Free Writing Prospectus - Filing Under Securities Act Rules 163/433 (fwp)

February 12 2016 - 3:55PM

Edgar (US Regulatory)

IMAGE

OMITTEDNorth America Structured

Investments 3yr Uncapped Dual Directional Contingent

Buffered Return Enhanced Note linked to SPX/RTY IMAGE

OMITTED

The following is

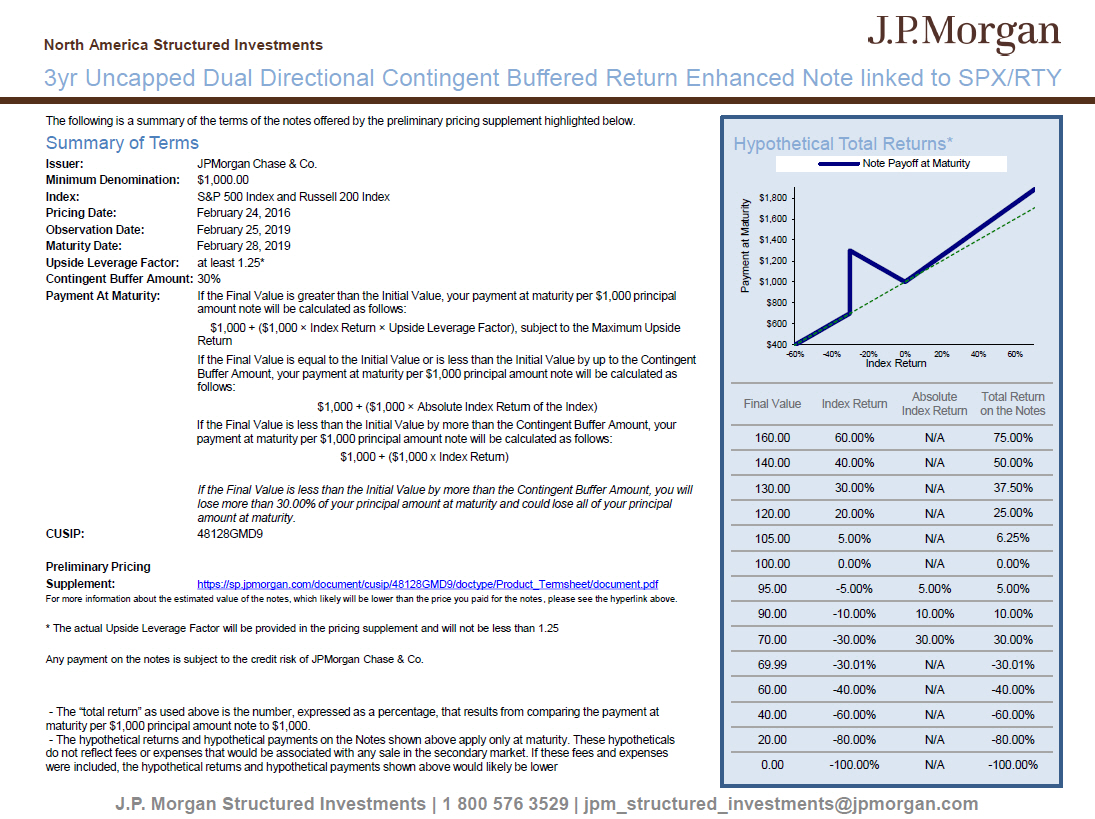

a summary of the terms of the notes offered by the preliminary pricing supplement highlighted below. Summary of Terms Issuer: JPMorgan

Chase & Co. Minimum Denomination: $1,000.00 Index: S&P 500 Index and Russell 200 Index Pricing Date: February

24, 2016 Observation Date: February 25, 2019 Maturity Date: February 28, 2019 Upside Leverage Factor: at

least 1.25* Contingent Buffer Amount: 30% Payment At Maturity: If the Final Value is greater than the Initial

Value, your payment at maturity per $1,000 principal amount note will be calculated as follows: $1,000 + ($1,000 × Index

Return × Upside Leverage Factor), subject to the Maximum Upside Return If the Final Value is equal to the Initial Value

or is less than the Initial Value by up to the Contingent Buffer Amount, your payment at maturity per $1,000 principal amount

note will be calculated as follows: $1,000 + ($1,000 × Absolute Index Return of the Index) If the Final Value is less than

the Initial Value by more than the Contingent Buffer Amount, your payment at maturity per $1,000 principal amount note will be

calculated as follows: $1,000 + ($1,000 x Index Return) If the Final Value is less than the Initial Value by more than the

Contingent Buffer Amount, you will lose more than 30.00% of your principal amount at maturity and could lose all of your

principal amount at maturity. CUSIP: 48128GMD9 Preliminary Pricing Supplement: https://sp.jpmorgan.com/document/cusip/48128GMD9/doctype/Product_Termsheet/document.pdf

For more information about the estimated value of the notes, which likely will be lower than the price you paid for the notes,

please see the hyperlink above. * The actual Upside Leverage Factor will be provided in the pricing supplement and will not be

less than 1.25 Any payment on the notes is subject to the credit risk of JPMorgan Chase & Co. The “total return”

as used above is the number, expressed as a percentage, that results from comparing the payment at maturity per $1,000 principal

amount note to $1,000. The hypothetical returns and hypothetical payments on the Notes shown above apply only at maturity. These

hypotheticals do not reflect fees or expenses that would be associated with any sale in the secondary market. If these fees and

expenses were included, the hypothetical returns and hypothetical payments shown above would likely be lower

Hypothetical Total Returns* Note Payoff at Maturity Maturity $1,800 $1,600 at $1,400 Payment $1,200 $1,000

$800 $600 $400 -60% -40%-20% 0% 20% 40% 60% Index Return Final Value Index Return Absolute Total Return Index Return

on the Notes 160.00 60.00% N/A 75.00% 140.00 40.00% N/A 50.00% 130.00 30.00% N/A 37.50% 120.00 20.00% N/A

25.00% 105.00 5.00% N/A 6.25% 100.00 0.00% N/A 0.00% 95.00 -5.00% 5.00% 5.00% 90.00 -10.00% 10.00% 10.00%

70.00 -30.00% 30.00% 30.00% 69.99 -30.01% N/A -30.01% 60.00 -40.00% N/A -40.00% 40.00 -60.00% N/A -60.00%

20.00 -80.00% N/A -80.00% 0.00 -100.00% N/A -100.00%

J.P.

Morgan Structured Investments | 1 800 576 3529 | jpm_structured_investments@jpmorgan.com

IMAGE

OMITTEDNorth America Structured Investments 3yr

Uncapped Dual Directional Contingent Buffered Return Enhanced Note linked to SPX/RTY IMAGE

OMITTED

IMAGE

OMITTEDNorth America Structured Investments 3yr

Uncapped Dual Directional Contingent Buffered Return Enhanced Note linked to SPX/RTY IMAGE

OMITTED

Selected

Risks Your investment in the notes may result in a loss. The Notes do not guarantee any return of principal. Your maximum gain

on the notes is limited by the maximum upside return if the Index Return is positive Your maximum gain on the notes if the Index

return is negative is limited by the contingent buffer amount Any payment on the notes is subject to our credit risk. Therefore

the value of the notes prior to maturity are subject to changes in the market’s view of our creditworthiness. The benefit

provided by the contingent buffer amount may terminate on the Observation Date. No interest or dividend payments, voting rights,

or ownership rights with the securities included in the Index.

Selected Risks (continued) JPMS’s estimated value will be lower

than the original issue price (price to public) of the notes. JPMS’ estimated value does not represent future values and

may differ from others’ estimates. The notes’ value which may be reflected in customer account statements may be higher

than JPMS’ then current estimated value. JPMS’ estimated value is not determined by reference to our credit spreads

for our conventional fixed rate debt. Lack of liquidity: JPMorgan Securities, LLC, acting as agent for the Issuer (and who we

refer to as JPMS), intends to offer to purchase the notes in the secondary market but is not required to do so. The price, if

any, at which JPMS will be willing to purchase notes from you in the secondary market, if at all, may result in a significant

loss of your principal. Potential conflicts: we and our affiliates play a variety of roles in connection with the issuance of

notes, including acting as calculation agent, hedging our obligations under the notes and making the assumptions to determine

the pricing of the notes and the estimated value of the notes when the terms of the notes are set. It is possible that such hedging

or other trading activities of JPMorgan or its affiliates could result in substantial returns for JPMorgan and its affiliates

while the value of the notes decline. The tax consequences of the notes may be uncertain. You should consult your tax adviser

regarding the U.S. federal income tax consequences of an investment in the notes. The risks identified above are not exhaustive.

Please see “Risk Factors” in the applicable product supplement and “Selected Risk Considerations” to the

applicable preliminary price supplement for additional information. IMAGE OMITTED

Additional

Information SEC Legend: JPMorgan Chase & Co. has filed a registration statement (including a prospectus) with the SEC for

any offering to which these materials relate. Before you invest, you should read the prospectus in that registration statement

and the other documents relating to this offering that JPMorgan Chase & Co. has filed with the SEC for more complete information

about JPMorgan Chase & Co. and this offering. You may get these documents without cost by visiting EDGAR on the SEC web site

at www.sec.gov. Alternatively, JPMorgan Chase & Co., any agent or any dealer participating in the this offering will arrange

to send you the prospectus and the prospectus supplement as well as any product supplement and preliminary pricing supplement

if you so request by calling toll-free 1-866-535-9248. IRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates

do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not

intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated

with JPMorgan Chase & Co. of any of the matters address herein or for the purpose of avoiding U.S. tax-related penalties.

Investment suitability must be determined individually for each investor, and the financial instruments described herein may not

be suitable for all investors. This information is not intended to provide and should not be relied upon as providing accounting,

legal, regulatory or tax advice. Investors should consult with their own advisors as to these matters. This material is not a

product of J.P. Morgan Research Departments. Free Writing Prospectus Filed Pursuant to Rule 433, Registration Statement No. 333-199966

J.P. Morgan Structured Investments | 1 800 576 3529 | jpm_structured_investments@jpmorgan.com

JP Morgan Chase (NYSE:JPM)

Historical Stock Chart

From Mar 2024 to Apr 2024

JP Morgan Chase (NYSE:JPM)

Historical Stock Chart

From Apr 2023 to Apr 2024