period as soon as reasonably practicable after such determination, but in any event by the business day immediately prior to the interest

payment date.

Unless otherwise specified

in the applicable pricing supplement, the “Observation Period” in respect of each interest period for a series of the notes

will be the period from, and including, the date that is two U.S.

Government Securities Business Days preceding the

first date in such interest period to, but excluding, the date that is two U.S. Government Securities Business Days preceding the interest

payment date for such interest period.

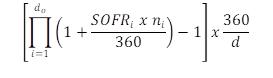

“Compounded

SOFR” means, with respect to any applicable interest period, the rate of return of a daily compounded interest investment over

the Observation Period corresponding to that interest period, calculated as follows:

“d0”,

for any Observation Period, is the number of U.S. Government Securities Business Days in the relevant Observation Period.

“i”

is a series of whole numbers from one to d0, each representing the relevant U.S. Government Securities Business Days in chronological

order from, and including, the first U.S. Government Securities Business Day in the relevant Observation Period.

“SOFRi”,

for any U.S. Government Securities Business Day “i” in the relevant Observation Period, is a reference rate equal to SOFR

in respect of that day.

“ni”

for any U.S. Government Securities Business Day “i” is the number of calendar days from, and including, such U.S. Government

Securities Business Day “i” to, but excluding, the following U.S. Government Securities Business Day “i+1”.

“d”

is the number of calendar days in the relevant Observation Period.

For these calculations,

the daily SOFR in effect on any U.S. Government Securities Business Day will be the applicable SOFR as reset on that date.

For purposes of determining

Compounded SOFR, “SOFR” means, with respect to any U.S. Government Securities Business Day:

| (1) | the Secured Overnight Financing Rate in respect of such U.S. Government Securities

Business Day as published by the New York Federal Reserve, as the administrator of such rate (or a successor administrator), on the New

York Federal Reserve’s Website on or about 5:00 p.m. (New York City time) on the immediately following U.S. Government Securities

Business Day; or |

| (2) | if the Secured Overnight Financing Rate in respect of such U.S. Government Securities

Business Day does not appear as specified in paragraph (1), unless both a Benchmark Transition Event and its related Benchmark Replacement

Date have occurred, the Secured Overnight Financing Rate in respect of the last U.S. Government Securities Business Day for which such

rate was published on the New York Federal Reserve’s Website; or |

| (3) | if a Benchmark Transition Event and its related Benchmark Replacement Date have occurred: |

·

the sum of: (a) the alternate rate of interest that has been selected or recommended by the Relevant Governmental Body as the replacement

for the then-current Benchmark and (b) the Benchmark Replacement Adjustment; or

| · | the sum of: (a) the ISDA Fallback Rate and (b)

the Benchmark Replacement Adjustment; or |

| · | the sum of: (a) the alternate

rate of interest that has been selected by us or our designee as the replacement for the then-current Benchmark giving due consideration

to any industry- |

accepted rate of interest as a

replacement for the then-current Benchmark for U.S. dollar-denominated floating rate notes at such time and (b) the Benchmark Replacement

Adjustment.

“Benchmark”

means the Compounded SOFR as defined above; provided that if a Benchmark Transition Event and its related Benchmark Replacement Date have

occurred with respect to the Compounded SOFR or the then-current Benchmark, then “Benchmark” means the applicable Benchmark

Replacement.

“Benchmark

Replacement” means the first alternative set forth in the order presented in clause (3) of the definition of “SOFR”

that can be determined by us or our designee as of the Benchmark Replacement Date. In connection with the implementation of a Benchmark

Replacement, we or our designee will have the right to make Benchmark Replacement Conforming Changes from time to time.

“Benchmark

Replacement Adjustment” means the first alternative set forth in the order below that can be determined by us or our designee

as of the Benchmark Replacement Date:

| (1) | the spread adjustment, or method for calculating or determining such spread adjustment,

(which may be a positive or negative value or zero) that has been selected or recommended by the Relevant Governmental Body for the applicable

Unadjusted Benchmark Replacement; |

| (2) | if the applicable Unadjusted Benchmark Replacement is equivalent to the ISDA Fallback

Rate, then the ISDA Fallback Adjustment; |

| (3) | the spread adjustment (which may be a positive or negative value or zero) that

has been selected by us or our designee giving due consideration to any industry-accepted spread adjustment, or method for calculating

or determining such spread adjustment, for the replacement of the then-current Benchmark with the applicable Unadjusted Benchmark Replacement

for U.S. dollar-denominated floating rate notes at such time. |

“Benchmark Replacement

Conforming Changes” means, with respect to any Benchmark Replacement, any technical, administrative or operational changes (including

changes to the definitions of “interest period” and “Observation Period,” timing and frequency of determining

rates and making payments of interest and other administrative matters) that we or our designee decide may be appropriate to reflect the

adoption of such Benchmark Replacement in a manner substantially consistent with market practice (or, if we or our designee decide that

adoption of any portion of such market practice is not administratively feasible or if we or our designee determine that no market practice

for use of the Benchmark Replacement exists, in such other manner as we or our designee determine is reasonably necessary).

“Benchmark

Replacement Date” means the earliest to occur of the following events with respect to the then-current Benchmark:

| (1) | in the case of clause (1) or (2) of the definition of “Benchmark Transition

Event,” the later of (a) the date of the public statement or publication of information referenced therein and (b) the date on which

the administrator of the Benchmark permanently or indefinitely ceases to provide the Benchmark; or |

| (2) | in the case of clause (3) of the definition of “Benchmark Transition Event,”

the date of the public statement or publication of information referenced therein. |

For the avoidance of doubt,

if the event giving rise to the Benchmark Replacement Date occurs on the same day as, but earlier than, the Reference Time in respect

of any determination, the Benchmark Replacement Date will be deemed to have occurred prior to the Reference Time for such determination.

“Benchmark

Transition Event” means the occurrence of one or more of the following events with respect to the then-current Benchmark:

| (1) | a public statement or publication of information by or on behalf of the administrator

of the |

Benchmark announcing that such

administrator has ceased or will cease to provide the Benchmark, permanently or indefinitely, provided that, at the time of such statement