Dana Petroleum

07/19/2005

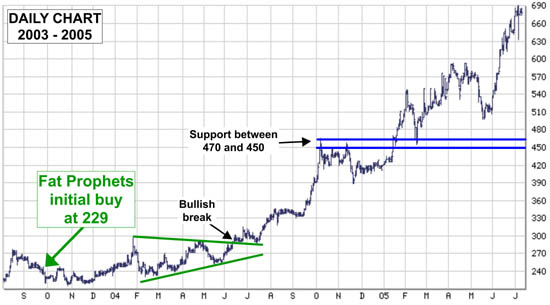

We have been heartened by the hub of activity at Dana Petroleum (DNX) in recent months. New production has been brought on stream while international exploration and development interests in Africa and the North Sea have been expanded. We remain excited by Dana's long-term earnings profile, which we expect to be driven by high oil prices, robust production, and an expanding exploration portfolio. We have been heartened by the hub of activity at Dana Petroleum (DNX) in recent months. New production has been brought on stream while international exploration and development interests in Africa and the North Sea have been expanded. We remain excited by Dana's long-term earnings profile, which we expect to be driven by high oil prices, robust production, and an expanding exploration portfolio.

Recently Dana confirmed that it had been awarded an eight-year exploration licence for a 6,540 square kilometre area offshore of Morocco. Dana plans to acquire a large 3D seismic survey of the field, with a view to commencing exploration drilling in 2007. This license builds on Dana's existing strong exploration position offshore West Africa. The area, which is relatively under-explored, could have significant potential.

Dana's North Sea exploration and appraisal programme also received a boost in June after the company increased its stake in the Barbara Field. Dana commenced drilling at a new well there earlier this month. Dana has also acquired a 60 percent interest in the Fiacre well from Endeavour Energy.

In another North Sea development with BP, Dana will receive a 100 percent interest in areas of North Sea Blocks 42/29 and 42/30, and an 81.28 percent interest in areas of Block 47/5c. Dana will now conduct studies and reprocess existing seismic data with a view to drilling an exploration well at the Colden Parva prospect. Preliminary gas in place estimates range up to 170 billion cubic feet (bcf). Dana will also review development options for the Monkwell gas discovery which has in place estimates ranging up to 100 bcf.

Dana has also received the go-ahead from the UK and Norwegian governments to develop an 8.8 percent interest in the Enoch oil field in the North Sea. Production is planned to start before the end of 2006 with Dana's share expected to be over 1,000 barrels per day.

We have held a bullish view on the oil price since 2001, and maintain a positive longer term outlook for the sector. On an individual stock basis, DNX remains one of our preferred exposures. Future production is un-hedged and is expected to grow to at least 23,000 boepd in 2005, and 30,000 boepd in 2006. As such, we view Dana's 2005 price earnings multiple of 10 times as undemanding.

|