SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

Under the Securities Exchange Act of 1934

For the month of November, 2015

Commission File Number: 001-13240

Empresa Nacional de Electricidad S.A.

National

Electricity Co of Chile Inc.

(Translation of Registrant’s Name into English)

Santa Rosa 76,

Santiago, Chile

(56)

22630 9000

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F x Form

40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by

Regulation S-T Rule 101(b)(1):

Yes

¨ No x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ¨ No x

Indicate by check mark whether by furnishing the information contained in this Form, the Registrant is also

thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

Yes ¨ No x

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 13g3-2(b): N/A

Empresa Nacional de Electricidad S.A.

Santa Rosa 76

Santiago,

Chile

NOTICE OF EXTRAORDINARY SHAREHOLDERS’ MEETING

To be held on December 18, 2015

To the Holders of American Depositary Shares of Empresa Nacional de Electricidad S.A. (“ADS Holders”):

NOTICE IS HEREBY GIVEN that an Extraordinary Shareholders’ Meeting, including any adjournments or postponements thereof (the

“Meeting”), of Empresa Nacional de Electricidad S.A., a publicly-held limited liability stock company organized under the laws of the Republic of Chile (the “Company”), will be held on December 18, 2015 at 10:00 A.M., local

time, at Espacio Riesco, Avenida El Salto 5000, Huechuraba, Santiago, Chile. The purpose of the Meeting is to address the following issues:

| |

1. |

Provide shareholders with information on the proposed corporate reorganization (the “Reorganization”), which consists of (i) the spin-offs by the Company (“Spin-Off”), creating Endesa

Américas S.A. (“Endesa Américas”); of Enersis S.A. (“Enersis”) and Chilectra S.A. (“Chilectra”), in order to separate the generation and distribution businesses in Chile from their businesses outside of

Chile and (ii) the subsequent merger of the companies that will own the non-Chilean businesses. |

| |

2. |

Provide shareholders with supporting information that underlies the proposed Reorganization and that is relevant in accordance with the provisions of Official Letter No. 15,452 issued on July 20, 2015 by the

Chilean Superintendence of Securities and Insurance (Superintendencia de Valores y Seguros, or the “SVS”), which information was made available to the shareholders on November 5, 2015, consisting of: |

| |

(i) |

The Company’s consolidated financial statements as of and for the nine-months ended September 30, 2015, audited in accordance with Chilean auditing standards, which shall be used for the Spin-Off by the

Company. |

| |

(ii) |

Report of the Company’s Board of Directors on the absence of significant changes to the assets, liabilities or shareholders’ equity that have occurred after September 30, 2015. |

| |

(iii) |

Description of principal assets and liabilities assigned to Endesa Américas. |

| |

(iv) |

Pro forma combined statements of financial position as of October 1, 2015 of the Company and Endesa Américas, with attestation reports by the respective external auditors of the Company and Endesa

Américas, which contemplate, among other things, the allocation of the assets, liabilities and shareholders’ equity of the Company between the Company and Endesa Américas. |

| |

(v) |

Presentation prepared by the financial advisor appointed by the Company’s Board of Directors, Deutsche Bank Securities Inc., solely for the purposes of assisting the Company’s Board of Directors in its

consideration of the Reorganization. |

| |

(vi) |

Report of the Chilean independent expert appointed by the Company’s Board of Directors, Mr. Colin Becker, including the estimated values of the entities to be merged (the “Merger”), and the estimates

regarding the applicable share exchange ratios in the Merger, within the context of the Reorganization. |

| |

(vii) |

Report of the Chilean financial advisor appointed by Company’s Directors’ Committee, Asesorias Tyndall Limitada, with respect to its findings regarding the Reorganization. |

| |

(viii) |

Report of the Company’s Directors’ Committee, with its findings regarding the Reorganization. |

| |

(ix) |

Document describing the Reorganization and its terms and conditions. |

| |

(x) |

Determination of the number of Endesa Américas shares to be received by the Company’s shareholders. |

| |

(xi) |

Presentation of the Company’s Board of Directors regarding the purposes and expected benefits of the Reorganization, including the Spin-Off and the Merger, which shall be effected pursuant to applicable law.

|

| |

(xii) |

Resolutions adopted by the Company’s Board of Directors approving the transactions contemplated by the Reorganization subject to certain conditions. |

| |

(xiii) |

Drafts of the by-laws (estatutos) of the Company and Endesa Américas subsequent to the Spin-Off. |

| |

3. |

Approve, in accordance with the terms of Title IX of the Chilean Companies Act, Law No. 18,046 and paragraph 1 of Title IX under the Chilean

Companies Act Regulations, and subject to the conditions precedent described in No. 4 below, the proposed demerger of the Company into two companies in connection with the Spin-Off. The new company, Endesa Américas S.A. will be a

publicly held limited liability stock corporation, which |

ii

| |

will be governed by Title XII under D.L. 3500, and will be assigned the equity interests, assets and associated liabilities of the Company’s businesses outside of Chile. The Company will

distribute to its shareholders shares of Endesa Américas in proportion to their share ownership in the Company (1:1 ratio). Following the Spin-Off, the Company will retain the electricity generation businesses currently being developed in

Chile, including assets, equity interest and liabilities associated with them, as well as all other assets and liabilities not expressly assigned to Endesa Américas in the Spin-Off. |

| |

4. |

Approve that the Spin-Off shall be subject to the condition precedent that the shareholders of Enersis and Chilectra have approved the spin-offs of Enersis Chile and Chilectra Américas, respectively, and minutes

of the shareholders’ meetings reflecting such approvals have been duly recorded as a public deed and the extracts of such minutes have been duly registered and published pursuant to Chilean law. Additionally, pursuant to Articles 5 and 148 of

the Chilean Companies Act Regulations, approve that the Spin-Off shall be effective as of the first calendar day of the month following the month in which the “Public Deed on Fulfillment of the Conditions for the Spin-Off by Endesa Chile”

described in No. 5 below is granted, notwithstanding timely compliance with all of the registration and publication formalities in the relevant Commerce Registry and Diario Oficial of the excerpt of the public deed of the extraordinary

shareholders’ meeting of the Company approving the Spin-Off and the creation of Endesa Américas. |

| |

5. |

Authorize the Board of Directors of the Company to grant the necessary powers-of-attorney to execute one or more documents necessary or convenient to certify compliance with the conditions precedent to which the

Spin-Off is subject; certify the assets subject to registration that are assigned to Endesa Américas; certify any other representations that are considered necessary for these purposes; and grant a public deed, within 10 calendar days of the

date on which the last of the conditions to which the Spin-Off is subject is satisfied, representing that the conditions precedent to which the Spin-Off is subject have been satisfied. Such public deed shall be named the “Public Deed on

Fulfillment of the Conditions for the Spin-Off by Endesa Chile,” and shall be registered in the corporate record books of the Company and Endesa Américas. |

| |

6. |

Approve the reduction of authorized capital of the Company in connection with the Spin-Off and the allocation of the corporate assets of the Company between the Company and Endesa Américas. |

| |

7. |

Approve the amended and restated by-laws of the Company, which will incorporate the Spin-Off, the resulting capital reduction and other items related to the Spin-Off. |

| |

8. |

Elect an interim Board of Directors of Endesa Américas and determine its compensation, which members will serve until the first ordinary shareholders’ meeting of Endesa Américas expected to be held in

April 2016. |

| |

9. |

Approve the by-laws of Endesa Américas, which will be substantially the same as the amended and restated by-laws of the Company with certain exceptions. |

iii

| |

10. |

Approve the number of shares of Endesa Américas that the Company’s shareholders will receive in connection with the Spin-Off. |

| |

11. |

Inform shareholders of the estimated terms of the Merger. |

| |

12. |

Appoint the external auditors for Endesa Américas. |

| |

13. |

Appoint the accounts inspectors, and deputy accounts inspectors, for Endesa Américas. |

| |

14. |

Inform shareholders about the agreements with related parties (included in Title XVI of Chilean Companies Act, Law No. 18,046) regarding transactions, entered into during the time elapsed since the Company’s

last shareholders’ meeting held on April 27, 2015. |

| |

15. |

Provide shareholders with information regarding authorizations granted to KPMG Auditores Consultores Ltda., external auditors of the Company, to deliver documents and reports related to external audit services provided

to the Company, to the U.S. Public Company Accounting Oversight Board (PCAOB). |

| |

16. |

Instruct the Board of Directors of Endesa Américas to apply for the registration of Endesa Américas and its shares with the SVS and the U.S. Securities and Exchange Commission and the Chilean and U.S.

stock exchanges on which its shares are to be traded. |

| |

17. |

Instruct the Board of Directors of Endesa Américas to approve the powers-of-attorneys of Endesa Américas. |

The shareholders of the Company will also vote on all agreements necessary to carry out the Spin-Off, on the terms and conditions that the

shareholders of the Company ultimately approve at the Meeting, and will grant powers deemed necessary for effecting the Spin-Off.

The

foregoing proposals do not prevent the Meeting from exercising its full capacity to adopt, reject, or modify any of the foregoing or agree to something different as long as the matter is included in the agenda.

ADS Holders may obtain a copy of relevant documentation that explains and supports the Spin-Off at the Company’s headquarters, located in

Santa Rosa 76, 15th Floor, Santiago, Chile, commencing fifteen days prior to the Meeting. The information will also be made available on the Company’s website: www.endesa.cl.

Citibank N.A., as depositary (the “Depositary”), has fixed the close of business on November 20, 2015, as the record date for

determination of ADS Holders entitled to notice of and to instruct the Depositary how to vote at the Meeting. Accordingly, only ADS Holders of our American Depositary Receipts evidencing American Depositary Shares representing shares of common stock

of record at the close of business on that date will be entitled to notice of and to instruct the Depositary how to vote at the Meeting.

The deadline for returning your Voting Instructions to the Depositary is 10:00 A.M. E.S.T. on December 15, 2015.

iv

Your vote is important. Please sign, date and return your Voting Instructions as soon as possible

to make sure that your shares are represented at the Meeting.

By Order of the Board of Directors,

Valter Moro

Chief Executive Officer

November 20, 2015

v

INFORMATION FOR EXTRAORDINARY SHAREHOLDERS’ MEETING

TO BE HELD ON DECEMBER 18, 2015

(this “Statement”)

This Statement

and the accompanying Notice and Voting Instructions are furnished in connection with the solicitation by the Board of Directors of Empresa Nacional de Electricidad S.A. (the “Company”) of instructions for the voting of shares of common

stock underlying American Depositary Shares (“ADSs”) of the Company at the Extraordinary Shareholders’ Meeting (the “Meeting”) to be held on December 18, 2015, at 10:00 A.M., local time, at Espacio Riesco, Avenida El

Salto 5000, Huechuraba, Santiago, Chile and at any adjournment or postponement thereof.

This Statement and the accompanying Notice and

Voting Instructions are first being mailed or delivered to holders of American Depositary Receipts (“ADRs”) evidencing ADSs (“ADS Holders”) on or about November 25, 2015.

THIS STATEMENT AND SOLICITATION OF VOTING INSTRUCTIONS SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY SECURITIES, NOR SHALL

THERE BE ANY SALE OF THE SECURITIES DESCRIBED HEREIN, IN ANY JURISDICTION, INCLUDING THE UNITED STATES, IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL PRIOR TO REGISTRATION OR QUALIFICATION UNDER THE SECURITIES LAWS OF SUCH

JURISDICTION.

SOLICITATION OF VOTING INSTRUCTIONS

Voting Instructions that are properly completed, signed and received by Citibank N.A., as depositary (the “Depositary”), prior to

10:00 A.M. E.S.T. on December 15, 2015 (the “Voting Instructions Deadline”) will be voted in accordance with the instructions of the persons executing the same. The Board encourages you to instruct the Depositary as more fully

described in the Voting Instructions. Your voting instructions may be revoked at any time before they are exercised, by submitting to the Depositary written notice of revocation, submitting properly executed Voting Instructions dated as of a later

date or by withdrawing the shares underlying the ADSs and attending the Meeting and voting in person.

If the Voting Instructions are

properly executed and returned but no specific directions are made, the Depositary will vote the shares or other securities represented by the ADSs in favor all of the proposals proposed by the Board of Directors.

If no voting instructions are received by the Depositary from an ADS Holder on or before the Voting Instructions Deadline, such ADS Holder

shall be deemed, and the Depositary shall deem such ADS Holder, to have instructed the Depositary to give a discretionary proxy with full

power of substitution, to the Chairman of the Board of the Company or to a person designated by him, to vote the shares underlying the ADSs on any matters at the Meeting, and the Depositary will

give such a discretionary proxy, except that no such instruction shall be deemed and no such discretionary proxy shall be given with respect to any matter as to which (i) the Chairman of the Board directs the Depositary that he does not wish

such proxy to be given, (ii) substantial opposition exists by the ADS Holders or (iii) such matter materially and adversely affects the rights of ADS Holders.

The Depositary has fixed the close of business on November 20, 2015 as the record date for determination of ADS Holders entitled to

notice of and to instruct the Depositary how to vote at the Meeting (the “ADS Record Date”). Accordingly, only ADS Holders of record, at the close of business on the ADS Record Date, of our ADRs evidencing ADSs representing shares of

common stock will be entitled to notice of and to instruct the Depositary how to vote at the Meeting.

As of the ADS Record Date for the

Meeting, there were 8,201,754,580 shares of common stock outstanding and entitled to vote at the Meeting. Each share of common stock is entitled to one vote. As of November 18, 2015, the most recent date for which information is reasonably

available, there were 326,986,950 shares of common stock represented by ADSs. Each ADS represents 30 shares of common stock of the Company.

As of November 18, 2015: (i) Enersis S.A., a publicly-held limited liability stock company organized under the laws of the Republic

of Chile, owned 60.0% of the common stock of the Company, (ii) Administradoras de Fondos de Pensiones, Chilean private pension funds, owned 15.0% of the Company’s common stock in the aggregate; (iii) Chilean stockbrokers, mutual

funds, insurance companies, foreign equity funds, and other Chilean institutional investors collectively owned 16.5% of the Company’s common stock; (iv) ADS Holders owned 4.0% of the Company’s common stock; and (v) the remaining

4.6% of the Company’s common stock was owned by 15,928 minority shareholders.

Approval of the Spin-Off proposal as well as the

proposed amendments to the Company’s by-laws (estatutos) presented by the Board of Directors for the consideration and vote of shareholders at the Meeting require the affirmative vote of at least two-thirds of the outstanding common

stock of the Company. Approval of all other proposals presented by the Board of Directors for the consideration and vote of shareholders at the Meeting requires the affirmative vote of at least a majority of the outstanding common stock of the

Company. See “The Meeting—Votes Required.”

In order to constitute a quorum, shares of stock representing a majority of the

aggregate voting power of such shares must be present in person or represented by proxy at the Meeting.

If you have any questions regarding the

matters to be voted on at the Meeting after reading this Statement, please contact the Investor Relations team for the Company, at (+562) 2353-4682, e-mail ir.endesacl@enel.com, or the Information Agent, Georgeson S.A., at 1-800-903-2897

(Stockholders from the U.S. and Canada Call Toll-Free), and at 1-39-06-421-71-777 / Telefax at 1-39-06-452-39-163 (Stockholders from Other Countries).

2

TABLE OF CONTENTS

3

APPENDICES

4

WHERE YOU CAN FIND MORE INFORMATION

The Company files annual, quarterly and current reports and other information with the U.S. Securities and Exchange Commission (the

“SEC”). The Company’s SEC filings are available to the public from the SEC’s web site at www.sec.gov. You may also read and copy any document the Company files at the SEC’s public reference room in Washington, D.C. located

at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. You may also obtain copies of any document the Company files at prescribed rates by writing to the Public Reference Section of the SEC at that address. Please call the SEC at 1-800-SEC-0330

for further information on the public reference room. Information about the Company, including its SEC filings, is also available on the Company’s website at www.endesa.cl. Except as otherwise specifically provided, information contained on and

linked from the Company’s website is not incorporated by reference into this Statement.

The Company is “incorporating by

reference” in this Statement specified documents that it files with the SEC, which means:

| • |

|

incorporated documents are considered part of this Statement; |

| • |

|

the Company is disclosing important information to you by referring you to those documents; and |

| • |

|

information contained in documents that the Company files in the future with the SEC automatically will update and supersede earlier information contained in or incorporated by reference in this Statement (any

information so updated or superseded will not constitute a part of this Statement, except as so updated or superseded). |

The

Company incorporates by reference in this Statement the documents listed below and any documents that it files with the SEC under Section 13(a), 13(c), 14, or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange

Act”), after the date of this Statement:

| • |

|

The Company’s Annual Report on Form 20-F for the year ended December 31, 2014 (the “2014 Form 20-F”); and |

| • |

|

The Company’s Reports on Form 6-K furnished on November 6, 2015; and on November 12, 2015 (with respect to the agenda for the Meeting). |

Except as otherwise provided above, the Company is not incorporating any document or information furnished and not filed in accordance with

SEC rules. Upon written or oral request, the Company will provide you with a copy of any of the incorporated documents without charge (not including exhibits to the documents unless the exhibits are specifically incorporated by reference into the

documents). You may submit such a request for this material to Empresa Nacional de Electricidad S.A., Santa Rosa 76, 15th Floor, Santiago, Chile, Attention: Investor Relations, (+562) 2353-4682.

In accordance with Chilean laws and regulations, documents, reports and other information relating to the Reorganization have been made

publicly available to the shareholders of the Company on the Company’s website at www.endesa.cl under the heading “Corporate Reorganization.” Except as otherwise specifically provided, information contained on and linked from the

Company’s website is not incorporated by reference into this Statement.

5

FORWARD-LOOKING STATEMENTS

This Statement contains statements that are or may constitute forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933, as amended (“Securities Act”), and Section 21E of the Exchange Act. These statements appear throughout this Statement and include statements regarding the Company’s intent, belief or current expectations,

including but not limited to any statements concerning:

| • |

|

the future impact of competition and regulation; |

| • |

|

political and economic conditions in the countries in which the Company or its subsidiaries and associated companies (including Endesa Américas) operate or may operate in the future; |

| • |

|

any statements preceded by, followed by or that include the words “believes”, “expects”, “predicts”, “anticipates”, “intends”, “estimates”, “should”,

“may” or similar expressions; and |

| • |

|

other statements contained or incorporated by reference in this Statement regarding matters that are not historical facts. |

Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking

statements. Factors that could cause actual results to differ materially include, but are not limited to the following:

| • |

|

the proposed Spin-Off may affect the Company’s stock price; |

| • |

|

there may not be a liquid market for the shares of Endesa Américas; |

| • |

|

the historical performance of the non-Chilean businesses of the Company may not be representative of Endesa Américas’ performance as a separate company; |

| • |

|

Endesa Américas will be a new company that has never operated independently of the Company; |

| • |

|

Endesa Américas may face difficulty in financing its operations and capital expenditures following the Spin-Off, which could have an adverse impact on its business and results; |

| • |

|

the Merger may not be consummated; and |

| • |

|

the factors discussed in the 2014 Form 20-F under the heading “Risk Factors.” |

You

should not place undue reliance on such statements, which speak only as of the date that they were made. The Company’s independent public accountants have not examined or compiled the forward-looking statements, and, accordingly, do not provide

any assurance with respect to such statements. You should consider these cautionary statements together with any written or oral forward-looking statements that the Company may issue in the future. The Company does not undertake any obligation to

release publicly any revisions to forward-looking statements contained in this Statement to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

6

For all these forward-looking statements, the Company claims the protection of the safe harbor

for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

7

SUMMARY

The Company

The

Company’s principal businesses involve electricity generation, directly or through other companies, in Chile, Argentina, Colombia and Peru. The Company also has unconsolidated equity investments in companies engaged primarily in the electricity

generation, transmission and distribution businesses in Brazil. The Company is a publicly held limited liability stock company organized under the laws of the Republic of Chile and Enersis S.A. (“Enersis”) owns 60.0% of the Company For

more information regarding the Company and its operations, see “Item 4. Information on the Company” in the 2014 Form 20-F, which is incorporated herein by reference.

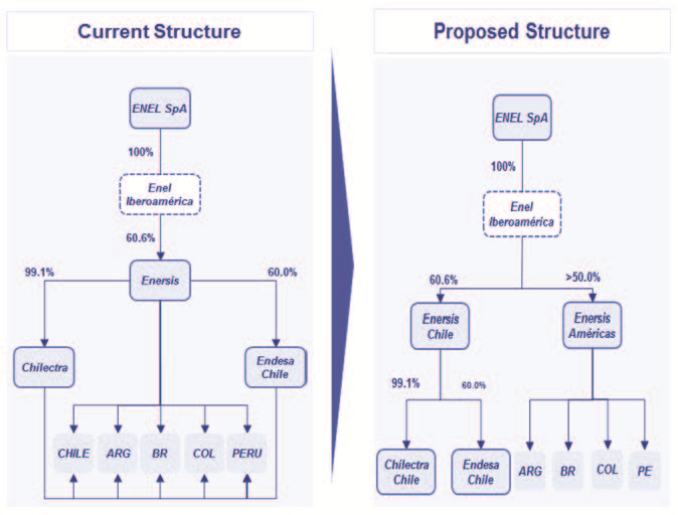

The Reorganization

The Board of Directors proposes a transaction that consists of the reorganization (the “Reorganization”) of certain companies

ultimately controlled by Enel S.p.A., an Italian electricity and generation company (“Enel”), which beneficially owns 60.6% of the Enersis. The Reorganization is intended to separate the Company’s electricity generation businesses and

assets in Chile from those in Argentina, Brazil, Colombia and Peru as shown in the chart below.

8

The Spin-Offs

First, as shown in the chart below, the Company will conduct a “división” or “demerger” under Chilean corporate law

to separate the Company into two companies. The new company, Endesa Américas S.A. (“Endesa Américas”) will be established as a separate company and will be assigned the equity interests, assets and associated liabilities of

the Company’s businesses outside of Chile (the “Separation”). Upon the completion of the Separation, Endesa Américas will register the shares of Endesa Américas with the Securities Registry of the Chilean Superintendence

of Securities and Insurance (Superintendencia de Valores y Seguros, or the “SVS”) and the SEC under applicable U.S. federal securities laws, and subject to the receipt of necessary authorizations, the completion of legal formalities

and the satisfaction of the conditions precedent, the Company will distribute to its shareholders shares of Endesa Américas in proportion to their share ownership in the Company based on a ratio of one share of Endesa Américas for each

outstanding share of the Company (the “Distribution,” and together with the Separation, the “Spin-Off”). Following the Separation, the Company will hold the Chilean businesses and assets of the Company (“Endesa Chile”).

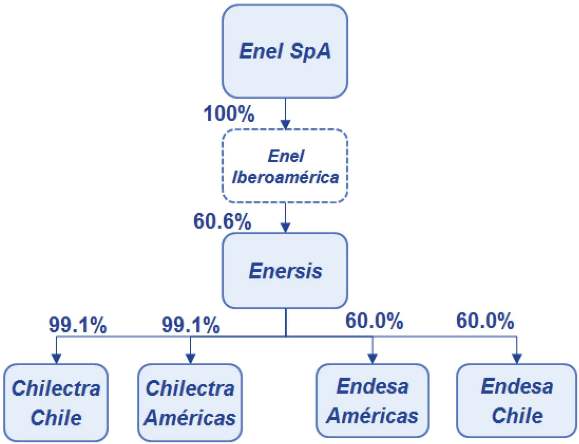

In addition to the Spin-Off, Chilectra S.A., a Chilean electricity distribution company and subsidiary of Enersis S.A.

(“Chilectra”), will also conduct a “división” or “demerger” and spin-off to its shareholders pro rata the shares of a new Chilean company, Chilectra Américas S.A. (“Chilectra

Américas”), that will hold the non-Chilean businesses and assets, comprised exclusively of Chilectra’s ownership interests in shares of companies domiciled outside of Chile (the “Chilectra Spin-Off” and together with the

Spin-Off, the “Endesa/Chilectra Spin-Offs”). In connection with the Chilectra Spin-Off, Chilectra Américas will register the shares of Chilectra Américas with the Securities Registry of the SVS and Chilectra will continue to

hold the Chilean businesses and assets of Chilectra (“Chilectra Chile”).

Enersis S.A. (“Enersis”), as the 60.0% owner

of the Company and the 99.1% owner of Chilectra, will own 60.0% of Endesa Américas and 99.1% of Chilectra Américas as a result of the Endesa/Chilectra Spin-Offs and the minority shareholders of the Company and Chilectra will own their

respective percentage interests in Endesa Américas and Chilectra Américas, respectively. The shares of Endesa Américas and Chilectra Américas will be listed and traded on the Santiago Stock Exchange, the Electronic Stock

Exchange and the Valparaíso Stock Exchange (collectively, the “Chilean Stock Exchanges”) and the American Depositary Receipts (“ADRs”) of Endesa Américas will be listed and traded on the New York Stock Exchange

(“NYSE”).

9

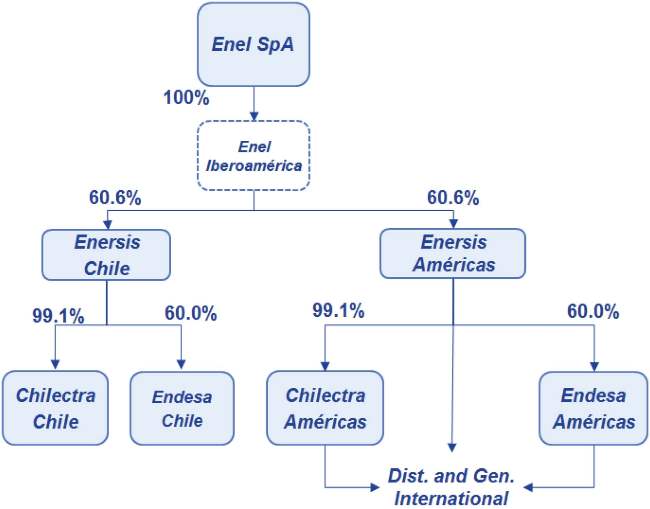

Second, following the Endesa/Chilectra Spin-Offs, Enersis will also conduct a

“división” or “demerger” and spin-off to its shareholders pro rata the shares of a new Chilean company, Enersis Chile S.A. (“Enersis Chile”) that will be assigned the Chilean businesses and assets,

including the equity interests in each of Endesa Chile and Chilectra Chile after giving effect to the Endesa/Chilectra Spin-Offs (the “Enersis Spin-Off”). Upon the effectiveness of the Enersis Spin-Off, Enersis will change its name to

Enersis Américas S.A. (“Enersis Américas”). Enersis Chile will register the shares of Enersis Chile with the Securities Registry of the SVS and the SEC under applicable U.S. federal securities laws in connection with the

Enersis Spin-Off.

Enel will beneficially own 60.6% of Enersis Chile as a result of the Enersis Spin-Off and the minority

shareholders of Enersis will own their respective percentage interest in Enersis Chile. The shares of Enersis Chile will be listed and traded on the Chilean Stock Exchanges and the ADRs of Enersis Chile will be listed and traded on the NYSE.

10

Each of the Spin-Off and the Chilectra Spin-Off is conditioned on the approval by the Enersis’

shareholders of the Enersis Spin-Off, and the Spin-Off is conditioned on the approval by the shareholders of Chilectra of the Chilectra Spin-Off. See “The Spin-Off—The Background and Description of the Spin-Off—Conditions

Precedent.”

Prior to the effectiveness of the Spin-Off and the Enersis Spin-Off, as the case may be, the Company and Enersis will

distribute to their respective shareholders an information statement with respect to the Spin-Off and the Enersis Spin-Off containing the information included in the registration statements filed with the SEC. The information statements are expected

to be distributed in the first quarter of 2016, after Endesa Américas and Enersis Chile have completed the registration process with the SEC.

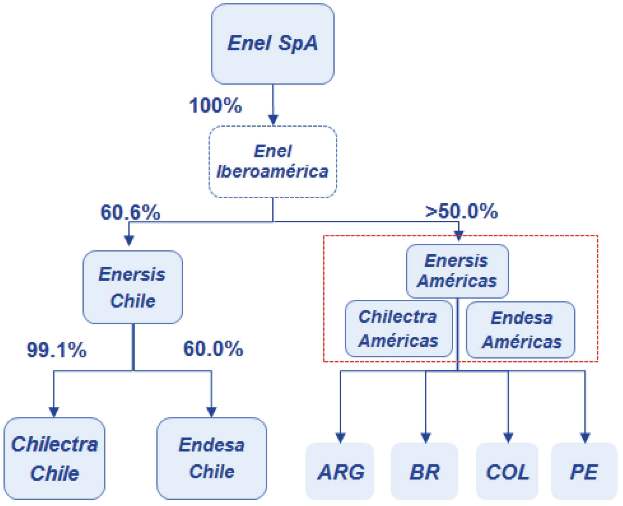

The Merger

Following the

completion of the Endesa/Chilectra Spin-Offs and the Enersis Spin-Off described above, each of Enersis Américas, Endesa Américas and Chilectra Américas (then holding the non-Chilean assets of their respective businesses), and

subject to approval by shareholders holding at least two-thirds of the outstanding shares of the relevant companies,

11

intend to merge together (the “Merger”), with Enersis Américas continuing as the surviving company under the name Enersis Américas S.A. (the “Surviving

Company”). Following completion of the Merger, the Surviving Company will continue to have its shares publicly traded and listed in Chile on the Chilean Stock Exchanges and its ADRs traded on the NYSE. In the Merger, the shares of Endesa

Américas and Chilectra Américas will be converted into shares of the Surviving Company and Endesa Américas and Chilectra Américas shares will cease trading on the Chilean Stock Exchanges and Endesa Américas ADRs

will cease to trade on the NYSE. Following the Merger, Enel is expected to continue to be the ultimate controlling shareholder, through its beneficial ownership, of the Surviving Company and the former minority shareholders of Enersis

Américas, Endesa Américas and Chilectra Américas will own the minority interest in the Surviving Company.

In connection with the Merger, each of Enersis Américas, Endesa Américas and Chilectra

Américas will hold an extraordinary shareholders’ meeting to approve the Merger. Prior to such extraordinary shareholders’ meetings, Enersis Américas will register the shares of the Surviving Company to be issued in the

Merger with the SEC under the Securities Act. In connection with their respective extraordinary shareholders’ meetings to approve the Merger, which are expected to be held in mid-2016, Enersis Américas will distribute to the shareholders

of each of Enersis Américas, Endesa Américas and, if necessary, Chilectra Américas a proxy statement/prospectus containing information about the Merger and the Surviving Company.

12

The shareholders of the Company are not being asked to vote on the Merger at this time;

there will be a separate extraordinary shareholders’ meeting to vote on the Merger at the appropriate time. The consummation of the Spin-Off, the Chilectra Spin-Off and the Enersis Spin-Off are not conditioned on shareholder approval of the

Merger.

The Matters to be Voted Upon

At the Meeting, the Board of Directors of the Company will present the following proposals to the shareholders of the Company for their

consideration and vote. At present, there is no proposed wording of the resolutions to be brought before the shareholders. It is also not a requirement of Chilean law that a specific proposal or resolution be presented to shareholders before an

extraordinary shareholders’ meeting.

The Spin-Off

The shareholders of the Company will vote to approve the Spin-Off, subject to the approval by the respective shareholders of Enersis and

Chilectra of the Enersis Spin-Off and the Chilectra Spin-Off and other conditions of the Spin-Off by the Company approved by shareholders at the Meeting. See “The Spin-Off—The Background and Description of the Spin-Off—Conditions

Precedent.” Enersis will own 60.0% of Endesa Américas as a result of the Spin-Off and the minority shareholders of the Company will own their respective percentage interest in Endesa Américas, based on the spin-off ratio of one

share of Endesa Américas for each outstanding share of the Company.

The shareholders will also vote to authorize the Board of

Directors of the Company to grant powers-of-attorney to execute necessary documents to certify compliance with the condition precedent to the Spin-Off, the assignment of the non-Chilean businesses and assets to Endesa Américas in the

demerger, and certain representations that are considered necessary and to grant a public deed regarding satisfaction of the conditions precedent to the Spin-Off.

Reduction of the Company’s Capital

In connection with the Spin-Off, the Company’s shareholders will vote to approve the reduction of authorized capital of the Company in

connection with the Spin-Off and the allocation of the corporate assets of the Company between the Company and Endesa Américas.

Amendments

to the Company’s By-Laws

In connection with the Spin-Off, the Company’s shareholders will vote to approve

amendments to the Company’s by-laws, effective with the effectiveness of the Separation, to reflect changes to the Company’s name, business purposes and authorized capital following the Separation as described in further detail under

“Amendment of By-Laws (Estatutos) of the Company.”

13

Certain Endesa Américas Corporate Governance Matters

In connection with the Spin-Off, the Company’s shareholders will vote to approve, effective with the effectiveness of the Separation, that

Endesa Américas voluntarily subject itself to the provisions in Article 50 bis of the Chilean Companies Act with respect to the election of independent directors and the creation of an independent Directors’ Committee.

Interim Board of Directors of Endesa Américas

In connection with the Spin-Off, the Company’s shareholders will vote at the Meeting to elect nine directors who will serve as the interim

Board of Directors of Endesa Américas until the first ordinary shareholders’ meeting of Endesa Américas expected to be held in April 2016. The identities of the director nominees to be voted upon at the Meeting will be made

available to the shareholders of the Company 10 days prior to the Meeting, in the case of independent director nominees, and at or prior to the Meeting, in the case of non-independent director nominees.

By-Laws of Endesa Américas

In connection with the Spin-Off, the Company’s shareholders will vote to approve the by-laws of Endesa Américas, which will

be substantially the same as the by-laws of the Company, after giving effect to the amendments to the Company’s by-laws described under “Amendment of By-Laws (Estatutos) of the Company,” except as described in further detail

under “By-Laws (Estatutos) of Endesa Américas.”

Endesa Américas Shares to be Distributed

In connection with the Spin-Off, the Company’s shareholders will vote to approve the number of shares of Endesa Américas that

shareholders of the Company will receive in the Spin-Off based on the spin-off ratio of one share of Endesa Américas for each outstanding share of the Company.

Appointment of Independent External Auditors for Endesa Américas

In connection with the Spin-Off, the Company’s shareholders will vote to approve the appointment of KPMG Auditores Consultores Ltda. as

the independent external auditor for Endesa Américas.

Appointment of Accounts Inspectors and Deputy Accounts Inspectors for Endesa

Américas

In connection with the Spin-Off, the Company’s shareholders will vote to approve the appointment of

Mr. Rolf Heller Ihle and Mr. Manuel Onetto Fuore as accounts inspectors for Endesa Américas, and Ms. Marcela Araya Nogara and Mr. Ignacio Rodríguez Llona, as deputy accounts inspectors for Endesa Américas.

14

Other Informational Matters

At the Meeting, the Board of Directors will present certain additional information on the following matters to shareholders. These matters are

reported for informational purposes only and are not subject to a vote by shareholders.

| |

• |

|

Information Required by the Administrative Rules of the Chilean Companies Act, Law 18,046, the SVS General Rule No. 30, of 1989, and Official Letter No. 15,452. In accordance with the Chilean regulation

and the Ordinary Official Letter No. 15,452 dated July 20, 2015 issued by the SVS (“Official Letter No. 15,452”), the Company is making publicly available to shareholders the following information relating to the

Reorganization, English translations of which are either attached as Appendices to this Statement or made available on the Company’s website: |

| |

• |

|

The consolidated financial statements of the Company as of and for the nine-months ended September 30, 2015 audited in accordance with Chilean auditing standards; |

| |

• |

|

The statement of the Company’s Board of Directors on the absence of significant changes to the assets, liabilities or shareholders’ equity of the Company since September 30, 2015; |

| |

• |

|

A description of principal assets and liabilities to be assigned to Endesa Américas in the Separation; |

| |

• |

|

Pro forma combined statements of financial position as of October 1, 2015 of Endesa Chile and Endesa Américas, with attestation reports by the respective external auditors of Endesa Chile and Endesa

Américas, which contemplate, among other things, the allocation of the assets, liabilities and shareholders’ equity of the Company between Endesa Chile and Endesa Américas in the Separation; |

| |

• |

|

The report of Mr. Colin Becker, the Chilean independent expert appointed by the Board of Directors of the Company to conduct an independent expert appraisal of the estimated values of the parties to the Merger and

the applicable share exchange ratios in the Merger, within the context of the Reorganization (see “Report of Chilean Independent Expert Appointed by the Board”); |

| |

• |

|

The report of Asesorias Tyndall Limitada, the Chilean financial advisor appointed by the Company’s Directors’ Committee, regarding the Reorganization; |

| |

• |

|

The report of the Directors’ Committee of the Company regarding the Reorganization; |

| |

• |

|

The presentation of the Board of Directors of the Company regarding the purposes and expected benefits of the Reorganization, including the Spin-Off and the Merger; |

15

| |

• |

|

A description of the Reorganization and its terms and conditions; |

| |

• |

|

The determination of the number of shares of Endesa Américas that the shareholders of the Company will receive; |

| |

• |

|

Resolutions adopted by the Board of Directors of the Company approving the transactions contemplated by the Reorganization subject to certain conditions; and |

| |

• |

|

Other informational documents related to the Reorganization, including the presentation prepared by Deutsche Bank Securities Inc., the financial advisor appointed by the Board of Directors of the Company, solely for the

purposes of assisting the Company’s Board of Directors in its consideration of the Reorganization. |

| |

• |

|

The Merger. In accordance with Official Letter No. 15,452, the Board of Directors is required to present to shareholders certain information regarding the proposed terms of the Merger as set forth above.

However, approval of the Merger will be the subject of a separate extraordinary shareholders’ meeting, and such approval is not a condition precedent to the Spin-Off. |

| |

• |

|

Related Party Transactions. Pursuant to Chilean law, the Board of Directors is required to present to shareholders information regarding certain transactions involving potential conflicts of interest in which

members of the Board of Directors or principal executive officers have an interest, that have been approved by the Board in the period between the last shareholders’ meeting held on April 27, 2015 and the Meeting. |

16

THE MEETING

The Meeting will take place on December 18, 2015 at 10:00 A.M., local time, at Espacio Riesco, Avenida El Salto 5000, Huechuraba,

Santiago, Chile.

Quorum

Under Chilean law, a quorum for a shareholders’ meeting is established by the presence, in person or by proxy, of shareholders

representing at least a majority of the issued shares with voting rights of a company. Enersis, which owns 60.0% of the Company’s common stock, can establish a quorum at the Meeting without the attendance of any other shareholder. Additionally,

upon the written request of the Company, the Depositary will represent all shares of the Company’s common stock underlying ADSs at any shareholders’ meeting for the sole purpose of establishing quorum at such meeting.

Votes Required

Approval of the Spin-Off proposal under “The Spin-Off” and the proposal to amend the Company’s by-laws as described under

“Amendments to the By-Laws (Estatutos) of the Company” presented by the Board of Directors for the consideration and vote of shareholders at the Meeting require the affirmative vote of at least two-thirds of the outstanding common

stock of the Company. Approval of all other proposals presented by the Board of Directors for the consideration and vote of shareholders at the Meeting requires the affirmative vote of at least a majority of the outstanding common stock of the

Company. Enersis currently owns 60.0% of the Company’s outstanding common stock, and will be entitled to vote its shares of common stock on all matters at the Meeting, and intends to vote its shares in favor of each of the proposals. As a

result, all proposals, other than the Spin-Off proposal and the proposal to amend the Company’s by-laws, will be approved without need for any additional votes of minority shareholders of the Company.

How to Vote

Under the Amended and Restated Deposit Agreement, dated as of September 30, 2010, among the Company, the Depositary and all ADS Holders

from time to time thereunder (the “Deposit Agreement”), ADS Holders have the right to instruct the Depositary how to vote their shares at the Meeting. For more information regarding the Deposit Agreement, see “Item 10. Additional

Information” in the 2014 Form 20-F, which is incorporated herein by reference.

If the Voting Instructions are properly executed and

returned but no specific directions are made, the Depositary will vote the shares or other securities represented by the ADSs in favor of the proposals proposed by the Board of Directors.

The Depositary has set November 20, 2015, as the ADS Record Date. Accordingly, only ADS Holders as of the ADS Record Date are entitled to

instruct the Depositary how to vote at the Meeting. Upon the timely receipt of voting instructions from an ADS Holder entitled to instruct the Depositary how to vote at the Meeting as explained in the attached Voting Instructions, the Depositary

will, insofar as practicable and permitted under applicable law, the provisions of the Deposit Agreement, the by-laws of the Company and the provisions of the

17

common stock of the Company, vote, or cause Banco Santander-Chile, as Custodian, to vote the shares underlying the ADS Holder’s ADSs in accordance with such voting instructions.

Additionally, ADS Holders may withdraw the shares underlying the ADSs and attend and vote at the Meeting in person. If you do not attend the Meeting or do not instruct the Depositary to vote on your behalf, the Company has the contractual right

under the Deposit Agreement to designate a person to vote your shares in such person’s sole discretion, unless (i) the Chairman of the Board directs the Depositary not to give such a proxy, (ii) substantial opposition exists by the

ADS Holders or (iii) the matters to be voted on materially and adversely affect the rights of ADS Holders.

THE FAILURE TO EXERCISE

YOUR RIGHT TO VOTE IN ONE OF THE MANNERS LISTED ABOVE MAY HAVE THE EFFECT OF PERMITTING A DESIGNEE OF THE COMPANY TO EXERCISE THE COMPANY’S CONTRACTUAL RIGHT TO EXERCISE ITS DISCRETIONARY AUTHORITY TO VOTE YOUR SHARES, DEPENDING ON WHETHER OR

NOT CERTAIN CONDITIONS EXIST.

Under the Chilean Companies Act, in connection with shareholder approvals of certain matters at a meeting

of shareholders, dissenting shareholders acquire the right to withdraw from the Company and may compel the Company to repurchase their shares (derecho a retiro), subject to the fulfillment of certain terms and conditions. The proposed

Spin-Off is not a matter which would give rise to withdrawal rights.

18

THE SPIN-OFF

Background and Description of the Spin-Off

Overview

The Spin-Off will

establish Endesa Américas as a new Chilean corporation, independent of the Company. Endesa Américas will be a holding company that will hold the non-Chilean electricity generation business and assets formerly held by the Company.

Neither Endesa Chile nor Endesa Américas will own any capital stock of the other following the Spin-Off. The relationships between the two companies will be limited to:

| |

• |

|

Agreements relating to the implementation of the Spin-Off; and |

| |

• |

|

Intercompany agreements for staff and support services, among others. |

Endesa Chile and Endesa

Américas may also have certain intercompany financial arrangements with Enersis Chile, Enersis Américas, Chilectra Chile and Chilectra Américas following the Spin-Off, the Chilectra Spin-Off and the Enersis Spin-Off. See

“—Intercompany Arrangements.”

Establishing two separate, publicly traded companies through the Spin-Off is expected to

create a more efficient and focused structure that maximizes value creation for both Endesa Chile and Endesa Américas, which benefits include:

| |

• |

|

Better alignment of interests; |

| |

• |

|

Elimination of potential conflicts of interest and redundancies, resulting in a more agile and efficient decision-making process, allowing the companies to better tailor business strategies; and |

| |

• |

|

Reduction of cross shareholdings, by reducing minority interest, and improvement of visibility, which is expected to increase the cash flow retention due to lower leakage. |

Description of the Spin-Off

The Spin-Off will be implemented using a procedure under Chilean corporate law called división or “demerger.” In

a división, an existing company is divided, creating a new company to which specified assets and liabilities are assigned. The shares of the new company are issued to the shareholders of the existing company, pro rata in proportion to

their share ownership in the existing company.

The Spin-Off will be presented to the shareholders of the Company for approval at

the extraordinary shareholders’ meeting. Upon approval of the Spin-Off, holders of the Company’s common stock (“Company Shares”) will have the right to receive one share of common stock of Endesa Américas (“Endesa

Américas Shares”) for each Company Share. See “—Description of Distribution—Distribution of Endesa Américas Shares.”

19

Following the approval of the Spin-Off by the shareholders of the Company at the extraordinary

shareholders’ meeting (the date of such approval, the “Approval Date”), subject to the receipt of necessary authorizations, the completion of legal formalities and the satisfaction of the conditions precedent, the following actions

will occur:

| |

• |

|

Endesa Américas will be established as a separate company, with a fully independent legal existence and full capacity to own and dispose of its assets. Its initial interim Board of Directors will be elected at

the Meeting to serve until the first annual ordinary shareholders’ meeting of Endesa Américas expected to be held in April 2016. |

| |

• |

|

Specified assets and liabilities of the Company relating to its non-Chilean businesses, including the shares of specified subsidiaries and jointly controlled entities, will be transferred to Endesa Américas. All

of the non-Chilean businesses to be conveyed to Endesa Américas are conducted by separate operating entities, and the continuity of existence of those entities will be undisturbed by the Separation. |

| |

• |

|

Certain agreements to accomplish the separation of the Company’s business in the Spin-Off and to provide for ongoing relationships between Endesa Chile and Endesa Américas will take effect. See

“—Intercompany Arrangements.” |

Based on the unaudited pro forma condensed combined statements of financial

position prepared in connection with the Separation, the Company will convey to Endesa Américas, and Endesa Américas will be formed with, assets amounting to Ch$ 3,892,030 million, liabilities amounting to Ch$

1,847,254 million and stockholders’ equity of Ch$ 2,044,776 million. These figures will be adjusted to reflect amounts as of the effective date of the Separation.

Promptly following the Approval Date, the shareholders’ resolution approving the Spin-Off from the Meeting will be notarized and

registered with the Chilean Commerce Registry (Registro de Comercio del Conservador de Bienes Raíces de Santiago) and a notice of the Separation will be published in the Diario Oficial.

The Board of Directors of the Company must grant the necessary powers-of-attorney to execute one or more documents necessary or convenient to

certify compliance with the conditions precedent to which the Spin-Off is subject, certify that the assets subject to registration are assigned to Endesa Américas, and grant the Public Deed certifying the satisfaction of the conditions

precedent for the Spin-Off (the “Public Deed”) within 10 calendar days of the satisfaction of all of the conditions precedent. The Separation will be fully effective as of the first calendar day of the month following the date on which the

Public Deed is granted. However, until the registration of the Endesa Américas Shares with the SVS and the SEC described below under “—Description of Distribution—Distribution of Endesa Américas Shares” is

completed, Endesa Américas Shares will not be delivered or traded separately.

20

Conditions Precedent

In addition to the receipt of shareholder approval at the Meeting and the completion of legal formalities, the effectiveness of the Separation

is subject to the following conditions precedent:

| |

• |

|

Shareholders of Chilectra must have approved the spin-off of Chilectra Américas at an extraordinary shareholders’ meeting of Chilectra, the minutes of such meeting must have been duly recorded as a public

deed and the extracts of such minutes must have been duly registered and published pursuant to Chilean law; and |

| |

• |

|

Shareholders of Enersis must have approved the spin-off of Enersis Chile at an extraordinary shareholders’ meeting of Enersis, the minutes of such meeting must have been duly recorded as a public deed and the

extracts of such minutes must have been duly registered and published pursuant to Chilean law. |

As described above, the

Public Deed must be executed within 10 calendar days of the satisfaction of all of the conditions precedent.

Share Capital and Capital Structure of

Endesa Américas

Immediately after the effectiveness of the Spin-Off the share capital of Endesa Américas will be Ch$

778,936,764,259. The Company and Endesa Américas will initially have the same shareholders, and they will continue to be controlled by the same group of shareholders.

Shareholder Approval

On

November 5, 2015, the Board of Directors of the Company determined that the Reorganization, including the Spin-Off and the Merger, is in the best interest of the Company, subject to the satisfaction of certain conditions established by certain

members of the Board of Directors. On November 10, 2015, the Board of Directors of the Company resolved to summon an extraordinary shareholders’ meeting to approve the Spin-Off to be held on December 18, 2015.

At the Meeting, the shareholders of the Company will vote to approve the Spin-Off, which includes the Separation establishing Endesa

Américas and allocating certain assets and liabilities of the Company relating to its non-Chilean businesses to Endesa Américas. The approval of the Spin-Off requires the affirmative vote of holders of two-thirds of the Company’s

outstanding common stock. Enersis owns 60.0% of the Company’s common stock and intends to vote all of its shares in favor of the Spin-Off at the extraordinary shareholders’ meeting.

Costs Associated with the Spin-Off

The Company will assume the notary fees, duties and other costs incurred in connection with the Spin-Off, except for those fees, duties and

other costs that by their nature are incurred by any subsidiary of the Company, which shall be assumed by that entity.

21

Third Party Approvals and Consents

With respect to any obligation of the Company that will be assigned to Endesa Américas, consent of the relevant creditor may be required

in order for Endesa Américas to succeed to the rights and obligations of the Company. In these cases, failure to obtain consent from the creditor may require that the Company remain liable for such obligation of Endesa Américas. Endesa

Américas will agree to indemnify the Company against liabilities of this kind.

Description of Distribution

Distribution of Endesa Américas Shares

Once the Separation is effective, Endesa Américas will apply to register the Endesa Américas Shares in the Securities

Registry of the SVS and to list the Endesa Américas Shares for trading on the Chilean Stock Exchanges. Once the SVS has authorized the registration of the shares, the Endesa Américas Shares will be distributed to their legal holders.

Distribution of shares that are not deposited with the Chilean Central Securities Depositary (DCV Registros, S.A., Depósito Central de Valores, or the “DCV”), the clearing system for securities traded on the Chilean Stock

Exchanges, will be made against the presentation of the Company Share certificates. For shares deposited with the DCV, distribution will generally be made by book-entry annotation in the shareholder list maintained by the DCV, by which holders of

outstanding Company Shares will receive one Endesa Américas Share for each Company Share.

Holders of Company Shares as of

a specified record date, referred to as the Share Record Date, will receive Endesa Américas Shares on the “Share Distribution Date.” The Company will advise shareholders at a later time of the Share Record Date and the Share

Distribution Date. The Share Distribution Date will not occur until the registration of Endesa Américas Shares under Chilean and U.S. securities laws is effective. The Company cannot be certain when this will occur, but the Company expects it

will be during the first quarter of 2016.

Following the Separation but prior to the Share Distribution Date, there will be no separate

certificates for Endesa Américas Shares, and the right to receive Endesa Américas Shares will trade and be transferred together with Company Shares. Investors will not be able to buy or otherwise acquire, or sell or otherwise transfer

or deliver, Company Shares or Endesa Américas Shares separately.

After the Spin-Off has become effective, distribution to

shareholders of the Company will take place on the Share Distribution Date in the following manner:

| |

• |

|

Each holder of Company Shares will receive one Endesa Américas Share for each Company Share held; and |

| |

• |

|

Holders of Company Shares will continue to own the same number of Company Shares. |

Beginning

on the Share Distribution Date, the Company expects that:

| |

• |

|

Endesa Américas Shares will commence trading on the Chilean Stock Exchanges; |

22

| |

• |

|

Company Shares will trade on the Chilean Stock Exchanges separately from Endesa Américas Shares; and |

| |

• |

|

Shareholders will be able to trade Company Shares and Endesa Américas Shares separately. |

Distribution of Endesa Américas ADSs

In connection with the Spin-Off, Endesa Américas will file a registration statement (the “Spin-Off Registration Statement”)

with the SEC to register the Endesa Américas Shares under the Exchange Act. As of the date of this Statement, the Spin-Off Registration Statement has not yet been filed with the SEC. After the Spin-Off Registration Statement is filed, it will

be subject to review and comment by the SEC and amendment before it is declared effective by the SEC.

Upon the completion of the

Spin-Off, each American Depositary Share (“ADS”) of the Company (“Company ADS”) will represent, in addition to 30 Company Shares, the right to receive 30 Endesa Américas Shares. Endesa Américas will arrange with a

U.S. depositary bank to issue ADSs of Endesa Américas (“Endesa Américas ADSs”), each representing 30 Endesa Américas Shares. Applications will be made to list the Endesa Américas ADSs on the NYSE.

On a date, referred to as the “ADS Distribution Date,” as promptly as practicable after the Share Distribution Date, each record

holder of Company ADSs as of a specified date, referred to as the “ADS Record Date,” will receive one Endesa Américas ADS for each Company ADS.

Endesa Américas ADSs will be issued and distributed to each record holder of Company ADSs at the close of business (New York time) on

the ADS Record Date. The Company expects that the Depositary of the Company ADSs will announce the ADS Record Date and the ADS Distribution Date on or about the same date on which the Company announces the Share Record Date and the Share

Distribution Date, although no assurances can be given that such an announcement will be made by such date.

Persons holding Company ADSs

through the facilities of The Depository Trust Company, or DTC, will receive the distribution of Endesa Américas ADSs by book entry only, through the facilities of DTC. Persons holding Company ADSs directly will receive the distribution of

Endesa Américas ADSs in the form of certificated American Depositary Receipts, representing Endesa Américas ADSs. These ADRs will be sent to direct holders of Company ADSs on or as soon as practicable after the ADS Distribution Date.

Persons holding Company ADSs through a broker or other securities intermediary should consult such broker or other securities intermediary concerning distribution of the Endesa Américas ADSs.

Beginning on the ADS Distribution Date, the Company expects that:

| |

• |

|

Endesa Américas ADSs will commence trading on the NYSE; |

| |

• |

|

Company ADSs will trade on the NYSE separately from the Endesa Américas ADSs; and |

| |

• |

|

ADS holders will be able to trade Company ADSs and Endesa Américas ADSs separately. |

23

Intercompany Arrangements

Immediately after the Spin-Off, Endesa Chile will not own any Endesa Américas Shares or Endesa Américas ADSs and Endesa

Américas will not own any Company Shares or Company ADSs. Under Chilean law, Endesa Chile will remain jointly and severally liable for the obligations of the Company assumed by Endesa Américas pursuant to the Spin-Off. Such liability,

however, will not extend to any obligation to a person or entity that has given its express consent relieving Endesa Chile of such liability and approving the Spin-Off.

Following the Spin-Off, there will be a variety of contractual relationships between Endesa Chile and Endesa Américas, both to

accomplish the Spin-Off and to provide for ongoing relationships. These will be fully described in the Spin-Off Registration Statement. They fall into two broad categories:

Arrangements Related to the Approval of the Spin-Off. The separation of the two companies and the transfer of certain assets and

liabilities of the Company to Endesa Américas will be effected by the action of the shareholders of the Company at the Meeting.

Intercompany Services. Endesa Chile and Endesa Américas will enter into intercompany agreements under which Endesa Chile will

provide a variety of services to Endesa Américas. These services will include certain legal, financial, accounting, investor relations, data processing and other corporate support and administrative services. They will generally be provided

at cost plus a specified percentage.

In addition, following the Spin-Off, the Chilectra Spin-Off and the Enersis Spin-Off, Endesa

Chile and Endesa Américas may also have certain intercompany financial arrangements with Enersis Chile, Enersis Américas, Chilectra Chile and Chilectra Américas.

Risk Factors Relating to the Spin-Off

Certain risks relating to the Spin-Off are described below. You should carefully consider and evaluate them before you submit your vote.

The proposed Spin-Off may affect the Company’s stock price and there may not be a liquid market for the shares and ADSs of Endesa

Chile after the Spin-Off.

Immediately following the Spin-Off, substantially all of the Company’s operations will be conducted

in Chile, which could increase the business risk profile, be perceived to limit the diversification of the Company’s businesses and its growth potential and thus could cause the market price of the shares and ADSs of the continuing company,

Endesa Chile, to decline. In addition, it is possible that the future trading of the shares and ADSs of Endesa Chile will be less liquid than those of the Company before the Spin-Off, and the combined market values of the shares of Endesa Chile and

Endesa Américas may be less than, equal to or greater than the market value of Company Shares before the Spin-Off.

24

There may not be a liquid market for the shares of Endesa Américas.

There is currently no public market for the Endesa Américas Shares. It is expected that the Endesa Américas Shares will be listed

on the Chilean Stock Exchanges and the Endesa Américas ADSs will be listed on the NYSE after the effectiveness of the Spin-Off. There can be no assurance as to the liquidity of any markets that may develop for the Endesa Américas

Shares or Endesa Américas ADSs or the price at which the Endesa Américas Shares or Endesa Américas ADSs may trade. Also, the liquidity and the market for the Endesa Américas Shares or Endesa Américas ADSs may be

affected by a number of factors including variations in exchange and interest rates, the deterioration and volatility of the markets for similar securities and any changes in Endesa Américas’ liquidity, financial condition,

creditworthiness, results and profitability and uncertainty with respect to the consummation of the Merger. As a result, the initial trading prices of Endesa Américas Shares and Endesa Américas ADSs may not be indicative of future

trading prices. In addition, trading of Endesa Américas Shares and Endesa Américas ADSs, in the aggregate, may be significantly less liquid than trading of the Company Shares and Company ADSs before the Spin-Off.

The historical performance of the Company’s non-Chilean businesses may not be representative of Endesa Américas’

performance as a separate company.

Endesa Américas’ combined financial statements will be based on the historical

results of operations and historical bases of the assets and liabilities of the former non-Chilean businesses of the Company. Endesa Américas’ historical performance might have been different if it had been a separate, consolidated

entity during the periods presented. The pro forma financial information included in this Statement is not necessarily indicative of what Endesa Américas’ results of operations, financial position and cash flows will be in the future.

There may be changes that will occur in Endesa Américas’ cost structure, funding and operations as a result of its separation from the Company, including increased costs associated with reduced economies of scale, and increased costs

associated with being a stand-alone publicly traded company.

Endesa Américas may face difficulty in financing its operations

and capital expenditures following the Spin-Off, which could have an adverse impact on its business and results.

Endesa

Américas may need to incur debt or issue additional equity in order to fund working capital and capital expenditures or to make acquisitions and other investments following the Spin-Off. There can be no assurance that debt or equity financing

will be available to Endesa Américas on acceptable terms, if at all. As a result of the Spin-Off, it may also become more expensive for Endesa Américas to raise funds through the issuance of debt than it was prior to the consummation

of the Spin-Off. If Endesa Américas is not able to obtain sufficient financing on attractive terms, it could have a material adverse effect on its business and results of operations.

25

The Spin-Off may not be completed if certain required conditions, many of which are outside

of the Company’s control, are not satisfied.

Completion of the Spin-Off is subject to conditions, including, but not limited

to, (i) satisfaction of the conditions precedent as described in “The Spin-Off—The Background and Description of the Spin-Off—Conditions Precedent,” (ii) the receipt of certain

regulatory approvals, and (iii) the absence of any order or injunction prohibiting the consummation of the Spin-Off.

Despite its

best efforts, the Company may not be able to satisfy or receive in a timely fashion the various conditions precedent and obtain the necessary approvals, and such failure or delay in completing the Spin-Off may cause uncertainty or other negative

consequences that may materially and adversely affect the Company’s performance, financial condition, results of operations, price per share of the Company’s common stock.

The Spin-Off and the Reorganization may be subject to judicial or administrative injunctions.

Shareholders of Enersis and the Company, AFP Hábitat and AFP Capital, brought action in the Santiago Court of Appeals in order to block

the Reorganization and the matter is pending resolution. It is possible that additional actions may be brought by shareholders, bondholders, regulators or others seeking to enjoin the Spin-Off or the Reorganization. Any litigation may delay the

Spin-Off and the Reorganization, distract management, divert resources, result in negative publicity or otherwise negatively affect the Spin-Off and the Reorganization.

Endesa Américas and Endesa Chile will need to rely on intercompany arrangements with each other and other affiliates.

Substantially all of the Company’s personnel will be assigned to Endesa Chile in connection with the Spin-Off, and Endesa

Chile following the Spin-Off, will provide Endesa Américas with certain legal, financial, accounting, investor relations and other corporate support and administrative services. Furthermore, Endesa Américas and Endesa Chile may also

need to rely on certain intercompany financial arrangements with affiliates such as Enersis Chile, Enersis Américas, Chilectra Chile and Chilectra Américas. Therefore, if the Merger does not occur and Endesa Américas does not

develop its own administrative infrastructure or achieve full autonomy for some of these services or develop alternative financial arrangements, there could be a material adverse effect on its business.

The businesses and the shares and ADSs of Endesa Chile and Endesa Américas may be adversely impacted if the Merger is not

consummated.

The failure to consummate the Merger following the Spin-Off will require both Endesa Chile and Endesa Américas

to operate as separate standalone companies, which may result in significant discounts to the valuation of the shares and ADSs of both Endesa Chile and Endesa Américas. The business and the shares and ADSs of Endesa Américas may be

especially vulnerable due to, among other things, uncertainty with respect to its future and because it has never operated independently of the Company.

26

Purposes and Benefits of the Spin-Off

Under Chilean corporate law, the Company must provide shareholders and the SVS detailed information about the purposes and expected benefits of

the Reorganization, including the Spin-Off, as well as the terms and conditions thereof, which the Board of Directors of the Company took into consideration in recommending the Spin-Off to shareholders for approval.

On November 5, 2015, the Board of Directors of the Company made public a presentation on the purposes and expected benefits of the

Reorganization, including the Spin-Off and the Merger. The presentation indicated that the benefits of the Reorganization mainly involve the reduction of inefficiencies, optimization of means and resources, creation of a more efficient structure

with improved visibility and a reduced discount holding structure, decreases in costs and increases in quantified efficiencies.

An

English translation of the full text of the presentation on the purposes and expected benefits of the Reorganization is attached as Appendix A to this Statement and is incorporated herein by reference. The presentation on the purposes and expected

benefits of the Reorganization is also available on the Company’s website at www.endesa.cl in Spanish and in English.

The English translation is not to be construed as being identical in content to the Spanish documents (which will prevail in the event

of any discrepancy with the English translation).

Description of the Assets and Liabilities to be Assigned to Endesa

Américas

Under Chilean corporate law, the Company must provide to shareholders and the SVS a description of the assets and

liabilities of the Company to be assigned to Endesa Américas in the Spin-Off.

An English translation of the full text of the

description of the assets and liabilities to be assigned to Endesa Américas is attached as Appendix B to this Statement and is incorporated herein by reference. The description of the assets and liabilities to be assigned to Endesa

Américas is also available on the Company’s website at www.endesa.cl in Spanish and in English.

The English

translation is not to be construed as being identical in content to the Spanish documents (which will prevail in the event of any discrepancy with the English translation).

Audited Historical Financial Information of the Company

Under Chilean corporate law, the Company must provide shareholders and the SVS financial statements used for the Separation, which may not be

older than 90 days from the date of the Meeting. The Company has provided consolidated audited financial statements of the Company as of and for the nine-months ended September 30, 2015, which were audited under the Chilean audit standards (the

“Audited September 30, 2015 Financial Statements”).

27

In addition, under Chilean corporate law, the Company must provide shareholders and the SVS a

report of the Board of Directors of the Company on significant changes to the assets, liabilities or shareholders’ equity, if any, that have occurred subsequent to the closing date of the Company’s consolidated statements of financial

position as of September 30, 2015. If there are no such changes, the Board must expressly make a statement to that effect.

The Board

of Directors of the Company has certified that no significant changes to the assets, liabilities or shareholders’ equity have occurred subsequent to the closing date of the Company’s consolidated statements of financial position as of

September 30, 2015 (the “Board Statement on Absence of Significant Changes”).

The Audited September 30, 2015

Financial Statements and the Board Statement On Absence of Significant Changes (both as originally furnished to the Company in Spanish, and translated into English for the convenience of investors) are available on the Company’s website at

www.endesa.cl and are incorporated herein by reference.

The English translations are not to be construed as being identical

in content to the Spanish documents (which will prevail in the event of any discrepancy with the English translations).

Unaudited Pro Forma Condensed Combined Statements of Financial Position

Under Chilean corporate law, the Company must provide shareholders and the SVS pro forma statements of financial position that reflect the

allocation of the assets, liabilities and equity of the Company to Endesa Américas in the Spin-Off, including pro forma combined statements of financial position for Endesa Chile and Endesa Américas as of the day following the date of

the Audited September 30, 2015 Financial Statements. The Company has provided pro forma condensed combined statements of financial position of Endesa Chile and Endesa Américas as of October 1, 2015 (the “Unaudited Pro Forma

Condensed Combined Statements of Financial Position”).

An English translation of the full text of the Unaudited Pro Forma

Condensed Combined Statements of Financial Position is attached as Appendix C to this Statement and is incorporated herein by reference. The Unaudited Pro Forma Condensed Combined Statements of Financial Position are also available on the

Company’s website at www.endesa.cl in Spanish and in English.

The English translation is not to be construed as being

identical in content to the Spanish documents (which will prevail in the event of any discrepancy with the English translation).

28

Board Resolution

On November 5, 2015, the Board of Directors of the Company adopted resolutions regarding the Reorganization (the “Board

Resolution”). The Board Resolution memorializes the conclusion by the Board of Directors of the Company that the Reorganization is in the best interest of the Company, subject to the satisfaction of certain conditions established by certain

members of the Board of Directors. See “Board Resolution” and Appendix D for additional details.

Directors’

Committee Report

On November 4, 2015, the Directors’ Committee of the Company, an independent committee of the

Company’s Board of Directors comprised of Messrs. Enrique Cibié Bluth, Jorge Atton Palma and Felipe Lamarca Claro (the “Directors’ Committee”), issued a report to the Board of Directors with its conclusions regarding the

Reorganization in accordance with Official Letter No. 15,452 (the “Directors’ Committee Report”). See “Directors’ Committee Report” and Appendix E for additional details.

Estimated Timeline

The following is an estimated timeline of significant dates for implementation of the Spin-Off (dates are subject to change):

|

|

|

| April 28, 2015 |

|

The Company’s Board of Directors authorized analysis of the Reorganization. |

|

|