As filed with the Securities and Exchange Commission on November 12, 2015

Registration No. 333-206365

UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3 to

Form F-4

REGISTRATION

STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Nokia Corporation

(Exact name of registrant as specified in its charter)

|

|

|

|

|

| Republic of Finland |

|

3663 |

|

Not Applicable |

| (State or other jurisdiction of incorporation or organization) |

|

(Primary Standard Industrial Classification Code Number) |

|

(I.R.S. Employer Identification Number) |

Karaportti 3, FI-02610 Espoo, Finland, +358 (0) 10-448-8000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Genevieve A. Silveroli, Nokia USA Inc., 6000 Connection Drive, Irving, Texas 75039, +1 (972) 374-3000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

|

|

| Riikka Tieaho Vice President, Corporate Legal Nokia Corporation

Karaportti 3 FI-02610

Espoo Finland

Tel. No.: +358 (0) 10-448-8000 |

|

Scott V. Simpson Michal Berkner

Skadden, Arps, Slate, Meagher & Flom (UK) LLP

40 Bank Street London E14

5DS United Kingdom

Tel. No.: +44 20-7519-7000 |

Approximate date of commencement of proposed sale to the

public: As soon as practicable after this registration statement becomes effective.

If this Form is

filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the

same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective

registration statement for the same offering. ¨

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender

Offer) ¨

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) x

The registrant hereby amends

this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective

in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission (the “SEC”), acting pursuant to said Section 8(a), may

determine.

Exchange Offer/Prospectus

The U.S. Offer to exchange Alcatel Lucent Shares and OCEANEs set forth in this exchange offer/prospectus is not made to any person located in the European Economic Area and the U.S. Offer to exchange Alcatel

Lucent ADSs set forth in this exchange offer/prospectus is only made to persons located in the European Economic Area pursuant to an exemption or exemptions from the Prospectus Directive (Directive 2003/71/EC, as amended). In addition, for the

purposes of the proposed French Offer and Admission (both terms as defined below), this exchange offer/prospectus is not offer documentation or a prospectus and no such person should subscribe for or purchase any transferable securities referred to

in this document except on the basis of information contained in the prospectus approved by the Finnish Financial Supervisory Authority and “passported” in France in accordance with the Prospectus

Directive (the “Listing Prospectus”), and the separate French Offer documentation filed with the French stock market authority (Autorité des marchés financiers, or “AMF”) (the “French Offer

Documentation”), which in each case are proposed to be published by Nokia in due course in connection with the proposed French Offer and the Admission of the Nokia Shares to Euronext Paris. A copy of the Listing Prospectus and the French Offer

Documentation will, following publication, be available on Nokia’s website at www.nokia.com. None of the Listing Prospectus, the French Offer Documentation or the information on Nokia’s website forms a part of

this exchange offer/prospectus, nor are such documents incorporated by reference herein.

U.S. Offer to Exchange

All

Ordinary Shares held

by U.S. Holders

American Depositary Shares

OCEANEs held by U.S. Holders

of

ALCATEL LUCENT

for

0.5500 Nokia Share per Alcatel Lucent Ordinary Share

0.5500 Nokia American Depositary Share per Alcatel Lucent American Depositary Share

0.6930

Nokia Share per 2018 Alcatel Lucent OCEANE

0.7040 Nokia Share per 2019 Alcatel Lucent OCEANE

0.7040 Nokia Share per 2020 Alcatel Lucent OCEANE

by

NOKIA CORPORATION

Nokia Corporation (“Nokia”), a Finnish corporation, is conducting, upon the terms and subject to the conditions set forth in this exchange offer/prospectus and the French Offer Documentation, an exchange

offer comprised of two offers (separately, the “U.S. Offer” and the “French Offer” and collectively, the “Exchange Offer”). The U.S. Offer is being made pursuant to this exchange offer/prospectus to:

| |

• |

|

all U.S. holders (within the meaning of Rule 14d-1(d) under the U.S. Securities Exchange Act of 1934 (the “Exchange Act”)) of outstanding ordinary

shares, nominal value EUR 0.05 per share (the “Alcatel Lucent Shares”) of Alcatel Lucent, a French société anonyme (“Alcatel Lucent”), |

| |

• |

|

all holders of outstanding Alcatel Lucent American depositary shares, each representing one Alcatel Lucent Share (the “Alcatel Lucent ADSs”), wherever

located, and |

| |

• |

|

all U.S. holders of outstanding (i) EUR 628 946 424.00 Alcatel Lucent bonds convertible into new Alcatel Lucent Shares or exchangeable for

existing Alcatel Lucent Shares due on July 1, 2018 (the “2018 OCEANEs”), (ii) EUR 688 425 000.00 Alcatel Lucent bonds convertible into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on

January 30, 2019 (the “2019 OCEANEs”) and (iii) EUR 460 289 979.90 Alcatel Lucent bonds convertible into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on January 30, 2020 (the

“2020 OCEANEs” and, together with the 2018 OCEANEs and the 2019 OCEANEs, the “OCEANEs” and, together with the Alcatel Lucent Shares and the Alcatel Lucent ADSs, the “Alcatel Lucent Securities”).

|

Holders of Alcatel Lucent ADSs located outside of the United States may participate in the U.S. Offer only to the

extent the local laws and regulations applicable to those holders permit them to participate in the U.S. Offer. Holders of Alcatel Lucent Securities who are restricted from participating in the U.S. Offer pursuant to the Sanctions (as defined below)

may not participate in the U.S. Offer.

For every Alcatel Lucent Share you validly tender into, and do not withdraw from, the U.S. Offer, you will

receive 0.5500 share of Nokia (a “Nokia Share”). For every Alcatel Lucent ADS you validly tender into, and do not withdraw from, the U.S. Offer, you will receive 0.5500 Nokia American depositary share (a “Nokia ADS”), each Nokia

ADS representing one Nokia Share. For every 2018 OCEANE you validly tender into, and do not withdraw from, the U.S. Offer, you will receive 0.6930 Nokia Share, for every 2019 OCEANE you validly tender into, and do not withdraw from, the U.S. Offer,

you will receive 0.7040 Nokia Share, and for every 2020 OCEANE you validly tender into, and do not withdraw from, the U.S. Offer, you will receive 0.7040 Nokia Share.

The French Offer to exchange 0.5500 Nokia Share for every Alcatel Lucent Share, 0.6930 Nokia Share for every 2018 OCEANE, 0.7040 Nokia Share for every 2019 OCEANE, and 0.7040 Nokia Share for every 2020 OCEANE, is

being made pursuant to the French Offer Documentation available to holders of Alcatel Lucent Shares and OCEANEs located in France (holders of Alcatel Lucent Shares and OCEANEs located outside of France may not participate in the French Offer except

if, pursuant to the local laws and regulations applicable to those holders, they are permitted to participate in the French Offer).

No fractional Nokia

Shares or fractional Nokia ADSs will be issued. Holders of Alcatel Lucent Securities tendering into the U.S. Offer or the French Offer will receive cash in lieu of any fractional Nokia Shares or Nokia ADSs to which such holders may otherwise be

entitled, following the implementation of a mechanism to resell such fractional Nokia Shares or Nokia ADSs.

Holders of options to acquire Alcatel

Lucent Shares (“Alcatel Lucent Stock Options”) who wish to tender in the Exchange Offer or the subsequent offering period, if any, must exercise their Alcatel Lucent Stock Options, and Alcatel Lucent Shares must be issued to such holders

prior to the Expiration Date (as defined below) or the expiration of the subsequent offering period, as applicable. Pursuant to the Memorandum of Understanding dated April 15, 2015 between Nokia and Alcatel Lucent, as amended on October 28,

2015 (the “Memorandum of Understanding”), Alcatel Lucent agreed to accelerate or waive certain terms of the Alcatel Lucent Stock Options, subject to certain conditions.

Restricted stock granted by Alcatel Lucent (“Alcatel Lucent Performance Shares”) cannot be tendered in the Exchange Offer or the subsequent offering period, if any, unless such Alcatel Lucent Performance

Shares have vested and are transferable prior to the Expiration Date (as defined below) or the expiration of the subsequent offering period, as applicable. Pursuant to the Memorandum of Understanding, Nokia and Alcatel Lucent agreed to implement a

mechanism with respect to unvested Performance Shares granted before April 15, 2015 pursuant to which the beneficiaries may waive their rights to receive Alcatel Lucent Performance Shares in exchange for Alcatel Lucent Shares, subject to

certain conditions.

As a result of the matters described in “The Transaction—Reasons

for the Alcatel Lucent Board of Directors’ Approval of the Transaction”, the participating members of the Alcatel Lucent board of directors, taking into account the factors described in that section, unanimously:

| |

(i) |

determined that the Exchange Offer is in the best interest of Alcatel Lucent, its employees and its stakeholders (including the holders of the

Alcatel Lucent Shares and holders of other

Alcatel Lucent Securities); |

i

| |

(ii) |

recommended that all holders of Alcatel Lucent Shares and holders of Alcatel Lucent ADSs tender their Alcatel Lucent Shares and/or their Alcatel Lucent ADSs pursuant to the Exchange Offer; and |

| |

(iii) |

recommended that all holders of OCEANEs tender their OCEANEs pursuant to the Exchange Offer. |

The U.S. Offer is being made on the terms and subject to the conditions set forth in “The Exchange Offer” section of this exchange offer/prospectus

beginning on page 115 and the related forms of letters of transmittal.

THE U.S. OFFER AND WITHDRAWAL RIGHTS FOR TENDERS OF ALCATEL LUCENT SHARES AND

OCEANEs IN THE U.S. OFFER WILL EXPIRE AT 11:00 A.M., NEW YORK CITY TIME (5:00 P.M. PARIS TIME), ON DECEMBER 23, 2015 (AS SUCH TIME AND DATE MAY BE EXTENDED, THE “EXPIRATION DATE”), UNLESS THE EXCHANGE OFFER IS EXTENDED.

THE DEADLINE FOR VALIDLY TENDERING AND WITHDRAWING ALCATEL LUCENT ADSs IN THE U.S. OFFER IS 5:00 P.M., NEW YORK CITY TIME ON THE U.S. BUSINESS

DAY IMMEDIATELY PRECEDING THE EXPIRATION DATE, WHICH WILL BE DECEMBER 22, 2015 (AS SUCH TIME AND DATE MAY BE EXTENDED, THE “ADS TENDER DEADLINE”), UNLESS THE U.S. OFFER IS EXTENDED.

Nokia Shares are traded on NASDAQ OMX Helsinki Ltd. (the “Nasdaq Helsinki”) under the symbol “NOKIA” and Nokia ADSs are traded on the New York

Stock Exchange (the “NYSE”) under the symbol “NOK.” On November 10, 2015, the most recent practicable trading day before the opening of the Exchange Offer, the closing price of Nokia Shares listed on the Nasdaq Helsinki was

EUR 6.76 and the closing price of Nokia ADSs on the NYSE was USD 7.22.

Nokia has applied for the Nokia Shares (including the Nokia

Shares to be issued in connection with the Exchange Offer) to be listed on Euronext Paris (the “Admission”). Nokia expects to request that Admission be approved to take effect prior to the Completion of the Exchange Offer. In addition,

Nokia will apply for listing of the Nokia Shares and Nokia ADSs to be issued in connection with the Exchange Offer on the Nasdaq Helsinki and the NYSE, respectively.

Alcatel Lucent Shares are traded on Euronext Paris under the symbol “ALU” and Alcatel Lucent ADSs are traded on the NYSE under the symbol “ALU.” OCEANEs are traded on Euronext Paris, under the

symbol “YALU” for the 2018 OCEANEs, “YALU1” for the 2019 OCEANEs and “YALU2” for the 2020 OCEANEs. On November 10, 2015, the closing price of Alcatel Lucent Shares on Euronext Paris was EUR 3.69 and the closing

price of Alcatel Lucent ADSs on the NYSE was USD 3.94 and the latest reasonably available quotations for the OCEANEs was EUR 4.61 for the 2018 OCEANEs, EUR 4.74 for the 2019 OCEANEs and EUR 4.73 for the 2020 OCEANEs. As promptly

as practicable following Completion of the Exchange Offer and subject to applicable law and Euronext Paris rules, Nokia intends to request Euronext Paris to delist the Alcatel Lucent Shares and OCEANEs from the regulated market of Euronext Paris. As

promptly as practicable following Completion of the Exchange Offer, Nokia also intends to cause Alcatel Lucent to terminate the deposit agreement in respect of the Alcatel Lucent ADSs (the “Alcatel Lucent deposit agreement”), to seek to

delist the Alcatel Lucent ADSs from the NYSE and, subject to applicable law, to deregister the Alcatel Lucent Shares and Alcatel Lucent ADSs and terminate the reporting obligations of Alcatel Lucent under the Exchange Act.

ii

SEE THE “RISK FACTORS” SECTION OF THIS EXCHANGE OFFER/PROSPECTUS BEGINNING ON

PAGE 25 FOR A DISCUSSION OF IMPORTANT RISK FACTORS THAT YOU SHOULD CONSIDER BEFORE DECIDING WHETHER OR NOT TO TENDER YOUR ALCATEL LUCENT SECURITIES INTO THE U.S. OFFER.

Nokia has not authorized any person to provide any information or to make any representation in connection with the U.S. Offer other than the information contained or incorporated by reference in this exchange

offer/prospectus, and if any person provides any of this information or makes any representation of this kind, that information or representation must not be relied upon as having been authorized by Nokia.

Nokia is not asking you for a proxy pursuant to this exchange offer/prospectus and you are requested not to send to Nokia a proxy in response hereto.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in

the transactions described in this exchange offer/prospectus or passed upon the adequacy or accuracy of this exchange offer/prospectus. Any representation to the contrary is a criminal offense.

The date of this exchange offer/prospectus is November 12, 2015.

iii

CERTAIN DEFINED TERMS

Unless otherwise specified or if the context so requires in this exchange offer/prospectus:

| |

• |

|

“Admission” refers to Nokia’s application

for the Nokia Shares (including the Nokia Shares to be issued in connection with the Exchange Offer) to be listed on Euronext Paris. |

| |

• |

|

“ADS Tender Deadline” refers to the deadline for

validly tendering and withdrawing Alcatel Lucent ADSs in the U.S. Offer, set for 5:00 P.M., New York City time on the U.S. business day immediately preceding the Expiration Date, which will be December 22, 2015 (as such time and date may be

extended). |

| |

• |

|

“Alcatel Lucent” refers to Alcatel Lucent, a

French société anonyme. |

| |

• |

|

“Alcatel Lucent ADSs” refer to American

depositary shares each representing one Alcatel Lucent Share. |

| |

• |

|

“Alcatel Lucent 2014 Form 20-F” refers to

Alcatel Lucent’s Annual Report on Form 20-F for the year ended December 31, 2014 filed with the SEC on March 24, 2015. |

| |

• |

|

“Alcatel Lucent Securities” refer to the Alcatel

Lucent Shares, the Alcatel Lucent ADSs and the OCEANEs. |

| |

• |

|

“Alcatel Lucent Shares” refer to ordinary

shares, nominal value EUR 0.05 per share of Alcatel Lucent. |

| |

• |

|

“Alcatel Lucent Stock Options” refer to options

to acquire Alcatel Lucent Shares. |

| |

• |

|

“Alcatel Lucent Performance Shares” refer to

restricted stock granted by Alcatel Lucent. |

| |

• |

|

“AMF” refers to the French stock market

authority (Autorité des marchés financiers). |

| |

• |

|

“AMF General Regulation” refers to Article 236-3

of the General Regulation (Règlement général) published by the AMF. |

| |

• |

|

“ATOP System” refers to the automated tender

system of DTC. |

| |

• |

|

“Completion of the Exchange Offer,”

“completion of the U.S. Offer,” “completion of the French Offer” or “completion of the subsequent offering period” refer to settlement and delivery of the

Nokia Shares to the holders of Alcatel Lucent Securities in accordance with the terms of the Exchange Offer and Conditions after announcement of the successful results of the French Offer by the AMF (taking into account the results of the U.S.

Offer) or the results of the subsequent offering period, as applicable. |

| |

• |

|

“Conditions” refer collectively to the Minimum

Tender Condition and the Nokia Shareholder Approval. |

| |

• |

|

“Convertible Bond” refers to Nokia’s EUR

750 million convertible bond issued in October 2012 and maturing in 2017. |

| |

• |

|

“DTC” refers to The Depository Trust Company,

the U.S. clearing and settlement system for equity securities. |

| |

• |

|

“Exchange Offer” refers collectively to the U.S.

Offer and the French Offer. |

| |

• |

|

“Expiration Date” refers to the expiration date

of the the U.S. Offer and withdrawal rights for tenders of Alcatel Lucent Shares and OCEANEs in the U.S. Offer, set for 11:00 A.M., New York City time (5:00 P.M. Paris time), on December 23, 2015 (as such time and date may be extended).

|

| |

• |

|

“French business day” refers to any day, other

than a Saturday, Sunday or French public holiday. |

iv

| |

• |

|

“French Offer” refers to Nokia’s exchange

offer in France to exchange 0.5500 Nokia Share for every Alcatel Lucent Share, 0.6930 Nokia Share for every 2018 OCEANE, 0.7040 Nokia Share for every 2019 OCEANE and 0.7040 Nokia Share for every 2020 OCEANE, made pursuant to separate French Offer

Documentation. |

| |

• |

|

“French trading day” refers to any day on which

Euronext Paris is generally open for business. |

| |

• |

|

“French Offer Documentation” refers to the

French Offer documentation filed with the AMF by Nokia. |

| |

• |

|

“IFRS” refers to the International Financial

Reporting Standards as issued by the International Accounting Standards Board. |

| |

• |

|

“Mandatory Minimum Acceptance Threshold” refers

to a number of Alcatel Lucent Shares representing more than 50% of the Alcatel Lucent share capital or voting rights, taking into account, if necessary, the Alcatel Lucent Shares resulting from the conversion of the OCEANEs validly tendered into the

Exchange Offer. Refer to “The Exchange Offer—Terms of the Exchange Offer—Conditions to the Exchange Offer” for a description of how the Mandatory Minimum Acceptance Threshold is calculated. |

| |

• |

|

“Memorandum of Understanding” refers to the

Memorandum of Understanding dated April 15, 2015, as amended on October 28, 2015, between Nokia and Alcatel Lucent. |

| |

• |

|

“Minimum Tender Condition” refers to the number

of Alcatel Lucent Securities validly tendered in accordance with the terms of the Exchange Offer representing, on the date of announcement by the AMF of the results of the French Offer taking into account the results of the U.S. Offer, more than 50%

of the Alcatel Lucent Shares on a fully diluted basis. |

| |

• |

|

“MoU Business Day” refers to any day on which

banking institutions are open for regular business in Finland, France and the United States which is not a Saturday, a Sunday or a public holiday. |

| |

• |

|

“Nasdaq Helsinki” refers to NASDAQ OMX Helsinki

Ltd. |

| |

• |

|

“Nokia,” the “company,” “we,” “us” or “our” refers to Nokia Corporation,

a Finnish corporation. |

| |

• |

|

“Nokia ADSs” refer to American depositary shares

each representing one Nokia Share. |

| |

• |

|

“Nokia depositary” refers to Citibank, N.A., the

depositary for the Nokia ADSs pursuant to a deposit agreement. |

| |

• |

|

“Nokia 2014 Form 20-F” refers to Nokia’s

Annual Report on Form 20-F for the year ended December 31, 2014 filed with the SEC on March 19, 2015. |

| |

• |

|

“Nokia Shareholder Approval” refers to Nokia

shareholders having approved the authorization for the Nokia board of directors to issue such number of new Nokia Shares as may be necessary for delivering the Nokia Shares offered in consideration for the Alcatel Lucent Securities tendered into the

Exchange Offer and for the Completion of the Exchange Offer. |

| |

• |

|

“Nokia Shares” refer to shares of Nokia

Corporation. |

| |

• |

|

“NYSE” refers to the New York Stock Exchange.

|

| |

• |

|

“2018 OCEANEs” refer to EUR

628 946 424.00 Alcatel Lucent bonds convertible into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on July 1, 2018. |

v

| |

• |

|

“2019 OCEANEs” refer to EUR

688 425 000.00 Alcatel Lucent bonds convertible into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on January 30, 2019. |

| |

• |

|

“2020 OCEANEs” refer to EUR

460 289 979.90 Alcatel Lucent bonds convertible into new Alcatel Lucent Shares or exchangeable for existing Alcatel Lucent Shares due on January 30, 2020. |

| |

• |

|

“OCEANEs” refer to the 2018 OCEANEs, the 2019

OCEANEs and the 2020 OCEANEs. |

| |

• |

|

“Schedule TO” refers to the tender offer

statement on Schedule TO. |

| |

• |

|

“U.S. business day” refers to any day, other

than a Saturday, Sunday or U.S. federal holiday or a day on which banking institutions are required or authorized by law or executive order to be closed in New York, New York. |

| |

• |

|

“U.S. exchange agent” refers to Citibank, N.A.

|

| |

• |

|

“U.S. Offer” refers to the exchange offer to be

made in the United States. |

vi

TABLE OF CONTENTS

vii

viii

ix

Nokia Shares are listed and traded on the Nasdaq Helsinki and Nokia ADSs are listed and traded on the NYSE and are

registered under the Exchange Act. Alcatel Lucent Shares and OCEANEs are listed and traded on Euronext Paris and Alcatel Lucent ADSs are listed and traded on the NYSE and are registered under the Exchange Act. Accordingly, the Exchange Offer,

insofar as it relates to the Alcatel Lucent Shares, OCEANEs and Alcatel Lucent ADSs, and the related issuance of Nokia Shares are subject to the rules and regulations of the United States, France and Finland. Some of the information contained in

this exchange offer/prospectus is included because it is required to be included in the French Offer Documentation or in the Finnish prospectus. Some of that information has been prepared in accordance with French or Finnish format and style, which

differs from the U.S. format and style for documents of this type.

This exchange offer/prospectus incorporates by reference important business and

financial information about Nokia and Alcatel Lucent that is contained in their respective filings with the SEC but which is not included in, or delivered with, this exchange offer/prospectus. This information is available on the SEC’s website

at www.sec.gov and from other sources. For more information about how to obtain copies of these documents, see the “Where You Can Find More Information” section of this exchange offer/prospectus. Nokia will also make copies of this

information available to you without charge upon your written or oral request to Georgeson Inc. at (800) 314-4549. In order to receive timely delivery of these documents, holders of Alcatel Lucent

Shares and OCEANEs must make such a request no later than five U.S. business days before the then-scheduled Expiration Date and holders of Alcatel Lucent ADSs must make such a request no later than five U.S. business days before the then-scheduled

ADS Tender Deadline. The Expiration Date is currently December 23, 2015 and the ADS Tender Deadline is currently December 22, 2015 but the actual deadlines will be different if the U.S. Offer is extended.

x

QUESTIONS AND ANSWERS ABOUT THE EXCHANGE OFFER

Below are some of the questions that you as a holder of Alcatel Lucent Securities may have regarding the Exchange Offer and answers to those questions. The

answers to these questions do not contain all information relevant to your decision whether to tender your Alcatel Lucent Securities. To better understand the Exchange Offer, Nokia (also referred to as “we,” “us,” or

“our”) urges you to read carefully the remainder of this exchange offer/prospectus and the accompanying letters of transmittal.

Why am I receiving this exchange offer/prospectus?

Nokia, a

Finnish corporation, is offering, upon the terms and subject to the Conditions set forth in this exchange offer/prospectus and the French Offer Documentation, to acquire all of the Alcatel Lucent Securities through the Exchange Offer whereby Alcatel

Lucent Securities will be exchanged for Nokia Shares or Nokia ADSs, as described below. The Exchange Offer is comprised of the U.S. Offer and the French Offer. The U.S. Offer is being made pursuant to this exchange offer/prospectus to all

U.S. holders of outstanding Alcatel Lucent Shares, all U.S. holders of outstanding OCEANEs and all holders of outstanding Alcatel Lucent ADSs, wherever located. Holders of Alcatel Lucent ADSs located outside of the United States may participate

in the U.S. Offer only to the extent the local laws and regulations applicable to those holders permit them to participate in the U.S. Offer. Holders of Alcatel Lucent Securities who are restricted from participating in the U.S. Offer pursuant to

the Sanctions may not participate in the U.S. Offer.

What is the purpose of the Exchange Offer?

The purpose of the Exchange Offer is for Nokia to acquire all of the Alcatel Lucent Securities in order to combine the businesses of Nokia and Alcatel Lucent.

What will I receive if the Exchange Offer is completed?

Following the Completion of the Exchange Offer, you will receive:

| |

• |

|

0.5500 Nokia Share for every Alcatel Lucent Share you validly tender into, and do not withdraw from, the U.S. Offer, |

| |

• |

|

0.5500 Nokia ADS for every Alcatel Lucent ADS you validly tender into, and do not withdraw from, the U.S. Offer, and |

| |

• |

|

0.6930 Nokia Share for every 2018 OCEANE, 0.7040 Nokia Share for every 2019 OCEANE and 0.7040 Nokia Share for every 2020 OCEANE you validly tender into, and do

not withdraw from, the U.S. Offer. |

The French Offer comprises an offer to exchange 0.5500 Nokia Share for every Alcatel Lucent Share,

0.6930 Nokia Share for every 2018 OCEANE, 0.7040 Nokia Share for every 2019 OCEANE and 0.7040 Nokia Share for every 2020 OCEANE, made pursuant to separate French Offer Documentation available to holders of Alcatel Lucent Shares and OCEANEs located

in France (holders of Alcatel Lucent Shares and OCEANEs located outside of France may not participate in the French Offer except if, pursuant to the local laws and regulations applicable to those holders, they are permitted to participate in the

French Offer).

No fractional Nokia Shares or fractional Nokia ADSs will be issued. Holders of Alcatel Lucent Securities tendering into the U.S. Offer

or the French Offer will receive cash in lieu of any fractional Nokia Shares or Nokia ADSs to which such holders may otherwise be entitled, following the implementation of a mechanism to resell such fractional Nokia Shares or Nokia ADSs.

xi

What options are available to the holders of the OCEANEs in connection with the Exchange Offer?

In connection with the Exchange Offer, holders of the OCEANEs may elect to take any of the following steps with respect to their OCEANEs:

| |

• |

|

Tender the OCEANEs into the Exchange Offer. The Exchange Offer is being made to all holders of the OCEANEs issued and outstanding and such holders

may accept the Exchange Offer by tendering their OCEANEs into the U.S. Offer or the French Offer, as applicable. For every 2018 OCEANE you validly tender into, and do not withdraw from, the U.S. Offer, you will receive 0.6930 Nokia Share, for every

2019 OCEANE you validly tender into, and do not withdraw from, the U.S. Offer, you will receive 0.7040 Nokia Share and for every 2020 OCEANE you validly tender into, and do not withdraw from, the U.S. Offer, you will receive 0.7040 Nokia Share.

|

| |

• |

|

Convert the OCEANEs into or exchange the OCEANEs for Alcatel Lucent Shares at the change of control conversion/exchange ratio. Prior to the opening

of the Exchange Offer the conversion/exchange ratio was 1.06 Alcatel Lucent Share for every 2018 OCEANE, 1.00 Alcatel Lucent Share for every 2019 OCEANE and 1.00 Alcatel Lucent Share for every 2020 OCEANE. The opening of the Exchange Offer has

resulted in a temporary adjustment to the conversion/exchange ratios applicable to each series of OCEANEs. The adjusted conversion/exchange ratios resulting from the Exchange Offer are 1.26 Alcatel Lucent Shares for every 2018 OCEANE, 1.28 Alcatel

Lucent Share for every 2019 OCEANE and 1.28 Alcatel Lucent Share for every 2020 OCEANE. The right of OCEANEs holders to obtain Alcatel Lucent Shares on the basis of the adjusted conversion/exchange ratios will expire, (x) if the AMF declares

that the French Offer is successful, on the date that is 15 French business days after the publication by the AMF of the results of the French Offer (taking into account the results of the U.S. Offer), which is currently expected to be approximately

seven and in no event later than nine French trading days following the Expiration Date, or, if there is a subsequent offering period, the date that is 15 French business days after the end of the subsequent offering period of the French Offer;

(y) if the AMF declares that the French Offer (taking into account the results of the U.S. Offer) is unsuccessful, the date of publication by the AMF of the result of the French Offer; or (z) if Nokia withdraws the Exchange Offer, the date

on which such withdrawal is published. If the holders of the OCEANEs choose to convert their OCEANEs into or exchange their OCEANEs for Alcatel Lucent Shares, they may then be able to tender such Alcatel Lucent Shares into the Exchange Offer in

accordance with its terms and Conditions. |

| |

• |

|

After the Completion of the Exchange Offer, request an early redemption of their OCEANEs. If the Exchange Offer is successful (resulting in a

change of control of Alcatel Lucent under the terms of the OCEANEs), each holder of the OCEANEs who did not tender their OCEANEs into the Exchange Offer may request that Alcatel Lucent redeem their OCEANEs for cash at par plus, as applicable,

accrued interest from the last interest payment date for each series of the OCEANEs until the early redemption date. |

| |

• |

|

Early redemption decided by the general meeting of the holders of any series of OCEANEs. In the event the Alcatel Lucent Shares cease to be listed

on Euronext Paris and are not listed on any other regulated market within the European Union within the meaning of the European Union Directive 2004/39/EC, and the Alcatel Lucent ADSs or the Alcatel Lucent Shares cease to be listed on a regulated

market in the United States, the representative of the body for each type of OCEANE (le représentant de la masse) may, upon decision of the general meeting of the holders of such OCEANEs, other than Nokia if it holds more than 10% of

the relevant series of OCEANEs, make all of such OCEANEs redeemable by Alcatel Lucent at a price in cash equal to par plus, as applicable, accrued interest from the last interest payment date for each of the OCEANEs until the early redemption date.

|

xii

In addition to the foregoing and in accordance with the terms of the OCEANEs, if the Exchange Offer is successful and

subject to applicable law, Nokia reserves the right to cause Alcatel Lucent to redeem for cash at par value plus, as applicable, accrued interest, any series of the OCEANEs if less than 15% of the issued OCEANEs of any such series remain outstanding

at any time.

Holders of OCEANEs that remain outstanding after the events described above will remain creditors of Alcatel Lucent with the ability to

convert their OCEANEs into or exchange their OCEANEs for Alcatel Lucent Shares at the then applicable conversion/exchange ratio.

Holders of the 2018

OCEANEs who do not convert their 2018 OCEANEs into Alcatel Lucent Shares prior to December 31, 2015, the record date for the next interest payment with respect to the 2018 OCEANEs, are expected to be eligible to receive such interest payment on

January 4, 2016, whether or not they tender their 2018 OCEANEs into the Exchange Offer.

As promptly as possible following Completion of the Exchange

Offer and subject to applicable law and stock exchange rules, Nokia intends to request Euronext Paris to delist Alcatel Lucent Shares and OCEANEs from the regulated market of Euronext Paris and seek to delist Alcatel Lucent ADSs from the NYSE.

For the avoidance of doubt, Nokia does not intend to arrange for any of the OCEANEs to become convertible into Nokia convertible bonds whether as a

part of the Exchange Offer or otherwise.

If OCEANEs are converted into or exchanged for Alcatel Lucent Shares during the Exchange Offer and the

Exchange Offer is unsuccessful, will former holders of OCEANEs have to surrender their Alcatel Lucent Shares?

No. After conversion/exchange has

taken place, the OCEANEs are no longer outstanding and the relevant Alcatel Lucent Shares will not have to be surrendered if the Exchange Offer is not successful.

Can holders of Alcatel Lucent Stock Options and Performance Shares participate in the Exchange Offer?

Holders

of options to acquire Alcatel Lucent Shares who wish to tender into the Exchange Offer or the subsequent offering period, if any, must exercise their Alcatel Lucent Stock Options, and Alcatel Lucent Shares must be issued to such holders prior to the

Expiration Date or the expiration of the subsequent offering period, as applicable.

Pursuant to the Memorandum of Understanding, Alcatel Lucent agreed

to accelerate or waive certain terms of the Alcatel Lucent Stock Options, subject to certain conditions.

Alcatel Lucent Performance Shares granted by

Alcatel Lucent cannot be tendered in the Exchange Offer or the subsequent offering period, if any, unless such Alcatel Lucent Performance Shares have vested and are transferable prior to the Expiration Date or the expiration of the subsequent

offering period, as applicable.

Pursuant to the Memorandum of Understanding, Nokia and Alcatel Lucent agreed to implement a mechanism with respect to

unvested Performance Shares granted before April 15, 2015 pursuant to which the beneficiaries may waive their rights to receive Performance Shares in exchange for Alcatel Lucent Shares, subject to certain conditions.

What percentage of Nokia will holders of Alcatel Lucent Securities own after the Exchange Offer?

After Completion of the Exchange Offer and assuming that all Alcatel Lucent Securities are tendered into the Exchange Offer or the subsequent offering period, if any, former holders of Alcatel Lucent

xiii

Securities are expected to own approximately 33.5% of the issued and outstanding Nokia Shares on a fully diluted basis (based on the number of shares outstanding on December 31, 2014).

What are the benefits of a combination of Nokia and Alcatel Lucent?

We believe that the combination of Nokia’s and Alcatel Lucent’s businesses will create significant value for stakeholders of both companies. Following the Completion of the Exchange Offer, Nokia will be

well-positioned to create the foundation of seamless connectivity for people and things wherever they are. We believe that this foundation is essential for enabling the next wave of technological change, including the “internet of things”

and transition to the cloud.

The strategic rationale for combining the two companies includes:

| |

• |

|

creation of end-to-end portfolio scope and scale player with leading global positions across products, software and services to meet changing industry paradigms;

|

| |

• |

|

complementary offerings, customers and geographic footprint; |

| |

• |

|

enhanced research and development capabilities creating an innovation powerhouse with significant combined R&D resources; |

| |

• |

|

the recent execution track-record on both sides and common vision for the future; |

| |

• |

|

the opportunity to realize significant cost savings and other synergies; and |

| |

• |

|

the development of a robust capital structure and strong balance sheet. |

Does Alcatel Lucent support the Exchange Offer?

Yes. At their meeting of October 28, 2015 and as a result

of the matters described in the section entitled “The Transaction—Reasons for the Alcatel Lucent Board of Directors’ Approval of the Transaction”, the participating members of the Alcatel Lucent board of directors, taking into

account the factors described in that section, unanimously:

| |

(i) |

determined that the Exchange Offer is in the best interest of Alcatel Lucent, its employees and its stakeholders (including the holders of the Alcatel Lucent Shares and holders

of other Alcatel Lucent Securities); |

| |

(ii) |

recommended that all holders of Alcatel Lucent Shares and holders of Alcatel Lucent ADSs tender their Alcatel Lucent Shares and/or their Alcatel Lucent ADSs pursuant to the

Exchange Offer; and |

| |

(iii) |

recommended that all holders of OCEANEs tender their OCEANEs pursuant to the Exchange Offer. |

What is the market value of my Alcatel Lucent Securities as of a recent date?

On November 10, 2015, the

most recent practicable trading day before the opening of the Exchange Offer, the closing price of an Alcatel Lucent Share on Euronext Paris was EUR 3.69, the closing price of an Alcatel Lucent ADS on the NYSE was USD 3.94, the last reasonably

available quotation of a 2018 OCEANE was EUR 4.61, the last reasonably available quotation of a 2019 OCEANE was EUR 4.74 and the last reasonably available quotation of a 2020 OCEANE was EUR 4.73. Please obtain a recent quotation for your

Alcatel Lucent Securities prior to deciding whether or not to tender.

xiv

What is the expected governance structure of the combined company?

It is proposed that following the Completion of the Exchange Offer, Nokia’s corporate governance structure will include the following:

| |

• |

|

Chairman of the board of directors: Risto Siilasmaa; |

| |

• |

|

President and Chief Executive Officer: Rajeev Suri; |

| |

• |

|

Nokia’s board of directors having ten members, including Louis R. Hughes, Jean C. Monty and Olivier Piou, who have been nominated jointly by the Corporate

Governance & Nomination committee of the Nokia board of directors and by Alcatel Lucent. If elected, Olivier Piou is expected to serve as Vice Chairman of Nokia; and |

| |

• |

|

Leadership built on strengths of both Nokia and Alcatel Lucent. |

Appointment of members of the Nokia board of directors is subject to approval by Nokia shareholders.

What are the

Conditions to the U.S. Offer?

Nokia’s obligation to accept, and to exchange, any Alcatel Lucent Securities validly tendered into the U.S. Offer

is subject only to:

| |

• |

|

the Minimum Tender Condition; and |

| |

• |

|

the Nokia Shareholder Approval. |

Subject to

applicable SEC and AMF rules and regulations, Nokia reserves the right, in its sole discretion, to waive the Minimum Tender Condition to any level at or above the Mandatory Minimum Acceptance Threshold.

How does the Nokia shareholders’ vote impact the deal?

Nokia’s obligation to accept, and to exchange, any Alcatel Lucent Securities validly tendered into the Exchange Offer will be subject to, among other

Conditions, the Nokia Shareholder Approval.

Nokia’s extraordinary general meeting of shareholders has been convened for December 2, 2015 to

consider and vote on the resolution contemplated by the Nokia Shareholder Approval. Proxy materials for such meeting were separately distributed by Nokia prior to the date of this exchange offer/prospectus. The resolution must be approved by

shareholders representing at least two-thirds of the votes cast and Nokia Shares represented at such extraordinary general meeting of Nokia’s shareholders.

What happens if less than 100% of Alcatel Lucent Securities have been purchased following the Completion of the Exchange Offer or the subsequent offering period, if any?

If, at the Completion of the Exchange Offer or the subsequent offering period, if any, Nokia owns 95% or more of the share capital and voting rights of Alcatel

Lucent (Alcatel Lucent Shares held in treasury being considered as held by Nokia for the purpose of the calculation), Nokia intends to request from the AMF, within three months of the expiration of the French Offer period or the subsequent offering

period, if any, the implementation of a squeeze-out for the remaining outstanding Alcatel Lucent Shares for cash consideration. In addition, if, at the Completion of the Exchange Offer or the subsequent offering period, if any, Nokia owns 95% or

more of the sum of the outstanding Alcatel Lucent Shares and the Alcatel Lucent Shares issuable upon conversion of all of the OCEANEs then outstanding (Alcatel Lucent Shares held in treasury being considered as held by Nokia for the purpose of the

calculation), Nokia intends to request from the AMF, within three months of the expiration of the French Offer period or the subsequent offering period, if any, the implementation of a squeeze-out for the remaining OCEANEs for cash consideration.

xv

In accordance with French law and the AMF General Regulation, in such a squeeze-out, Nokia intends, prior to the

implementation of the squeeze-out for cash consideration, to propose to the holders of Alcatel Lucent Securities as an alternative to cash consideration, an option to exchange their Alcatel Lucent Securities for Nokia Shares and/or Nokia ADSs, as

applicable, at the same exchange ratios offered in the context of the Exchange Offer (the “Exchange Option”). The holders of Alcatel Lucent Securities may opt for the Exchange Option for all or part of their Alcatel Lucent Securities

within a time period to be determined at a later date. The Alcatel Lucent Securities not tendered into the Exchange option will be subject to the squeeze-out for cash consideration.

If Nokia owns less than 95% of the share capital and voting rights of Alcatel Lucent immediately after the Completion of the subsequent offering period, then Nokia reserves the right, subject to applicable law, to

(i) commence a buy-out offer for the Alcatel Lucent Securities it does not own on the relevant date pursuant to the AMF General Regulation if at any time thereafter it owns 95% or more of the voting rights of Alcatel Lucent; (ii) commence

at any time a simplified offer for the Alcatel Lucent Securities it does not own on the relevant date pursuant to Article 233-1 et seq. of the AMF General Regulation; (iii) purchase Alcatel Lucent Securities on the market; (iv) cause Alcatel

Lucent to be merged into Nokia or an affiliate thereof, contribute assets to, merge certain of its subsidiaries with, or undertake other reorganizations of, Alcatel Lucent; or (v) take any other steps to consolidate its ownership of Alcatel

Lucent. We do not currently intend to structure any of the foregoing steps so that it would result in the OCEANEs becoming convertible bonds of Nokia Corporation, becoming debt obligations of Nokia Corporation or otherwise convertible into Nokia

Shares or Nokia ADSs.

In addition, Nokia reserves the right, subject to applicable law, at any time after the Completion of the Exchange Offer or the

subsequent offering period, as applicable, to cause Alcatel Lucent to redeem at par value, plus, as applicable, accrued interest from the date the interest was last paid, to the date set for the early redemption all of the outstanding 2018 OCEANEs,

2019 OCEANEs or 2020 OCEANEs, if less than 15% of the issued OCEANEs of any such series remain outstanding.

Why is there a separate French Offer?

As Alcatel Lucent is a French société anonyme with a listing on Euronext Paris, a French Offer is required pursuant to French

laws and regulations and is being conducted in accordance with French law and the AMF General Regulation.

What are the differences between the U.S.

Offer and the French Offer?

The financial conditions of the U.S. Offer and the French Offer are the same. As a result of differences in law and

market practice between the United States and France, however, the procedures for accepting the Exchange Offer and tendering Alcatel Lucent Securities, and some of the rights of tendering holders of Alcatel Lucent Securities, under the U.S. Offer

and the French Offer, are not identical. The primary difference between the U.S. Offer and the French Offer is that the U.S. Offer is available to U.S. holders of Alcatel Lucent Shares and OCEANEs and to holders of Alcatel Lucent ADSs, wherever

located, while the French Offer is available to holders of Alcatel Lucent Shares and OCEANEs located in France (holders of Alcatel Lucent Shares and OCEANEs located outside of France may not participate in the French Offer except if, pursuant to the

local laws and regulations applicable to those holders, they are permitted to participate in the French Offer). Holders of Alcatel Lucent ADSs located outside of the United States may participate in the U.S. Offer only to the extent the local laws

and regulations applicable to those holders permit them to participate in the U.S. Offer. Holders of Alcatel Lucent Securities who are restricted from participating in the U.S. Offer pursuant to the Sanctions may not participate in the U.S. Offer.

xvi

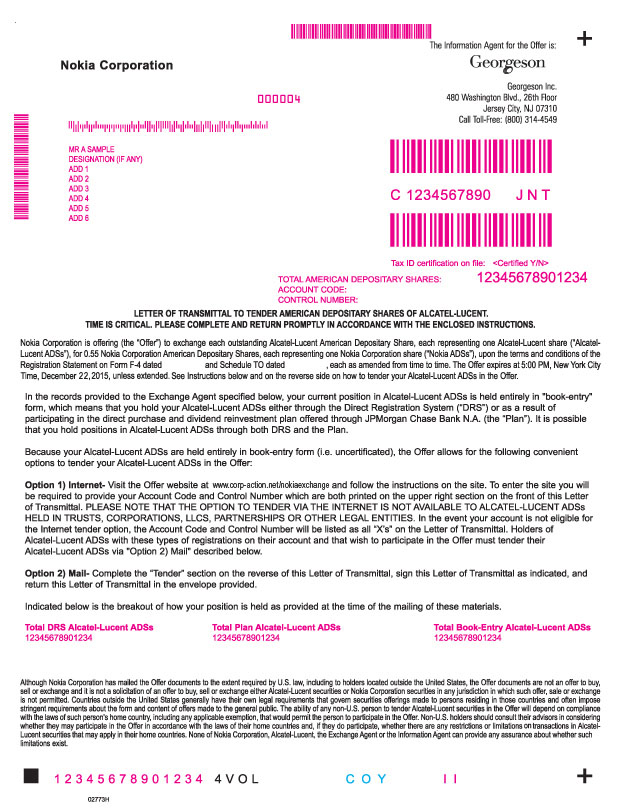

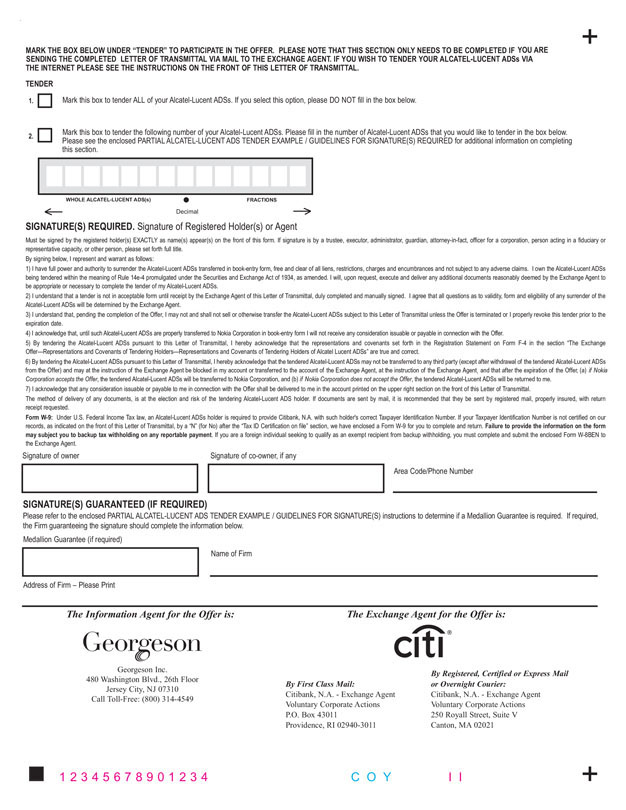

How do I validly tender my Alcatel Lucent ADSs into the U.S. Offer?

The steps you must take to validly tender your Alcatel Lucent ADSs will depend on whether you hold your Alcatel Lucent ADSs directly or indirectly through a broker,

dealer, commercial bank, trust company or other nominee.

| |

• |

|

If you hold Alcatel Lucent ADSs directly and would like to tender them into the Exchange Offer, you must tender them to the U.S. exchange agent prior to the ADS

Tender Deadline, which is 5:00 P.M., New York time, on the U.S. business day immediately preceding the Expiration Date, which is December 22, 2015, unless the U.S. Offer is extended. In order to validly tender your directly-held Alcatel Lucent ADSs,

you must take the following actions: |

| |

• |

|

if you hold your Alcatel Lucent ADSs in certificated form, you must complete and sign the letter of transmittal included with this exchange offer/prospectus and

return it together with your Alcatel Lucent ADS certificates and any required documentation to the U.S. exchange agent at the appropriate address specified on the back cover page of this exchange offer/prospectus; |

| |

• |

|

if you hold your Alcatel Lucent ADSs in uncertificated form on the register of the Alcatel Lucent depositary (in direct registration form), you must complete and

sign the letter of transmittal included with this exchange offer/prospectus and return it with any required documentation to the U.S. exchange agent at the appropriate address specified on the back cover page of this exchange offer/prospectus; and

|

| |

• |

|

if you hold your Alcatel Lucent ADSs in book-entry form indirectly through DTC, you must tender your Alcatel Lucent ADSs to the U.S. exchange agent by using the

ATOP system. |

| |

• |

|

If you hold your Alcatel Lucent ADSs indirectly through a broker, dealer, commercial bank, trust company or other nominee, you should not complete and sign the

letter of transmittal included with this exchange offer/prospectus. Instead, you should instruct your broker, dealer, commercial bank, trust company or other nominee to validly tender your Alcatel Lucent ADSs to the U.S. exchange agent on your

behalf. |

The U.S. exchange agent has established an additional means for registered holders of uncertificated Alcatel Lucent ADSs to

complete and deliver letters of transmittal via the internet, by signing onto a secure website established and maintained by the U.S. exchange agent and filling in the applicable information online. Detailed instructions for completing and

delivering the letter of transmittal via the internet (including the applicable password) are set forth in the letter of transmittal being delivered to holders of uncertificated Alcatel Lucent ADSs together with this exchange offer/prospectus.

If your Alcatel Lucent ADSs are not immediately available, you may also follow the guaranteed delivery procedures described in this exchange

offer/prospectus.

How do I validly tender my Alcatel Lucent Shares or OCEANEs into the U.S. Offer?

You do not need to complete a letter of transmittal to tender your Alcatel Lucent Shares or OCEANEs into the U.S. Offer.

If you hold Alcatel Lucent Shares or OCEANEs through a custodian that is not a French financial intermediary, your custodian should either forward to you the

transmittal materials and instructions sent by the French financial intermediary that holds the Alcatel Lucent Shares or OCEANEs on behalf of the custodian as record owner or send you a separate form prepared by the custodian. If you have not yet

received instructions from your custodian, please contact your custodian directly.

If you hold Alcatel Lucent Shares or OCEANEs through a French

financial intermediary, your French financial intermediary should send you transmittal materials and instructions for accepting the U.S. Offer before the last day of the offer. If you have not yet received instructions from your French financial

intermediary, please contact your French financial intermediary directly.

xvii

If your Alcatel Lucent Shares or OCEANEs are held in pure registered form (nominatif pur), you must first

request that your Alcatel Lucent Shares or OCEANEs be converted to administered registered form (nominatif administré) or to bearer form (au porteur).

How much time do I have to decide whether to tender?

You may tender your Alcatel Lucent Shares and OCEANEs

into the U.S. Offer at any time prior to the Expiration Date (which is currently 11:00 A.M., New York City time (5:00 P.M. Paris time), on December 23, 2015, but will change if the U.S. Offer is extended). You may tender your Alcatel Lucent ADSs

into the U.S. Offer at any time prior to the ADS Tender Deadline (which is currently 5:00 P.M., New York City time, on the U.S. business day immediately preceding the Expiration Date, which is currently December 22, 2015, unless the U.S. Offer is

extended).

Can the Exchange Offer be extended?

Yes. Subject to the applicable rules and regulations of the AMF and the SEC, the Expiration Date and the ADS Tender Deadline may be extended.

Only the AMF has the authority to set or to extend the expiration date of the French Offer. If the French Offer is extended, the AMF will issue a notice of extension on its website http://www.amf-france.org.

In addition, Nokia will post a notice of any extension of the French Offer or the U.S. Offer on its website www.nokia.com, and will issue a public announcement. The information on Nokia’s or the AMF’s website is not a part of this

exchange offer/prospectus and is not incorporated by reference herein.

Pursuant to the Memorandum of Understanding, Nokia agreed to ensure that,

subject to applicable law, the period during which the U.S. Offer is open corresponds to the period during which the French Offer is open (including any extensions or subsequent offering periods in relation to the French Offer), and Nokia expressly

reserves the right to extend the U.S. Offer either to match any extension of the French Offer or otherwise. Furthermore, Nokia may be required by the U.S. federal securities laws (including Rule 14e-1 under the Exchange Act) to extend the

duration of the U.S. Offer if Nokia makes a material change to the terms of the U.S. Offer.

Will there be a subsequent offering period?

Pursuant to the Memorandum of Understanding and according to the AMF General Regulation, (i) if at the Completion of the Exchange Offer, Nokia owns

95% or more of the share capital and voting rights of Alcatel Lucent (Alcatel Lucent Shares held in treasury being considered as held by Nokia for the purpose of the calculation), Nokia may open the subsequent offering period within ten French

trading days of the announcement by the AMF of the results of the French Offer (taking into account the results of the U.S. Offer), unless Nokia files the request for a squeeze-out with the AMF within ten French trading days of the announcement by

the AMF; or (ii) if at the Completion of the Exchange Offer Nokia owns more than 50% but less than 95% of Alcatel Lucent share capital and voting rights, Nokia agreed to conduct a subsequent offering period after the date of announcement of the

results of the French Offer by the AMF (taking into account the results of the U.S. Offer) (subject to the satisfaction or waiver of the Minimum Tender Condition and the receipt of the Nokia Shareholder Approval). The subsequent offering period

would be conducted on the same terms as the Exchange Offer, but the Alcatel Lucent Securities properly tendered during the subsequent offering period will not be permitted to be withdrawn and will be accepted without any minimum condition.

Can I withdraw Alcatel Lucent Securities that I have tendered into the U.S. Offer?

Yes. You may withdraw any Alcatel Lucent Shares and OCEANEs tendered into the U.S. Offer at any time prior to the Expiration Date, and you may withdraw any Alcatel Lucent ADSs tendered into the U.S. Offer at any

time prior to the ADS Tender Deadline. In addition, in accordance with U.S. securities

xviii

laws, you may generally withdraw your tendered Alcatel Lucent Securities tendered into the U.S. Offer if they have not been accepted for exchange within 60 days after the beginning of the offer

period. However, these withdrawal rights will not be available following the Expiration Date, in the case of Alcatel Lucent Shares and OCEANEs, or the ADS Tender Deadline, in the case of Alcatel Lucent ADSs, and prior to the commencement of the

subsequent offering period, if any. Also, subject to satisfaction of all Conditions other than the Minimum Tender Condition, these withdrawal rights will not be available during the period that the securities tendered into the Exchange Offer are

being counted. Pursuant to Rule 14d-7(a)(2) under the Exchange Act, no withdrawal rights will apply to Alcatel Lucent Securities tendered during a subsequent offering period, if any.

How do I withdraw Alcatel Lucent Securities previously tendered into the U.S. Offer?

To withdraw previously

tendered Alcatel Lucent ADSs, the U.S. exchange agent must receive a timely written or facsimile transmission notice of withdrawal. Any such notice must specify the name of the person who tendered the Alcatel Lucent ADSs being withdrawn, the number

of Alcatel Lucent ADSs being withdrawn and the name of the registered holder if different from that of the person who tendered such Alcatel Lucent ADSs. To withdraw previously tendered Alcatel Lucent Shares or OCEANEs, you should contact your French

or non-French financial intermediary or nominee through whom you tendered the Alcatel Lucent Shares or OCEANEs regarding their withdrawal procedures to validly withdraw tendered Alcatel Lucent Shares or OCEANEs in the U.S. Offer.

Will I have to pay any fees or commissions for tendering my Alcatel Lucent Securities?

If your Alcatel Lucent Securities are tendered into the U.S. Offer by your broker, dealer, commercial bank, trust company or other nominee, you will be responsible for any fees or commissions they may charge you in

connection with such tender. No commission will be paid by Nokia to any intermediary of Alcatel Lucent Security holders or any person soliciting the contribution of Alcatel Lucent Securities into the Exchange Offer.

You will also be responsible for all governmental charges and taxes payable in connection with tendering your Alcatel Lucent Securities.

Will tendered Alcatel Lucent Securities be subject to proration?

No. Subject to the terms and Conditions, Nokia will acquire any and all Alcatel Lucent Securities validly tendered into, and not withdrawn from, the U.S. Offer.

Can I tender less than all the Alcatel Lucent Securities that I own into the Exchange Offer?

Yes. You may elect to tender all or a portion of the Alcatel Lucent Securities that you own into the U.S. Offer.

If I decide not to tender, how will the Exchange Offer affect my Alcatel Lucent Securities?

The Completion of the Exchange Offer is conditioned, among other things, upon the satisfaction or waiver of the Minimum Tender Condition.

If the Exchange Offer is successful, the acquisition by Nokia of Alcatel Lucent Securities in the Exchange Offer will reduce the number of Alcatel Lucent Securities that might otherwise trade publicly and may

reduce the number of holders of Alcatel Lucent Securities, which could adversely affect the liquidity and market value of the Alcatel Lucent Securities not acquired in the Exchange Offer.

On opening of the first U.S. business day following the ADS Tender Deadline, the NYSE may suspend trading in the Alcatel Lucent ADSs pending public announcement of the results of the Exchange Offer.

xix

Because the AMF may not announce the results of the French Offer (taking into account the results of the U.S. Offer) until up to nine French trading days after the Expiration Date (although we

expect the announcement to be made approximately seven French trading days after the Expiration Date), holders of Alcatel Lucent ADSs who do not tender their Alcatel Lucent ADSs in the U.S. Offer may be unable to trade Alcatel Lucent ADSs on the

NYSE during this period. Further, if fewer than 600 000 Alcatel Lucent ADSs would remain outstanding following Completion of the Exchange Offer, the NYSE may not resume trading in the Alcatel Lucent ADSs even after the publication of the

results of the Exchange Offer. Holders of Alcatel Lucent ADSs who do not tender their Alcatel Lucent ADSs in the Exchange Offer may therefore be unable to trade their Alcatel Lucent ADSs on the NYSE at any point following the Expiration Date.

As promptly as practicable following Completion of the Exchange Offer and subject to applicable law and Euronext Paris rules, Nokia intends to

request Euronext Paris to delist the Alcatel Lucent Shares and OCEANEs from the regulated market of Euronext Paris. Nokia also intends to seek to delist the Alcatel Lucent ADSs from the NYSE and, subject to applicable law, to deregister the Alcatel

Lucent Shares and Alcatel Lucent ADSs and terminate the reporting obligations of Alcatel Lucent under the Exchange Act.

Will I have appraisal rights

in connection with the Exchange Offer?

No. There are no appraisal or similar rights available to holders of Alcatel Lucent Securities in connection

with the Exchange Offer.

What are the tax consequences if I participate or do not participate in the Exchange Offer?

For information on certain French, Finnish, and U.S. tax consequences of the Exchange Offer, see the “Tax Considerations” section of this exchange

offer/prospectus. You should consult your own tax advisor on the tax consequences to you of tendering your Alcatel Lucent Securities in the Exchange Offer.

How and where will the outcome of the Exchange Offer be announced?

The AMF is expected to announce the

results of the French Offer taking into account the results of the U.S. Offer approximately seven and in any event no later than nine French trading days following the Expiration Date and, if applicable, the ending of the subsequent offering period.

In addition, Nokia will post a notice of the results of the Exchange Offer on www.nokia.com, and will issue a public announcement. The information on Nokia’s website is not a part of this exchange offer/prospectus and is not incorporated

by reference herein.

When will I receive my Nokia Shares or Nokia ADSs?

You will receive the Nokia Shares or Nokia ADSs you are entitled to receive pursuant to the U.S. Offer approximately five French trading days following the announcement of the results of the French Offer (taking

into account the results of the U.S. Offer) by the AMF and, if applicable, of the subsequent offering period. If the Exchange Offer expires and the Conditions are not satisfied or terminated in accordance with applicable law, the U.S. exchange agent

will return tendered Alcatel Lucent ADSs to you within one U.S. business day after the expiration or termination of the U.S. Offer, and the tendered Alcatel Lucent Shares or OCEANEs will be returned to you within three U.S. business days after the

expiration or termination of the U.S. Offer.

Who can I call with questions?

If you have more questions about the Exchange Offer, you should contact Nokia’s information agent, Georgeson Inc., toll-free at (800) 314-4549.

xx

PRESENTATION OF INFORMATION

Currency and Exchange Rates

In this exchange offer/prospectus, all references to “U.S. dollar,”

“USD” and “$” are to the lawful currency of the United States. All references to “euro,” “EUR” and

“€” are to the official currency of the member states of the European Union (the “EU”) that adopted the single

currency in accordance with the Treaty Establishing the European Economic Community (signed in Rome on March 25, 1957), as amended by the Treaty of European Union signed in Maastricht on February 7, 1992.

The following tables set forth, for the periods indicated, information concerning the exchange rates between the euro and the U.S. dollar based on the noon buying

rate for cable transfers as certified by the Federal Reserve Board of New York. Such rates are provided solely for your convenience and are not necessarily the rates used by Alcatel Lucent or Nokia in the preparation of their financial statements or

otherwise.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Average ($) |

|

|

High ($) |

|

|

Low ($) |

|

|

Period End ($) |

|

| Year ended December 31, 2010 |

|

|

1.3216 |

|

|

|

1.4536 |

|

|

|

1.1959 |

|

|

|

1.3269 |

|

| Year ended December 31, 2011 |

|

|

1.4002 |

|

|

|

1.4875 |

|

|

|

1.2926 |

|

|

|

1.2973 |

|

| Year ended December 31, 2012 |

|

|

1.2909 |

|

|

|

1.3463 |

|

|

|

1.2062 |

|

|

|

1.3186 |

|

| Year ended December 31, 2013 |

|

|

1.3303 |

|

|

|

1.3816 |

|

|

|

1.2774 |

|

|

|

1.3779 |

|

| Year ended December 31, 2014 |

|

|

1.3210 |

|

|

|

1.3927 |

|

|

|

1.2101 |

|

|

|

1.2101 |

|

| Six months ended June 30, 2015 |

|

|

1.1090 |

|

|

|

1.2015 |

|

|

|

1.0524 |

|

|

|

1.1154 |

|

|

|

|

|

|

|

|

|

|

| |

|

High ($) |

|

|

Low ($) |

|

| May 2015 |

|

|

1.1428 |

|

|

|

1.0876 |

|

| June 2015 |

|

|

1.1404 |

|

|

|

1.0913 |

|

| July 2015 |

|

|

1.1150 |

|

|

|

1.0848 |

|

| August 2015 |

|

|

1.1580 |

|

|

|

1.0868 |

|

| September 2015 |

|

|

1.1358 |

|

|

|

1.1104 |

|

| October 2015 |

|

|

1.1437 |

|

|

|

1.0963 |

|

| November 2015 (through November 6, 2015) |

|

|

1.1026 |

|

|

|

1.0746 |

|

Solely for convenience, this exchange offer/prospectus contains translations of certain euro balances into U.S. dollars at

specified rates. These are simply translations, and you should not expect that a euro amount actually represents a stated U.S. dollar amount or that it could be converted into U.S. dollars at specified rates or at all.

Other Information

Within this exchange offer/prospectus,

references to the Exchange Offer, the U.S. Offer or the French Offer refer to such offer without any subsequent offering period, unless stated otherwise.

xxi

SUMMARY

This summary highlights selected information from this exchange offer/prospectus. It does not contain all the information that is important to you. Before you decide whether or not to tender your Alcatel Lucent

Securities, you should read carefully this entire exchange offer/prospectus as well as the documents that are incorporated by reference into or filed as exhibits to the registration statement of which this exchange offer/prospectus forms a

part. See the “Where You Can Find More Information” section of this exchange offer/prospectus.

The Companies

Nokia (page 182)

Nokia

is a Finnish Corporation, established in 1865 and organized under the laws of the Republic of Finland. The company is registered with the Finnish Trade Register under the business identity code 0112038-9. Under its articles of association in

effect on the date of this exchange offer/prospectus, Nokia’s corporate purpose is to engage in the telecommunications industry and other sectors of the electronics industry as well as the related service businesses, including the development,

manufacture, marketing and sales of mobile devices, other electronic products and telecommunications systems and equipment as well as related mobile, Internet and network infrastructure services and other consumer and enterprise services. Nokia may

also create, acquire and license intellectual property and software as well as engage in other industrial and commercial operations. Further, Nokia may engage in securities trading and other investment activities.

Nokia is currently focused on three businesses: network infrastructure software, hardware and services, which is offered through Nokia Networks; mapping and

location intelligence, which is provided through HERE; and advanced technology development and licensing, which is pursued through Nokia Technologies. Through its three businesses, Nokia has a global presence, with operations and research

and development (“R&D”) facilities in Europe, North America and Asia, sales in approximately 140 countries, and employs approximately 62 000 people. Nokia is also a major investor in R&D, with expenditure through its

three businesses exceeding EUR 2.5 billion in 2014.

On August 3, 2015, Nokia announced an agreement to sell its HERE digital mapping and location

services business to a consortium of leading automotive companies, comprising AUDI AG, BMW Group and Daimler AG. The transaction values HERE at an enterprise value of EUR 2.8 billion with a normalized level of working capital and is expected to

close in the first quarter of 2016, subject to customary closing conditions and regulatory approvals. Upon closing, Nokia estimates that it will receive net proceeds of slightly above EUR 2.5 billion, as the purchaser would be compensated for

certain defined liabilities of HERE currently expected to be slightly below EUR 300 million as part of the transaction. Upon closing of the HERE transaction, which does not affect the exchange ratio of this Exchange Offer, and assuming that the

Exchange Offer has not yet been completed, Nokia will consist of two businesses: Nokia Networks and Nokia Technologies.

It is currently expected that

after the Completion of the Exchange Offer, Networks business would be conducted through four business groups: Mobile Networks, Fixed Networks, Applications & Analytics and IP/Optical Networks. The business group leaders would report directly to

Nokia’s President and Chief Executive Officer:

| |

• |

|

Mobile Networks (MN) would include Nokia’s and

Alcatel Lucent’s comprehensive Radio portfolios and most of their converged Core network portfolios including IMS/VoLTE and Subscriber Data Management, as well as the associated mobile networks-related Global Services business. This unit would

also include Alcatel Lucent’s Microwave business and all of the combined company’s end-to-end Managed Services business. |

1

| |

• |

|

Fixed Networks (FN) would comprise the current Alcatel

Lucent Fixed Networks business, whose cutting-edge innovation and market position would be further supported through strong collaboration with the other business groups. |

| |

• |

|

Applications & Analytics (A&A) would combine the

Software and Data Analytics-related operations of both companies. This comprehensive applications portfolio would include Customer Experience Management, OSS as distinct from network management such as service fulfilment and assurance, Policy and

Charging, services, Cloud Stacks, management and orchestration, communication and collaboration, Security Solutions, network intelligence and analytics, device management and Internet of Things connectivity management platforms. CloudBand would also

be housed in this business group, which would drive innovation to meet the needs of a convergent, Cloud-centric future. |

| |

• |

|

IP/Optical Networks (ION) would combine the current

Alcatel Lucent IP Routing, Optical Transport and IP video businesses, as well as the software defined networking (SDN) start-up, Nuage, plus Nokia’s IP partner and Packet Core portfolio. |

Along side these four business groups of Networks, Nokia Technologies would continue to operate as a separate business group with a clear focus on licensing and

the incubation of new technologies.

Nokia’s registered office and its principal executive office is Karaportti 3, FI-02610 Espoo, Finland, and the

telephone number is +358 (0) 10-448-8000.

Nokia Shares are traded on the Nasdaq Helsinki under the symbol “NOKIA” and Nokia ADSs are

traded on the NYSE under the symbol “NOK.” In addition, application has been made for Admission of the Nokia Shares to Euronext Paris. Nokia expects to request that the Admission be approved to take effect prior to the Completion of the

Exchange Offer. As of June 30, 2015, 3 678 328 858 Nokia Shares were outstanding (including 54 326 556 Nokia Shares owned by Nokia group companies and 477 477 741 Nokia Shares represented by Nokia ADSs).

In October 2012, Nokia issued the Convertible Bond. If the Convertible Bond is converted into Nokia Shares in its entirety, which would occur by

November 17, 2015 because of Nokia’s prior announcement that it will exercise its option to redeem the Convertible Bonds on November 26, 2015, at the current conversion price of EUR 2.39 per Nokia Share, approximately 313 723 849

Nokia Shares (assuming full conversion) would be issued, representing approximately 5.2% of the issued and outstanding Nokia Shares after Completion of the Exchange Offer (assuming that all Alcatel Lucent Securities are tendered into the Exchange

Offer or the subsequent offering period, if any).

Alcatel Lucent (page 189)

Alcatel Lucent is a French société anonyme, established in 1898, originally as a listed company named Compagnie Générale

d’Électricité. Alcatel Lucent is registered at the Nanterre Trade and Companies Registry under number 542019096. Its APE business activity code is 7010Z. Alcatel Lucent’s corporate purpose is the design, manufacture,

operation and sale of all equipment, material and software related to domestic, industrial, civil, military or other applications concerning electricity, telecommunications, computers, electronics, aerospace industry, nuclear energy, metallurgy,

and, in general, of all the means of production or transmission of energy or communications (cables, batteries and other components), as well as, secondarily, all activities relating to operations and services in connection with the above-mentioned

means worldwide. It may acquire interests in any company, regardless of its form, in associations, French or foreign business groups, whatever their corporate purpose and activity may be and, in general, may carry out any industrial, commercial,

financial, assets or real estate transactions, in connection, directly or indirectly, totally or partially, with any of the corporate purposes set out in Article 2 of its articles of association and with all similar or related purposes.

2

Alcatel Lucent currently has two operating segments: Core Networking and Access. Until March 2014, Alcatel Lucent

had a third operating segment: Other. The Core Networking segment includes three business divisions: IP Routing, IP Transport and IP Platforms. In 2014, revenues in the Core Networking segment were EUR 5.97 billion, representing 45% of Alcatel

Lucent’s total revenues. The Access segment includes four business divisions: Wireless, Fixed Access, Licensing and Managed Services. In 2014, revenues in the Access segment were EUR 7.16 billion, representing 54% of Alcatel Lucent’s total

revenues. Until 2014, the Other segment included the government business, which built and delivered complete turnkey solutions in support of U.S. federal government agencies in the U.S. On March 31, 2014, Alcatel Lucent completed the disposal

of LGS Innovations LLC. In 2014 revenues in Alcatel Lucent’s Other segment were EUR 41 million, representing less than 1% of Alcatel Lucent’s total revenues.

On October 6, 2015, Alcatel Lucent announced that it is to continue to operate its undersea cables business, Alcatel Lucent Submarine Networks (“ASN”), as a wholly owned subsidiary. Alcatel Lucent

announced that ASN will continue to execute its strategic roadmap, strengthen its leadership in submarine cable systems for telecom applications and pursue further diversification into the Oil & Gas sector.

Alcatel Lucent’s principal office is located at 148/152 Route de la Reine 92100 Boulogne-Billancourt, France, and the telephone number is +33 (0)1 55 14 10

10.

The Alcatel Lucent Shares are traded on Euronext Paris under the symbol “ALU” and Alcatel Lucent ADSs are traded on the NYSE under