UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

Current Report Pursuant

to Section 13 OR 15(d) of The

Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

February 23, 2016

| LEXINGTON REALTY TRUST |

| (Exact name of registrant as specified in its charter) |

| |

|

|

| Maryland |

1-12386 |

13-3717318 |

|

(State or other jurisdiction

of incorporation) |

(Commission File Number) |

(IRS Employer

Identification No.) |

| One Penn Plaza, Suite 4015, New York, New York |

10119-4015 |

| (Address of principal executive offices) |

(Zip Code) |

(212) 692-7200

(Registrant's telephone number, including

area code)

(Former name

or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended

to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction

A.2.):

| ¨ | Written communications pursuant to Rule 425 under the

Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the

Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 2.02. | Results of Operations and Financial Condition. |

On February 23, 2016, we issued a press

release announcing our financial results for the quarter ended December 31, 2015. A copy of the press release is furnished herewith

as part of Exhibit 99.1.

The information furnished pursuant to this

“Item 2.02 - Results of Operations and Financial Condition”, including Exhibit 99.1, shall not be deemed to be “filed”

for the purposes of Section 18 of the Securities Exchange Act of 1934, as amended, which we refer to as the Exchange Act, or otherwise

subject to the liabilities of that section, and shall not be deemed to be incorporated by reference into any filing made by us

under the Exchange Act or Securities Act of 1933, as amended, which we refer to as the Securities Act, regardless of any general

incorporation language in any such filing, except as shall be expressly set forth by specific reference in such a filing.

| Item 7.01. | Regulation FD Disclosure. |

On February 23, 2016, we made available

supplemental information, which we refer to as the Quarterly Earnings and Supplemental Operating and Financial Data, December 31,

2015, a copy of which is furnished herewith as Exhibit 99.1.

Also on February 23, 2016, our management

discussed our financial results and certain aspects of our business plan on a conference call with analysts and investors. A transcript

of the conference call is furnished herewith as Exhibit 99.2.

On February 24, 2016, we made available

a presentation entitled “Lexington Realty Trust, Investor Presentation, February 2016” on the “Investor Relations”

section of our web site (www.LXP.com). A copy of the presentation is furnished as Exhibit 99.3

to this Current Report and is incorporated herein by reference solely for purposes of this Item 7.01 disclosure.

The information furnished pursuant to this

“Item 7.01 - Regulation FD Disclosure”, including Exhibit 99.1, Exhibit 99.2 and Exhibit 99.3, shall not be deemed

to be “filed” for the purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that section,

and shall not be deemed to be incorporated by reference into any filing made by us under the Exchange Act or the Securities Act,

regardless of any general incorporation language in any such filing, except as shall be expressly set forth by specific reference

in such a filing. Information contained on our web site is not incorporated by reference into this Current Report on Form 8-K.

| Item 9.01. | Financial Statements and Exhibits. |

| 99.1 |

Quarterly Earnings and Supplemental Operating and Financial Data, December 31, 2015. |

| 99.2 |

February 23, 2016 Conference Call Transcript. |

| 99.3 |

Lexington Realty Trust, Investor Presentation, February 2016 |

SIGNATURES

Pursuant to the requirements of the Securities

Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| |

Lexington Realty Trust |

|

| |

|

|

|

| |

|

|

|

| Date: February 24, 2016 |

By: |

/s/ Patrick Carroll |

|

| |

|

Patrick Carroll |

|

| |

|

Chief Financial Officer |

|

Exhibit Index

| 99.1 |

Quarterly Earnings and Supplemental Operating and Financial Data, December 31, 2015. |

| 99.2 |

February 23, 2016 Conference Call Transcript. |

| 99.3 |

Lexington Realty Trust, Investor Presentation, February 2016 |

Exhibit 99.1

Quarterly

Earnings and

Supplemental

Operating and Financial Data

December

31, 2015

LEXINGTON

REALTY TRUST

SUPPLEMENTAL

REPORTING PACKAGE

December 31,

2015

Table of

Contents

| Section |

|

Page |

| |

|

|

| Fourth Quarter 2015 Earnings Press Release |

|

3 |

| |

|

|

| Portfolio Data |

|

|

| 2015 Fourth Quarter Investment/Capital Recycling Summary |

|

13 |

| Build-To-Suit Projects/Forward Commitments |

|

14 |

| 2015 Fourth Quarter Financing Summary |

|

15 |

| 2015 Fourth Quarter Leasing Summary |

|

16 |

| Other Revenue Data |

|

17 |

| Portfolio Detail By Asset Class |

|

19 |

| Portfolio Composition |

|

20 |

| Components of Net Asset Value |

|

21 |

| Top Markets |

|

22 |

| Single-Tenant Office Markets |

|

23 |

| Tenant Industry Diversification |

|

24 |

| Top 10 Tenants or Guarantors |

|

25 |

| Lease Rollover Schedules – GAAP Basis |

|

26 |

| Property Leases and Vacancies – Consolidated Portfolio |

|

28 |

| Select Credit Metrics Summary |

|

36 |

| Financial Covenants |

|

37 |

| Mortgages and Notes Payable |

|

38 |

| Debt Maturity Schedule |

|

41 |

| Mortgage Loans Receivable |

|

42 |

| Partnership Interests |

|

43 |

| Selected Balance Sheet and Income Statement Account Data |

|

44 |

| Investor Information |

|

45 |

This Quarterly

Earnings Release and Supplemental Reporting Package contains certain forward-looking statements which involve known and unknown

risks, uncertainties or other factors not under the control of Lexington Realty Trust “Lexington”, which may cause

actual results, performance or achievements of Lexington to be materially different from the results, performance, or other expectations

implied by these forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited

to, those discussed under the headings “Management’s Discussion and Analysis of Financial Condition and Results of

Operations” and “Risk Factors” in Lexington’s periodic reports filed with the Securities and Exchange

Commission, including risks related to: (1) the authorization of Lexington’s Board of Trustees of future dividend declarations,

(2) Lexington’s ability to achieve its estimate of Company FFO for the year ending December 31, 2016, (3) the successful

consummation of any lease, acquisition, build-to-suit, disposition, financing or other transaction, (4) the failure to continue

to qualify as a real estate investment trust, (5) changes in general business and economic conditions, including the impact of

any new legislation, (6) competition, (7) increases in real estate construction costs, (8) changes in interest rates, (9) changes

in accessibility of debt and equity capital markets, and (10) future impairment charges. Copies of the periodic reports Lexington

files with the Securities and Exchange Commission are available on Lexington’s web site at www.lxp.com. Forward-looking

statements, which are based on certain assumptions and describe Lexington’s future plans, strategies and expectations, are

generally identifiable by use of the words “believes,” “expects,” “intends,” “anticipates,”

“estimates,” “projects,” may,” “plans,” “predicts,” “will,”

“will likely result,” “is optimistic,” “goal,” “objective” or similar expressions.

Except as required by law, Lexington undertakes no obligation to publicly release the results of any revisions to those forward-looking

statements which may be made to reflect events or circumstances after the occurrence of unanticipated events. Accordingly, there

is no assurance that Lexington’s expectations will be realized.

| |

LEXINGTON

REALTY

TRUST |

| |

TRADED: NYSE: LXP |

| |

ONE

PENN PLAZA, SUITE

4015 |

| |

NEW

YORK, NY 10119-4015 |

FOR

IMMEDIATE RELEASE

LEXINGTON

REALTY TRUST REPORTS FOURTH QUARTER 2015 RESULTS

New York,

NY - Tuesday, February 23, 2016 - Lexington Realty Trust (“Lexington”) (NYSE:LXP), a real estate investment trust

focused on single-tenant real estate investments, today announced results for the fourth quarter ended December 31, 2015.

Fourth Quarter 2015 Highlights

| • | Generated

Company Funds From Operations (“Company FFO”) of $69.6 million, or $0.29

per diluted common share. |

| • | Acquired/completed two build-to-suit

properties for an aggregate initial basis of $253.5 million. |

| • | Invested

$45.4 million in on-going build-to-suit projects and commenced funding an office build-to-suit

project for $62.4 million. |

| • | Completed

0.9 million square feet of new leases and lease extensions with overall portfolio 96.8%

leased at quarter end. |

| • | Obtained

$110.0 million 10-year non-recourse financing, which bears interest at a 4.0% fixed interest

rate and is secured by the Richland, Washington property. |

| • | Repurchased 0.9 million

common shares at an average price of $8.12 per share. |

Full Year 2015 Highlights

| • | Generated Company FFO of

$268.0 million, or $1.10 per diluted common share. |

| • | Acquired/completed nine

properties for an aggregate initial basis of $483.0 million. |

| • | Disposed of nine properties

for gross proceeds of $265.2 million. |

| • | Completed 4.0 million square

feet of new leases and lease extensions. |

| • | Refinanced

$616 million of debt, extended weighted-average maturity to 7.2 years and lowered average

borrowing cost by 50 bps to 4.01%. |

| • | Repurchased over 2.2 million

common shares at an average price of $8.29 per share. |

Subsequent Events

| • | Acquired one industrial

property for $29.7 million. |

| • | Renewed 0.7 million square

feet of leases. |

| • | Closed

on $57.5 million, 15-year, 5.2% fixed rate mortgage on newly-constructed Gateway Plaza

property in Richmond, Virginia. |

| • | Repurchased approximately

1.0 million common shares at an average price of $7.48 per share. |

T.

Wilson Eglin, President and Chief Executive Officer of Lexington, stated “We finished off 2015 on a strong note with good

execution in all aspects of our business. During the quarter we closed on two substantial build-to-suit transactions for

$253 million and subsequently obtained favorable financing on both, bringing our total acquisitions for the year to $483 million

at an average cap rate of 7.4%. At year end, our overall portfolio was 96.8% leased as leasing volume remained strong at nearly

one million square feet during the fourth quarter of 2015. We continue to believe our own shares represent an uncommon value and

continued to execute on our share repurchase plan in the fourth quarter and into 2016.”

Mr.

Eglin added, “In 2015, we executed a highly successful capital recycling program and disposed of $265 million of properties

at an average cap rate of 6.3%. We expect our disposition volume in 2016 will be even more robust as we look to monetize our New

York City land investments and certain other properties. The proceeds will be used primarily to fund new build-to-suit projects,

retire short-term debt, and repurchase common shares. We have made good progress on leasing as we begin 2016, extending 700,000

square feet of leases to date. Elevated leasing velocity and investment volume have produced high levels of occupancy, balanced

lease expirations and a longer weighted-average lease term with more secure cash flow. As a result, we expect underlying cash

flows to remain strong in 2016. ”

FINANCIAL RESULTS

Revenues

For the quarter

ended December 31, 2015, total gross revenues were $106.6 million, a 1.1% decrease compared with total gross revenues of $107.8

million for the quarter ended December 31, 2014. The decrease is primarily due to 2015 property sales and lease expirations, partially

offset by revenue generated from property acquisitions and new leases signed.

Company FFO

For the quarter

ended December 31, 2015, Lexington generated Company FFO of $69.6 million, or $0.29 per diluted share, compared to Company FFO

for the quarter ended December 31, 2014 of $66.3 million, or $0.27 per diluted share. The calculation of Company FFO and a reconciliation

to net income attributable to common shareholders is included later in this press release.

Dividends/Distributions

Lexington declared

a regular quarterly common share/unit dividend/distribution for the quarter ended December 31, 2015 of $0.17 per common share/unit,

which was paid on January 15, 2016 to common shareholders/unitholders of record as of December 31, 2015. Lexington also declared

a dividend of $0.8125 per share on its Series C Cumulative Convertible Preferred Stock (“Series C Preferred Shares”),

which is payable on May 16, 2016 to Series C Preferred Shareholders of record as of April 29, 2016.

Net Income Attributable to Common

Shareholders

For the quarter

ended December 31, 2015, net income attributable to common shareholders was $33.2 million, or $0.14 per diluted share, compared

with net income attributable to common shareholders for the quarter ended December 31, 2014 of $35.7 million, or $0.15 per diluted

share.

OPERATING ACTIVITIES

During the

quarter ended December 31, 2015, Lexington completed the following build-to-suit projects:

COMPLETED BUILD-TO-SUIT PROJECTS

| Primary Tenant | |

Location | |

Property Type | |

Initial

Basis

($000) | | |

Initial

Annualized Cash

Rent ($000) | | |

Initial Cash Yield | | |

Estimated GAAP Yield | | |

Lease Term

(Yrs) |

| | |

| |

| |

| | |

| | |

| | |

| | |

|

| Preferred Freezer Services of Richland

LLC(1) | |

Richland, WA | |

Industrial | |

$ | 152,000 | | |

$ | 10,792 | | |

| 7.1 | % | |

| 8.6 | % | |

20 |

| McGuireWoods LLP(2) | |

Richmond,

VA | |

Office | |

| 101,489 | | |

| 8,701 | | |

| 8.2 | % | |

| 9.0 | % | |

15 |

| | |

| |

| |

$ | 253,489 | | |

$ | 19,493 | | |

| 7.6 | % | |

| 8.8 | % | |

|

| 1. | ConAgra

Foods, Inc. provides credit support. Guarantors are Preferred Freezer Services LLC and

Preferred Freezer Services Operating LLC. |

| 2. | Property

is 100% leased. McGuireWoods LLP is primary tenant with 68% of the space. Initial basis

does not include $8.1 million for estimated earnout lease payments for developer leased

space. Initial yields include $4.0 million of earnout lease payments earned but not yet

paid as of December 31, 2015. |

Lexington funded

$45.4 million of the projected costs of the following projects:

ON-GOING BUILD-TO-SUIT PROJECTS

| Location | |

Sq.

Ft. | | |

Property

Type | |

Lease Term (Years) | | |

Maximum

Commitment/

Estimated

Completion

Cost

($000) | | |

GAAP

Investment

Balance as

of

12/31/2015

($000) | | |

Estimated Acquisition/ Completion Date | |

Estimated Initial Cash Yield | | |

Estimated GAAP Yield | |

| Anderson, SC | |

| 1,325,000 | | |

Industrial | |

| 20 | | |

$ | 70,012 | | |

$ | 23,826 | | |

2Q 16 | |

| 5.9 | % | |

| 7.3 | % |

| Lake Jackson, TX | |

| 664,000 | | |

Office | |

| 20 | | |

| 166,164 | | |

| 62,353 | | |

4Q 16 | |

| 7.3 | % | |

| 8.9 | % |

| Charlotte, NC | |

| 201,000 | | |

Office | |

| 15 | | |

| 62,445 | | |

| 9,223 | | |

1Q 17 | |

| 8.3 | % | |

| 9.5 | % |

| Houston, TX(1) | |

| 274,000 | | |

Retail/Specialty | |

| 20 | | |

| 86,491 | | |

| 38,367 | | |

3Q 16 | |

| 7.5 | % | |

| 7.5 | % |

| | |

| 2,464,000 | | |

| |

| | | |

$ | 385,112 | | |

$ | 133,769 | | |

| |

| | | |

| | |

| 1. | Lexington

has a 25% interest as of December 31, 2015. Lexington is providing construction financing

up to $56.7 million to the joint venture of which $8.5 million has been funded as of

December 31, 2015. Lease contains annual CPI increases. |

In addition,

Lexington was committed to acquire, and subsequently acquired in January 2016, the following property:

FORWARD COMMITMENT

| Location | |

Property Type | |

Estimated Acquisition

Cost ($000) | | |

Acquisition

Date | |

Estimated Initial Cash

Yield | | |

Estimated GAAP Yield | | |

Lease Term (Years) |

| Detroit, MI | |

Industrial | |

$ | 29,680 | | |

1Q 16 | |

| 7.4 | % | |

| 7.4 | % | |

20 |

PROPERTY DISPOSITIONS

| Tenant | |

Location | |

Property Type | |

Gross

Disposition Price ($000) | | |

Annualized NOI ($000) | | |

Month

of Disposition |

| Vacant(1) | |

Rochester,

NY | |

Office | |

$ | 17,234 | | |

$ | — | | |

December |

| 1. | Conveyed

in foreclosure. |

LEASING

As of December

31, 2015, Lexington's portfolio was 96.8% leased, excluding a property subject to a mortgage in default.

During the

fourth quarter of 2015, Lexington executed the following new and extended leases:

| | |

LEASE EXTENSIONS | |

| |

| |

| | |

| |

| |

| |

| |

| |

| |

| | |

Location | |

Primary

Tenant(1) | |

Prior Term | |

Lease Expiration

Date | |

Sq.

Ft. | |

| | |

Office/Multi-Tenant | |

| |

| |

| |

| |

| | |

| 1-3 | |

Various | |

HI | |

N/A | |

2015 | |

2016-2018 | |

| 886 | |

| 3 | |

Total office

lease extensions | |

| |

| |

| |

| |

| 886 | |

| | |

| |

| |

| |

| |

| |

| | |

| | |

Industrial | |

| |

| |

| |

| |

| | |

| 1 | |

Rockford | |

IL | |

Jacobson Warehouse Company, Inc. | |

12/2015 | |

12/2018 | |

| 150,000 | |

| 2 | |

Olive Branch | |

MS | |

MAHLE Aftermarket Inc. | |

02/2016 | |

02/2023 | |

| 268,104 | |

| 2 | |

Total industrial

lease extensions | |

| |

| |

| |

| |

| 418,104 | |

| | |

| |

| |

| |

| |

| |

| | |

| 5 | |

Total lease

extensions | |

| |

| |

| |

| |

| 418,990 | |

| | |

NEW LEASES | |

| |

| |

| |

| |

| | |

| |

| |

| |

| |

| |

| | |

Location | |

| |

Lease

Expiration Date | |

Sq.

Ft. | |

| | |

Office/Multi-Tenant | |

| |

| |

| |

| | |

| 1 | |

Westlake | |

TX | |

Charles Schwab & Co., Inc. | |

06/2021 | |

| 130,199 | |

| 2 | |

Florence | |

SC | |

United States of America | |

01/2016 | |

| 12,851 | |

| 3 | |

Farmers Branch | |

TX | |

International Business Machines Corporation | |

04/2021 | |

| 66,018 | |

| 4 | |

Honolulu | |

HI | |

N/A | |

12/2017 | |

| 379 | |

| 4 | |

Total

new office leases | |

| |

| |

| |

| 209,447 | |

| | |

| |

| |

| |

| |

| | |

| | |

Industrial | |

| |

| |

| |

| | |

| 1 | |

McDonough | |

GA | |

United States Cold Storage,

Inc. | |

08/2028 | |

| 296,972 | |

| 1 | |

Total

new industrial leases | |

| |

| |

| |

| 296,972 | |

| | |

| |

| |

| |

| |

| | |

| 5 | |

Total

new leases | |

| |

| |

| |

| 506,419 | |

| | |

| |

| |

| |

| |

| | |

| 10 | |

TOTAL

NEW AND EXTENDED LEASES | |

| |

| |

| |

| 925,409 | |

| (1) | Leases greater than 10,000 square feet. |

BALANCE

SHEET/CAPITAL MARKETS

In December

2015, Lexington financed its industrial property in Richland, Washington with a $110.0 million non-recourse secured mortgage.

The loan bears interest at a fixed rate of 4.0% and matures in 2026.

During 2015,

Lexington announced a 10.0 million common share repurchase authorization. In the fourth quarter of 2015, Lexington repurchased

910,499 common shares at an average price of $8.12 per share, bringing the total common shares repurchased in 2015 to 2,216,799

common shares at an average price of $8.29 per share.

In 2016, Lexington acquired an additional

951,792 common shares at an average price of $7.48 per share. To date, we have repurchased a total of 3.2 million shares at an

average share price of $8.05 per share

2016

EARNINGS GUIDANCE

Lexington is

estimating that its Company FFO guidance for the year ended December 31, 2016 would be within the range of $1.00 to $1.10 per

diluted share. This guidance is forward looking, excludes the impact of certain items and is based on current expectations.

FOURTH

QUARTER 2015 CONFERENCE CALL

Lexington will

host a conference call today, Tuesday, February 23, 2016, at 11:00 a.m. Eastern Time, to discuss its results for the quarter ended

December 31, 2015. Interested parties may participate in this conference call by dialing 877-407-0789 or 201-689-8562. A replay

of the call will be available through March 8, 2016, at 877-870-5176 or 858-384-5517, pin: 13629156. A live webcast of the conference

call will be available at www.lxp.com within the Investors section.

ABOUT

LEXINGTON REALTY TRUST

Lexington Realty

Trust is a real estate investment trust that owns a diversified portfolio of equity and debt interests in single-tenant commercial

properties and land. Lexington seeks to expand its portfolio through acquisitions, sale-leaseback transactions, build-to-suit

arrangements and other transactions. A majority of these properties and all land interests are subject to net or similar leases,

where the tenant bears all or substantially all of the operating costs, including cost increases, for real estate taxes, utilities,

insurance and ordinary repairs. Lexington also provides investment advisory and asset management services to investors in the

single-tenant area. Lexington common shares are traded on the New York Stock Exchange under the symbol “LXP”. Additional

information about Lexington is available on-line at www.lxp.com or by contacting Lexington Realty Trust, One Penn Plaza,

Suite 4015, New York, New York 10119-4015, Attention: Investor Relations.

Contact:

Investor or Media Inquiries for

Lexington Realty Trust:

Heather Gentry, Senior Vice President

of Investor Relations

Lexington Realty Trust

Phone: (212) 692-7200 E-mail: hgentry@lxp.com

This release

contains certain forward-looking statements which involve known and unknown risks, uncertainties or other factors not under Lexington's

control which may cause actual results, performance or achievements of Lexington to be materially different from the results,

performance, or other expectations implied by these forward-looking statements. Factors that could cause or contribute to such

differences include, but are not limited to, those discussed under the headings “Management's Discussion and Analysis of

Financial Condition and Results of Operations” and “Risk Factors” in Lexington's periodic reports filed with

the Securities and Exchange Commission, including risks related to: (1) the authorization by Lexington's Board of Trustees of

future dividend declarations, (2) Lexington's ability to achieve its estimate of Company FFO, as adjusted, for the year ending

December 31, 2016, (3) the successful consummation of any lease, acquisition, build-to-suit, disposition, financing or other transaction,

(4) the failure to continue to qualify as a real estate investment trust, (5) changes in general business and economic conditions,

including the impact of any legislation, (6) competition, (7) increases in real estate construction costs, (8) changes in interest

rates, (9) changes in accessibility of debt and equity capital markets, and (10) future impairment charges. Copies of the periodic

reports Lexington files with the Securities and Exchange Commission are available on Lexington's web site at www.lxp.com.

Forward-looking statements, which are based on certain assumptions and describe Lexington's future plans, strategies and expectations,

are generally identifiable by use of the words “believes,” “expects,” “intends,” “anticipates,”

“estimates,” “projects”, “may,” “plans,” “predicts,” “will,”

“will likely result,” “is optimistic,” “goal,” “objective” or similar expressions.

Except as required by law, Lexington undertakes no obligation to publicly release the results of any revisions to those forward-looking

statements which may be made to reflect events or circumstances after the occurrence of unanticipated events. Accordingly, there

is no assurance that Lexington's expectations will be realized.

References

to Lexington refer to Lexington Realty Trust and its consolidated subsidiaries. All interests in properties and loans are held

through special purpose entities, which are separate and distinct legal entities, some of which are consolidated for financial

statement purposes and/or disregarded for income tax purposes.

LEXINGTON

REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

CONDENSED

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited

and in thousands, except share and per share data)

| | |

Three months

ended December 31, | | |

Twelve months

ended December 31, | |

| | |

2015 | | |

2014 | | |

2015 | | |

2014 | |

| Gross revenues: | |

| | | |

| | | |

| | | |

| | |

| Rental | |

$ | 98,934 | | |

$ | 99,610 | | |

$ | 399,485 | | |

$ | 392,480 | |

| Tenant reimbursements | |

| 7,692 | | |

| 8,173 | | |

| 31,354 | | |

| 31,338 | |

| Total gross revenues | |

| 106,626 | | |

| 107,783 | | |

| 430,839 | | |

| 423,818 | |

| Expense applicable to revenues: | |

| | | |

| | | |

| | | |

| | |

| Depreciation and amortization | |

| (41,403 | ) | |

| (40,105 | ) | |

| (163,198 | ) | |

| (154,837 | ) |

| Property operating | |

| (14,055 | ) | |

| (17,039 | ) | |

| (59,655 | ) | |

| (63,673 | ) |

| General and administrative | |

| (6,750 | ) | |

| (7,221 | ) | |

| (29,276 | ) | |

| (28,255 | ) |

| Non-operating income | |

| 3,216 | | |

| 4,136 | | |

| 11,429 | | |

| 14,505 | |

| Interest and amortization expense | |

| (21,466 | ) | |

| (23,847 | ) | |

| (89,739 | ) | |

| (97,303 | ) |

| Gains on sales of financial assets, net | |

| — | | |

| 855 | | |

| — | | |

| 855 | |

| Debt satisfaction gains (charges), net | |

| 11,397 | | |

| (1,505 | ) | |

| 25,150 | | |

| (9,452 | ) |

| Impairment charges and loan loss | |

| (2,762 | ) | |

| (18,469 | ) | |

| (36,832 | ) | |

| (37,333 | ) |

| Gains on sales of properties | |

| — | | |

| — | | |

| 23,307 | | |

| — | |

| Income before provision for income taxes, equity in earnings of non-consolidated

entities and discontinued operations | |

| 34,803 | | |

| 4,588 | | |

| 112,025 | | |

| 48,325 | |

| Provision for income taxes | |

| (104 | ) | |

| (162 | ) | |

| (568 | ) | |

| (1,109 | ) |

| Equity in earnings of non-consolidated entities | |

| 814 | | |

| 380 | | |

| 1,752 | | |

| 626 | |

| Income from continuing operations | |

| 35,513 | | |

| 4,806 | | |

| 113,209 | | |

| 47,842 | |

| Discontinued operations: | |

| | | |

| | | |

| | | |

| | |

| Income from discontinued operations | |

| — | | |

| 651 | | |

| 109 | | |

| 6,252 | |

| Provision for income taxes | |

| — | | |

| (8 | ) | |

| (4 | ) | |

| (59 | ) |

| Debt satisfaction charges, net | |

| — | | |

| (14 | ) | |

| — | | |

| (312 | ) |

| Gains on sales of properties | |

| — | | |

| 35,455 | | |

| 1,577 | | |

| 57,507 | |

| Impairment charges | |

| — | | |

| (2,705 | ) | |

| — | | |

| (13,767 | ) |

| Total discontinued operations | |

| — | | |

| 33,379 | | |

| 1,682 | | |

| 49,621 | |

| Net income | |

| 35,513 | | |

| 38,185 | | |

| 114,891 | | |

| 97,463 | |

| Less net income attributable

to noncontrolling interests | |

| (663 | ) | |

| (822 | ) | |

| (3,188 | ) | |

| (4,359 | ) |

| Net income attributable to Lexington Realty Trust shareholders | |

| 34,850 | | |

| 37,363 | | |

| 111,703 | | |

| 93,104 | |

| Dividends attributable to preferred shares – Series C | |

| (1,572 | ) | |

| (1,572 | ) | |

| (6,290 | ) | |

| (6,290 | ) |

| Allocation to participating securities | |

| (49 | ) | |

| (91 | ) | |

| (313 | ) | |

| (490 | ) |

| Net income attributable to common shareholders | |

$ | 33,229 | | |

$ | 35,700 | | |

$ | 105,100 | | |

$ | 86,324 | |

| Income per common share – basic: | |

| | | |

| | | |

| | | |

| | |

| Income from continuing operations | |

$ | 0.14 | | |

$ | 0.01 | | |

$ | 0.44 | | |

$ | 0.17 | |

| Income from discontinued

operations | |

| — | | |

| 0.14 | | |

| 0.01 | | |

| 0.21 | |

| Net income attributable

to common shareholders | |

$ | 0.14 | | |

$ | 0.15 | | |

$ | 0.45 | | |

$ | 0.38 | |

| Weighted-average

common shares outstanding – basic | |

| 233,448,100 | | |

| 230,830,905 | | |

| 233,455,056 | | |

| 228,966,253 | |

| Income per common share – diluted: | |

| | | |

| | | |

| | | |

| | |

| Income from continuing operations | |

$ | 0.14 | | |

$ | 0.01 | | |

$ | 0.44 | | |

$ | 0.17 | |

| Income from discontinued

operations | |

| — | | |

| 0.14 | | |

| 0.01 | | |

| 0.21 | |

| Net income attributable

to common shareholders | |

$ | 0.14 | | |

$ | 0.15 | | |

$ | 0.45 | | |

$ | 0.38 | |

| Weighted-average

common shares outstanding – diluted | |

| 239,411,055 | | |

| 231,239,828 | | |

| 233,751,775 | | |

| 229,436,708 | |

| Amounts attributable to common shareholders: | |

| | | |

| | | |

| | | |

| | |

| Income from continuing operations | |

$ | 33,229 | | |

$ | 2,322 | | |

$ | 103,418 | | |

$ | 37,652 | |

| Income from discontinued

operations | |

| — | | |

| 33,378 | | |

| 1,682 | | |

| 48,672 | |

| Net income attributable

to common shareholders | |

$ | 33,229 | | |

$ | 35,700 | | |

$ | 105,100 | | |

$ | 86,324 | |

LEXINGTON

REALTY TRUST AND CONSOLIDATED SUBSIDIARIES

CONDENSED

CONSOLIDATED BALANCE SHEETS

As of December

31,

(Unaudited and

in thousands, except share and per share data)

| | |

2015 | | |

2014 | |

| Assets: | |

| | | |

| | |

| Real estate, at cost | |

$ | 3,789,711 | | |

$ | 3,671,560 | |

| Real estate - intangible assets | |

| 692,778 | | |

| 705,566 | |

| Investments in real estate under construction | |

| 95,402 | | |

| 106,238 | |

| | |

| 4,577,891 | | |

| 4,483,364 | |

| Less: accumulated depreciation and amortization | |

| 1,179,969 | | |

| 1,196,114 | |

| Real estate, net | |

| 3,397,922 | | |

| 3,287,250 | |

| Assets held for sale | |

| 24,425 | | |

| 3,379 | |

| Cash and cash equivalents | |

| 93,249 | | |

| 191,077 | |

| Restricted cash | |

| 10,637 | | |

| 17,379 | |

| Investment in and advances to non-consolidated

entities | |

| 31,054 | | |

| 19,402 | |

| Deferred expenses, net | |

| 63,832 | | |

| 65,860 | |

| Loans receivable, net | |

| 95,871 | | |

| 105,635 | |

| Rent receivable – current | |

| 7,193 | | |

| 6,311 | |

| Rent receivable – deferred | |

| 87,547 | | |

| 61,372 | |

| Other assets | |

| 18,505 | | |

| 20,229 | |

| Total assets | |

$ | 3,830,235 | | |

$ | 3,777,894 | |

| | |

| | | |

| | |

| Liabilities and Equity: | |

| | | |

| | |

| Liabilities: | |

| | | |

| | |

| Mortgages and notes payable | |

$ | 882,952 | | |

$ | 945,216 | |

| Credit facility borrowings | |

| 177,000 | | |

| — | |

| Term loans payable | |

| 505,000 | | |

| 505,000 | |

| Senior notes payable | |

| 497,947 | | |

| 497,675 | |

| Convertible notes payable | |

| 12,180 | | |

| 15,664 | |

| Trust preferred securities | |

| 129,120 | | |

| 129,120 | |

| Dividends payable | |

| 45,440 | | |

| 42,864 | |

| Liabilities held for sale | |

| 8,405 | | |

| 2,843 | |

| Accounts payable and other liabilities | |

| 41,479 | | |

| 37,740 | |

| Accrued interest payable | |

| 8,851 | | |

| 8,301 | |

| Deferred revenue - including below market leases,

net | |

| 42,524 | | |

| 68,215 | |

| Prepaid rent | |

| 16,806 | | |

| 16,336 | |

| Total liabilities | |

| 2,367,704 | | |

| 2,268,974 | |

| | |

| | | |

| | |

| Commitments and contingencies | |

| | | |

| | |

| Equity: | |

| | | |

| | |

| Preferred shares, par value $0.0001 per share;

authorized 100,000,000 shares: | |

| | | |

| | |

| Series C Cumulative Convertible

Preferred, liquidation preference $96,770; 1,935,400 shares issued and outstanding | |

| 94,016 | | |

| 94,016 | |

| Common shares, par value

$0.0001 per share; authorized 400,000,000 shares, 234,575,225 and 233,278,037 shares issued and outstanding in 2015 and 2014,

respectively | |

| 23 | | |

| 23 | |

| Additional paid-in-capital | |

| 2,776,837 | | |

| 2,763,374 | |

| Accumulated distributions in excess of net income

(loss) | |

| (1,428,908 | ) | |

| (1,372,051 | ) |

| Accumulated other comprehensive

income (loss) | |

| (1,939 | ) | |

| 404 | |

| Total shareholders’ equity | |

| 1,440,029 | | |

| 1,485,766 | |

| Noncontrolling interests | |

| 22,502 | | |

| 23,154 | |

| Total equity | |

| 1,462,531 | | |

| 1,508,920 | |

| Total liabilities and equity | |

$ | 3,830,235 | | |

$ | 3,777,894 | |

| LEXINGTON

REALTY TRUST AND CONSOLIDATED SUBSIDIARIES |

| EARNINGS

PER SHARE |

| (Unaudited

and in thousands, except share and per share data) |

| | |

Three Months

Ended

December 31, | | |

Twelve Months

Ended

December 31, | |

| | |

2015 | | |

2014 | | |

2015 | | |

2014 | |

| EARNINGS PER SHARE: | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | |

| |

| Basic: | |

| | | |

| | | |

| | | |

| | |

| Income from

continuing operations attributable to common shareholders | |

$ | 33,229 | | |

$ | 2,322 | | |

$ | 103,418 | | |

$ | 37,652 | |

| Income

from discontinued operations attributable to common shareholders | |

| — | | |

| 33,378 | | |

| 1,682 | | |

| 48,672 | |

| Net

income attributable to common shareholders | |

$ | 33,229 | | |

$ | 35,700 | | |

$ | 105,100 | | |

$ | 86,324 | |

| | |

| | | |

| | | |

| | | |

| | |

| Weighted-average

number of common shares outstanding | |

| 233,448,100 | | |

| 230,830,905 | | |

| 233,455,056 | | |

| 228,966,253 | |

| | |

| | | |

| | | |

| | | |

| | |

| Income per common share: | |

| | | |

| | | |

| | | |

| | |

| Income from continuing operations | |

$ | 0.14 | | |

$ | 0.01 | | |

$ | 0.44 | | |

$ | 0.17 | |

| Income from

discontinued operations | |

| — | | |

| 0.14 | | |

| 0.01 | | |

| 0.21 | |

| Net income

attributable to common shareholders | |

$ | 0.14 | | |

$ | 0.15 | | |

$ | 0.45 | | |

$ | 0.38 | |

| | |

| | | |

| | | |

| | | |

| | |

| Diluted: | |

| | | |

| | | |

| | | |

| | |

| Income from continuing operations

attributable to common shareholders - basic | |

$ | 33,229 | | |

$ | 2,322 | | |

$ | 103,418 | | |

$ | 37,652 | |

| Impact of assumed conversions | |

| 711 | | |

| — | | |

| — | | |

| — | |

| Income

from continuing operations attributable to common shareholders | |

| 33,940 | | |

| 2,322 | | |

| 103,418 | | |

| 37,652 | |

| Income from discontinued operations

attributable to common shareholders - basic | |

| — | | |

| 33,378 | | |

| 1,682 | | |

| 48,672 | |

| Impact of assumed conversions | |

| — | | |

| — | | |

| — | | |

| — | |

| Income

from discontinued operations attributable to common shareholders | |

| — | | |

| 33,378 | | |

| 1,682 | | |

| 48,672 | |

| Net income attributable

to common shareholders | |

$ | 33,940 | | |

$ | 35,700 | | |

$ | 105,100 | | |

$ | 86,324 | |

| | |

| | | |

| | | |

| | | |

| | |

| Weighted-average common shares

outstanding - basic | |

| 233,448,100 | | |

| 230,830,905 | | |

| 233,455,056 | | |

| 228,966,253 | |

| Effect of dilutive securities: | |

| | | |

| | | |

| | | |

| | |

| Share options | |

| 220,125 | | |

| 408,923 | | |

| 296,719 | | |

| 470,455 | |

| Operating Partnership Units | |

| 3,834,962 | | |

| — | | |

| — | | |

| — | |

| 6.00% Convertible

Guaranteed Notes | |

| 1,907,868 | | |

| — | | |

| — | | |

| — | |

| Weighted-average

common shares outstanding | |

| 239,411,055 | | |

| 231,239,828 | | |

| 233,751,775 | | |

| 229,436,708 | |

| | |

| | | |

| | | |

| | | |

| | |

| Income per common share: | |

| | | |

| | | |

| | | |

| | |

| Income from continuing operations | |

$ | 0.14 | | |

$ | 0.01 | | |

$ | 0.44 | | |

$ | 0.17 | |

| Income from

discontinued operations | |

| — | | |

| 0.14 | | |

| 0.01 | | |

| 0.21 | |

| Net income

attributable to common shareholders | |

$ | 0.14 | | |

$ | 0.15 | | |

$ | 0.45 | | |

$ | 0.38 | |

| LEXINGTON

REALTY TRUST AND CONSOLIDATED SUBSIDIARIES |

| COMPANY

FUNDS FROM OPERATIONS & FUNDS AVAILABLE FOR DISTRIBUTION |

| (Unaudited

and in thousands, except share and per share data) |

| | |

Three Months

Ended

December 31, | | |

Twelve Months

Ended

December 31, | |

| | |

2015 | | |

2014 | | |

2015 | | |

2014 | |

| FUNDS

FROM OPERATIONS: (1) | |

| | | |

| | | |

| | | |

| | |

| Basic and

Diluted: | |

| | | |

| | | |

| | | |

| | |

| Net income attributable

to common shareholders | |

$ | 33,229 | | |

$ | 35,700 | | |

$ | 105,100 | | |

$ | 86,324 | |

| Adjustments: | |

| | | |

| | | |

| | | |

| | |

| Depreciation and amortization | |

| 39,708 | | |

| 39,546 | | |

| 157,644 | | |

| 157,537 | |

| Impairment charges - real estate,

including non-consolidated entities | |

| 2,762 | | |

| 18,673 | | |

| 36,832 | | |

| 49,529 | |

| Noncontrolling interests - OP

units | |

| 457 | | |

| 434 | | |

| 1,999 | | |

| 2,990 | |

| Amortization of leasing commissions | |

| 1,695 | | |

| 1,426 | | |

| 5,554 | | |

| 5,932 | |

| Joint venture and noncontrolling

interest adjustment | |

| 453 | | |

| 335 | | |

| 1,788 | | |

| 2,068 | |

| Gains on

sales of properties, including non-consolidated entities | |

| (487 | ) | |

| (36,374 | ) | |

| (25,371 | ) | |

| (58,426 | ) |

| FFO available

to common shareholders and unitholders - basic | |

| 77,817 | | |

| 59,740 | | |

| 283,546 | | |

| 245,954 | |

| Preferred dividends | |

| 1,572 | | |

| 1,572 | | |

| 6,290 | | |

| 6,290 | |

| Interest and amortization on

6.00% Convertible Notes | |

| 253 | | |

| 472 | | |

| 1,048 | | |

| 2,090 | |

| Amount

allocated to participating securities | |

| 49 | | |

| 91 | | |

| 313 | | |

| 490 | |

| FFO available

to common shareholders and unitholders - diluted | |

| 79,691 | | |

| 61,875 | | |

| 291,197 | | |

| 254,824 | |

| Debt satisfaction (gains) charges,

net, including non-consolidated entities | |

| (11,397 | ) | |

| 1,519 | | |

| (25,086 | ) | |

| 9,764 | |

| Impairment loss - loan receivable | |

| — | | |

| 2,500 | | |

| — | | |

| 2,500 | |

| Transaction

costs/Other | |

| 1,285 | | |

| 368 | | |

| 1,864 | | |

| 1,882 | |

| Company FFO

available to common shareholders and unitholders - diluted | |

| 69,579 | | |

| 66,262 | | |

| 267,975 | | |

| 268,970 | |

| | |

| | | |

| | | |

| | | |

| | |

| FUNDS

AVAILABLE FOR DISTRIBUTION: (2) | |

| | | |

| | | |

| | | |

| | |

| Adjustments: | |

| | | |

| | | |

| | | |

| | |

| Straight-line rents | |

| (12,460 | ) | |

| (16,170 | ) | |

| (47,702 | ) | |

| (47,227 | ) |

| Lease incentives | |

| 387 | | |

| 386 | | |

| 1,544 | | |

| 1,490 | |

| Amortization of below/above

market leases | |

| 418 | | |

| 233 | | |

| 261 | | |

| 1,136 | |

| Lease termination payments,

net | |

| 2,420 | | |

| (1,227 | ) | |

| 3,086 | | |

| 1,571 | |

| Non-cash interest, net | |

| (638 | ) | |

| 1,294 | | |

| (118 | ) | |

| (2,892 | ) |

| Non-cash charges, net | |

| 2,213 | | |

| 2,141 | | |

| 8,821 | | |

| 8,704 | |

| Tenant improvements | |

| (7,242 | ) | |

| (5,435 | ) | |

| (20,426 | ) | |

| (11,395 | ) |

| Lease costs | |

| (2,439 | ) | |

| (2,070 | ) | |

| (6,681 | ) | |

| (10,484 | ) |

| Company

Funds Available for Distribution | |

$ | 52,238 | | |

$ | 45,414 | | |

$ | 206,760 | | |

$ | 209,873 | |

| | |

| | | |

| | | |

| | | |

| | |

| Per Common

Share and Unit Amounts | |

| | | |

| | | |

| | | |

| | |

| Basic: | |

| | | |

| | | |

| | | |

| | |

| FFO | |

$ | 0.33 | | |

$ | 0.25 | | |

$ | 1.19 | | |

$ | 1.06 | |

| | |

| | | |

| | | |

| | | |

| | |

| Diluted: | |

| | | |

| | | |

| | | |

| | |

| FFO | |

$ | 0.33 | | |

$ | 0.25 | | |

$ | 1.19 | | |

$ | 1.05 | |

| Company FFO | |

$ | 0.29 | | |

$ | 0.27 | | |

$ | 1.10 | | |

$ | 1.11 | |

| Company FAD | |

$ | 0.21 | | |

$ | 0.19 | | |

$ | 0.85 | | |

$ | 0.87 | |

| | |

| | | |

| | | |

| | | |

| | |

| Weighted-Average Common Shares: | |

| | | |

| | | |

| | | |

| | |

| Basic(3) | |

| 237,283,062 | | |

| 234,688,921 | | |

| 237,303,490 | | |

| 232,838,280 | |

| Diluted | |

| 244,121,625 | | |

| 243,398,807 | | |

| 244,355,734 | | |

| 241,967,017 | |

1

Lexington believes that Funds from Operations (“FFO”), which is not a measure under

generally accepted accounting principles (“GAAP”), is a widely recognized and appropriate measure of the performance

of an equity REIT. Lexington believes FFO is frequently used by securities analysts, investors and other interested parties in

the evaluation of REITs, many of which present FFO when reporting their results. FFO is intended to exclude GAAP historical cost

depreciation and amortization of real estate and related assets, which assumes that the value of real estate diminishes ratably

over time. Historically, however, real estate values have risen or fallen with market conditions. As a result, FFO provides a

performance measure that, when compared year over year, reflects the impact to operations from trends in occupancy rates, rental

rates, operating costs, development activities, interest costs and other matters without the inclusion of depreciation and amortization,

providing perspective that may not necessarily be apparent from net income.

The National

Association of Real Estate Investment Trusts, Inc. (“NAREIT”) defines FFO as “net income (or loss) computed

in accordance with GAAP, excluding gains (or losses) from sales of property, plus real estate depreciation and amortization and

after adjustments for unconsolidated partnerships and joint ventures.” NAREIT clarified its computation of FFO to exclude

impairment charges on depreciable real estate owned directly or indirectly. FFO does not represent cash generated from operating

activities in accordance with GAAP and is not indicative of cash available to fund cash needs.

Lexington presents

FFO available to common shareholders and unitholders - basic. Lexington also presents FFO available to common shareholders and

unitholders - diluted on a company-wide basis as if all securities that are convertible, at the holder's option, into Lexington's

common shares, are converted at the beginning of the period. Lexington also presents Company FFO which adjusts FFO for certain

items which Management believes are not indicative of the operating results of its real estate portfolio. Management believes

this is an appropriate presentation as it is frequently requested by security analysts, investors and other interested parties.

Since others do not calculate funds from operations in a similar fashion, Company FFO may not be comparable to similarly titled

measures as reported by others. Company FFO should not be considered as an alternative to net income as an indicator of our operating

performance or as an alternative to cash flow as a measure of liquidity.

2 Company

Funds Available for Distribution ("FAD") is calculated by making adjustments to Company FFO for (1) straight-line rent

revenue, (2) lease incentive amortization, (3) amortization of above/below market leases, (4) lease termination payments, net,

(5) non-cash interest, net, (6) non-cash charges, net, (7) cash paid for tenant improvements, and (8) cash paid for lease costs.

Although FAD may not be comparable to that of other REITs, Lexington believes it provides a meaningful indication of its ability

to fund cash needs. FAD is a non-GAAP financial measure and should not be viewed as an alternative measurement of operating performance

to net income, as an alternative to net cash flows from operating activities or as a measure of liquidity.

3 Includes

OP units other than OP units held by us.

#

# #

LEXINGTON

REALTY TRUST

2015 Fourth

Quarter Investment / Capital Recycling Summary

PROPERTY INVESTMENTS

| | |

Primary

Tenant (Guarantor) | |

Location | |

Property

Type | |

Initial

Basis

($000) | | |

Initial

Annualized

Cash Rent ($000) | | |

Initial

Cash

Yield | | |

Initial

GAAP

Yield | | |

Month

Closed | |

Primary

Lease

Expiration |

| 1 | |

Preferred Freezer Services of Richland

LLC (Preferred Freezer Services, LLC & Preferred Freezer Services Operating, LLC) (1) | |

Richland | |

WA | |

Industrial | |

$ | 152,000 | | |

$ | 10,792 | | |

| 7.1 | % | |

| 8.6 | % | |

November | |

08/2035 |

| 2 | |

McGuireWoods LLP

(2) | |

Richmond | |

VA | |

Office | |

| 101,489 | | |

| 8,701 | | |

| 8.2 | % | |

| 9.0 | % | |

December | |

08/2030 |

| 2 | |

TOTAL PROPERTY

INVESTMENT | |

| |

| |

| |

$ | 253,489 | | |

$ | 19,493 | | |

| 7.6 | % | |

| 8.8 | % | |

| |

|

CAPITAL RECYCLING

| | |

PROPERTY DISPOSITIONS | |

| |

| |

| | |

| | |

| | |

| | |

| |

| | |

| |

| |

| |

| | |

| | |

| | |

| | |

| |

| | |

Tenant | |

Location | |

Property

Type | |

Gross

Disposition

Price

($000) | | |

Annualized NOI

($000) | | |

Month of

Disposition | | |

% Leased | | |

Gross

Disposition

Price PSF | |

| 1 | |

Vacant (3) | |

Rochester | |

NY | |

Office | |

$ | 17,234 | | |

$ | - | | |

| December | | |

| 0 | % | |

$ | 76.26 | |

| |

Footnotes |

| (1) |

ConAgra Foods Inc. provides credit support. |

| (2) |

Property is 100% leased. McGuireWoods LLP is primary tenant with 68% of the space.

Initial basis does not include

$8.1 million for estimated earnout lease payments for developer leased space.

Initial yields include $4.0 million of earnout lease

payments earned but not yet paid as of 12/31/2015. |

| (3) |

Property conveyed through foreclosure. |

LEXINGTON

REALTY TRUST

BUILD-TO-SUIT

PROJECTS / FORWARD PURCHASE COMMITMENTS

12/31/2015

BUILD-TO-SUIT PROJECTED CONSTRUCTION

FUNDING SCHEDULE (1)

| | |

Location | |

Sq.

Ft | | |

Asset

Type | |

Lease

Term (Years) | |

Maximum

Commitment/

Estimated

Completion

Cost ($000) | | |

Investment

balance as of

12/31/15

($000) | | |

Estimated

Cash Investment Next 12 Months ($000) | | |

Estimated

Completion/

Acquisition

Date | |

Estimated

Initial

Cash

Yield | | |

Estimated

GAAP

Yield | |

| | |

| |

| |

| | |

| |

| |

| | |

| | |

Q1

2016 | | |

Q2

2016 | | |

Q3

2016 | | |

Q4

2016 | | |

| |

| | |

| |

| 1 | |

Anderson | |

SC | |

| 1,325,000 | | |

Industrial | |

20 | |

$ | 70,012 | | |

$ | 23,826 | | |

$ | 21,088 | | |

$ | 24,536 | | |

$ | - | | |

$ | - | | |

2Q16 | |

| 5.9 | % | |

| 7.3 | % |

| 2 | |

Lake Jackson | |

TX | |

| 664,000 | | |

Office | |

20 | |

| 166,164 | | |

| 62,353 | | |

| 300 | | |

| 33,818 | | |

| 50,577 | | |

| 16,859 | | |

4Q 16 | |

| 7.3 | % | |

| 8.9 | % |

| 3 | |

Charlotte | |

NC | |

| 201,000 | | |

Office | |

15 | |

| 62,445 | | |

| 9,223 | | |

| 8,425 | | |

| 11,130 | | |

| 11,130 | | |

| 11,130 | | |

1Q 17 | |

| 8.3 | % | |

| 9.5 | % |

| | |

| |

| |

| | | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| | | |

| | |

| 3 | |

TOTAL CONSOLIDATED BUILD-TO-SUIT PROJECTS (2) | |

| | | |

| |

| |

$ | 298,621 | | |

$ | 95,402 | | |

$ | 29,813 | | |

$ | 69,484 | | |

$ | 61,707 | | |

$ | 27,989 | | |

| |

| | | |

| | |

| | |

| |

| |

| | | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| | | |

| | |

| 1 | |

Houston (3) | |

TX | |

| 274,000 | | |

Retail/Specialty | |

20 | |

$ | 86,491 | | |

$ | 38,367 | | |

$ | 15,269 | | |

$ | 15,269 | | |

$ | 15,269 | | |

$ | - | | |

3Q 16 | |

| 7.5 | % | |

| 7.5 | % |

| | |

| |

| |

| | | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| | | |

| | |

| 1 | |

TOTAL NON-CONSOLIDATED BUILD-TO-SUIT PROJECTS | |

| | | |

| |

| |

$ | 86,491 | | |

$ | 38,367 | | |

$ | 15,269 | | |

$ | 15,269 | | |

$ | 15,269 | | |

$ | - | | |

| |

| | | |

| | |

| | |

| |

| |

| | | |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| |

| | | |

| | |

| 4 | |

TOTAL BUILD-TO-SUIT PROJECTS | |

| | | |

| |

| |

$ | 385,112 | | |

$ | 133,769 | | |

$ | 45,082 | | |

$ | 84,753 | | |

$ | 76,976 | | |

$ | 27,989 | | |

| |

| | | |

| | |

FORWARD PURCHASE COMMITMENTS

(1)

| | |

Tenant | |

Location | |

Property Type | |

Sq.

Ft. | | |

Estimated

Acquisition

Cost ($000) | | |

Estimated

Completion/

Acquisition

Date | |

Estimated

Initial Cash

Yield | | |

Estimated

GAAP Yield | | |

Lease Term |

| 1 | |

FCA US LLC (F/K/A Chrysler Group

LLC) (4) | |

Detroit, MI | |

Industrial | |

| 189,960 | | |

$ | 29,680 | | |

1Q 16 | |

| 7.4 | % | |

| 7.4 | % | |

20 yrs |

| | |

| |

| |

| |

| | | |

| | | |

| |

| | | |

| | | |

|

| 1 | |

TOTAL FORWARD PURCHASE COMMITMENTS | |

| |

| |

| | | |

| | | |

| |

| | | |

| | | |

|

| BUILD-TO-SUIT NOI (5) | |

| | |

| | |

| | |

| | |

| |

| | |

2011 | | |

2012 | | |

2013 | | |

2014 | | |

2015 | |

| Net operating income ($000) | |

$ | 1,156 | | |

$ | 5,268 | | |

$ | 11,920 | | |

$ | 21,438 | | |

$ | 27,462 | |

Footnotes

| (1) | Lexington can give no assurance that

any of the build-to-suit projects or other potential investments that are under commitment

or contract or in process will be completed. |

| (2) | Investment balance in accordance with

GAAP included in investment in real estate under construction. Aggregate equity invested

is $98.2 million. |

| (3) | Lexington has a 25% interest as of

December 31, 2015. Lexington is providing construction financing up to $56.7 million

to the joint venture, of which $8.5 million has been funded as of December 31, 2015.

Estimated cash investments for the next 12 months are Lexington's estimated loan amounts.

Lease contains annual CPI increases. |

| (4) | Lexington funded a $2.5 million deposit.

Property acquired January 2016. |

| (5) | Net operating income generated from

completed build-to-suit projects funded by Lexington beginning in 2010. |

LEXINGTON

REALTY TRUST

2015 Fourth

Quarter Financing Summary

| DEBT RETIRED | |

| |

| |

| | |

| | |

|

| | |

| |

| |

| | |

| | |

|

| Location | |

Tenant (Guarantor) | |

Property Type | |

Face / Satisfaction

($000) | | |

Fixed Rate | | |

Maturity Date |

| | |

| |

| |

| | | |

| | | |

|

| Consolidated Mortgage Debt: | |

| |

| |

| | | |

| | | |

|

| Rochester, NY (1) | |

Vacant | |

Office | |

$ | 17,234 | | |

| 6.21 | % | |

08/2016 |

PROPERTY LEVEL FINANCING

| | |

| |

| |

| | |

| | |

|

| Location | |

Tenant (Guarantor) | |

Property Type | |

| Face

($000) | | |

| Fixed Rate | | |

Maturity Date |

| | |

| |

| |

| | | |

| | | |

|

| Richland, WA | |

Preferred Freezer Services of Richland LLC (Preferred Freezer Services, LLC & Preferred Freezer Services Operating, LLC) | |

Industrial | |

$ | 110,000 | | |

| 4.00 | % | |

01/2026 |

Footnotes

| (1) | Property conveyed through foreclosure. |

LEXINGTON REALTY TRUST

2015 Fourth Quarter Leasing Summary

LEASE EXTENSIONS

| | |

Tenant (Guarantor) | |

Location | |

Prior

Term | |

Lease Expiration

Date | |

Sq.

Ft. | | |

New

Cash

Rent Per

Annum

($000)(1) | | |

Prior

Cash Rent

Per Annum

($000) | | |

New

GAAP

Rent Per

Annum

($000)(1) | | |

Prior

GAAP Rent

Per Annum

($000) | |

| | |

| |

| |

| |

| |

| |

| | |

| | |

| | |

| | |

| |

| | |

Office / Multi-Tenant | |

| |

| |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | |

| 1-3 | |

Various | |

Honolulu | |

HI | |

2015 | |

2016-2018 | |

| 886 | | |

$ | 10 | | |

$ | 10 | | |

$ | 10 | | |

$ | 10 | |

| | |

| |

| |

| |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | |

| 3 | |

Total office lease extensions | |

| |

| |

| |

| |

| 886 | | |

$ | 10 | | |

$ | 10 | | |

$ | 10 | | |

$ | 10 | |

| | |

| |

| |

| |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

Industrial | |

| |

| |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | |

| 1 | |

MAHLE Aftermarket Inc. (MAHLE Industries, Incorporated) | |

Olive Branch | |

MS | |

02/2016 | |

02/2023 | |

| 268,104 | | |

$ | 871 | | |

$ | 954 | | |

$ | 906 | | |

$ | 905 | |

| 2 | |

Jacobson Warehouse Company, Inc. | |

Rockford | |

IL | |

12/2015 | |

12/2018 | |

| 150,000 | | |

| 525 | | |

| 476 | | |

| 471 | | |

| 488 | |

| | |

| |

| |

| |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | |

| 2 | |

Total industrial lease extensions | |

| |

| |

| |

| |

| 418,104 | | |

$ | 1,396 | | |

$ | 1,430 | | |

$ | 1,377 | | |

$ | 1,393 | |

| | |

| |

| |

| |

| |

| |

| | | |

| | | |

| | | |

| | | |

| | |

| 5 | |

TOTAL EXTENDED LEASES | |

| |

| |

| |

| |

| 418,990 | | |

$ | 1,406 | | |

$ | 1,440 | | |

$ | 1,387 | | |

$ | 1,403 | |

NEW LEASES

| | |

Tenant | |

Location | |

Lease

Expiration

Date | |

Sq.

Ft. | | |

New

Cash

Rent Per

Annum

($000)(1) | | |

New

GAAP

Rent Per

Annum

($000)(1) | |

| | |

Office / Multi-Tenant Office | |

| |

| |

| |

| | | |

| | | |

| | |

| 1 | |

Charles Schwab & Co, Inc. | |

Westlake | |

TX | |

06/2021 | |

| 130,199 | | |

$ | 2,018 | | |

$ | 3,476 | |

| 2 | |

United States of America (2) | |

Florence | |

SC | |

01/2016 | |

| 12,851 | | |

| 257 | | |

| 257 | |

| 3 | |

International Business Machines Corporation | |

Farmers Branch | |

TX | |

04/2021 | |

| 66,018 | | |

| 988 | | |

| 1,056 | |

| 4 | |

Valdeshia Kelly and Corinthian Kelly | |

Honolulu | |

HI | |

12/2017 | |

| 379 | | |

| 8 | | |

| 8 | |

| | |

| |

| |

| |

| |

| | | |

| | | |

| | |

| 4 | |

Total office new leases | |

| |

| |

| |

| 209,447 | | |

$ | 3,271 | | |

$ | 4,797 | |

| | |

| |

| |

| |

| |

| | | |

| | | |

| | |

| | |

Industrial | |

| |

| |

| |

| | | |

| | | |

| | |

| 1 | |

United States Cold Storage, Inc. | |

McDonough | |

GA | |

08/2028 | |

| 296,972 | | |

$ | 2,109 | | |

$ | 2,251 | |

| | |

| |

| |

| |

| |

| | | |

| | | |

| | |

| 1 | |

Total industrial new lease | |

| |

| |

| |

| 296,972 | | |

$ | 2,109 | | |

$ | 2,251 | |

| | |

| |

| |

| |

| |

| | | |

| | | |

| | |

| 5 | |

TOTAL NEW LEASES | |

| |

| |

| |

| 506,419 | | |

$ | 5,380 | | |

$ | 7,048 | |

| | |

| |

| |

| |

| |

| | | |

| | | |

| | |

| 10 | |

TOTAL NEW AND EXTENDED

LEASES | |

| |

| |

| |

| 925,409 | | |

$ | 6,786 | | |

$ | 8,435 | |

Footnotes

| (1) | Assumes twelve months rent from the later of 1/1/16 or full lease commencement/extension, excluding free rent periods as applicable. |

| (2) | Tenant lease has expired, and tenant has vacated. |

LEXINGTON REALTY TRUST

Other Revenue Data

12/31/2015

($000)

Other Revenue Data

| | |

GAAP Rent | |

| Asset Class | |

Twelve months ended | |

| | |

| 12/31/15 (1) | | |

| 12/31/15

Percentage | | |

| 12/31/14

Percentage | |

| Office | |

$ | 192,863 | | |

| 50.1 | % | |

| 51.4 | % |

| Industrial | |

| 107,263 | | |

| 27.9 | % | |

| 23.0 | % |

| Land / Infrastructure | |

| 61,534 | | |

| 16.0 | % | |

| 14.3 | % |

| Multi-tenant | |

| 11,450 | | |

| 3.0 | % | |

| 8.7 | % |

| Retail/Specialty | |

| 11,879 | | |

| 3.0 | % | |

| 2.6 | % |

| | |

$ | 384,989 | | |

| 100.0 | % | |

| 100.0 | % |

| | |

GAAP Rent | |

| Credit Ratings (2) | |

Twelve months ended | |

| | |

| 12/31/15 (1) | | |

| 12/31/15

Percentage | | |

| 12/31/14

Percentage | |

| Investment Grade | |

$ | 132,787 | | |

| 34.5 | % | |

| 36.6 | % |

| Non-Investment Grade | |

| 57,419 | | |

| 14.9 | % | |

| 12.4 | % |

| Unrated | |

| 194,783 | | |

| 50.6 | % | |

| 51.0 | % |

| | |

$ | 384,989 | | |

| 100.0 | % | |

| 100.0 | % |

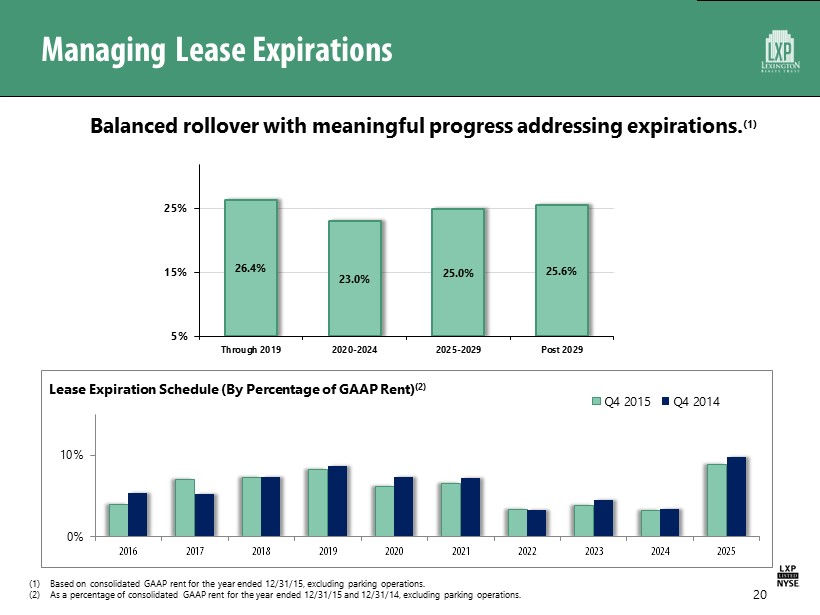

| Weighted-Average Lease Term - Cash Basis |

As of 12/31/15 |

|

As of 12/31/14 |

|

| |

12.6 years |

|

12.1 years |

|

| Weighted-Average Lease Term - Cash Basis - Adjusted (3) |

As of 12/31/15 |

|

As of 12/31/14 |

|

| |

9.1 years |

|

8.6 years |

|

Rent Estimates for Current Assets

| Year | |

Cash (4) | | |

GAAP (4) | | |

Projected

Straight-line /

GAAP Rent

Adjustment | |

| 2016 | |

$ | 355,680 | | |

$ | 401,712 | | |

$ | (46,032 | ) |

| 2017 | |

$ | 331,210 | | |

$ | 372,673 | | |

$ | (41,463 | ) |

Footnotes

| (1) | Twelve months ended 12/31/2015 GAAP rent recognized for consolidated properties owned as of 12/31/2015. |

| (2) | Credit ratings are based upon either tenant, guarantor or parent. Generally, multi-tenant assets are included in unrated. |

| (3) | Adjusted to reflect NY land leases to the first purchase option date. |

| (4) | Amounts assume (1) lease terms for non-cancellable periods only, (2) no new or renegotiated leases are entered into after 12/31/2015,

and (3) no properties are sold or acquired after 12/31/2015. |

LEXINGTON REALTY TRUST

Other Revenue Data (Continued)

12/31/2015

($000)

Same-Store NOI (1)(2)

| | |

Twelve months ended December 31, | |

| | |

2015 | | |

2014 | |

| Total Base Rent | |

$ | 302,827 | | |

$ | 303,495 | |

| Tenant Reimbursements | |

| 28,637 | | |

| 28,109 | |

| Property Operating Expenses | |

| (47,578 | ) | |

| (47,416 | ) |

| Same-Store NOI | |

$ | 283,886 | | |

$ | 284,188 | |

| | |

| | | |

| | |

| Change in Same-Store NOI | |

| (0.1 | )% | |

| | |

Same-Store Percent Leased (2)

| | |

As of 12/31/15 | | |

As of 12/31/14 | |

| |

| 97.6 | % | |

| 98.0 | % |

Lease Escalation Data (3)

Footnotes

| (1) |

NOI is on a consolidated cash basis for all consolidated properties except properties acquired/expanded and sold in 2015 and 2014 and excludes lease termination payments. |

| (2) |

Adjusted for potential foreclosure on the Bridgewater, NJ property. |

| (3) |

Based on twelve months consolidated cash base rents for single-tenant leases. Excludes parking operations and $7.8 million in step-down leases. |

LEXINGTON REALTY TRUST

Portfolio Detail By Asset Class

12/31/2015

( $000, except square footage)

| Asset Class | |

YE 2012 | | |

YE 2013 | | |

YE 2014 | | |

YE 2015 | |

| | |

| | | |

| | | |

| | | |

| | |

| Office | |

| | | |

| | | |

| | | |

| | |

| % of ABR (1) | |

| 64.3 | % | |

| 61.3 | % | |

| 51.4 | % | |

| 50.1 | % |

| LTL (5) | |

| 22.4 | % | |

| 26.8 | % | |

| 31.8 | % | |

| 23.4 | % |

| STL (6) | |

| 77.6 | % | |

| 73.2 | % | |

| 68.2 | % | |

| 76.6 | % |

| Leased | |

| 98.6 | % | |

| 99.0 | % | |

| 98.6 | % | |

| 99.6 | % |

| Wtd. Avg. Lease Term (2) | |

| 6.6 | | |

| 7.2 | | |

| 7.4 | | |

| 7.2 | |

| Mortgage Debt | |

$ | 1,078,345 | | |

$ | 692,460 | | |

$ | 426,635 | | |

$ | 329,696 | |

| % Investment Grade (1) | |

| 62.1 | % | |

| 57.2 | % | |

| 53.7 | % | |

| 48.7 | % |

| Square Feet | |

| 15,726,609 | | |

| 15,316,875 | | |

| 13,264,134 | | |

| 12,847,877 | |

| Cash Base Rent | |

$ | 198,183 | | |

$ | 214,774 | | |

$ | 192,865 | | |

$ | 183,249 | |

| | |

| | | |

| | | |

| | | |

| | |

| Industrial | |

| | | |

| | | |

| | | |

| | |

| % of ABR (1) | |

| 22.9 | % | |

| 23.2 | % | |

| 23.0 | % | |

| 27.9 | % |

| LTL (5) | |

| 33.7 | % | |

| 35.2 | % | |

| 42.8 | % | |

| 43.1 | % |

| STL (6) | |

| 66.3 | % | |

| 64.8 | % | |

| 57.2 | % | |

| 56.9 | % |

| Leased | |

| 99.6 | % | |

| 99.8 | % | |

| 99.7 | % | |

| 99.6 | % |

| Wtd. Avg. Lease Term (2) | |

| 7.5 | | |

| 7.2 | | |

| 7.9 | | |

| 9.5 | |

| Mortgage Debt | |

$ | 221,055 | | |

$ | 206,209 | | |

$ | 177,951 | | |

$ | 292,293 | |

| % Investment Grade (1) | |

| 23.1 | % | |

| 34.1 | % | |

| 29.3 | % | |

| 30.3 | % |

| Square Feet | |

| 21,317,359 | | |

| 21,473,994 | | |

| 22,612,691 | | |

| 25,561,136 | |

| Cash Base Rent | |

$ | 70,600 | | |

$ | 84,039 | | |

$ | 89,991 | | |

$ | 105,032 | |

| | |

| | | |

| | | |

| | | |

| | |

| Land/Infrastructure | |

| | | |

| | | |

| | | |

| | |

| % of ABR (1) | |

| 0.5 | % | |

| 4.9 | % | |

| 14.3 | % | |

| 16.0 | % |

| LTL (5) | |

| 100.0 | % | |

| 100.0 | % | |

| 100.0 | % | |

| 100.0 | % |

| STL (6) | |

| 0.0 | % | |

| 0.0 | % | |

| 0.0 | % | |

| 0.0 | % |

| Leased | |

| 100.0 | % | |

| 100.0 | % | |

| 100.0 | % | |

| 100.0 | % |

| Wtd. Avg. Lease Term (2) | |

| 19.1 | | |

| 72.7 | | |

| 73.1 | | |

| 70.3 | |

| Wtd. Avg. Lease Term Adjusted (3) | |

| 19.1 | | |

| 23.7 | | |

| 22.8 | | |

| 22.8 | |

| Mortgage Debt | |

$ | - | | |

$ | 213,500 | | |

$ | 213,475 | | |

$ | 242,494 | |

| % Investment Grade (1) | |

| 0.0 | % | |

| 0.2 | % | |

| 0.4 | % | |

| 0.4 | % |

| Cash Base Rent | |

$ | 1,219 | | |

$ | 9,259 | | |

$ | 22,717 | | |

$ | 25,651 | |

| | |

| | | |

| | | |

| | | |

| | |

| Multi-Tenant | |

| | | |

| | | |

| | | |

| | |

| % of ABR (1) | |

| 9.0 | % | |

| 7.9 | % | |

| 8.7 | % | |

| 3.0 | % |

| Leased | |

| 67.4 | % | |

| 66.4 | % | |

| 53.9 | % | |

| 44.1 | % |

| Wtd. Avg. Lease Term (2) | |

| 7.1 | | |

| 7.0 | | |

| 6.9 | | |

| 3.4 | |

| Mortgage Debt | |

$ | 102,582 | | |

$ | 71,754 | | |

$ | 116,763 | | |

$ | 14,118 | |

| % Investment Grade (1) | |

| 33.2 | % | |

| 34.5 | % | |

| 19.3 | % | |

| 36.9 | % |

| Square Feet | |

| 2,396,631 | | |

| 2,259,189 | | |

| 2,414,889 | | |

| 2,301,864 | |

| Cash Base Rent | |

$ | 25,169 | | |

$ | 27,941 | | |

$ | 34,458 | | |

$ | 11,425 | |

| | |

| | | |

| | | |

| | | |

| | |

| Retail/Specialty | |

| | | |

| | | |

| | | |

| | |

| % of ABR (1) | |

| 3.3 | % | |

| 2.7 | % | |

| 2.6 | % | |

| 3.0 | % |

| LTL (5) | |

| 15.3 | % | |

| 21.0 | % | |

| 28.1 | % | |

| 34.7 | % |

| STL (6) | |

| 84.7 | % | |

| 79.0 | % | |

| 71.9 | % | |

| 65.3 | % |

| Leased | |

| 99.3 | % | |

| 98.5 | % | |

| 94.3 | % | |

| 97.9 | % |

| Wtd. Avg. Lease Term (2) | |

| 8.0 | | |

| 7.2 | | |

| 9.1 | | |

| 8.4 | |

| Mortgage Debt | |

$ | 13,979 | | |

$ | 13,566 | | |

$ | 13,170 | | |

$ | 12,724 | |

| % Investment Grade (1) | |

| 22.0 | % | |

| 18.7 | % | |

| 22.4 | % | |

| 16.4 | % |

| Square Feet | |

| 1,755,608 | | |

| 1,489,267 | | |

| 1,447,724 | | |

| 1,395,517 | |

| Cash Base Rent | |

$ | 8,186 | | |

$ | 7,947 | | |

$ | 8,948 | | |

$ | 9,557 | |

| | |

| | | |

| | | |

| | | |

| | |

| Loans Receivable | |

$ | 72,540 | | |

$ | 99,443 | | |

$ | 105,635 | | |

$ | 95,871 | |

| Construction in progress (4) | |

$ | 71,634 | | |

$ | 78,656 | | |

$ | 121,184 | | |

$ | 103,954 | |

Footnotes

| (1) | Percentage of GAAP rent. |

| (3) | Cash basis adjusted to reflect NY land leases to the

first purchase option date. |

| (4) | Includes development classified as real estate under

construction on a consolidated basis. |

| (5) | Long-term leases ("LTL") are defined as leases

having a term of ten years or longer. |

| (6) | Short-term leases ("STL") are defined as leases

having a term of less than ten years. |

LEXINGTON REALTY TRUST

Portfolio Composition

12/31/2015

As a Percent