UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

Date: February 2, 2016

UBS Group AG

Commission File Number: 1-36764

UBS AG

Commission File Number: 1-15060

(Registrants' Names)

Bahnhofstrasse 45, Zurich, Switzerland, and

Aeschenvorstadt 1, Basel, Switzerland

(Address of principal executive office)

Indicate by check mark whether the registrant files or

will file annual reports under cover of Form 20‑F or Form 40-F.

Form 20-F x

Form 40-F o

This Form 6-K consists of the presentation

materials related to the Fourth Quarter 2015 Results of UBS Group AG and UBS

AG, and the related speaker notes, which appear immediately following this

page.

UBS

Fourth Quarter 2015 Earnings Call Remarks

February

2, 2016

Sergio P. Ermotti (Group CEO): Opening

remarks

SLIDE 2 – 2015 – Strong results and execution

Thank

you, Caroline. Good morning everyone.

2015

was another year of disciplined execution, where once again, we showed that we

can deliver sound advice to clients and strong returns to our shareholders in a

variety of market conditions.

For

the full year, we reported a net profit attributable to shareholders of 6.2

billion Swiss francs, a 79% increase over 2014. Adjusted profit before tax more

than doubled to 5.6 billion, and we delivered a return on tangible equity of

almost 14%, above our 2015 target of about 10%. Diluted earnings per share totaled

1.64 francs.

As

we expected, we were faced with exceptional levels of volatility, a challenging

macroeconomic outlook, escalating geopolitical tensions and a continued

deterioration in the risk appetite of our clients. It is no surprise that the

turbulent markets continue to impact investor sentiment. And our clients'

reluctance to remain fully invested has not changed. Our response is simple and

consistent, we stay close to our clients, and maintain our strong risk

discipline while carefully managing resources.

We

made excellent progress meeting future regulatory requirements in 2015. We

created UBS Switzerland AG, established our Group service company as a

subsidiary of UBS Group AG, and we successfully issued our first TLAC and AT1

instruments from our holding company.

In

addition, we delivered a net cost reduction in the Corporate Center of 1.1

billion francs compared to the full year 2013. While we are slightly behind

schedule on cost reduction, we are picking up the pace of execution and I am

confident we can deliver on our 2.1 billion net cost reduction target by the

end of next year as previously communicated.

In Non-core and Legacy Portfolio, we continued to

successfully reduce resource utilization by taking down risk-weighted assets by

14% and LRD by 47 billion.

Maintaining

a strong capital position remains a key competitive advantage for UBS, and we

continue to have the best Basel 3 CET1 basis among large global banks, with a

fully applied CET1 ratio of 14.5%. Our fully applied Swiss SRB leverage ratio

increased to 5.3%, and we believe we are well positioned to comply with future

Swiss TBTF requirements.

As

a consequence of our strong financial performance last year, and in line with

our capital returns policy, the Board of Directors intends to propose for

shareholder approval, an ordinary dividend of 60 Rappen per share, up 20%

compared to 2014 and a special dividend of 25 Rappen per share.

SLIDE 3 – The world's leading wealth

management franchise

UBS

is the world's largest wealth manager and the only large-scale player with a

truly global wealth management franchise at the center of its strategy.

Our

wealth management businesses' number one focus is to stay close to its clients

and guide them in achieving their wealth objectives, and we lead the industry

in doing this. In better markets the businesses puts clients' money to work,

and that happened in the first half of the year. In more challenging markets,

they advise clients to ensure they remain positioned to achieve their long term

objectives, including reducing risk when appropriate.

In

the past three years, we have grown invested assets in our wealth management

businesses at 8% per year on average, due both to strong markets and

significant net new money, taking our invested asset base to around 2 trillion

francs.

Most

importantly, profits have grown at nearly twice the rate of revenue, which is a

testament to the success of our strategic initiatives to grow higher margin

products and services like our banking, lending and mandate offerings, as well

as careful management of pricing and good cost control.

While

markets have not been kind so far this year, as the world's leading wealth

manager, we will not be distracted from our objective to deliver 10-15% annual

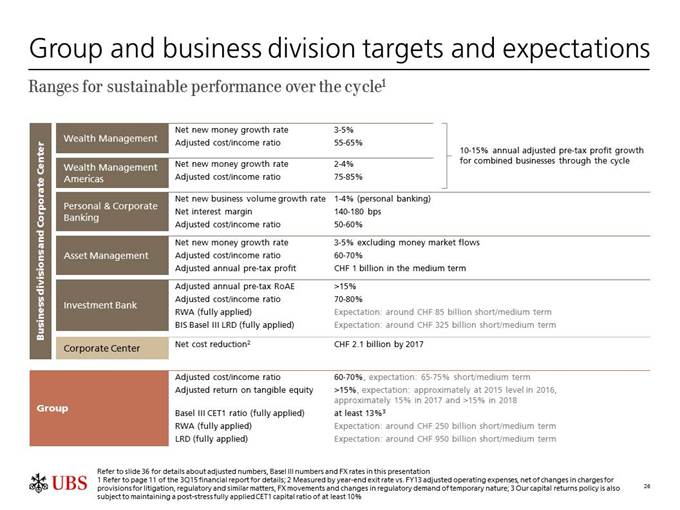

adjusted pre-tax profit growth in these businesses over the cycle.

SLIDE 4 - 2015 – Strong progress in all our

businesses

All

of our business divisions delivered strong results in 2015.

Wealth

Management delivered its highest adjusted pre-tax profit since 2008, and also

made good progress on one of its most critical strategic objectives, growing

mandate penetration by 200 basis points. Net new money was solid in aggregate,

despite the effects of our balance sheet optimization exercise and elevated

client deleveraging. We remain focused on attracting high quality assets, which

will drive long term growth rather than short term headlines. That means we are

seeking assets that will be invested over time and accretive to our results.

Wealth

Management Americas delivered record operating income and record net interest

income, as we saw continued growth in our banking and lending products. Net new

money was driven by advisors who have been with the firm for over a year and by

very strong recruiting in the fourth quarter.

Personal

& Corporate Banking recorded another excellent performance, posting its

best full year pre-tax profit since 2010 and attracting a record number of new

clients, while managing significant interest-rate headwinds.

Asset

Management progressed towards its medium-term goal, growing pre-tax profit by

20% compared with 2014. In the second half, net new money was affected by money

market outflows and material withdrawals by institutional clients to support

their liquidity needs. While overall net new money for the year was negative,

the inflows we saw were materially higher in margin, and thus we expect a

positive net effect on our revenues in 2016, another example where quality is

much more important to us than quantity.

Our

Investment Bank delivered an adjusted return on attributed equity of 31%,

substantially above its target of greater than 15%. The IB achieved excellent

financial returns and stayed close to its institutional and corporate clients,

helping them to manage through volatile markets.

We

saw strong growth in revenues in FRC and Equities, with continued efficient and

disciplined resource utilization, in line with client activity levels. We

advised on several of the year's landmark transactions, including the two deals

named "Equity Issues of the Year" by IFR. UBS acted as joint

bookrunner on the Santander capital increase and in North America, we were sole

global coordinator and lead left bookrunner on the 1 billion dollar listing of

Ferrari.

For the first time ever, International Financing

Review named the Investment Bank "Bank of the Year", highlighting the

recognition our innovative and sustainable operating model has attracted from

the industry. This is yet another example of the remarkable turnaround of our

investment bank. A few years ago it would have been inconceivable for UBS to

win an award like this, and it is a credit to our employees and our clients who

allowed us to deliver such an achievement.

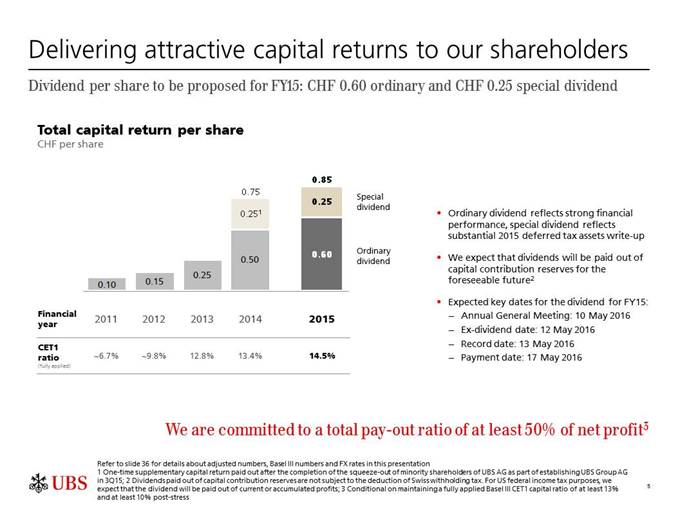

Slide 5 - Delivering attractive returns to

our shareholders

As

I mentioned earlier, our Board intends to recommend an ordinary dividend of 60

Rappen per share and a special dividend of 25 Rappen per share, which will be

paid in May following approval at our AGM. We will pay the ordinary dividend as

a reflection of our strong operating performance, while the special dividend

reflects the substantial upward revaluation of our deferred tax assets in 2015.

Going

forward, we remain committed to our policy of returning at least 50% of net

profits to shareholders. Although it's still very early in the year, our aim is

to continue to grow our ordinary dividend, while building the capital needed to

address regulatory requirements and to support our growth.

I

would like to add a few comments about our fourth quarter results before I hand

over to Kirt.

SLIDE 6 – 4Q15 results

The

last quarter of 2015 was the most challenging we have experienced in several

years and the risk-off sentiment among our clients intensified. Having said

that, one can't overlook that on an adjusted basis, fourth quarter results were

up 47% to 754 million. No matter how you look at it, risk aversion is still

very high. Clients know they should invest more, but cash helps them sleep

better at night. And while the long-term outlook remains sound, they are

questioning the predictability of tomorrow.

Underlying

results in WMA, Personal and Corporate and Asset Management were strong, while

our largest businesses were most affected by market volatility and client risk

aversion. Despite this, we were not tempted to deploy more risk or buy

unprofitable net new money to flatter our results. Instead we stayed close to

our clients, took risk off and continue to focus on our efficiency measures.

Driving sustainable performance and growth are our main priorities, and, as in

the past, short term vagaries of the market will not distract us from our

goals.

Kirt Gardner: speaker notes for 4Q15 results, 2

February 2016

Thank

you, Sergio. Good morning everyone.

Slide 7 - UBS Group AG results (consolidated)

My

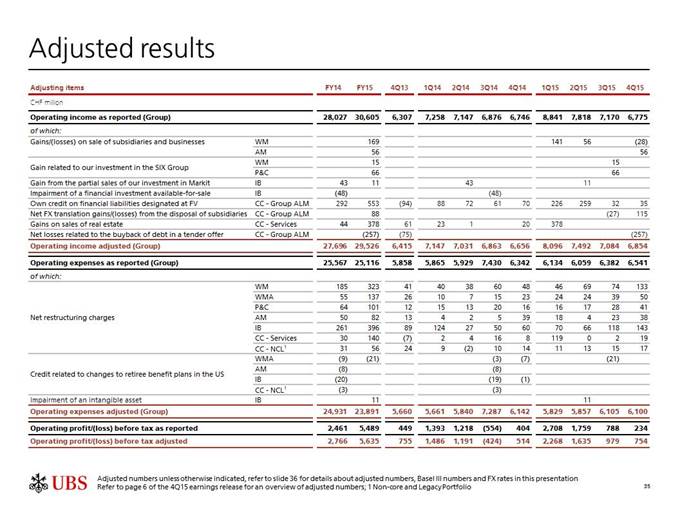

commentary will reference adjusted results unless otherwise stated.

This

quarter, we excluded 28 million Swiss francs of net gains and a 115 million net

foreign currency translation gain from the sales of subsidiaries and

businesses, an own credit gain of 35 million, a charge of 257 million for a

debt buyback, and net restructuring charges of 441 million.

Reported

net profit attributable to UBS Group AG shareholders was 949 million, up 11%

year-over-year, and profit before tax was 754 million, up 47% year-over-year.

We had a reported net tax benefit of 715 million, which included a 794 million

benefit with respect to DTAs, partially offset by current tax expenses.

The

annualized return on tangible equity was 11.4% for the quarter.

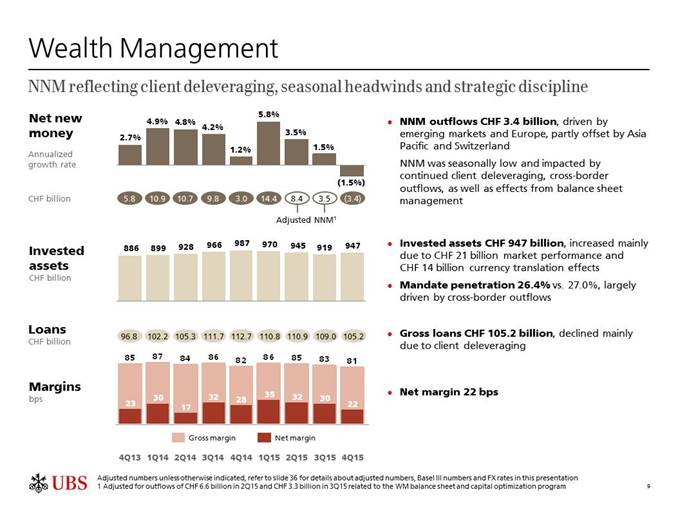

Slide 8 - Wealth Management

Wealth

Management performance reflected very challenging market conditions, with the

lowest client activity levels seen since the financial crisis.

Profit

before tax was 505 million, and included 79 million in charges for provisions

for litigation, regulatory and similar matters. Excluding these charges, profit

before tax was 584 million.

Operating

income was 1.9 billion, down 2% sequentially, driven by lower recurring net fee

income, mainly due to the ongoing effects of cross-border outflows.

Net

interest income was stable, as higher revenues from deposits were more than

offset by lower lending revenues, reflecting deleveraging and disciplined

lending practices.

Transaction-based

income was 364 million and included a 45 million fee received from Personal

& Corporate Banking. Excluding this fee, transaction-based income decreased

on significantly lower client activity, primarily in Asia Pacific and emerging

markets.

Operating expenses increased to 1.4 billion, largely

due to provisions, as well as the annual UK bank levy and other regulatory

charges, which totaled 102 million.

In

addition, allocations from Corporate Center increased, due to higher charges

from Group Technology, as we continued to invest in our platform.

Slide 9 - Wealth Management

Net

new money outflows of 3.4 billion reflects both the challenging environment and

wealth management's consistent disciplined approach to managing its business.

Net outflows were driven by continued deleveraging, as clients reduced risk in

response to extreme uncertainty, as well as cross-border outflows, and

proactive and disciplined balance sheet management.

Invested

assets increased to 947 billion, on positive market performance and currency

effects.

Mandate

penetration decreased by 60 basis points to 26.4%, largely driven by

cross-border outflows.

Monthly

gross margin was 79 basis points in October, decreasing to 77 basis points in

November, and picked up slightly to 82 basis points in December.

For

the last two quarters, gross margin from transaction-based revenues has been 16

basis points, the lowest since the crisis, while margins from recurring net

fees and net interest income have held up.

Slide 10 - Wealth Management

Net

new money was positive in APAC, despite continued client deleveraging, and

together with net inflows in Switzerland was more than offset by net outflows

in emerging markets and Europe.

We

expect to meet our 3-5% net new money growth target while absorbing

cross-border related outflows and maintaining our quality standards.

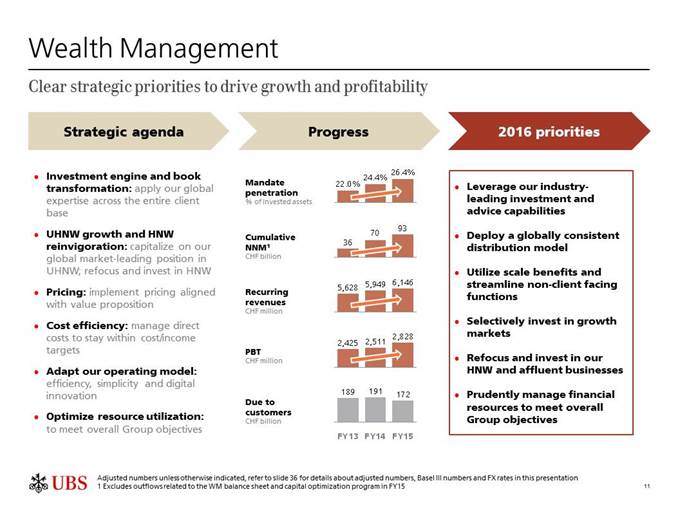

Slide 11

- Wealth Management

Despite

a challenging quarter, the trends over the past three years underline the

business's success in delivering its strategic agenda.

Since

the end of 2013, mandate penetration has increased by 440 basis points to

26.4%, and we continue to strive to increase this further to 40%.

The

business has attracted nearly 100 billion in adjusted net new money over the

past three years, which is more than double the prior three year period. This

strong performance was driven by our ultra high net worth segment. We'll build

on this success, and look to capture additional growth opportunities,

particularly in high net worth.

Pricing

discipline has added almost 300 million to annual revenues over the last two

years, helping offset the effects of cross-border outflows.

Growth

in top line revenues has been complemented by successful management of costs,

and we have met our cost/income ratio target for the last three years.

The

balance sheet and capital optimization program resulted in a 9 billion

reduction in LRD.

Looking

ahead, we see additional opportunity to improve both our client offering and

our efficiency. We intend to further optimize the delivery of content, by

deploying a globally consistent distribution model to capture synergies, as we

believe this provides the most value for our clients and shareholders. We will

also focus on capitalizing on our scale benefits, by streamlining non-client

facing functions.

We

are investing in select growth markets and remain committed to a balanced

onshore and offshore model.

And,

we will continue to optimize our financial resource usage and focus on net new

money quality to drive growth.

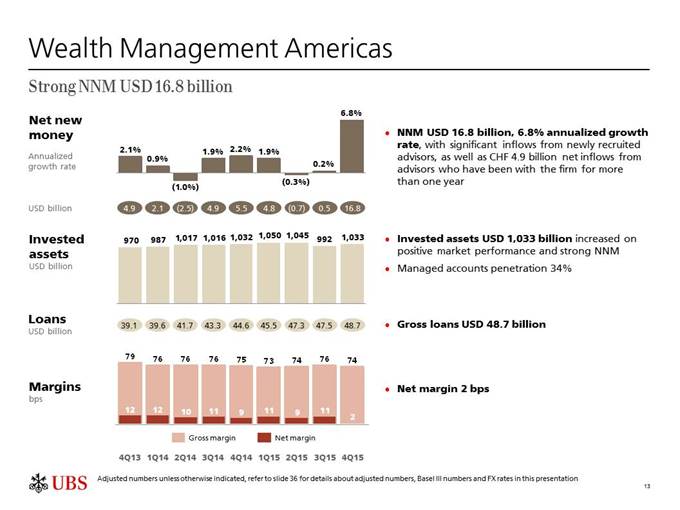

Slide 12 - Wealth Management Americas

UBS

is the only wealth management franchise that is truly global, which benefits

both clients and shareholders. These benefits were evident in the fourth

quarter, as US markets were less challenged than the rest of the world, and WMA

delivered excellent underlying results, with record net interest income and

16.8 billion dollars of net new money.

Profit

before tax was 63 million, and included 233 million of litigation provisions.

Excluding these charges, PBT was nearly 300 million.

Operating

income decreased by 3% as recurring net fee income was impacted by lower

invested assets at the end of the prior quarter, and as transaction-based

income decreased on lower client activity. This more than offset higher net

interest income, which increased by 5% to a record 326 million, as lending and

deposit volumes continued to grow.

Excluding

provisions, operating expenses decreased on lower personnel costs and charges

from other business divisions and Corporate Center.

Slide 13 - Wealth Management Americas

Net

new money was 16.8 billion, a 6.8% annualized growth rate, mainly reflecting

significant inflows from newly recruited experienced advisors, as well as 4.9

billion from advisors who have been with the firm for more than one year.

Invested

assets increased by 4% to over a trillion dollars. Managed account assets were

up 3% to 351 billion, and were 34% of total invested assets.

Slide 14 - Wealth Management Americas

Annualized

revenue per FA remained industry-leading. We had a very successful recruiting

quarter, increasing the number of FAs by 151, with 76% of recruits ranked in

the top two quintiles.

Loan

balances continued to grow, increasing by 3%.

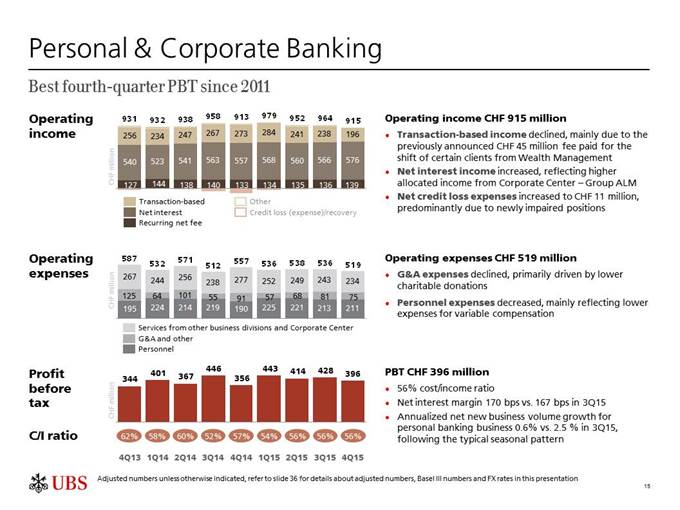

Slide 15 – Personal & Corporate Banking

Personal

and Corporate Banking delivered a profit before tax of 396 million, its

strongest fourth quarter since 2011.

Operating

income was 915 million, down 5% as higher net interest income was more than

offset by lower transaction-based income, which included the 45 million client

shift fee paid from P&C to WM.

Net

credit loss expense remained at historically low levels.

Operating

expenses decreased by 3%, and the cost/income ratio was stable at 56%,

comfortably within our target range.

Annualized

net new business volume growth for our personal banking business was seasonally

slower at 0.6%.

Slide 16 – Personal & Corporate Banking

Personal

& Corporate Banking closed another very strong year, further enhancing our

leadership position in Switzerland. We were recognized as the "Best Bank

in Switzerland" by Euromoney for the fourth consecutive year.

We

achieved the highest level of full-year profit before tax since 2010, as we

successfully offset headwinds with management actions to drive revenues, reduce

costs, and increase new business volume growth in our Personal Banking

business. Our Swiss franchise is an integral part of our business portfolio,

and it underpins the strength of our global brand.

Slide 17 - Asset Management

Asset

Management delivered a solid quarter, with profit before tax up 12%.

Operating

income was up 2%, on higher performance fees, mainly in Traditional Investments

and Global Real Estate.

Net management fees decreased by 2%, as higher fees in

Global Real Estate were more than offset by lower fees in other segments.

Net

new money outflows excluding money markets was 8.9 billion, driven by a small

number of institutional clients with liquidity needs. Excluding these outflows,

net new money was over 6 billion.

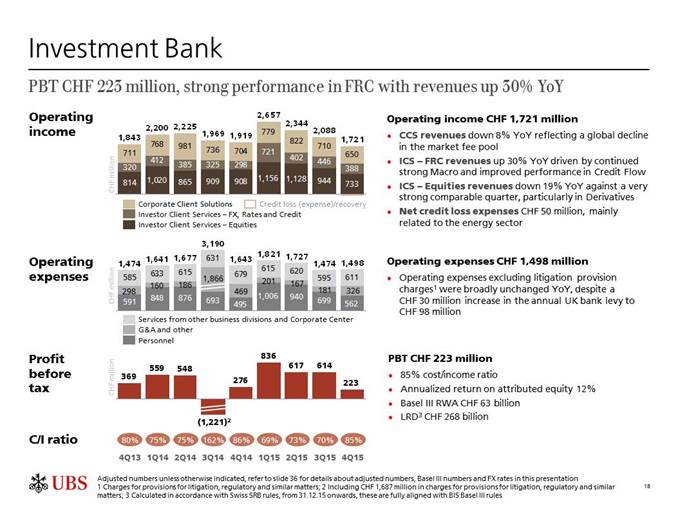

Slide 18 - Investment Bank

The

Investment Bank delivered a profit before tax of 223 million, which included a

98 million charge for the annual UK bank levy.

As

clients were less active, the business demonstrated disciplined resource

utilization, with balance sheet, RWA and average VaR decreasing

quarter-over-quarter and year-over-year.

FX,

Rates and Credit performance was strong, as revenues increased by 30%

year-over-year, on a strong result in Flow Rates and Macro options and improved

performance in Credit Flow.

In

Equities, revenues were down 19% year-over-year from a strong fourth quarter

2014. The decrease was largely driven by derivatives, as we saw lower client

activity and a challenging trading environment for structured products,

particularly in Asia Pacific and EMEA, where we have a significant presence.

This, along with lower revenues in Cash, more than offset a strong performance

from Financing Services, which delivered its best fourth quarter performance in

the last five years.

Corporate

Client Solutions delivered 650 million in revenues, down 8% year-over-year,

less than the decline in the global fee pool. Revenues in ECM were down from a

strong fourth quarter last year. In Advisory, revenues were down, but to a

lesser extent than the market fee pool, while DCM revenues were relatively

flat.

Net credit loss expense

was 50 million and mainly related to the energy sector. As of year-end, our

total net lending exposure to the oil and gas sector was 6.1 billion,

predominantly in North America. The majority of this exposure was investment

grade, and about half of this exposure was to the integrated and mid-stream

segments that we expect are less affected by the currently low energy price

levels. Exposures potentially vulnerable to low energy prices are closely

monitored and macro hedges are in place. Nevertheless, a sustained period of

depressed energy prices could result in increased credit loss expense for this

sub-segment of our portfolio.

Operating

expenses decreased 9% year-over-year to 1.5 billion, driven by lower G&A

expenses, primarily reflecting lower litigation provisions.

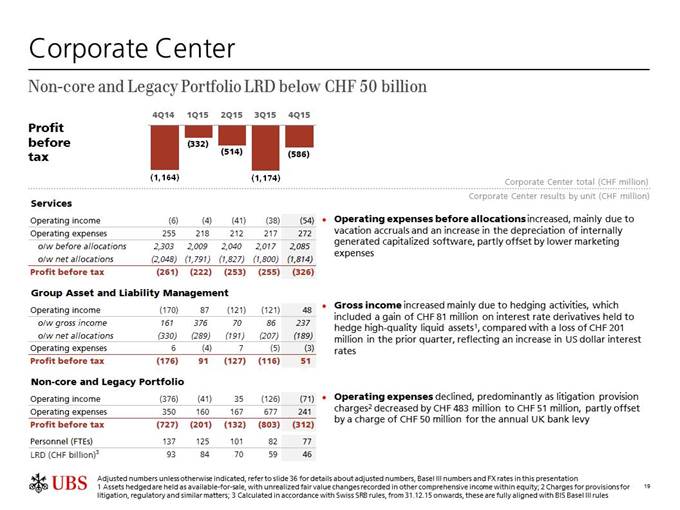

Slide 19 - Corporate Center

Profit

before tax in Corporate Center Services was negative 326 million, down 71

million, as full-year costs incurred by Corporate Center – Services exceeded

the cost allocations to the business divisions and Non-core and Legacy

Portfolio.

Expenses

before allocations increased, mainly due to vacation accruals and higher

depreciation charges.

Profit

before tax in Group ALM was 51 million, compared with negative 116 million in

the prior quarter. We saw a gain of 81 million from interest rate derivatives

used to hedge our high-quality liquid asset portfolio, compared with a loss of

201 million in the prior quarter.

Gross

funding costs increased by 91 million to 292 million, mostly due to higher fair

value gains on internal funding transactions in the prior quarter, but also

higher costs following the recent issuances of AT1 instruments and

TLAC-eligible debt.

We

expect the bond buyback from December and 2016 maturities, to generate a

benefit to funding costs of around 170 million in 2016.

Profit

before tax in Non-core and Legacy Portfolio was negative 312 million. Operating

income was negative 71 million, driven by losses from novation and unwind

activities, as well as valuation losses on financial assets designated at fair

value.

Operating expenses decreased by 436 million, as costs

decreased mainly due to lower litigation provisions, partially offset by a 50

million charge for the annual UK bank levy.

The

Non-core and Legacy Portfolio LRD was 46 billion, or 5% of the Group's total

LRD. Excluding operational risk RWA, Non-core and Legacy portfolio RWA is down

over 40% year-over-year to less than 10 billion.

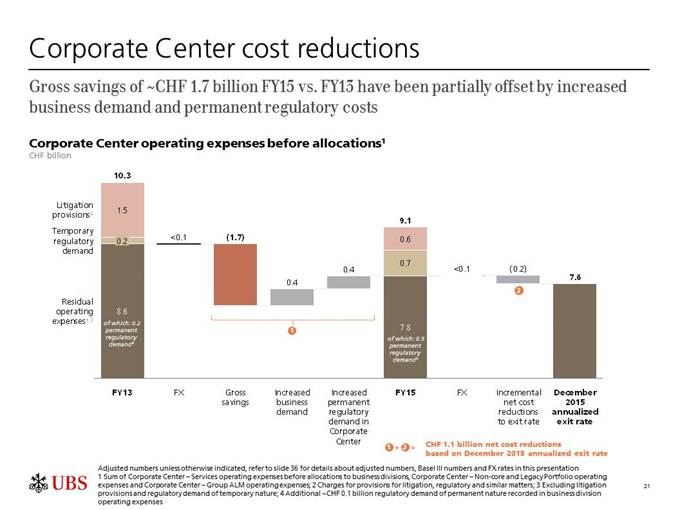

Slide 20 - Corporate Center cost reductions

Delivering

on our cost reduction initiatives continues to be one of our key priorities and

is a top priority for me as Group CFO.

We

achieved an additional 100 million of annualized net cost reduction in the

Corporate Center during the quarter, bringing the total to 1.1 billion. Savings

in the quarter were largely driven by lower personnel expenses in Group

Operations.

Full-year

restructuring charges were 1.2 billion. We still expect to incur the full three

billion we've guided for between 2015 and 2017.

Slide 21 – Corporate Center cost reductions

We've

encountered higher permanent regulatory costs and business demand, than was

originally anticipated.

Over

the past two years, we've generated 1.7 billion of gross saves, which have been

partially offset by a 400 million increase related to higher permanent

regulatory costs and a 400 million increase related to higher business demand.

Despite these headwinds, we are fully committed to our net cost reduction

targets. We currently expect to achieve 1.4 billion of net savings by around

the middle of this year, and we continue to target 2.1 billion by year-end

2017.

Slide 22 – Corporate Center Services cost

reductions

To

deliver on our cost targets, we continue to focus our efforts on the strategic

levers described in previous quarters. The majority of savings can be

categorized into one of three areas: workforce and footprint, organization and

process optimization, and technology.

Today, 27% of employees and contractors are in

offshore or near shore locations, compared with 18% only two years ago. In

addition to lower future personnel expenses, this is allowing us to realize

efficiencies in high-cost real estate.

Through

organization and process optimization, we look to increase effectiveness and

efficiency by leveraging common capabilities and creating centralized

functions. To give one example, we've created a Reporting and Analytics

Services unit, adopting common reporting processes and leading edge technology

to provide a better quality and lower-cost service to the business.

Within

Group Technology, we continue to modernize our infrastructure and simplify our

portfolio of applications.

For

example, we are migrating databases and servers to shared internal cloud

services, which are less costly to run, and more responsive to our business

needs.

We

are also rolling out our virtual desktop platform, which helps our employees to

become more efficient, while also reducing costs. In time, the platform will

also lead to reduced real estate costs as more of our employees can work

flexibly, both in the office and from home.

We

invested around 300 million in 2015 in our application portfolio to significantly

reduce the number of applications, simplify and modernize our technology, and

reduce operational risk.

The

savings associated with our technology initiatives require more lead time, but

by the completion of our program, we expect technology to contribute to a

sizeable portion of our cost savings.

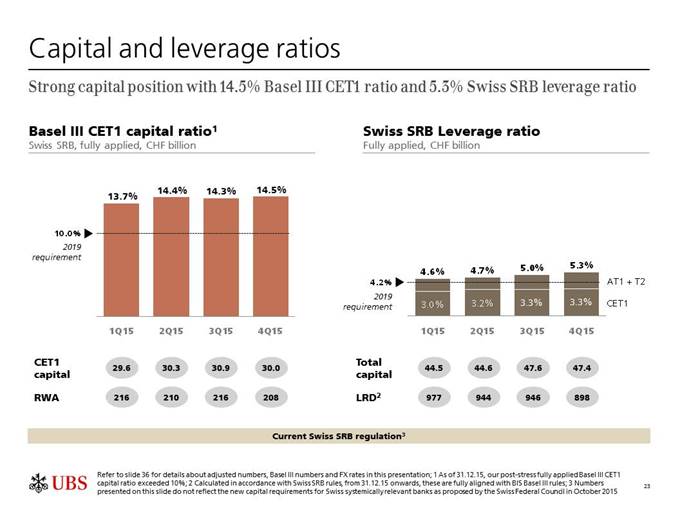

Slide 23 - Capital and leverage ratios

Our

capital position improved from already strong levels, with our fully applied

Basel III CET1 capital ratio increasing to 14.5% and a fully applied Swiss SRB

leverage ratio at 5.3%.

Our

CET1 capital ratio increased by 20 basis points as we reduced RWA by 9 billion,

mainly reflecting book size reductions, partially offset by currency effects

and methodology changes. This more than offset the impact of lower CET1

capital, which decreased as we accrued for dividends to shareholders and due to

tax effects.

We issued 1.4 billion of TLAC eligible debt in the

fourth quarter, which will contribute to the proposed gone-concern capital

ratios. AT1 capital increased by 0.6 billion, mainly due to deferred contingent

capital awards, to be granted to employees for the 2015 performance year.

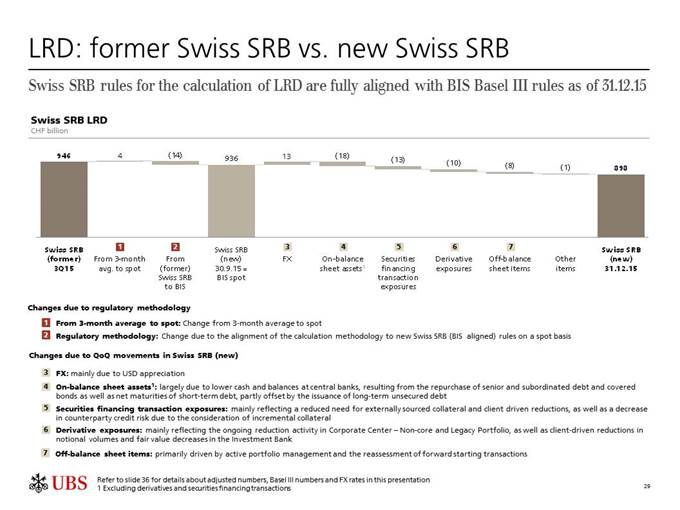

Our

fully applied BIS Basel III leverage ratio denominator was 898 billion, and

we've provided further details on LRD movements in the appendix of this

presentation.

From

December 2015, the Swiss SRB LRD calculation is fully aligned to the BIS Basel

III rules.

It

is worthwhile highlighting that, given our balance sheet composition, our LRD

is sensitive to foreign exchange as well as other market moves. For example,

currently, a 1% appreciation of the US Dollar against the Swiss Franc would

cause approximately a 4 billion increase in our LRD.

Thank

you, and with that, I will now hand it back over to Sergio.

Sergio P.

Ermotti (Group CEO): Closing remarks

CLOSING (SLIDE 24)

Thank

you, Kirt. Before we open up for questions, I would like to close with a few

remarks.

While

dovish tones from the FED and ECB have helped stabilize markets in the last few

days, uncertainties around energy prices and the outlook for China are still

driving a very cautious sentiment.

We

have begun a year that clearly looks very challenging, and our outlook remains

in line with our previous guidance. So what does that mean for us? By focusing

on our strengths, including capital and the clarity of our strategy, we believe

we have the ability to gain share of wallet and market share. We need to

maintain our global perspective on the trends driving long term wealth

accumulation. That is the reason we are keen to invest in those businesses and

geographies that will sustain growth over the long-term. Opportunities exist,

particularly in the US and Asia.

We

must also keep our focus on execution, including our cost reduction program.

Our goal is to deliver sustainable costs savings that improve our long-term

effectiveness. As we do that, we will free up resources which enables us to

selectively invest for growth.

Most

importantly, in the current environment, staying close to our clients and

delivering on our commitments remains paramount.

These

factors will underpin our ability to deliver value to shareholders and I have

every confidence in the future success of UBS.

Thank

you. And now Kirt and I will take your questions.

This Form 6-K is hereby incorporated by reference into each of

(1) the registration statement of UBS AG on Form F-3 (Registration

Number 333-204908) and (2) the registration statements of UBS Group AG on Form S-8

(Registration Numbers 333-200634; 333-200635; 333-200641; and 333-200665), and

into each prospectus outstanding under any of the foregoing registration

statements; and also into (3) any outstanding offering circular or similar

document issued or authorized by UBS AG that incorporates by reference any

Form 6-K’s of UBS AG that are incorporated into its registration

statements filed with the SEC, and (4) the base prospectus of Corporate

Asset Backed Corporation (“CABCO”) dated June 23, 2004 (Registration

Number 333-111572), the Form 8-K of CABCO filed and dated

June 23, 2004 (SEC File Number 001-13444), and the Prospectus

Supplements relating to the CABCO Series 2004-101 Trust dated May 10,

2004 and May 17, 2004 (Registration Number 033-91744 and

033-91744-05).

SIGNATURES

Pursuant to the requirements of the Securities

Exchange Act of 1934, the registrant has duly caused this report to be signed

on its behalf by the undersigned, thereunto duly authorized.

UBS Group AG

By: _/s/ David Kelly______________

Name: David Kelly

Title: Managing Director

By: _/s/ Sarah M. Starkweather______

Name: Sarah M. Starkweather

Title: Executive Director

UBS AG

By: _/s/ David Kelly______________

Name: David Kelly

Title: Managing Director

By: _/s/ Sarah M. Starkweather______

Name: Sarah M. Starkweather

Title: Executive Director

Date: February 2,

2016

UBS (NYSE:UBS)

Historical Stock Chart

From Mar 2024 to Apr 2024

UBS (NYSE:UBS)

Historical Stock Chart

From Apr 2023 to Apr 2024