UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the

Registrant x Filed by

a Party other than the Registrant ¨

Check the appropriate box:

|

|

|

| ¨ |

|

Preliminary Proxy Statement |

|

|

| ¨ |

|

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

|

|

| ¨ |

|

Definitive Proxy Statement |

|

|

| ¨ |

|

Definitive Additional Materials |

|

|

| x |

|

Soliciting Material under §240.14a-12 |

EMC Corporation

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

|

|

|

|

|

|

|

| x |

|

No fee required. |

|

|

| ¨ |

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

|

|

|

|

|

(1) |

|

Title of each class of securities to which the transaction applies:

|

|

|

(2) |

|

Aggregate number of securities to which the transaction applies:

|

|

|

(3) |

|

Per unit price or other underlying value of the transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the

filing fee is calculated and state how it was determined):

|

|

|

(4) |

|

Proposed maximum aggregate value of the transaction:

|

|

|

(5) |

|

Total fee paid:

|

|

|

| ¨ |

|

Fee paid previously with preliminary materials. |

|

|

| ¨ |

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement

number, or the Form or Schedule and the date of its filing. |

|

|

|

|

|

(1) |

|

Amount Previously Paid:

|

|

|

(2) |

|

Form, Schedule or Registration Statement No.:

|

|

|

(3) |

|

Filing Party:

|

|

|

(4) |

|

Date Filed:

|

The following communications were posted by EMC Corporation (the “Company”) at

http://www.twitter.com and made available on the Company’s employee intranet.

Message: Independent Survey: Customers optimistic about a

combined Dell/EMC: [link to http://www.esg-global.com/briefs/dell-emc-customer-sentiment-analysis/] IMPORTANT INFO: [link to http://www.emc.com/collateral/corporation/communication-legend.pdf]

The contents of the link above are as follows:

Enterprise Strategy Group | Getting to the bigger truth.TM

ESG Brief

Dell-EMC Customer Sentiment Analysis

Date: November 2015 Authors: Steve Duplessie, Founder & Senior Analyst; John McKnight, Vice President Research & Analyst Services; Bill Lundell, Senior Research

Analyst

Abstract: ESG recently surveyed 202 senior IT decision makers at organizations that currently purchase from Dell and/or EMC Federation companies. This

research found that customers are overwhelmingly positive about the possibility of a combined Dell-EMC, with 75% of respondents indicating that they view this pending merger of tech titans as a positive development for their firm.

Introduction

Ever since the October 12 announcement that Dell and EMC had signed a

definitive agreement under which Dell would acquire the Hopkinton, MA-based technology stalwart, there has been no shortage of opinions and prognostications by industry insiders and observers—this firm included—about the relative merits of

this transaction. While that discourse has its place, this brief will leave that conjecture for another day and will instead focus on what is arguably the only question that really matters: What do customers think this merger will mean for them

To help answer this question, ESG conducted a snapshot survey of current Dell and/or EMC customers between October 26 and November 3, meaning that survey

respondents had a minimum of two weeks to learn about the details of the announcement, hear both vendors— perspectives on the merger, consider media and industry observer commentary, and begin to digest what this could ultimately mean for their

organizations. Survey respondents were primarily senior IT decision makers (C/VP/Director-level) at North American organizations that currently purchase from Dell and/or one or more EMC Federation companies or brands (i.e., EMC, VMware, RSA, VCE,

Pivotal, and Virtustream). Respondent organizations included both midmarket (100-999 employees — 32% of respondents) and enterprise (1,000 or more employees — 68% of respondents) organizations. Please see the Research

Methodology & Respondent Demographics section at the end of this brief for more details. Here’s what we found out.

Customers Are Overwhelmingly

Positive About This Deal

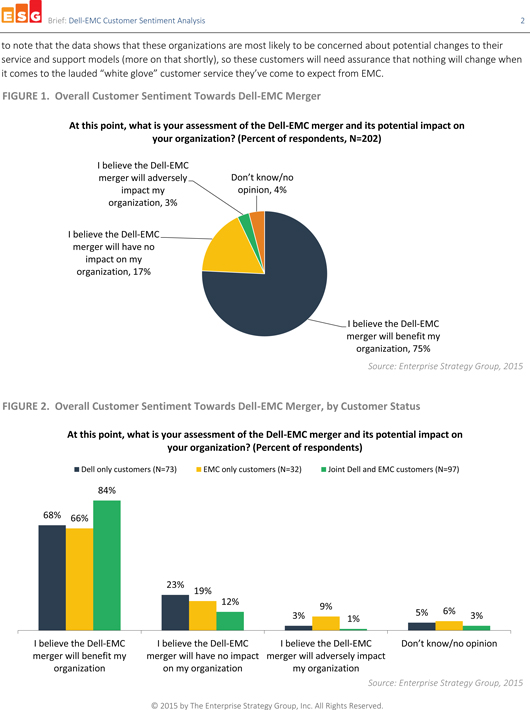

When asked to rate their current assessment of the Dell-EMC merger and what it could mean to their firm, three-quarters (75%) of

respondents indicated that they believe the merger would be beneficial to their organizations (see Figure 1). As shown in Figure 2, current joint customers of the two firms (i.e., customers that buy from both Dell and some combination of EMC

Federation companies) are most enthusiastic—84% of IT decision makers at these organizations believe that a Dell-EMC combination will be a net positive for their firms. To the extent that there is a pocket of skepticism, it lies with current

EMC-only customers. Nine percent of these organizations say they believe the merger will adversely impact their organization. While this group represents too small a sample size for statistically significant further analysis, it is instructive

© 2015 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Brief: Dell-EMC Customer Sentiment Analysis 2

to

note that the data shows that these organizations are most likely to be concerned about potential changes to their service and support models (more on that shortly), so these customers will need assurance that nothing will change when it comes to

the lauded _white glove_ customer service they_ve come to expect from EMC.

FIGURE 1. Overall Customer Sentiment Towards Dell-EMC Merger

At this point, what is your assessment of the Dell-EMC merger and its potential impact on your organization (Percent of respondents, N=202)

I believe the Dell-EMC

merger will adversely Don’t know/no

impact my opinion, 4%

organization, 3%

I believe the Dell-EMC

merger will have no

impact on my

organization, 17%

I believe the Dell-EMC

merger will benefit my

organization, 75%

Source: Enterprise Strategy Group, 2015

FIGURE 2. Overall Customer Sentiment Towards Dell-EMC Merger, by Customer Status

At this

point, what is your assessment of the Dell-EMC merger and its potential impact on your organization (Percent of respondents)

Dell only customers (N=73) EMC only

customers (N=32) Joint Dell and EMC customers (N=97)

84%

68% 66%

23%

19%

12% 9%

3% 5% 6% 3%

1%

I believe the Dell-EMC I believe the Dell-EMC I believe the Dell-EMC Don_t know/no opinion

merger will benefit my merger will have no impact merger will adversely impact

organization on my organization my organization

Source: Enterprise Strategy

Group, 2015

© 2015 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Brief: Dell-EMC Customer Sentiment Analysis

3

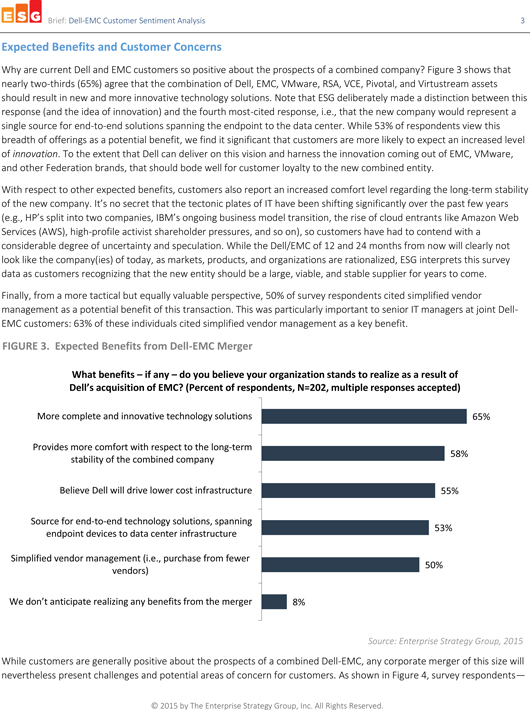

Expected Benefits and Customer Concerns

Why are current Dell and EMC

customers so positive about the prospects of a combined company? Figure 3 shows that nearly two-thirds (65%) agree that the combination of Dell, EMC, VMware, RSA, VCE, Pivotal, and Virtustream assets should result in new and more innovative

technology solutions. Note that ESG deliberately made a distinction between this response (and the idea of innovation) and the fourth most-cited response, i.e., that the new company would represent a single source for end-to-end solutions spanning

the endpoint to the data center. While 53% of respondents view this breadth of offerings as a potential benefit, we find it significant that customers are more likely to expect an increased level of innovation. To the extent that Dell can deliver on

this vision and harness the innovation coming out of EMC, VMware, and other Federation brands, that should bode well for customer loyalty to the new combined entity.

With respect to other expected benefits, customers also report an increased comfort level regarding the long-term stability of the new company. It_s no secret that

the tectonic plates of IT have been shifting significantly over the past few years (e.g., HP_s split into two companies, IBM_s ongoing business model transition, the rise of cloud entrants like Amazon Web

Services (AWS), high-profile activist shareholder pressures, and so on), so customers have had to contend with a considerable degree of uncertainty and speculation. While the

Dell/EMC of 12 and 24 months from now will clearly not look like the company(ies) of today, as markets, products, and organizations are rationalized, ESG interprets this survey data as customers recognizing that the new entity should be a large,

viable, and stable supplier for years to come.

Finally, from a more tactical but equally valuable perspective, 50% of survey respondents cited simplified vendor

management as a potential benefit of this transaction. This was particularly important to senior IT managers at joint Dell-EMC customers: 63% of these individuals cited simplified vendor management as a key benefit.

FIGURE 3. Expected Benefits from Dell-EMC Merger

What benefits _ if any _ do you believe your

organization stands to realize as a result of

Dell_s acquisition of EMC? (Percent of respondents, N=202, multiple responses accepted)

More complete and innovative technology solutions 65%

Provides more comfort with respect to

the long-term

stability of the combined company 58%

Believe Dell will drive

lower cost infrastructure 55%

Source for end-to-end technology solutions, spanning

endpoint devices to data center infrastructure 53%

Simplified vendor management (i.e.,

purchase from fewer

vendors) 50%

We don_t anticipate realizing any benefits

from the merger 8%

Source: Enterprise Strategy Group, 2015

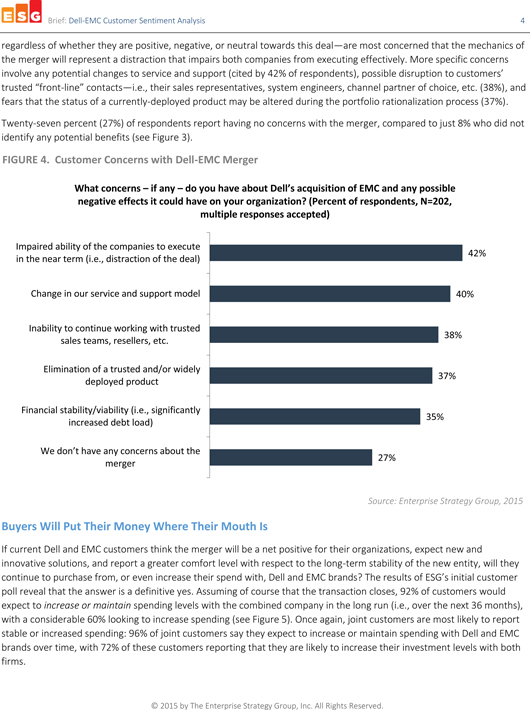

While customers

are generally positive about the prospects of a combined Dell-EMC, any corporate merger of this size will nevertheless present challenges and potential areas of concern for customers. As shown in Figure 4, survey respondents_

© 2015 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Brief: Dell-EMC Customer Sentiment Analysis

4

regardless of whether they are positive, negative, or neutral towards this deal_are most concerned that the mechanics of the merger will represent a distraction

that impairs both companies from executing effectively. More specific concerns involve any potential changes to service and support (cited by 42% of respondents), possible disruption to customers_ trusted _front-line_ contacts_i.e., their sales

representatives, system engineers, channel partner of choice, etc. (38%), and fears that the status of a currently-deployed product may be altered during the portfolio rationalization process (37%).

Twenty-seven percent (27%) of respondents report having no concerns with the merger, compared to just 8% who did not identify any potential benefits (see Figure 3).

FIGURE 4. Customer Concerns with Dell-EMC Merger

What concerns _ if any _do

you have about Dell_s acquisition of EMC and any possible negative effects it could have on your organization (Percent of respondents, N=202, multiple responses accepted)

Impaired ability of the companies to execute

in the near term (i.e., distraction of the deal)

42%

Change in our service and support model 40%

Inability to continue working

with trusted

sales teams, resellers, etc. 38%

Elimination of a trusted and/or

widely

deployed product 37%

Financial stability/viability (i.e.,

significantly

increased debt load) 35%

We don_t have any concerns about the

merger 27%

Source: Enterprise Strategy Group, 2015

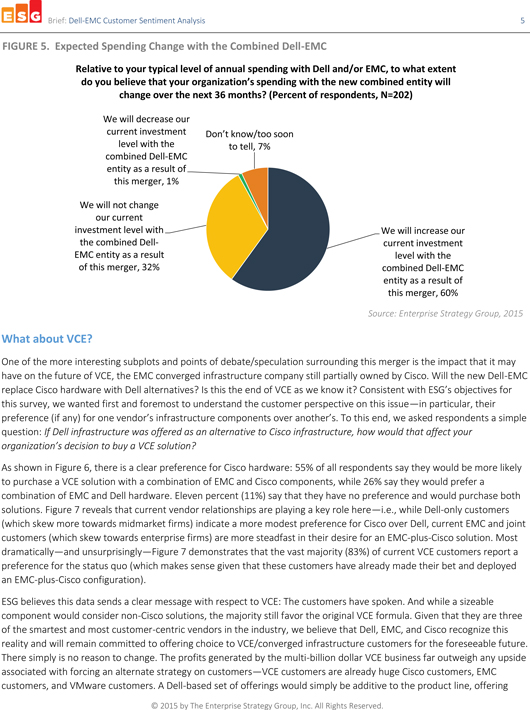

Buyers Will Put Their Money Where Their Mouth Is

If current Dell and EMC customers think the

merger will be a net positive for their organizations, expect new and innovative solutions, and report a greater comfort level with respect to the long-term stability of the new entity, will they continue to purchase from, or even increase their

spend with, Dell and EMC brands The results of ESG_s initial customer poll reveal that the answer is a definitive yes. Assuming of course that the transaction closes, 92% of customers would expect to increase or maintain spending levels with the

combined company in the long run (i.e., over the next 36 months), with a considerable 60% looking to increase spending (see Figure 5). Once again, joint customers are most likely to report stable or increased spending: 96% of joint customers say

they expect to increase or maintain spending with Dell and EMC brands over time, with 72% of these customers reporting that they are likely to increase their investment levels with both firms.

© 2015 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Brief: Dell-EMC Customer Sentiment Analysis 5

FIGURE 5. Expected Spending Change with the Combined Dell-EMC

Relative to

your typical level of annual spending with Dell and/or EMC, to what extent do you believe that your organization_s spending with the new combined entity will change over the next 36 months? (Percent of respondents, N=202)

We will decrease our

current investment Don_t know/too soon

level with the to tell, 7%

combined Dell-EMC

entity as a result of

this merger, 1%

We will not change

our current

investment level with We will increase our

the combined Dell- current investment

EMC entity as a result level with the

of this merger, 32% combined Dell-EMC

entity as a result of

this merger, 60%

Source: Enterprise Strategy Group, 2015

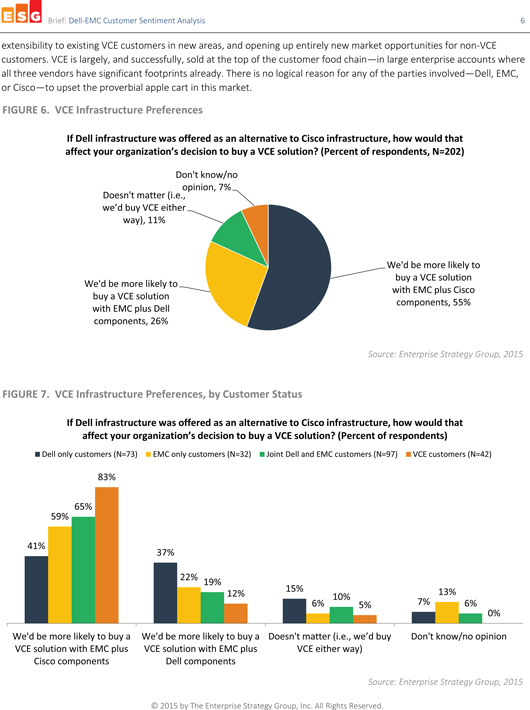

What about VCE?

One of the more interesting subplots and points of debate/speculation surrounding this merger is the impact that it may have on the future of VCE, the EMC converged infrastructure

company still partially owned by Cisco. Will the new Dell-EMC replace Cisco hardware with Dell alternatives? Is this the end of VCE as we know it? Consistent with ESG_s objectives for this survey, we wanted first and foremost to understand the

customer perspective on this issue_in particular, their preference (if any) for one vendor_s infrastructure components over another_s. To this end, we asked respondents a simple question: If Dell infrastructure was offered as an alternative to Cisco

infrastructure, how would that affect your organization_s decision to buy a VCE solution?

As shown in Figure 6, there is a clear preference for Cisco hardware: 55%

of all respondents say they would be more likely to purchase a VCE solution with a combination of EMC and Cisco components, while 26% say they would prefer a combination of EMC and Dell hardware. Eleven percent (11%) say that they have no

preference and would purchase both solutions. Figure 7 reveals that current vendor relationships are playing a key role here_i.e., while Dell-only customers (which skew more towards midmarket firms) indicate a more modest preference for Cisco over

Dell, current EMC and joint customers (which skew towards enterprise firms) are more steadfast in their desire for an EMC-plus-Cisco solution. Most dramatically_and unsurprisingly_Figure 7 demonstrates that the vast majority (83%) of current

VCE customers report a preference for the status quo (which makes sense given that these customers have already made their bet and deployed an EMC-plus-Cisco configuration).

ESG believes this data sends a clear message with respect to VCE: The customers have spoken. And while a sizeable component would consider non-Cisco solutions, the majority still

favor the original VCE formula. Given that they are three of the smartest and most customer-centric vendors in the industry, we believe that Dell, EMC, and Cisco recognize this reality and will remain committed to offering choice to VCE/converged

infrastructure customers for the foreseeable future. There simply is no reason to change. The profits generated by the multi-billion dollar VCE business far outweigh any upside associated with forcing an alternate strategy on customers_VCE customers

are already huge Cisco customers, EMC customers, and VMware customers. A Dell-based set of offerings would simply be additive to the product line, offering

©

2015 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Brief: Dell-EMC Customer Sentiment Analysis 6

extensibility to existing VCE customers in new areas, and opening up entirely new market opportunities for non-VCE customers. VCE is largely, and successfully,

sold at the top of the customer food chain_in large enterprise accounts where all three vendors have significant footprints already. There is no logical reason for any of the parties involved_Dell, EMC, or Cisco_to upset the proverbial apple cart in

this market.

FIGURE 6. VCE Infrastructure Preferences

If Dell infrastructure

was offered as an alternative to Cisco infrastructure, how would that affect your organization_s decision to buy a VCE solution? (Percent of respondents, N=202)

Don’t know/no

opinion, 7%

Doesn’t matter (i.e.,

we_d buy VCE either

way), 11%

We’d be more likely to

buy a VCE solution

We’d be more likely to

with EMC plus Cisco

buy a VCE solution

components, 55%

with EMC plus Dell

components, 26%

Source: Enterprise Strategy Group, 2015

FIGURE 7. VCE Infrastructure Preferences, by Customer Status

If Dell infrastructure was

offered as an alternative to Cisco infrastructure, how would that affect your organization_s decision to buy a VCE solution? (Percent of respondents)

Dell only

customers (N=73) EMC only customers (N=32) Joint Dell and EMC customers (N=97) VCE customers (N=42)

83%

65%

59%

41%

37%

22% 19%

12% 15% 13%

10%

6% 5% 7% 6%

0%

We’d be more likely to buy a We’d be more likely to buy a Doesn’t matter

(i.e., we_d buy Don’t know/no opinion

VCE solution with EMC plus VCE solution with EMC plus VCE either way)

Cisco components Dell components

Source: Enterprise Strategy Group, 2015

© 2015 by The Enterprise Strategy Group, Inc. All Rights Reserved.

Brief: Dell-EMC Customer Sentiment Analysis

7

The Bigger Truth

As we write this brief, we are still many months away from

Dell_s acquisition of EMC officially closing. Regulatory hurdles have to be overcome and a lot of hard work lies ahead as strategies are formulated, organizations aligned, and products rationalized. During this period, customers will undoubtedly

need lots of attention and both Dell and EMC must be proactive with constant, consistent, and clear messaging with respect to the new entity_s future plans. Nevertheless, this research data clearly indicates that_at this point_customers are

optimistic (and perhaps even enthused) about the prospect of a combined Dell/EMC. It is certainly safe to say that customers are not reporting high levels of skepticism or discouragement. The obvious but important caveats to this particular data set

are a) many of the questions are clearly predicated upon the transaction actually closing and b) this data represents the attitudes of the current Dell-EMC installed base. While retaining and growing these customers will be critical to the new

firm_s success, its aspirations will not stop there. As the new Dell-EMC looks to steal market share from incumbents such as HPE and IBM, and fend off encroachment from cloud entrants like AWS (among others), its ability to foster the levels of

interest described by respondents in this brief with these non-customers will be essential.

Research Methodology & Respondent Demographics

The data presented in this brief is based on an online survey of 202 North American (US & Canada) IT professionals conducted by ESG between 10/26/15 and 11/3/15. To

qualify for this survey, respondents were required to be IT professionals responsible for/familiar with their organization_s IT infrastructure and strategy. Respondents were also screened for IT purchase authority and/or influence. Additional

details on the respondent base are included below.

Survey respondents by title:

ESG targeted senior IT executives for this survey, although qualified IT managers and staff titles were also accepted. · 69% senior IT management (e.g.,

CIO, VP of IT, Director of IT, etc.); 24% IT management; 7% IT staff Survey respondents by company size: · 68% enterprise organizations (1,000+ employees); 32% midmarket (100-999 employees)

Survey respondents by customer status:

All respondent organizations were required to be

current customers of Dell and/or one or more EMC Federation companies or brands (i.e., EMC, VMware, RSA, VCE, Pivotal, Virtustream)

· 48% Dell and EMC

customers; 36% Dell-only customers; 16% EMC-only customers

All trademark names are property of their respective companies. Information contained in this

publication has been obtained by sources The Enterprise Strategy Group (ESG) considers to be reliable but is not warranted by ESG. This publication may contain opinions of ESG, which are subject to change. This publication is copyrighted by The

Enterprise Strategy Group, Inc. Any reproduction or redistribution of this publication, in whole or in part, whether in hard-copy format, electronically, or otherwise to persons not authorized to receive it, without the express consent of The

Enterprise Strategy Group, Inc., is in violation of U.S. copyright law and will be subject to an action for civil damages and, if applicable, criminal prosecution. Should you have any questions, please contact ESG Client Relations at 508.482.0188.

Enterprise Strategy Group is an IT analyst, research, validation, and strategy firm that provides market

intelligence and actionable insight to the global IT community.

© 2015 by The Enterprise

Strategy Group, Inc. All Rights Reserved.

www. esg-global.com contact@esg-global.com P. 508.482.0188

Disclosure Regarding Forward Looking Statements

This communication contains forward-looking information about EMC Corporation and the proposed transaction that is intended to be covered by the safe harbor

for “forward-looking statements” provided by the Private Securities Litigation Reform Act of 1995. Actual results could differ materially from those projected in the forward-looking statements as a result of certain risk factors, including

but not limited to: (i) the failure to obtain the approval of EMC shareholders in connection with the proposed transaction; (ii) the failure to consummate or delay in consummating the proposed transaction for other reasons; (iii) the

risk that a condition to closing of the proposed transaction may not be satisfied or that required financing for the proposed transaction may not be available or may be delayed; (iv) the risk that a regulatory approval that may be required for

the proposed transaction is delayed, is not obtained, or is obtained subject to conditions that are not anticipated; (v) risk as to the trading price of Class V Common Stock to be issued by Denali Holding Inc. in the proposed transaction

relative to the trading price of shares of VMware, Inc.’s common stock; (vi) the effect of the proposed transaction on VMware’s business and operating results and impact on the trading price of shares of Class V Common Stock of Denali

Holding Inc. and shares of VMware common stock; (vii) the diversion of management time on transaction-related issues; (viii) adverse changes in general economic or market conditions; (ix) delays or reductions in information technology

spending; (x) the relative and varying rates of product price and component cost declines and the volume and mixture of product and services revenues; (xi) competitive factors, including but not limited to pricing pressures and new product

introductions; (xii) component and product quality and availability; (xiii) fluctuations in VMware’s operating results and risks associated with trading of VMware common stock; (xiv) the transition to new products, the

uncertainty of customer acceptance of new product offerings and rapid technological and market change; (xv) the ability to attract and retain highly qualified employees; (xvi) insufficient, excess or obsolete inventory;

(xvii) fluctuating currency exchange rates; (xiii) threats and other disruptions to our secure data centers or networks; (xix) our ability to protect our proprietary technology; (xx) war or acts of terrorism; and (xxi) other

one-time events and other important factors disclosed previously and from time to time in EMC’s filings with the U.S. Securities and Exchange Commission (the “SEC”). Except to the extent otherwise required by federal securities law,

EMC disclaims any obligation to update any such forward-looking statements after the date of this communication.

Additional Information and Where to

Find It

This communication does not constitute an offer to sell or a solicitation of an offer to sell or a solicitation of an offer to buy any

securities or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any

such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended, and otherwise in accordance with applicable law. This communication is

being made in respect of the proposed business combination transaction between EMC Corporation and Denali Holding Inc. The proposed transaction will be submitted to the shareholders of EMC for their consideration. In connection with the issuance of

Class V Common Stock of Denali Holding Inc. in the proposed transaction, Denali Holding Inc. will file with the SEC a Registration Statement on Form S-4 that will include a preliminary proxy statement/prospectus regarding the proposed transaction

and each of Denali Holding Inc. and EMC Corporation plans to file with the SEC other documents regarding the proposed transaction. After the registration statement has been declared effective by the SEC, a definitive proxy statement/prospectus will

be mailed to each EMC shareholder entitled to vote at the special meeting in connection with the proposed transaction. INVESTORS ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS AND ANY OTHER DOCUMENTS RELATING TO THE TRANSACTION FILED WITH THE SEC

CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors may obtain copies of the proxy statement/prospectus (when available) and all other documents

filed with the SEC regarding the proposed transaction, free of charge, at the SEC’s website (http://www.sec.gov). Investors may also obtain these documents, free of charge, from EMC’s website (www.EMC.com) under the link “Investor

Relations” and then under the tab “Financials” then “SEC Filings” or by directing a request to: EMC Corporation, 176 South Street, Hopkinton, Massachusetts, Attn: Investor Relations, 866-362-6973.

Participants in the Solicitation

EMC Corporation and its

directors, executive officers and other members of management and employees may be deemed to be “participants” in the solicitation of proxies from EMC shareholders in connection with the proposed transaction. Information regarding the

persons who may, under the rules of the SEC, be deemed participants in the solicitation of EMC shareholders in connection with the proposed transaction and a description of their direct and indirect interest, by security holdings or otherwise, will

be set forth in the proxy statement/prospectus filed with the SEC in connection with the proposed transaction. You can find information about EMC’s executive officers and directors in its definitive proxy statement filed with the SEC on

March 2, 2015 and in its Annual Report on Form 10-K filed with the SEC on February 27, 2015. You can also obtain free copies of these documents from EMC using the contact information above.

Global X Funds (NYSE:EMC)

Historical Stock Chart

From Mar 2024 to Apr 2024

Global X Funds (NYSE:EMC)

Historical Stock Chart

From Apr 2023 to Apr 2024