UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE

SECURITIES EXCHANGE ACT OF 1934

For the month of

October 2015

Commission File Number: 1-9059

Barrick Gold

Corporation

(Registrant’s name)

Brookfield

Place, TD Canada Trust Tower, Suite 3700

161 Bay Street, P.O. Box 212

Toronto, Ontario M5J 2S1 Canada

(Address of principal executive offices)

Indicate by check mark whether the registrant files or

will file annual reports under cover of Form 20-F or Form 40-F.

Form

20-F ¨ Form 40-F x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation

S-T Rule 101(b)(7): ¨

INCORPORATION BY REFERENCE

This report on Form 6-K is hereby incorporated by reference into the Registration Statement on Form F-3 (File No. 333-206417) filed

with the SEC on August 14, 2015.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by

the undersigned, thereunto duly authorized.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BARRICK GOLD CORPORATION |

|

|

|

|

| Date: October 29, 2015 |

|

|

|

By: |

|

/s/ Richie Haddock |

|

|

|

|

|

|

Name: |

|

Richie Haddock |

|

|

|

|

|

|

Title: |

|

Senior Vice President and |

|

|

|

|

|

|

|

|

General Counsel |

EXHIBIT

|

|

|

| Exhibit |

|

Description of Exhibit |

|

|

| 99.1 |

|

Barrick Gold Corporation Third Quarter Report for 2015, including the Comparative Unaudited Financial Statements prepared in accordance with International Financial Reporting Standards (“IFRS”) and the notes thereto for

the three months ended September 30, 2015 and Management’s Discussion and Analysis (“MD&A”) for the same period. |

Exhibit 99.1

THIRD QUARTER REPORT 2015

All amounts

expressed in US dollars

Barrick Reports Third Quarter 2015 Results

Growing

Free Cash Flow

| |

● |

|

The company reported adjusted net earnings of $131 million ($0.11 per share)1 and a net loss of $264

million ($0.23 per share) in the third quarter. |

| |

● |

|

Third quarter adjusted EBITDA was $942 million1; EBITDA was $490 million1. |

| |

● |

|

Free cash flow was $866 million1, or $256 million excluding proceeds from the Pueblo Viejo streaming

transaction. |

| |

● |

|

Gold production in the third quarter was 1.66 million ounces at all-in sustaining costs (AISC) of $771 per ounce1 |

| |

● |

|

Full-year gold production is expected to be 6.1-6.3 million ounces. |

| |

● |

|

Full-year all-in sustaining cost guidance reduced to $830-$870 per ounce from previous range of $840-$880 per ounce. |

| |

● |

|

On track to achieve $2 billion in cash flow improvements by end of 2016. |

| |

● |

|

Total debt reduced by 15 percent year-to-date, on track to achieve $3 billion debt reduction target. |

| |

● |

|

Progressing drilling and feasibility study work to convert resources to reserves over the next five years at Cortez, Goldstrike, Lagunas Norte, Pueblo Viejo,

Turquoise Ridge and other sites. |

TORONTO,

October 28, 2015 — Barrick Gold Corporation (NYSE:ABX)(TSX:ABX) (Barrick or the “company”) today reported adjusted net earnings of $131 million ($0.11 per share) for the third quarter and a net loss of $264 million ($0.23 per

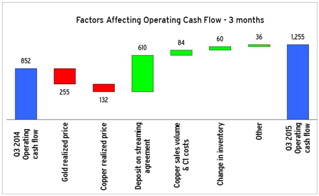

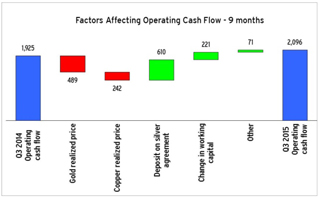

share). Third quarter adjusted EBITDA was $942 million and EBITDA was $490 million. Free cash flow was $866 million, or $256 million excluding the impact of $610 million in proceeds from the Pueblo Viejo streaming transaction2.

Production in the third quarter was in line with expectations at

1.66 million ounces of gold. All-in sustaining costs were $771 per ounce and cash costs were $570 per ounce1. Full-year 2015 gold production is expected to be 6.1-6.3 million ounces at

lower all-in sustaining costs of $830-$870 per ounce.

Our objective is to grow free cash flow per share from a portfolio of

high-quality gold assets through disciplined capital allocation and operational excellence. In support of this objective, we have returned to a leaner, decentralized operating model designed to maximize free cash flow and

1 Adjusted net earnings, adjusted net earnings per share, adjusted EBITDA, EBITDA, free cash flow, all-in sustaining costs per ounce and cash costs per ounce are non-GAAP financial performance measures

with no standardized definition under IFRS. For further information and detailed reconciliations, please see pages 52-58 of Barrick’s Third Quarter 2015 Report.

2 Please see page 23 of Barrick’s Third Quarter 2015 Report for more information about the

Pueblo Viejo streaming transaction.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

1 |

|

PRESS RELEASE |

improve execution. Clear capital allocation criteria, including a 15 percent hurdle rate for all investments, are driving greater financial rigor and stronger returns. The divestment of non-core

assets has refocused our portfolio and we have formed vital new strategic partnerships that will drive new opportunities in the future.

All of this is driving stronger performance across the business, reflected by two consecutive quarters of positive free cash flow and

improved costs. At the same time, we are strengthening our balance sheet and remain on track to reduce debt by $3 billion. This momentum will support our overriding objective of growing free cash flow per share, underpinned by a strong pipeline of

organic projects and mine site expansion opportunities in our core regions.

STRENGTHENING THE BALANCE SHEET

Earlier this year, we set a $3 billion debt reduction target for 2015. We said we would achieve this through the disciplined sale of non-core assets,

the formation of new joint ventures and partnerships, and by maximizing free cash flow from our operations. Thus far, we have completed or announced asset sales, joint ventures and partnerships valued at $2.46 billion. We have also generated $282

million in positive free cash flow in the last two quarters despite a lower gold price, reflecting the impact of our efforts to maximize free cash flow across the company. Both asset sales and cash flow improvements have been credit positive, and

have resulted in improvements to our debt-to-EBITDA ratio. Achieving our $3 billion debt reduction target will also reduce annual pre-tax interest payments by approximately $140 million.

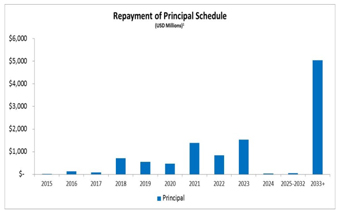

So far this year, total debt has been reduced by 15 percent, from $13.1 billion to $11.2 billion3, significantly reducing our near-term debt repayment obligations. We currently have less than $250 million in debt due before 2018 and approximately $5 billion of our $11.2 billion in outstanding

debt matures after 2032. Building on $1.9 billion in repayments already completed this year, we intend to use approximately $1 billion in proceeds from the sale of 50 percent of Zaldívar to reduce debt. The sale is expected to close in the

fourth quarter. This would bring total debt repayments to approximately $2.9 billion. We intend to use free cash flow to reach our target of $3 billion.

Assuming the completion of $3 billion in repayments, total debt will have been reduced by 23 percent, from $13.1 billion to $10.1

billion.

We also expect to announce the outcome of a process for the sale of certain non-core U.S. assets in the fourth quarter. As

we move into 2016 and beyond, we will continue to take prudent steps to strengthen our balance sheet, balancing debt repayments with investments in profitable production that will drive growth in free cash flow and EBITDA.

Our liquidity position continues to improve, with strong cash flow generation, very modest near-term debt repayment obligations, a $4

billion undrawn credit facility and $3.34 billion in cash on hand at the end of the third quarter.

3 Total debt as of October 28, 2015.

4 $1.1

billion used for debt retirement purposes subsequent to quarter end. Total includes $449 million held at Acacia and Pueblo Viejo, which may not be readily deployed outside of Acacia and/or Pueblo Viejo.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

2 |

|

PRESS RELEASE |

FINANCIAL DISCUSSION

Free cash flow increased to $866 million, or $256 million excluding the impact of $610 million in proceeds from the Pueblo Viejo streaming transaction.

This compares to $26 million in free cash flow in the second quarter of 2015. Two consecutive quarters of positive free cash flow after a prolonged period of negative free cash flow reflects our driving focus on maximizing free cash flow through

greater capital discipline, operational efficiencies and strong cost management.

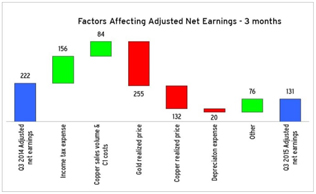

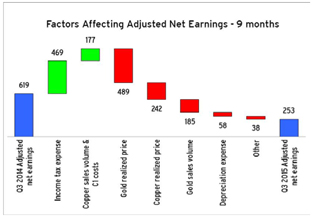

Third quarter 2015 adjusted net earnings were $131

million ($0.11 per share) compared to $222 million ($0.19 per share) in the prior year period. The net loss for the quarter was $264 million ($0.23 per share) compared to net earnings of $125 million ($0.11 per share) in the prior year quarter.

Lower adjusted net earnings reflect lower realized gold and copper prices and higher depreciation compared to the prior year period, partially offset by increased gold and copper sales. Significant adjusting items for the quarter (net of tax and

non-controlling interest effects) include:

| |

● |

|

$455 million in impairment charges primarily related to the reclassification of our Zaldívar mine as held-for-sale; and |

| |

● |

|

$29 million in costs arising from the write-down of obsolete supplies inventory; partially offset by |

| |

● |

|

$52 million of gains related to the sale of our Cowal mine and 50 percent of our interest in the Porgera mine; and |

| |

● |

|

$45 million in unrealized foreign currency translation gains. |

Third quarter adjusted EBITDA was $942 million compared to $1.1 billion in the prior year period. On an unadjusted basis, EBITDA was

$490 million for the third quarter compared to $1.0 billion in the prior year period. Operating cash flow was $1.26 billion compared to $852 million in the prior year period. Higher operating cash flow in the quarter reflects the impact of $610

million in proceeds from the Pueblo Viejo streaming transaction.

OPERATING HIGHLIGHTS AND GUIDANCE

Barrick’s operations continued to perform in line with expectations for the year, meeting cost and production targets for the third quarter while

generating stronger free cash flow. We have tightened our gold production guidance range for 2015, from 6.1-6.4 million ounces to 6.1-6.3 million ounces, reflecting lower anticipated gold production from Acacia Mining plc.

All-in sustaining cost guidance for the year has been reduced to $830-$870 per ounce from the previous range of $840-$880 per ounce.

Average all-in sustaining costs for our five core mines are now expected to be $700-$725 per ounce in 2015, down from $725-$775 per ounce at the start of this year. These mines are expected to account for about 75 percent of free cash flow from

operations and 60-65 percent of production in 2015.

Fourth quarter all-in sustaining costs are now expected to be similar to the

third quarter while production is expected to be slightly higher, primarily driven by the impact of higher sustaining capital expenditures offset by higher production at Cortez, Pueblo Viejo, Lagunas Norte and

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

3 |

|

PRESS RELEASE |

Veladero. We expect significantly higher depreciation in the fourth quarter, primarily related to a drawdown in inventory stockpiles at Cortez, Lagunas Norte and Goldstrike and higher sales

volumes at Pueblo Viejo.

Total copper guidance for 2015 remains unchanged at 480-520 million pounds. Full-year C1 cash costs

are now expected to be $1.60-$1.85 per pound5, down from $1.75-$2.00 per pound, driven by currency impacts and improved costs at Lumwana.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| Gold |

|

Third Quarter

2015 |

|

|

Current

2015 Guidance |

|

|

Original

2015 Guidance |

|

|

|

| |

|

|

|

|

|

| Production (000s of ounces)6 |

|

|

1,663 |

|

|

|

6,100-6,3007 |

|

|

|

6,200-6,600 |

|

|

|

|

|

|

|

|

| AISC ($ per ounce) |

|

|

771 |

|

|

|

830-870 |

|

|

|

860-895 |

|

|

|

|

|

|

|

|

| Cash costs ($ per ounce) |

|

|

570 |

|

|

|

600-625 |

|

|

|

600-640 |

|

|

|

|

|

|

|

|

| Copper |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

| Production (millions of pounds) |

|

|

140 |

|

|

|

480-520 |

|

|

|

310-340 |

|

|

|

|

|

|

|

|

| C1 cash costs ($ per pound) |

|

|

1.53 |

|

|

|

1.60-1.85 |

|

|

|

1.75-2.00 |

|

|

|

| |

|

|

|

|

|

| Total Capital Expenditures ($ millions)8 |

|

|

384 |

|

|

|

~1,700 |

|

|

|

1,900-2,200 |

|

|

|

| |

Cortez

The Cortez mine

produced 321,000 ounces at all-in sustaining costs of $501 per ounce in the third quarter. Production benefited from higher open pit tonnage and improved underground productivity through the implementation of short interval controls, an initiative

identified as part of our Value Realization review for Cortez. Higher production, lower operating costs and lower sustaining capital drove improved all-in sustaining costs. Production in 2015 is now forecast to be 900,000-950,000 ounces at all-in

sustaining costs of $675-$725 per ounce. Fourth quarter production at Cortez is expected to be slightly higher than the third quarter, at higher costs.

A prefeasibility study for expanded underground mining in an area known as Deep South below currently permitted levels will be completed

in late 2015 and results are expected to be disclosed with the company’s fourth quarter results. Our Value Realization review at Cortez also identified long-hole stoping as the preferred mining method for the deposit, as compared to the

cut-and-fill method previously contemplated for the underground expansion, which could improve the economics of the project. Mineralization in this zone is primarily oxide and higher grade compared to the current underground mine, which is sulfide

in nature. The limits of the Lower Zone have not yet been defined, and drilling has indicated the potential for new targets at depth.

With a 382-square-mile land package, Cortez remains a highly prospective district for Barrick.

5 C1 cash costs per pound is a non-GAAP financial performance measure. See pages 52-58 of

Barrick’s Third Quarter 2015 Report.

6 Barrick’s share.

7 Guidance reflects lower expected production from Acacia.

8 Barrick’s share on a 100 percent accrued basis.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

4 |

|

PRESS RELEASE |

Goldstrike

The

Goldstrike mine contributed 328,000 ounces in the third quarter in line with plan, while all-in sustaining costs of $558 per ounce were better than expected due to lower operating costs and lower sustaining capital. Our innovative thiosulfate (TCM)

circuit achieved commercial production in the third quarter, coming in at a capital cost of $610 million. We expect to complete the ramp up of the TCM circuit in the first half of 2016. Goldstrike’s production for 2015 is forecast to be

1.00-1.10 million ounces at improved all-in sustaining costs of $650-$700 per ounce. Fourth quarter production is expected to be similar to the third quarter, at slightly higher costs.

Exploration at Goldstrike is focused on the underground mine where good potential exists at depth, and we plan to accelerate near-mine

development in 2016. During the quarter, we began development of new areas below existing workings at Meikle and Rodeo in order to access deeper reserves which are expected to come into production at the end of 2016. This work will also open up new

drilling platforms to better define future potential in these areas.

Pueblo Viejo (60 percent)

Barrick’s 60 percent share of production from Pueblo Viejo for the third quarter was 172,000 ounces at all-in sustaining costs of $554 per ounce.

Production was slightly below plan due to lower gold grades and recoveries from a higher proportion of carbonaceous ore. All-in sustaining costs were impacted by lower silver recoveries associated with a combination of scheduled autoclave

maintenance in September, lime boil limitations and unscheduled maintenance on the limestone grinding circuit. Modifications to the lime boil are underway, including the addition of two lime boil tanks which will be operational in November. These

additional tanks are expected to improve silver recoveries to the targeted 80 percent level from around 60 percent currently. We continue to forecast attributable production of 625,000-675,000 ounces at all-in sustaining costs of $540-$590 per ounce

in 2015. Production is expected to be higher and costs lower in the fourth quarter compared to the third quarter on higher grades, improved recoveries and better autoclave availability.

At the end of 2014, Pueblo Viejo had approximately six million ounces of gold and 37 million ounces of silver in the measured and

indicated resource category (Barrick’s 60 percent share)9. A significant portion of these resources are not currently included in reserves due to tailings storage constraints. We have

completed a preliminary economic assessment on a plan to remove these constraints to tailings capacity, which if implemented could significantly extend the life of the mine. We expect to complete further engineering work and commission a

prefeasibility study in the second half of 2016 to refine the technical and financial analysis for the increase in tailings storage capacity and to confirm whether the measured and indicated resources described above can be brought into reserves.

9 Estimated in accordance with National Instrument 43-101 as required by Canadian securities

regulatory authorities. For a breakdown and additional detail on tonnes, grade and ounces, see pages 26-33 of Barrick’s 2014 Form 40-F/Annual Information Form.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

5 |

|

PRESS RELEASE |

Lagunas Norte

The Lagunas Norte mine contributed 108,000 ounces at all-in sustaining costs of $581 per ounce in the third quarter, in line with expectations.

Production in 2015 is now anticipated to be 550,000–590,000 ounces at improved all-in sustaining costs of $550-$600 per ounce, with stronger production expected in the fourth quarter driven by improved performance at the Phase Five leach pad.

Fourth quarter all-in sustaining costs are expected to be higher than the third quarter, reflecting the sale of higher cost inventory as well as increased sustaining capital for Phase Six leach pad construction. A pre-feasibility study on a plan to

extend the mine life by up to 12 years by mining nearly two million ounces of sulfide ore below the existing open pit is on schedule for completion in 2015.

Veladero

The Veladero mine produced 143,000 ounces of gold

in the third quarter at all-in sustaining costs of $914 per ounce. Production was below plan primarily due to lower grades in the Federico Phase Three pit and adverse weather events in August which impacted leach operations. All-in sustaining costs

were higher than plan on lower gold ounces sold, timing of sustaining capital and lower silver credits. The addition of reagents to the leach circuit was temporarily halted in September following a valve failure on a pipe carrying processing

solution, which led to a discharge to the environment through a diversion channel gate that was open at the time of the incident. Since the incident occurred, our first priority has been the safety of people and the environment. Water samples

analyzed by independent third-parties, including the United Nations, have confirmed that there are no risks to the health of downstream communities as a result of this incident. Restrictions on leaching activities were lifted following

implementation of additional monitoring and corrective actions. Production guidance for 2015 is unchanged at 575,000-625,000 ounces while all-in sustaining cost guidance has been narrowed to $950-$1,000 per ounce. Fourth quarter production is

expected to be higher, at lower all-in sustaining costs driven by better grades, lower capital expenditures and higher silver and inventory credits.

Turquoise

Ridge (75 percent)

The Turquoise Ridge mine contributed 55,000 ounces in the third quarter at all-in sustaining costs of $738 per ounce, in line

with expectations. The mine is forecast to produce 175,000-200,000 ounces in 2015 at improved all-in sustaining costs of $750-$800 per ounce. Detailed engineering and feasibility work on developing an additional shaft — which could bring

forward more than one million ounces of production and roughly double output to an average of 500,000 ounces per year (100 percent basis) at all-in sustaining costs of about $625-$675 per ounce — is on track to be completed by the end of the

year. Work to install additional ventilation capacity has also been initiated.

Porgera (47.5 percent)

The Porgera mine produced 134,000 ounces at all-in sustaining costs of $986 per ounce, in line with plan. Attributable production in 2015 is now expected

to be 400,000-450,000 ounces at all-in

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

6 |

|

PRESS RELEASE |

sustaining costs of $1,025-$1,125 per ounce, reflecting Barrick’s reduced interest following the sale of 50 percent of Barrick (Niugini) Ltd. to Zijin Mining. Recent drought conditions are

not expected to have a material impact on production in 2015. We expect to increase our exploration budget at Porgera in 2016 to focus on underground targets which have been identified through a new geological model.

Other Mines

Barrick’s other mines — consisting of

Bald Mountain, 50 percent of Round Mountain, Golden Sunlight, Ruby Hill, Hemlo, Cowal, KCGM and Pierina — contributed 298,000 ounces at all-in sustaining costs of $959 per ounce in the third quarter. A sale process is underway for Bald

Mountain, Round Mountain, Ruby Hill, Golden Sunlight and the Spring Valley and Hilltop properties, with strong interest received to date.

Acacia Mining (63.9

percent)

Barrick’s share of third quarter production was lower than expected at 104,000 ounces at all-in sustaining costs of $1,195 per

ounce due to temporary factors impacting output from Bulyanhulu and Buzwagi. We now expect attributable 2015 production from Acacia to be about 460,000 ounces at all-in sustaining costs of approximately $1,155 per ounce.

Copper

Copper production in the third quarter was

140 million pounds at C1 cash costs of $1.53 per pound. For 2015, copper production is anticipated to be 480-520 million pounds at lower C1 cash costs of $1.60-$1.85 per pound, reflecting currency impacts and improved costs at Lumwana.

Lumwana contributed 77 million pounds at C1 cash costs of $1.59 per pound in the third quarter, in line with expectations.

Power restrictions and potential reductions to smelter capacity in Zambia are not expected to have any material impact on Lumwana’s 2015 production guidance. Production is now anticipated to be 260-280 million pounds at lower C1 cash costs

of $1.80-$2.00 per pound in 2015, reflecting higher grades.

Production of 63 million pounds at Zaldívar at C1 cash costs

of $1.47 per pound in the third quarter was in line with plan.

At Jabal Sayid, first shipments of copper-in-concentrate continue to

be anticipated in early 2016. Once the mine reaches full production, average production in the first full five years is expected to be 100 million pounds per year.

TARGETING $2 BILLION IN CASH FLOW IMPROVEMENTS

This year,

we have taken significant actions to improve our business plans, resulting in positive free cash flow for two consecutive quarters. We remain focused on improving productivity and driving down costs to maximize free cash flow from our assets in any

gold price environment.

In support of this, we are targeting $2 billion in cash flow improvements across the company before the end

of 2016, relative to our original internal plans for 2015 and 2016. These improvements

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

7 |

|

PRESS RELEASE |

are coming from productivity gains and cost reductions across operating expenses, capital spending and corporate overhead.

While a majority of these actions will be incorporated into our 2016 plans, the initial outcomes are reflected in improvements to our

2015 guidance. Total capital expenditures for the year are expected to be 20 percent lower than 2014. Combined with reductions in corporate overhead and other operating cost savings, this has allowed us to reduce our 2015 all-in sustaining cost

guidance by about $30 per ounce since the start of year, from our original range of $860-$895 per ounce to $830-$870 per ounce in the third quarter. We are now focused on optimizing our 2016 plans, with an emphasis on operating cost and productivity

improvements.

Our temporary suspension plan for Pascua-Lama has now been approved by the mining authority in Chile. This will enable

us to complete the transition to care and maintenance, and should allow us to significantly reduce holding costs at the project in 2016. Implementation of the temporary suspension plan could require adjustments resulting from regulatory and legal

actions and weather conditions, which could increase costs associated with the plan.

CONVERTING RESOURCES TO RESERVES

At the end of 2014, Barrick had 93 million ounces of proven and probable gold reserves and 94 million ounces of measured and indicated gold

resources10. At 1.37 grams per tonne, our reserve grade is more than 50 percent higher than the senior peer average11.

For more than 20 years, Barrick has maintained an average reserve mine life of between 10 to 20 years with a track record of replacing

reserves and resources at our operations. Mine life and production rates at the majority of our mines have far surpassed initial estimates and we continue to identify excellent potential for resource conversion at many of our operations. Of our

exploration budget, 65 percent is focused on opportunities at or near our existing operations. Drilling and feasibility study work to convert resources to reserves over the next five years at Cortez, Goldstrike, Lagunas Norte, Pueblo Viejo and

Turquoise Ridge are progressing well. In addition, recent drilling at Hemlo and Porgera indicates strong potential for resource additions. We are also working to advance our Goldrush project in Nevada and drilling to define the limits of

mineralization at the Alturas project in Chile is expected to resume in the fourth quarter, following the South American winter.

An

illustration of the optionality that exists within our portfolio is the recent drill program at Hemlo. In the first quarter, Barrick completed the acquisition of surface and mineral rights adjacent to the Hemlo property in Ontario from subsidiaries

of Newmont Mining. These claims included an area of geological potential adjacent to Barrick’s existing underground workings. Barrick is currently undertaking an underground diamond drilling program in this area to evaluate its potential. To

date, drilling has encountered a number of high grade intercepts with significant potential. These results highlight the ongoing potential of mineral deposits such as the Hemlo camp, even as they become mature operations.

10 Estimated in accordance with National Instrument 43-101 as required by Canadian securities

regulatory authorities. For a breakdown and additional detail on tonnes, grade and ounces, see pages 26-33 of Barrick’s 2014 Form 40-F/Annual Information Form.

11 Senior peers include Newmont, Goldcorp, Kinross and Newcrest.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

8 |

|

PRESS RELEASE |

A detailed update on reserves and resources will be provided with the company’s fourth

quarter results in February 2016.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

9 |

|

PRESS RELEASE |

APPENDIX 1 — Detailed 2015 Operating and Capital Expenditure Guidance12

|

|

|

|

|

|

|

|

|

| |

| GOLD PRODUCTION AND COSTS |

|

|

|

|

| |

|

Production

(millions of ounces) |

|

AISC13

($ per ounce) |

|

Cash Costs14

($ per ounce) |

|

|

| |

| Cortez |

|

0.900-0.950 |

|

675-725 |

|

540-560 |

|

|

| Goldstrike |

|

1.000-1.100 |

|

650-700 |

|

525-550 |

|

|

| Pueblo Viejo (60%) |

|

0.625-0.675 |

|

540-590 |

|

450-475 |

|

|

| Lagunas Norte |

|

0.550-0.590 |

|

550-600 |

|

330-370 |

|

|

| Veladero |

|

0.575-0.625 |

|

950-1,000 |

|

550-600 |

|

|

| |

| Sub-total |

|

3.800-4.000 |

|

700-725 |

|

500-525 |

|

|

| |

| Porgera (47.5%) |

|

0.400-0.450 |

|

1,025-1,125 |

|

775-825 |

|

|

| Acacia (63.9%) |

|

~0.460 |

|

~1,155 |

|

~760 |

|

|

| KCGM (50%) |

|

0.315-0.330 |

|

850-900 |

|

725-775 |

|

|

| Cowal15 |

|

0.156 |

|

621 |

|

560 |

|

|

| Hemlo |

|

0.200-0.225 |

|

900-940 |

|

675-715 |

|

|

| Turquoise Ridge (75%) |

|

0.175-0.200 |

|

750-800 |

|

570-600 |

|

|

| Round Mountain (50%) |

|

0.170-0.190 |

|

975-1,025 |

|

725-775 |

|

|

| Bald Mountain |

|

0.170-0.195 |

|

1,125-1,175 |

|

600-640 |

|

|

| Golden Sunlight |

|

0.080-0.090 |

|

1,150-1,200 |

|

925-975 |

|

|

| |

| Total Gold |

|

6.100-6.30016 |

|

830-870 |

|

600-625 |

|

|

| |

| |

|

|

|

|

|

|

|

|

| |

| COPPER PRODUCTION AND COSTS |

|

|

|

|

| |

|

Production

(millions of pounds) |

|

C1 cash costs

($ per pound) |

|

C3 fully allocated costs17

($ per pound) |

|

|

| |

| Zaldívar (50%) |

|

210-230 |

|

1.65-1.85 |

|

1.95-2.20 |

|

|

| |

| Lumwana |

|

260-280 |

|

1.80-2.00 |

|

2.25-2.50 |

|

|

| |

| Total Copper |

|

480-520 |

|

1.60-1.85 |

|

2.10-2.35 |

|

|

| |

| |

|

|

|

|

|

|

|

|

| |

| CAPITAL EXPENDITURES |

|

|

|

|

|

|

| |

|

($ millions) |

|

|

|

|

|

|

| |

| Mine site sustaining |

|

1,400-1,50018 |

|

|

|

|

|

|

| Mine site expansion |

|

100-150 |

|

|

|

|

|

|

| Projects |

|

100-150 |

|

|

|

|

|

|

| |

| Total |

|

~1,70018 |

|

|

|

|

|

|

| |

12 2015 guidance is based on gold, copper and oil price assumptions of $1,125/oz, $2.35/lb, and $60/bbl, respectively, a AUS:US exchange rate of 0.80:1, a CAD:US exchange rate of 1.25:1, a CLP:US

exchange rate of 610:1 and a ARS:US exchange rate of 9.70:1.

13 All-in sustaining costs are calculated in

accordance with the standard published by the World Gold Council (“WGC”). See page 54 of Barrick’s Third Quarter 2015 Report for further details.

14 Cash costs reflect our equity share of unit production costs, including the impact of by-product credits, which is calculated in accordance with the standard published by the WGC. See page 54 of

Barrick’s Third Quarter 2015 Report for further details.

15 The Cowal mine was sold effective July 23,

2015.

16 Operating unit guidance ranges reflect expectations at each individual operating unit, but do not add

up to corporate-wide guidance range total.

17 C3 fully allocated costs per pound is a non-GAAP financial

performance measure. See pages 52-58 of Barrick’s Third Quarter 2015 Report.

18 We now expect minesite

sustaining capital expenditures to be in the range of $1,400-$1,500 million and total capital expenditures to be ~$1,700 million compared to our previous guidance ranges of $1,500-$1,700 million and $1,800-$2,100 million, respectively.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

10 |

|

PRESS RELEASE |

APPENDIX 2 — Economic Sensitivity Analysis

|

|

|

|

|

|

|

|

|

|

|

| |

| |

|

Hypothetical

Change |

|

Impact on AISC19

($ per ounce) |

|

EBITDA19

($ millions) |

|

FCF19

($ millions) |

|

|

| |

|

|

|

|

|

|

| Gold revenue, net of royalties |

|

+/- $100/oz |

|

n/a |

|

168 |

|

79 |

|

|

|

|

|

|

|

|

| Copper revenue, net of royalties |

|

+/- $0.50/lb |

|

n/a |

|

66 |

|

31 |

|

|

| |

|

|

|

|

|

|

| Gold all-in sustaining costs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold royalties &

production taxes |

|

$100/oz |

|

(3) |

|

5 |

|

2 |

|

|

|

|

|

|

|

|

| WTI crude oil price20, 21 |

|

$10/bbl |

|

(2) |

|

4 |

|

2 |

|

|

| |

|

|

|

|

|

|

| Australian dollar exchange

rate20,21 |

|

+10% |

|

(1) |

|

2 |

|

1 |

|

|

|

|

|

|

|

|

| Australian dollar exchange

rate20,21 |

|

-10% |

|

1 |

|

(2) |

|

(1) |

|

|

| |

|

|

|

|

|

|

| Canadian dollar exchange

rate20 |

|

+10% |

|

(2) |

|

3 |

|

1 |

|

|

|

|

|

|

|

|

| Canadian dollar exchange

rate20 |

|

-10% |

|

1 |

|

(2) |

|

(1) |

|

|

| |

| Copper C1 cash costs |

|

|

|

Impact on C1

($ per pound) |

|

|

|

|

|

|

|

|

|

|

|

|

| WTI crude oil price20,21 |

|

$10/bbl |

|

(0.01) |

|

1 |

|

0 |

|

|

|

|

|

|

|

|

| Chilean peso exchange rate20 |

|

+10% |

|

0.01 |

|

(2) |

|

(1) |

|

|

|

|

|

|

|

|

| Chilean peso exchange rate20 |

|

-10% |

|

(0.07) |

|

10 |

|

5 |

|

|

| |

19 All-in sustaining costs per ounce, EBITDA and free cash flow are non-GAAP financial performance

measures. See pages 52-58 of Barrick’s Third Quarter 2015 Report.

20 Due to our hedging

activities, which are reflected in these sensitivities, we are partially protected against changes in these factors.

21 Impact on EBITDA only reflects contracts that mature in 2015.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

11 |

|

PRESS RELEASE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Key Statistics |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Barrick Gold Corporation |

|

|

|

|

|

|

|

|

|

|

|

|

| (in United States dollars) |

|

Three months ended September 30, |

|

|

Nine months ended September 30, |

|

|

|

|

|

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| |

|

| Operating Results |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold production (thousands of ounces)1 |

|

|

1,663 |

|

|

|

1,649 |

|

|

|

4,498 |

|

|

|

4,722 |

|

| Gold sold (thousands of ounces)1 |

|

|

1,596 |

|

|

|

1,578 |

|

|

|

4,447 |

|

|

|

4,712 |

|

| Per ounce data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average spot gold price |

|

$ |

1,124 |

|

|

$ |

1,282 |

|

|

$ |

1,178 |

|

|

$ |

1,288 |

|

| Average realized gold price2 |

|

|

1,125 |

|

|

|

1,285 |

|

|

|

1,176 |

|

|

|

1,286 |

|

| Cash costs2 |

|

|

570 |

|

|

|

589 |

|

|

|

614 |

|

|

|

588 |

|

| All-in sustaining costs2 |

|

|

771 |

|

|

|

834 |

|

|

|

866 |

|

|

|

844 |

|

| All-in costs2 |

|

|

815 |

|

|

|

975 |

|

|

|

932 |

|

|

|

951 |

|

| Cash costs (on a co-product basis)2 |

|

|

592 |

|

|

|

607 |

|

|

|

639 |

|

|

|

609 |

|

| All-in sustaining costs (on a co-product basis)2 |

|

|

793 |

|

|

|

852 |

|

|

|

891 |

|

|

|

865 |

|

| All-in costs (on a co-product basis)2 |

|

|

837 |

|

|

|

993 |

|

|

|

957 |

|

|

|

972 |

|

|

|

|

|

|

| Copper production (millions of pounds) |

|

|

140 |

|

|

|

131 |

|

|

|

373 |

|

|

|

302 |

|

| Copper sold (millions of pounds) |

|

|

145 |

|

|

|

112 |

|

|

|

378 |

|

|

|

296 |

|

|

|

|

|

|

| Per pound data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average spot copper price |

|

$ |

2.39 |

|

|

$ |

3.17 |

|

|

$ |

2.58 |

|

|

$ |

3.15 |

|

| Average realized copper price2 |

|

|

2.18 |

|

|

|

3.09 |

|

|

|

2.44 |

|

|

|

3.08 |

|

| C1 cash costs2 |

|

|

1.53 |

|

|

|

1.82 |

|

|

|

1.75 |

|

|

|

1.98 |

|

| Depreciation3 |

|

|

0.13 |

|

|

|

0.44 |

|

|

|

0.21 |

|

|

|

0.40 |

|

| Other4 |

|

|

(0.17 |

) |

|

|

0.10 |

|

|

|

0.11 |

|

|

|

0.12 |

|

| C3 fully allocated costs2 |

|

|

1.49 |

|

|

|

2.36 |

|

|

|

2.07 |

|

|

|

2.50 |

|

| |

|

| Financial Results (millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Revenues |

|

$ |

2,315 |

|

|

$ |

2,624 |

|

|

$ |

6,791 |

|

|

$ |

7,729 |

|

| Net income (loss)5 |

|

|

(264 |

) |

|

|

125 |

|

|

|

(216 |

) |

|

|

(56) |

|

| Adjusted net earnings2 |

|

|

131 |

|

|

|

222 |

|

|

|

253 |

|

|

|

619 |

|

| Adjusted EBITDA2 |

|

|

942 |

|

|

|

1,059 |

|

|

|

2,465 |

|

|

|

3,056 |

|

| Operating cash flow6 |

|

|

1,255 |

|

|

|

852 |

|

|

|

2,096 |

|

|

|

1,925 |

|

| Free cash flow2, 6 |

|

|

866 |

|

|

|

199 |

|

|

|

694 |

|

|

|

40 |

|

| Per Share Data (dollars) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net earnings (loss) (basic) |

|

|

(0.23 |

) |

|

|

0.11 |

|

|

|

(0.19 |

) |

|

|

(0.05) |

|

| Adjusted net earnings (basic)2 |

|

|

0.11 |

|

|

|

0.19 |

|

|

|

0.22 |

|

|

|

0.53 |

|

| Net earnings (loss) (diluted) |

|

|

(0.23 |

) |

|

|

0.11 |

|

|

|

(0.19 |

) |

|

|

(0.05) |

|

|

|

|

|

|

| Weighted average basic and diluted common shares (millions) |

|

|

1,165 |

|

|

|

1,165 |

|

|

|

1,165 |

|

|

|

1,165 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| |

|

|

|

|

|

|

|

As at

September 30, |

|

|

As at

December 31, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

2015 |

|

|

2014 |

|

| |

|

| Financial Position (millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and equivalents |

|

|

|

|

|

|

|

|

|

$ |

3,317 |

|

|

$ |

2,699 |

|

| Working capital (excluding cash) |

|

|

|

|

|

|

|

|

|

|

1,523 |

|

|

|

1,937 |

|

| |

|

| |

1 |

Production includes Acacia on a 73.9% basis until February 28, 2014 and a 63.9% basis thereafter and Pueblo Viejo on a 60% basis, both of which reflect our equity share of production. Also includes production from

Plutonic up to January 31, 2014, Kanowna up to March 1, 2014, Marigold up to April 4, 2014, Cowal up to July 23, 2015 and Porgera on a 95% basis until August 31, 2015 and a 47.5% basis thereafter, the effective dates of sale

of these assets. Sales include our equity share of gold sales from Acacia and Pueblo Viejo. |

| |

2 |

Realized price, cash costs, all-in sustaining costs, all-in costs, cash costs (on a co-product basis), all-in sustaining costs (on a co-product basis), all-in costs (on a co-product basis), C1 cash costs, C3 fully

allocated costs, adjusted net earnings, adjusted EBITDA and free cash flow are non-GAAP financial performance measures with no standard definition under IFRS. Refer to the Non-GAAP |

| |

Financial |

Performance Measures section of the Company’s MD&A. |

| |

3 |

Represents equity depreciation expense divided by equity pounds of copper sold. |

| |

4 |

For a breakdown, see reconciliation of cost of sales to C1 cash costs and C3 fully allocated costs per pound in the Non-GAAP Financial Performance Measures section of the Company’s MD&A. |

| |

5 |

Net income (loss) represents net income (loss) attributable to the equity holders of the Company. |

| |

6 |

Includes a $610 million deposit received in third quarter 2015 related to the gold and silver streaming agreement. |

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

12 |

|

SUMMARY INFORMATION |

Production and Cost Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Gold Production (attributable ounces) (000’s) |

|

|

All-in sustaining costs5 ($/oz) |

|

| |

|

Three months ended

September 30, |

|

|

Nine months ended

September 30, |

|

|

Three months ended

September 30, |

|

|

Nine months ended

September

30, |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Goldstrike |

|

|

328 |

|

|

|

239 |

|

|

|

741 |

|

|

|

715 |

|

|

$ |

558 |

|

|

$ |

923 |

|

|

$ |

698 |

|

|

$ |

849 |

|

| Cortez |

|

|

321 |

|

|

|

273 |

|

|

|

647 |

|

|

|

717 |

|

|

|

501 |

|

|

|

591 |

|

|

|

711 |

|

|

|

667 |

|

| Pueblo Viejo3 |

|

|

172 |

|

|

|

168 |

|

|

|

438 |

|

|

|

488 |

|

|

|

554 |

|

|

|

559 |

|

|

|

628 |

|

|

|

585 |

|

| Lagunas Norte |

|

|

108 |

|

|

|

157 |

|

|

|

441 |

|

|

|

406 |

|

|

|

581 |

|

|

|

554 |

|

|

|

510 |

|

|

|

552 |

|

| Veladero |

|

|

143 |

|

|

|

178 |

|

|

|

443 |

|

|

|

525 |

|

|

|

914 |

|

|

|

822 |

|

|

|

957 |

|

|

|

786 |

|

| Turquoise Ridge |

|

|

55 |

|

|

|

54 |

|

|

|

156 |

|

|

|

156 |

|

|

|

738 |

|

|

|

592 |

|

|

|

745 |

|

|

|

594 |

|

| Porgera4 |

|

|

134 |

|

|

|

138 |

|

|

|

370 |

|

|

|

368 |

|

|

|

986 |

|

|

|

974 |

|

|

|

1,060 |

|

|

|

1,002 |

|

| Kalgoorlie |

|

|

97 |

|

|

|

82 |

|

|

|

237 |

|

|

|

244 |

|

|

|

725 |

|

|

|

1,040 |

|

|

|

923 |

|

|

|

1,004 |

|

| Acacia2 |

|

|

104 |

|

|

|

122 |

|

|

|

339 |

|

|

|

354 |

|

|

|

1,195 |

|

|

|

1,098 |

|

|

|

1,153 |

|

|

|

1,111 |

|

| Other Mines - Gold1 |

|

|

201 |

|

|

|

238 |

|

|

|

686 |

|

|

|

749 |

|

|

|

1,060 |

|

|

|

1,021 |

|

|

|

958 |

|

|

|

1,012 |

|

| |

|

| Total |

|

|

1,663 |

|

|

|

1,649 |

|

|

|

4,498 |

|

|

|

4,722 |

|

|

$ |

771 |

|

|

$ |

834 |

|

|

$ |

866 |

|

|

$ |

844 |

|

| |

|

|

|

|

| |

|

Copper Production (attributable pounds) (millions) |

|

|

C1 Cash Costs5 ($/lb) |

|

| |

|

Three months ended

September 30, |

|

|

Nine months ended

September 30, |

|

|

Three months ended

September 30, |

|

|

Nine months ended

September 30, |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Lumwana |

|

|

77 |

|

|

|

75 |

|

|

|

206 |

|

|

|

138 |

|

|

$ |

1.59 |

|

|

$ |

1.84 |

|

|

$ |

1.82 |

|

|

$ |

2.26 |

|

| Zaldívar |

|

|

63 |

|

|

|

56 |

|

|

|

167 |

|

|

|

164 |

|

|

|

1.47 |

|

|

|

1.82 |

|

|

|

1.67 |

|

|

|

1.78 |

|

| |

|

| Total |

|

|

140 |

|

|

|

131 |

|

|

|

373 |

|

|

|

302 |

|

|

$ |

1.53 |

|

|

$ |

1.82 |

|

|

$ |

1.75 |

|

|

$ |

1.98 |

|

| |

|

|

|

|

| |

|

|

|

|

Total Gold Production Costs ($/oz) |

|

| |

|

|

|

|

|

|

|

Three months ended

September 30, |

|

|

Nine months ended

September 30, |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| |

|

|

|

|

|

| Direct mining costs before impact of hedges at market foreign exchange rates |

|

|

$ |

538 |

|

|

$ |

585 |

|

|

$ |

588 |

|

|

$ |

592 |

|

| Losses (gains) realized on currency hedge and commodity hedge/economic hedge contracts |

|

|

|

18 |

|

|

|

(17) |

|

|

|

17 |

|

|

|

(20) |

|

| By-product credits |

|

|

|

(22 |

) |

|

|

(18) |

|

|

|

(25 |

) |

|

|

(21) |

|

| Royalties |

|

|

|

36 |

|

|

|

39 |

|

|

|

34 |

|

|

|

37 |

|

| |

|

| Cash costs5 |

|

|

|

570 |

|

|

|

589 |

|

|

|

614 |

|

|

|

588 |

|

| Depreciation |

|

|

|

219 |

|

|

|

198 |

|

|

|

229 |

|

|

|

198 |

|

| |

|

| Total production costs |

|

|

$ |

789 |

|

|

$ |

787 |

|

|

$ |

843 |

|

|

$ |

786 |

|

| |

|

| Cash costs5 |

|

|

$ |

570 |

|

|

$ |

589 |

|

|

$ |

614 |

|

|

$ |

588 |

|

| General & administrative costs |

|

|

|

13 |

|

|

|

41 |

|

|

|

30 |

|

|

|

46 |

|

| Rehabilitation - accretion and amortization (operating sites) |

|

|

|

24 |

|

|

|

19 |

|

|

|

25 |

|

|

|

21 |

|

| Mine on-site exploration and evaluation costs |

|

|

|

6 |

|

|

|

4 |

|

|

|

7 |

|

|

|

3 |

|

| Mine development expenditures |

|

|

|

82 |

|

|

|

94 |

|

|

|

104 |

|

|

|

109 |

|

| Sustaining capital expenditures |

|

|

|

76 |

|

|

|

87 |

|

|

|

86 |

|

|

|

77 |

|

| |

|

| All-in sustaining costs5 |

|

|

$ |

771 |

|

|

$ |

834 |

|

|

$ |

866 |

|

|

$ |

844 |

|

| |

|

| All-in costs5 |

|

|

$ |

815 |

|

|

$ |

975 |

|

|

$ |

932 |

|

|

$ |

951 |

|

| |

|

|

|

|

| |

|

|

|

|

Total Copper Production Costs ($/lb) |

|

| |

|

|

|

|

|

|

|

Three months ended

September 30, |

|

|

Nine months ended

September 30, |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| |

|

|

|

|

|

| C1 cash costs5 |

|

|

$ |

1.53 |

|

|

$ |

1.82 |

|

|

$ |

1.75 |

|

|

$ |

1.98 |

|

| Depreciation6 |

|

|

|

0.13 |

|

|

|

0.44 |

|

|

|

0.21 |

|

|

|

0.40 |

|

| Other7 |

|

|

|

(0.17 |

) |

|

|

0.10 |

|

|

|

0.11 |

|

|

|

0.12 |

|

| |

|

| C3 fully allocated costs5 |

|

|

$ |

1.49 |

|

|

$ |

2.36 |

|

|

$ |

2.07 |

|

|

$ |

2.50 |

|

| |

|

| |

1 |

Includes production from Plutonic up to January 31, 2014, Kanowna up to March 1, 2014, Marigold up to April 4, 2014 and Cowal up to July 23, 2015, the effective dates of sale of these assets.

|

| |

2 |

Figures relating to Acacia are presented on a 73.9% basis until February 28, 2014 and a 63.9% basis thereafter, which reflects our equity share of production. |

| |

3 |

Reflects production from Pueblo Viejo on a 60% basis, which reflects our equity share of production. |

| |

4 |

Reflects production on a 95% basis until August 31, 2015 and a 47.5% basis thereafter. |

| |

5 |

Cash costs, all-in sustaining costs, all-in costs, C1 cash costs and C3 fully allocated costs are non-GAAP financial performance measures with no standard meaning under IFRS. Refer to the Non-GAAP Financial Performance

Measures section of the Company’s MD&A. |

| |

6 |

Represents equity depreciation expense divided by equity pounds of copper sold. |

| |

7 |

For a breakdown, see reconciliation of cost of sales to C1 cash costs and C3 fully allocated costs per pound in the Non-GAAP Financial Performance Measures section of the Company’s MD&A. |

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

13 |

|

SUMMARY INFORMATION |

MANAGEMENT’S DISCUSSION AND ANALYSIS (“MD&A”)

This portion of the Quarterly Report provides management’s discussion and analysis

(“MD&A”) of the financial condition and results of operations to enable a reader to assess material changes in financial condition and results of operations as at and for the three and nine month periods ended September 30, 2015,

in comparison to the corresponding prior–year periods. The MD&A is intended to help the reader understand Barrick Gold Corporation (“Barrick”, “we”, “our” or the “Company”), our operations, financial

performance and present and future business environment. This MD&A, which has been prepared as of October 28, 2015, is intended to supplement and complement the condensed unaudited interim consolidated financial statements and notes

thereto, prepared in accordance with International Accounting Standard 34 Interim Financial Reporting (“IAS 34”) as issued by the International Accounting Standards Board (“IASB”), for the three and nine month periods ended

September 30, 2015 (collectively, the “Financial Statements”), which are included in this Quarterly Report on pages 59 to 84. You are encouraged to review the Financial Statements in conjunction with your review of this MD&A. This

MD&A should be read

in conjunction with both the annual audited consolidated financial statements for the two years ended

December 31, 2014, the related annual MD&A included in the 2014 Annual Report, and the most recent Form 40–F/Annual Information Form on file with the US Securities and Exchange Commission (“SEC”) and Canadian provincial

securities regulatory authorities. Certain notes to the Financial Statements are specifically referred to in this MD&A and such notes are incorporated by reference herein. All dollar amounts in this MD&A are in millions of US dollars, unless

otherwise specified.

For the purposes of preparing our MD&A, we consider the materiality of information. Information is considered material if:

(i) such information results in, or would reasonably be expected to result in, a significant change in the market price or value of our shares; or (ii) there is a substantial likelihood that a reasonable investor would consider it

important in making an investment decision; or (iii) it would significantly alter the total mix of information available to investors. We evaluate materiality with reference to all relevant circumstances, including potential market sensitivity.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Certain information contained or incorporated by reference in this MD&A, including any information as

to our strategy, projects, plans or future financial or operating performance constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words

“believe”, “expect”, “anticipate”, “contemplate”, “target”, “plan”, “intend”, “project”, “continue”, “budget”, “estimate”,

“potential”, “may”, “will”, “can”, “could” and similar expressions identify forward-looking statements. In particular, this MD&A contains forward-looking statements with respect to cash flow

forecasts, projected capital, operating and exploration expenditures, targeted cash flow improvements and debt reductions, mine life and production rates, potential mineralization and metal or mineral recoveries. Forward-looking statements are

necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company in light of management’s experience and perception of current conditions and expected developments, are inherently subject to

significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could

cause actual results to differ materially from those projected in the forward-looking statements. Such

factors include, but are not limited to: fluctuations in the spot and forward price of gold, copper or certain other commodities (such as silver, diesel fuel, natural gas and electricity); the speculative nature of mineral exploration and

development; changes in mineral production performance, exploitation and exploration successes; diminishing quantities or grades of reserves; increased costs, delays, suspensions and technical challenges associated with the construction of capital

projects; operating or technical difficulties in connection with mining or development activities, including disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with

environmental and health and safety laws and regulations; timing of receipt of, or failure to comply with, necessary permits and approvals; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets

and liabilities based on projected future cash flows; adverse changes in our credit ratings; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

14 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations and/or changes in the administration of laws,

policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States and other jurisdictions in which the Company does or may carry on business in the future; damage to the

Company’s reputation due to the actual or perceived occurrence of any number of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings with community groups, whether true or not;

the possibility that future exploration results will not be consistent with the Company’s expectations; risks that exploration data may be incomplete and considerable additional work may be required to complete further evaluation, including but

not limited to drilling, engineering and socio-economic studies and investment; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation; contests over title to properties, particularly title to undeveloped properties,

or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; our ability to successfully integrate acquisitions or complete divestitures; employee relations; increased

costs and risks related to the potential impact of climate change; availability and increased costs associated with mining inputs and labor; and the

organization of our previously held African gold operations and properties under a separate listed company.

In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold

bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can affect our actual results and could cause

actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us.

Readers are

cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this MD&A are qualified by these cautionary statements. Specific reference is made to the most recent

Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a discussion of some of the factors underlying forward-looking statements. We disclaim any intention or obligation to update or

revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

15 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

INDEX

|

|

|

|

|

| |

|

page |

|

|

|

| Results Overview |

|

|

|

|

|

|

| Review of 2015 Third Quarter Results and Full Year Outlook |

|

|

17 |

|

|

|

| Key Business Developments |

|

|

23 |

|

|

|

| Market Overview |

|

|

25 |

|

|

|

| Review of Financial Results |

|

|

|

|

|

|

| Revenue |

|

|

27 |

|

|

|

| Production Costs |

|

|

27 |

|

|

|

| Capital Expenditures |

|

|

28 |

|

|

|

| Additional Significant Statement of Income Items |

|

|

29 |

|

|

|

| Income Tax Expense |

|

|

30 |

|

|

|

| Operating Segments Performance |

|

|

30 |

|

|

|

| Financial Condition Review |

|

|

|

|

|

|

| Balance Sheet Review |

|

|

47 |

|

|

|

| Shareholders’ Equity |

|

|

47 |

|

|

|

| Comprehensive Income |

|

|

47 |

|

|

|

| Financial Position and Liquidity |

|

|

47 |

|

|

|

| Financial Instruments |

|

|

49 |

|

|

|

| Commitments and Contingencies |

|

|

49 |

|

|

|

| Internal Control over Financial Reporting and Disclosure Controls and Procedures |

|

|

50 |

|

|

|

| Review of Quarterly Results |

|

|

51 |

|

|

|

| IFRS Critical Accounting Policies and Accounting Estimates |

|

|

51 |

|

|

|

| Non-GAAP Financial Performance Measures |

|

|

52 |

|

|

|

|

|

|

| BARRICK THIRD QUARTER 2015 |

|

16 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

RESULTS

OVERVIEW

Review of 2015 Third Quarter Results and Full Year Outlook

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ($ millions, except where indicated) |

|

For the three months ended September 30 |

|

|

For the nine months ended September 30 |

|

| |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| |

|

| Financial Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Revenue |

|

|

$ 2,315 |

|

|

|

$ 2,624 |

|

|

|

$ 6,791 |

|

|

|

$ 7,729 |

|

| Net earnings (loss)1 |

|

|

(264) |

|

|

|

125 |

|

|

|

(216) |

|

|

|

(56) |

|

| Per share (“EPS”)2 |

|

|

(0.23) |

|

|

|

0.11 |

|

|

|

(0.19) |

|

|

|

(0.05) |

|

| Adjusted net earnings3 |

|

|

131 |

|

|

|

222 |

|

|

|

253 |

|

|

|

619 |

|

| Per share (“adjusted EPS”)2,3 |

|

|

0.11 |

|

|

|

0.19 |

|

|

|

0.22 |

|

|

|

0.53 |

|

| Adjusted EBITDA3 |

|

|

942 |

|

|

|

1,059 |

|

|

|

2,465 |

|

|

|

3,056 |

|

| Total project capital expenditures4 |

|

|

31 |

|

|

|

66 |

|

|

|

68 |

|

|

|

113 |

|

| Total capital expenditures - expansion4 |

|

|

11 |

|

|

|

128 |

|

|

|

130 |

|

|

|

301 |

|

| Total capital expenditures - sustaining4 |

|

|

342 |

|

|

|

410 |

|

|

|

1,056 |

|

|

|

1,201 |

|

| Operating cash flow5 |

|

|

1,255 |

|

|

|

852 |

|

|

|

2,096 |

|

|

|

1,925 |

|

| Free cash flow3 |

|

|

$ 866 |

|

|

|

$ 199 |

|

|

|

$ 694 |

|

|

|

$ 40 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| Operating Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold produced (000s ounces)6 |

|

|

1,663 |

|

|

|

1,649 |

|

|

|

4,498 |

|

|

|

4,722 |

|

| Gold sold (000s ounces)6 |

|

|

1,596 |

|

|

|

1,578 |

|

|

|

4,447 |

|

|

|

4,712 |

|

| Realized price ($ per ounce)3 |

|

|

$ 1,125 |

|

|

|

$ 1,285 |

|

|

|

$ 1,176 |

|

|

|

$ 1,286 |

|

| Cash costs ($ per ounce)3 |

|

|

570 |

|

|

|

589 |

|

|

|

614 |

|

|

|

588 |

|

| Cash costs on a co-product basis

($ per ounce)3 |

|

|

592 |

|

|

|

607 |

|

|

|

639 |

|

|

|

609 |

|

| All-in sustaining costs ($ per ounce)3 |

|

|

771 |

|