SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the Month of November 2015

Commission File Number: 001-32294

TATA MOTORS LIMITED

(Translation of registrant’s name into English)

BOMBAY HOUSE

24, HOMI MODY STREET,

MUMBAI 400 001, MAHARASHTRA, INDIA

Telephone # 91 22 6665 8282 Fax # 91 22 6665 7799

(Address of principal executive office)

Indicate by check mark whether

the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ¨ No

x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by

Regulation S-T Rule 101(b)(7):

Yes ¨ No

x

Indicate by check mark whether by furnishing the information contained in this Form, the

Registrant is also thereby furnishing theinformation to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

Yes ¨ No

x

If “Yes” is marked, indicate below the file number assigned to the registrant in

connection with Rule 12g 3-2(b): Not Applicable

TABLE OF CONTENTS

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned,

thereunto duly authorised.

|

|

|

| Tata Motors Limited |

|

|

| By: |

|

/s/ Hoshang K Sethna |

| Name: |

|

Hoshang K Sethna |

| Title: |

|

Company Secretary |

Dated: November 9, 2015

JAGUAR LAND ROVER

Jaguar Land Rover Automotive PLC

Interim Report

For the three and six month period ended

30 September 2015

Company registered number: 06477691

Contents

This report uses:

Group,

Company, Jaguar Land Rover and JLR to refer to Jaguar Land Rover Automotive plc and its subsidiaries.

|

|

|

| EBITDA |

|

measured as earnings before tax and adding back depreciation, amortisation, finance income, finance expense, foreign exchange gains/(losses) on financing and unrealised derivatives, commodity gains/(losses) on unrealised

derivatives, exceptional items and share of gains/(losses) from joint ventures. |

|

|

| EBITDA margin |

|

measured as EBITDA as a percentage of revenue. |

|

|

| PBT |

|

profit before tax. |

|

|

| PAT |

|

profit after tax. |

|

|

| Net cash |

|

measured as cash and cash equivalents and short term deposits less total borrowings (including secured and unsecured borrowings and factoring facilities, but excluding finance leases). |

|

|

| Free cash flow |

|

measured as the net change in cash and cash equivalents, less net cash in financing activities, less movement in short term deposits. |

|

|

| Product and other investment |

|

measured as cash outflows relating to tangible assets, intangible assets, expensed R&D and investment in joint ventures. |

|

|

| FY16 |

|

Year ending 31 March 2016. |

|

|

| FY15 |

|

Year ended 31 March 2015. |

|

|

| Q2 |

|

3 months ended 30 September. |

|

|

| China JV |

|

Chery Jaguar Land Rover Joint Venture. |

Management’s discussion and analysis of financial condition and results of

operations

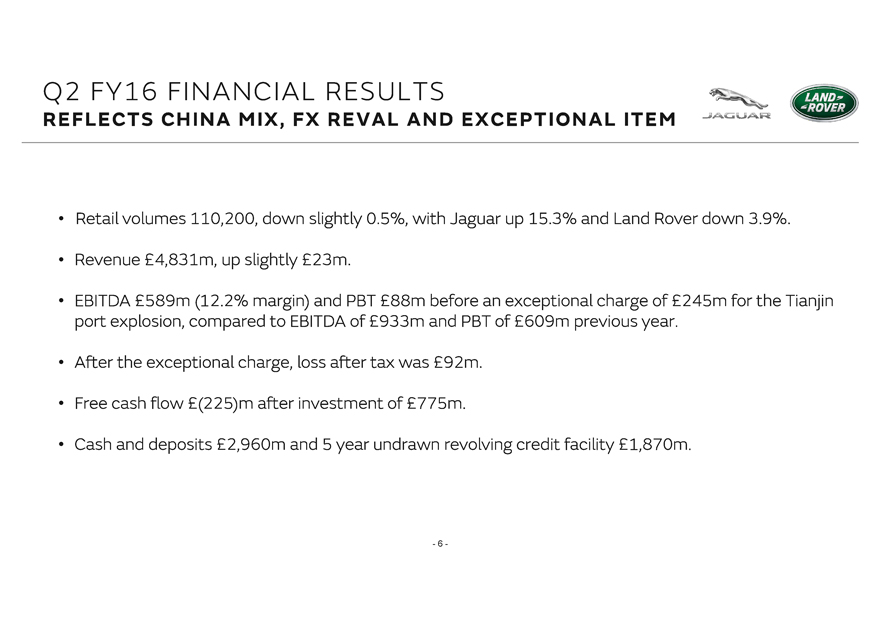

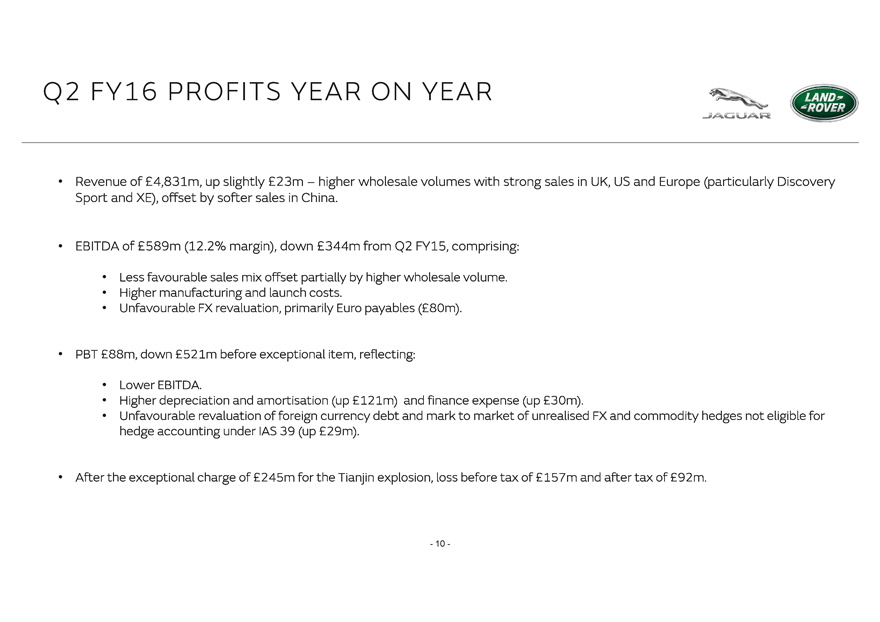

Retail sales in Q2 FY16 were broadly in line with the prior year’s record second quarter. Strong demand in the UK (up 9%

year-on-year), mainland Europe (up 34%) and North America (up 23%) – particularly for the new Land Rover Discovery Sport and Jaguar XE – helped offset weaker sales in China and emerging markets. However profitability was down primarily as

a result of weaker China sales and mix and foreign exchange revaluation as well as an exceptional charge for the inventory impacted by the Tianjin Port explosion.

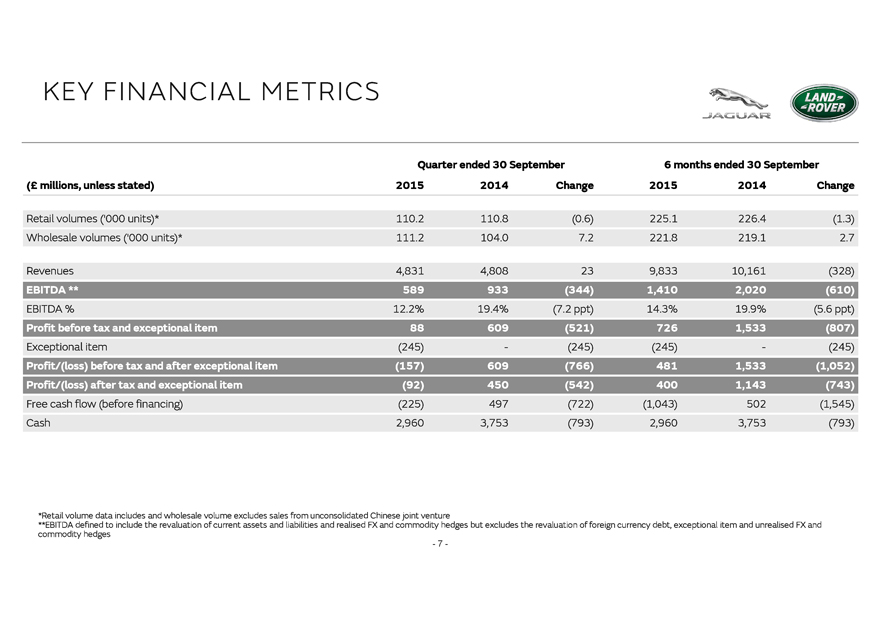

Key metrics for Q2 FY16, compared to Q2 FY15, are as follows:

| • |

|

Retail volumes (including China JV) were 110,200 units, down 0.5%. |

| • |

|

Wholesale volumes (excluding China JV) were 111,160 units, up 6.9%. |

| • |

|

Revenues of £4,831 million, up £23 million. |

| • |

|

EBITDA of £589 million, down £344 million. EBITDA margin of 12.2%, down 7.2 ppt. |

| • |

|

PBT of £88 million before exceptional item, down £521 million. |

| • |

|

Exceptional charge of £245 million for the inventory impacted by the Tianjin Port explosion. |

| • |

|

After the exceptional item of £245 million, loss after tax was £92 million. |

| • |

|

Negative free cash flow: £225 million before financing costs and after Investment spending of £775 million. |

| • |

|

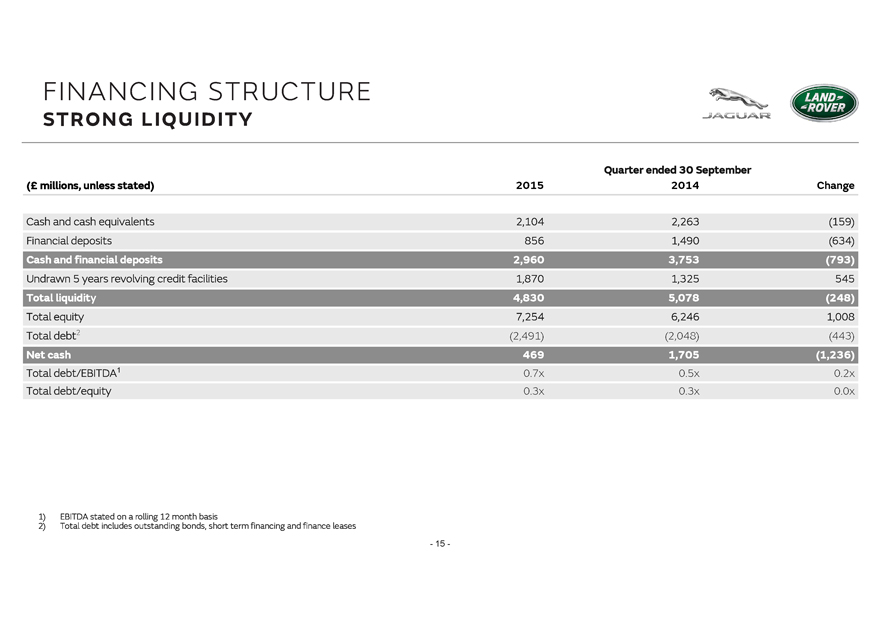

Cash and financial deposits: £2,960 million and an undrawn long-term 5 year credit facility of £1,870 million. |

Market environment

Macroeconomic

conditions remained mixed during the quarter. The economies of the UK and US continue to exhibit solid growth with low inflation whilst the European economy is picking up. The economic environment in China continues to be softer as GDP slipped below

the government’s growth target and market conditions in developing economies, notably Russia and Brazil, remain weak.

The US Dollar strengthened

against the Pound, despite the US Federal Reserve holding off on increasing interest rates, and the Chinese RMB strengthened against the Pound, to a lesser extent, following policy action which saw the RMB depreciate against the US Dollar. The Euro

also strengthened against the Pound over the quarter reflecting the gradual economic recovery in the Eurozone and emerging market currencies, such as the Russian Rouble and Brazilian Real weakened. Commodity prices also softened during Q2 FY16

primarily reflecting weaker industrial demand from China.

Total automotive industry car volumes (units)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Q2 FY16 |

|

|

Q2 FY15 |

|

|

Change (%) |

|

| China |

|

|

4,438,300 |

|

|

|

4,522,100 |

|

|

|

(1.9 |

)% |

| Europe (excluding UK) |

|

|

1,742,376 |

|

|

|

1,587,015 |

|

|

|

9.8 |

% |

| UK |

|

|

719,997 |

|

|

|

670,931 |

|

|

|

7.3 |

% |

| US |

|

|

4,509,500 |

|

|

|

4,245,300 |

|

|

|

6.2 |

% |

| All other markets |

|

|

3,422,914 |

|

|

|

3,705,572 |

|

|

|

(7.6 |

)% |

The total industry car volume data above has been compiled using relevant data available at the time of publishing this

interim report, compiled from national automotive associations such as the Society of Motor Manufacturers and Traders in the UK and the ACEA in Europe, according to their segment definitions, which may differ from those used by JLR.

2

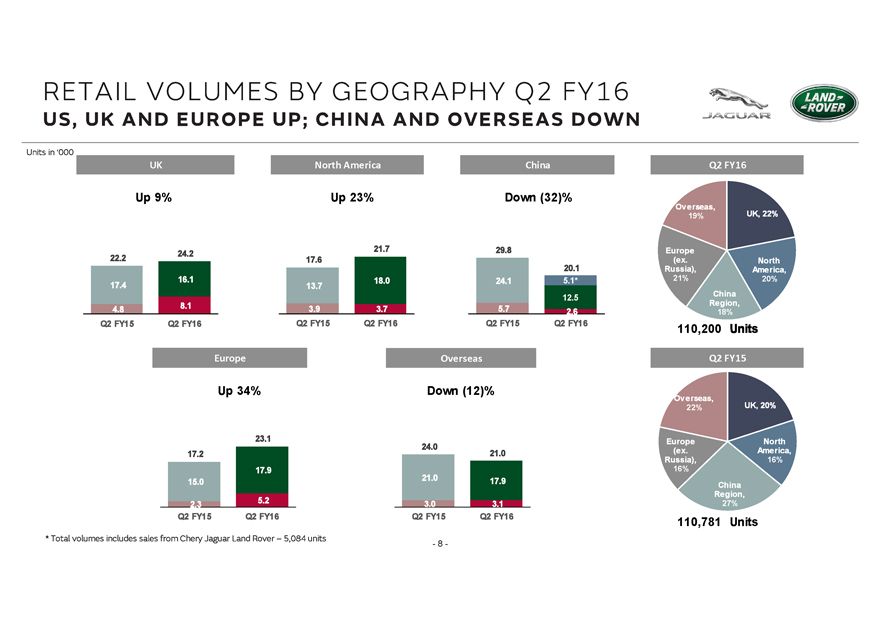

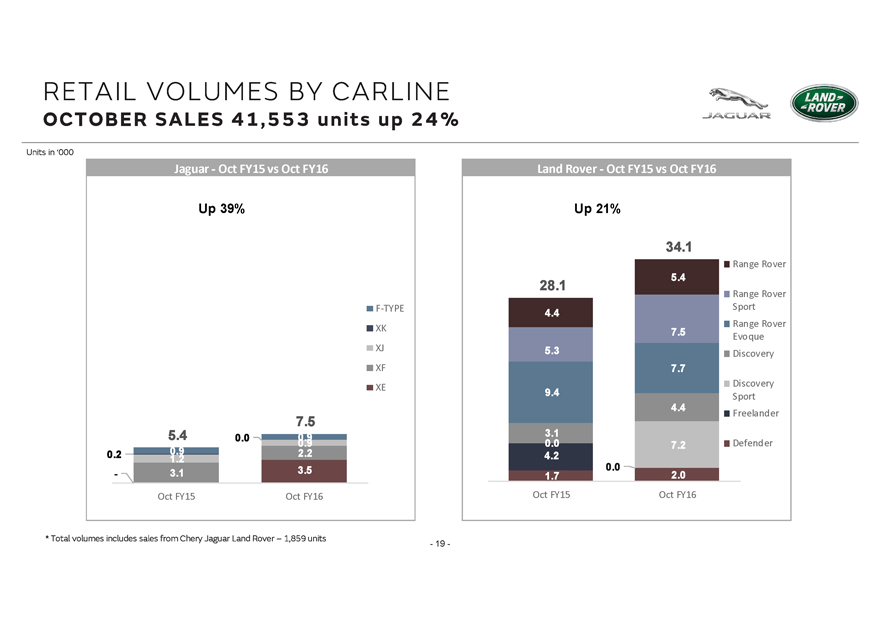

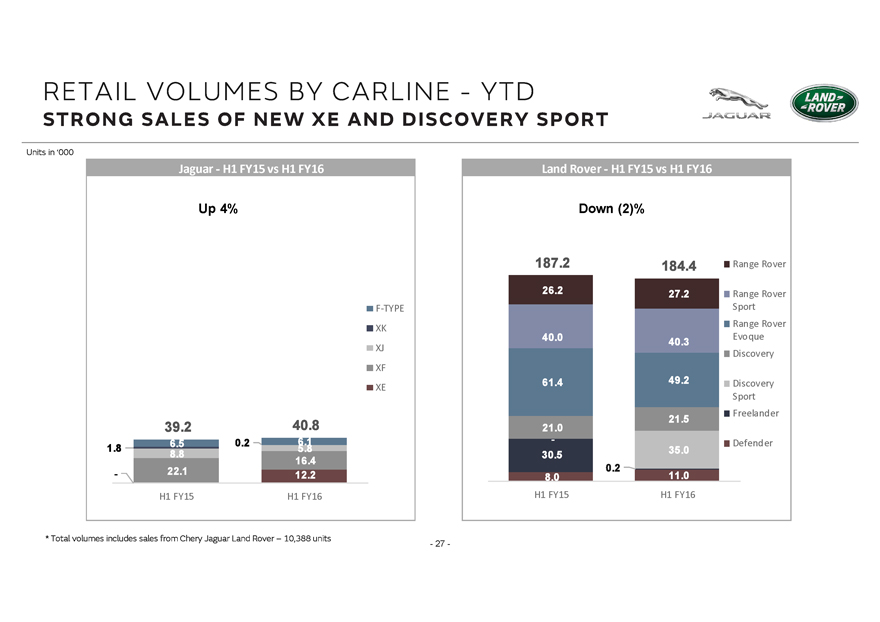

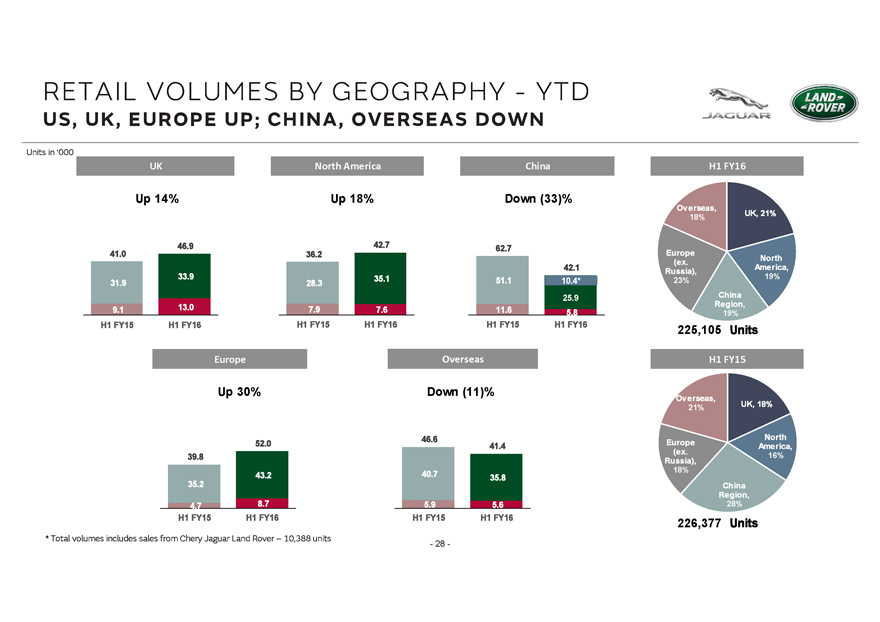

Jaguar Land Rover retail volume performance

Total retail volumes were 110,200 units for the quarter, a decrease of 0.5% compared to Q2 FY15. Higher retail sales in the UK, North America and Europe were

offset by lower sales in China and Other Overseas markets (which includes Russia and Brazil). The lower sales in China reflect continued softening demand and the timing of new model launches, such as the Jaguar XE which only went on sale in

September 2015, and the new XJ and XF models available in early 2016, as well as the transition to localised production first with the Evoque, followed by the Discovery Sport from November 2015.

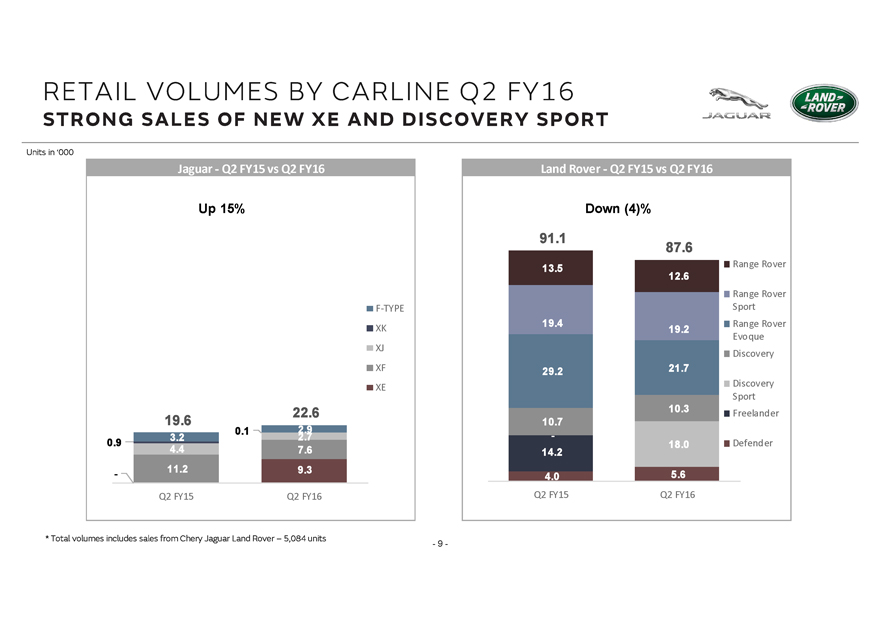

By brand, Land Rover retailed 87,554 units in Q2 FY16, down 3.9% compared to the same quarter last year, whilst Jaguar retailed 22,646 units, up 15.3%. Retail

sales of the Discovery Sport continue to grow with Q2 FY16 volumes up 26.6% compared to sales of the Freelander (which it replaced) in the same period last year. Discovery, Range Rover Sport and Range Rover retail sales remained robust, albeit down

slightly when compared to strong sales in the same quarter of last year. Evoque retail sales were down in the quarter, reflecting the transition to localised production in China and the start of production of the refreshed 16 Model Year Evoque

(starting from August 2015).

Jaguar retail volumes grew significantly, up 15.3%, due to strong XE sales, offset partially by lower sales of the XF and

XJ, ahead of the all new Jaguar XF (from August 2015) and a refreshed 16 Model Year Jaguar XJ (coming soon).

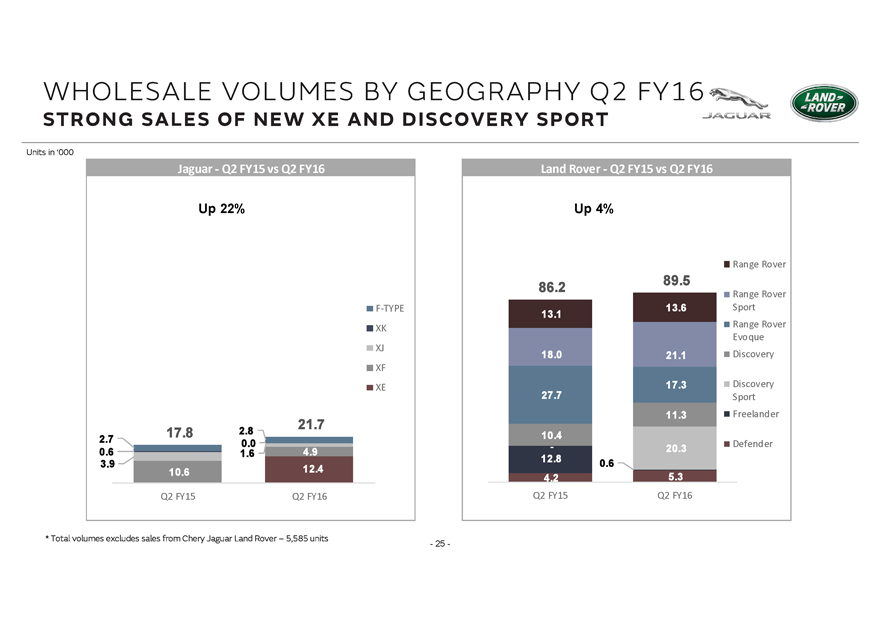

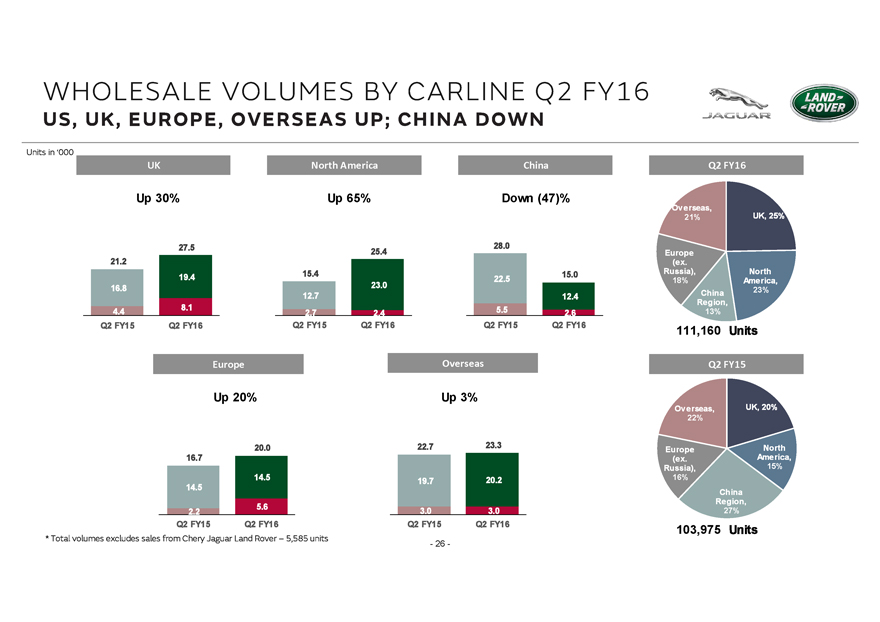

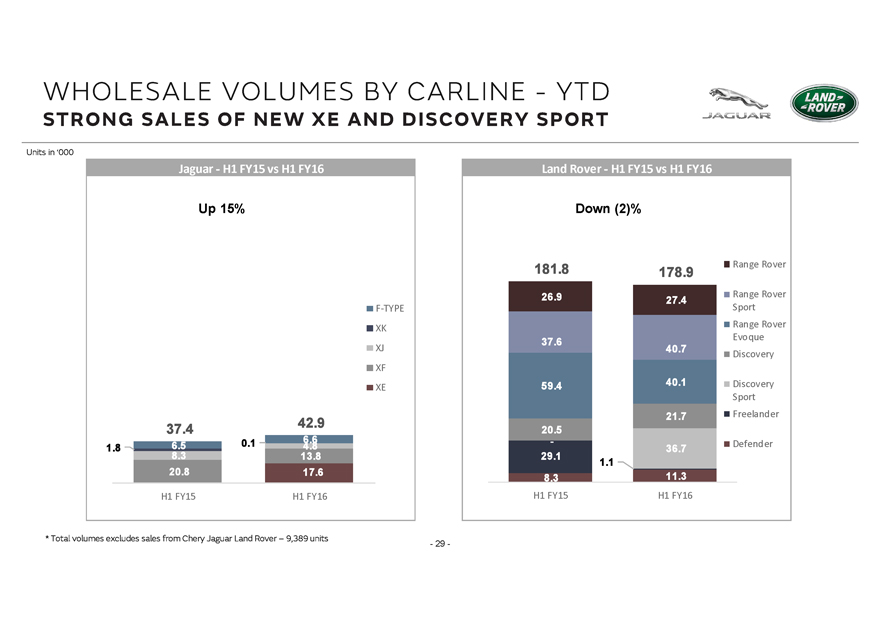

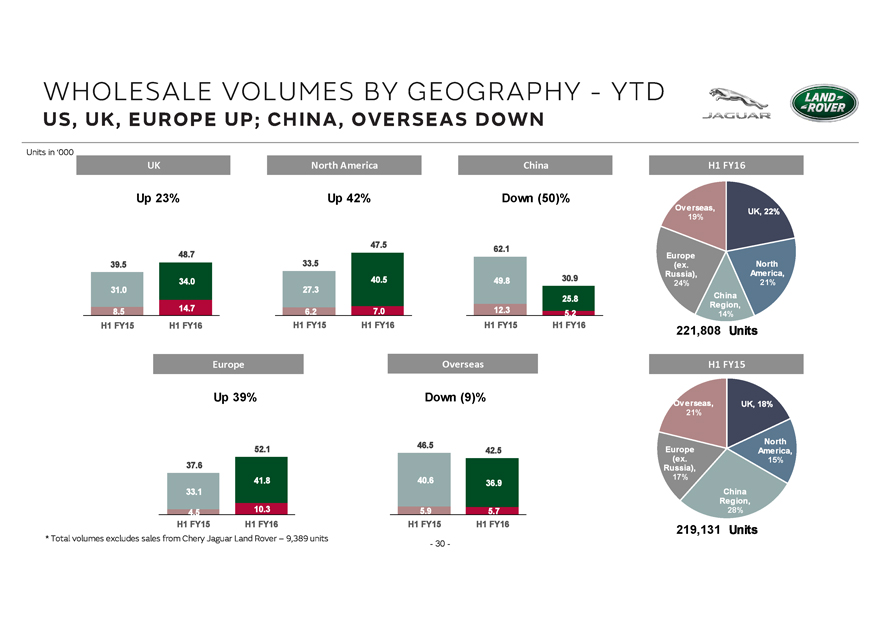

Wholesale volumes totalled 111,160 units

(excluding China JV) in Q2 FY16, up 6.9% compared to Q2 FY15. This comprised 89,473 units for Land Rover (down 3.8%) and 21,687 units for Jaguar (up 22.0% reflecting the ramp up of the Jaguar XE).

Jaguar Land Rover retail volume performance in key regions and by model for Q2 FY16 compared to Q2 FY15 is detailed in the following tables (figures in

units, and include China JV volumes).

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Q2 FY16 |

|

|

Q2 FY15 |

|

|

Change (%) |

|

| China |

|

|

20,149 |

|

|

|

29,786 |

|

|

|

(32.4 |

)% |

| Europe (excluding UK) |

|

|

23,113 |

|

|

|

17,227 |

|

|

|

34.2 |

% |

| UK |

|

|

24,180 |

|

|

|

22,151 |

|

|

|

9.2 |

% |

| North America |

|

|

21,743 |

|

|

|

17,616 |

|

|

|

23.4 |

% |

| All Other Markets |

|

|

21,015 |

|

|

|

24,001 |

|

|

|

(12.4 |

)% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total JLR |

|

|

110,200 |

|

|

|

110,781 |

|

|

|

(0.5 |

)% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| XE |

|

|

9,310 |

|

|

|

— |

|

|

|

n/a |

|

| XF |

|

|

7,598 |

|

|

|

11,217 |

|

|

|

(32.3 |

)% |

| XJ |

|

|

2,715 |

|

|

|

4,365 |

|

|

|

(37.8 |

)% |

| XK |

|

|

77 |

|

|

|

871 |

|

|

|

(91.2 |

)% |

| F-TYPE |

|

|

2,946 |

|

|

|

3,194 |

|

|

|

(7.8 |

)% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Jaguar |

|

|

22,646 |

|

|

|

19,647 |

|

|

|

15.3 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Defender |

|

|

5,619 |

|

|

|

4,038 |

|

|

|

39.2 |

% |

| Freelander |

|

|

41 |

|

|

|

14,235 |

|

|

|

(99.7 |

)% |

| Discovery Sport |

|

|

18,021 |

|

|

|

— |

|

|

|

n/a |

|

| Discovery |

|

|

10,344 |

|

|

|

10,717 |

|

|

|

(3.5 |

)% |

| Range Rover Evoque |

|

|

21,744 |

|

|

|

29,224 |

|

|

|

(25.6 |

)% |

| Range Rover Sport |

|

|

19,234 |

|

|

|

19,447 |

|

|

|

(1.1 |

)% |

| Range Rover |

|

|

12,551 |

|

|

|

13,473 |

|

|

|

(6.8 |

)% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Land Rover |

|

|

87,554 |

|

|

|

91,134 |

|

|

|

(3.9 |

)% |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total JLR |

|

|

110,200 |

|

|

|

110,781 |

|

|

|

(0.5 |

)% |

|

|

|

|

|

|

|

|

|

|

|

|

|

3

Revenue and profits

The Company generated revenue of £4,831 million in the three months to 30 September 2015, up £23 million, compared to revenue of

£4,808 million earned in the same three month period last year. Revenue for the 6 months to 30 September 2015 was £9,833 million, down £328 million compared to the same period a year ago.

EBITDA decreased by £344 million to £589 million in Q2 FY16 compared to £933 million in Q2 FY15 due to lower China sales and

mix, unfavourable revaluation of current assets and liabilities (primarily EUR payables) compared to a gain a year ago, and launch and other costs. EBITDA for the 6 months to 30 September 2015 was £1,410 million, down

£610 million compared to the same 6 month period last year.

PBT for Q2 FY16 before exceptional items was £88 million, down

£521 million from £609 million in Q2 FY15. The decrease in PBT was primarily driven by the lower EBITDA as well as higher depreciation and amortisation (£121 million higher), unfavourable revaluation of foreign currency

debt and unrealised hedges as well as higher net finance expense. An exceptional charge of £245 million has been recognised for about 5,800 vehicles involved in the August Tianjin Port explosion. After this exceptional charge, losses

before tax were £157 million. An insurance adjusting process is underway and insurance and any other recoveries will only be realised future periods.

PBT before exceptional items for the 6 months to 30 September 2015 was £726 million, down £807 million compared to the 6 months to

30 September 2014. PBT after the exceptional charge for the first half of the year was £481 million, down £1,052 million compared to the first half of the prior year.

Losses after tax for Q2 FY16 were £92 million, down £542 million compared to Q2 FY15. PAT for the 6 months to 30 September 2015 was

£400 million, down £743 million compared to the same 6 month period a year ago.

EBITDA reconciliation

|

|

|

|

|

|

|

|

|

| Three months ended 30 September (£ millions) |

|

2015 |

|

|

2014 |

|

| EBITDA margin |

|

|

12.2 |

% |

|

|

19.4 |

% |

| EBITDA |

|

|

589 |

|

|

|

933 |

|

| Adjustments: |

|

|

|

|

|

|

|

|

| Depreciation and amortisation |

|

|

(365 |

) |

|

|

(244 |

) |

| Foreign exchange losses – financing |

|

|

(59 |

) |

|

|

(53 |

) |

| Foreign exchange losses – unrealised derivatives |

|

|

(20 |

) |

|

|

(24 |

) |

| Commodity losses - unrealised derivatives |

|

|

(35 |

) |

|

|

(8 |

) |

| Finance income |

|

|

8 |

|

|

|

12 |

|

| Finance expense (net) |

|

|

(29 |

) |

|

|

(1 |

) |

| Share of loss from joint ventures |

|

|

(1 |

) |

|

|

(4 |

) |

| Other |

|

|

— |

|

|

|

(2 |

) |

|

|

|

|

|

|

|

|

|

| Profit before tax (excluding exceptional charge) |

|

|

88 |

|

|

|

609 |

|

|

|

|

|

|

|

|

|

|

| Exceptional charge |

|

|

(245 |

) |

|

|

— |

|

|

|

|

|

|

|

|

|

|

| (Loss)/profit before tax |

|

|

(157 |

) |

|

|

609 |

|

|

|

|

|

|

|

|

|

|

| Income tax credit/(expense) |

|

|

65 |

|

|

|

(159 |

) |

|

|

|

|

|

|

|

|

|

| (Loss)/profit after tax |

|

|

(92 |

) |

|

|

450 |

|

|

|

|

|

|

|

|

|

|

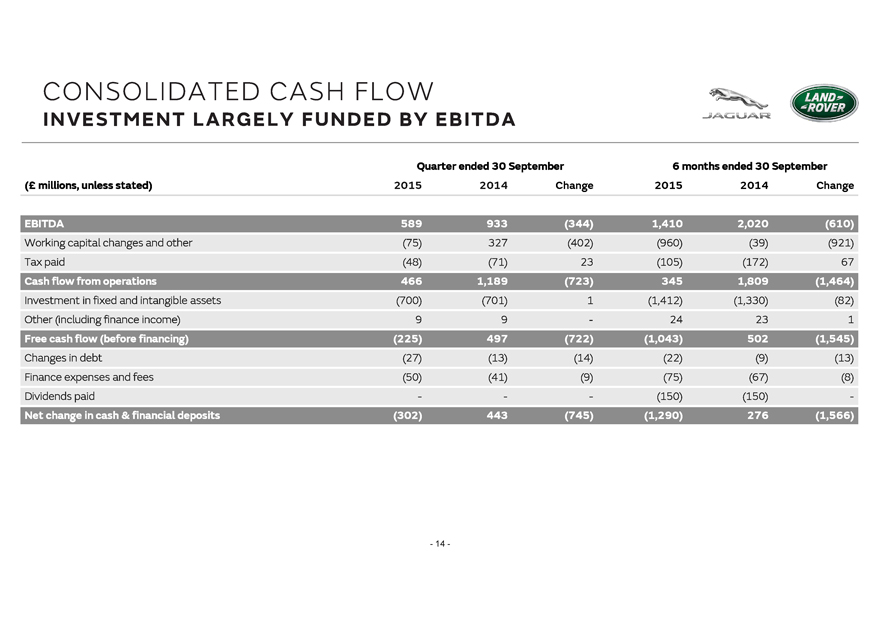

Cash flow, liquidity and capital resources

Free cash flow before financing for Q2 FY16 was negative £225 million, primarily reflecting capitalised investment spending of

£700 million exceeding EBITDA of £589m and higher working capital. Total investment spending was £775 million including £75 million expensed in EBITDA.

After the negative free cash flow of £225 million and finance expense of £50 million, cash and financial deposits stood at

£2,960 million as at 30 September 2015 (split £2,104 million of cash and cash equivalents and £856 million of bank deposits with maturities greater than 3 months). This includes an amount of

£531 million held in subsidiaries of Jaguar Land Rover outside of the United Kingdom. The cash in some of these jurisdictions is subject to impediments to remitting cash to the UK other than through annual dividends.

As at 30 September 2015, the Company also has undrawn committed credit facilities totalling £1,870 million all maturing in July 2020. Jaguar

Land Rover also had £95 million of undrawn shorter-term committed credit facilities.

4

Material events

On 12 August 2015 a series of explosions caused widespread damage at the Port of Tianjin in China. Tianjin Port is one of three major locations in China

through which Jaguar Land Rover imports vehicles and at the time of the explosion, approximately 5,800 vehicles were stored at various locations in Tianjin. Many of these vehicles were destroyed or damaged in the explosion and as a result an

exceptional charge of £245 million has been recognised in the financial statements of the Company for Q2 FY16. The process for finalising an insurance claim may take some months to conclude, so insurance and other potential recoveries

will only be recognised in future periods when paid or confirmed and have not been recognised in this period.

Borrowings

The following table shows details of the Company’s financing arrangements as at 30 September 2015.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (£ millions) |

|

Facility

amount |

|

|

Outstanding |

|

|

Undrawn |

|

|

First call

date |

|

| Committed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| £500m 8.250% Senior Notes due 2020* |

|

|

58 |

|

|

|

58 |

|

|

|

— |

|

|

|

Mar-2016 |

|

| £400m 5.000% Senior Notes due 2022** |

|

|

400 |

|

|

|

400 |

|

|

|

— |

|

|

|

n/a |

|

| £400m 3.875% Senior Notes due 2023** |

|

|

400 |

|

|

|

400 |

|

|

|

|

|

|

|

n/a |

|

| $410m 8.125% Senior Notes due 2021* |

|

|

55 |

|

|

|

55 |

|

|

|

— |

|

|

|

May-2016 |

|

| $500m 5.625% Senior Notes due 2023* |

|

|

330 |

|

|

|

330 |

|

|

|

— |

|

|

|

Feb-2018 |

|

| $700m 4.125% Senior Notes due 2018** |

|

|

462 |

|

|

|

462 |

|

|

|

— |

|

|

|

n/a |

|

| $500m 4.250% Senior Notes due 2019** |

|

|

330 |

|

|

|

330 |

|

|

|

— |

|

|

|

n/a |

|

| $500m 3.500% Senior Notes due 2020** |

|

|

330 |

|

|

|

330 |

|

|

|

— |

|

|

|

n/a |

|

| Revolving 5 year credit facility |

|

|

1,870 |

|

|

|

— |

|

|

|

1,870 |

|

|

|

n/a |

|

| Receivable factoring facilities*** |

|

|

231 |

|

|

|

136 |

|

|

|

95 |

|

|

|

n/a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Subtotal |

|

|

4,466 |

|

|

|

2,501 |

|

|

|

1,965 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Prepaid costs |

|

|

— |

|

|

|

(22 |

) |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total |

|

|

4,466 |

|

|

|

2,479 |

|

|

|

1,965 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| * |

The Notes are guaranteed on a senior unsecured basis by the guarantors Jaguar Land Rover Limited, Jaguar Land Rover Holdings Limited, Land Rover Exports Limited, JLR Nominee Company Limited and Jaguar Land Rover North

America LLC. |

| ** |

The Notes are guaranteed on a senior unsecured basis by the guarantors Jaguar Land Rover Limited and Jaguar Land Rover Holdings Limited. |

| *** |

The $350 million committed facility is drawn by Jaguar Land Rover Limited and guaranteed by Jaguar Land Rover Holdings Limited. |

A bilateral $200 million uncommitted receivables factoring facility is also available which remained undrawn as at 30 September 2015.

Acquisitions and disposals

There

were no material acquisitions or disposals in the period.

Off-balance sheet financial arrangements

The Company has no off-balance sheet financial arrangements other than commitments disclosed in the condensed consolidated financial statements.

Business risks and mitigating factors

As discussed on pages 76-81, and elsewhere, of the Annual Report 2014-15 of the Company, Jaguar Land Rover is exposed to various business risks including but

not limited to the uncertainty of global economic conditions, fluctuations of currency exchange rates and raw material prices.

Employees

At the end of Q2

FY16, Jaguar Land Rover employed 36,960 people worldwide including agency personnel. This compared to 31,826 at the end of Q2 FY15.

5

Board of Directors

The following table provides information with respect to members of the Board of Directors of Jaguar Land Rover:

|

|

|

|

|

| Name |

|

Position |

|

Year appointed as Director,

Chief Executive Officer |

| Cyrus P Mistry |

|

Chairman and Director |

|

2012 |

| Andrew M. Robb |

|

Director |

|

2009 |

| Dr. Ralf D. Speth |

|

Chief Executive Officer and Director |

|

2010 |

| Nasser Mukhtar Munjee |

|

Director |

|

2012 |

| Chandrasekaran Ramakrishnan |

|

Director |

|

2013 |

6

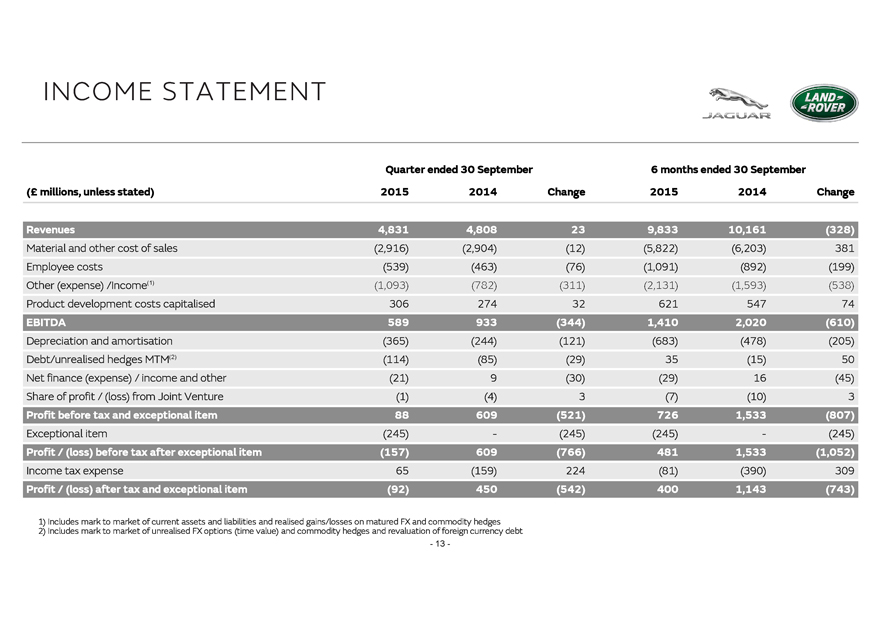

Condensed Consolidated Income Statement

For the three and six months ended 30 September 2015 (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Three months ended |

|

|

Six months ended |

|

| |

|

|

|

30 September |

|

|

30 September |

|

|

30 September |

|

|

30 September |

|

| |

|

|

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| (£ millions) |

|

Note |

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

| Revenue |

|

|

|

|

4,831 |

|

|

|

4,808 |

|

|

|

9,833 |

|

|

|

10,161 |

|

| Material cost of sales excluding exceptional item |

|

|

|

|

(2,916 |

) |

|

|

(2,904 |

) |

|

|

(5,822 |

) |

|

|

(6,203 |

) |

| Exceptional item |

|

2 |

|

|

(245 |

) |

|

|

— |

|

|

|

(245 |

) |

|

|

— |

|

| Material and other cost of sales |

|

|

|

|

(3,161 |

) |

|

|

(2,904 |

) |

|

|

(6,067 |

) |

|

|

(6,203 |

) |

| Employee cost |

|

|

|

|

(539 |

) |

|

|

(463 |

) |

|

|

(1,091 |

) |

|

|

(892 |

) |

| Other expenses |

|

|

|

|

(1,052 |

) |

|

|

(939 |

) |

|

|

(2,088 |

) |

|

|

(1,866 |

) |

| Net impact of commodity derivatives |

|

|

|

|

(46 |

) |

|

|

(7 |

) |

|

|

(73 |

) |

|

|

8 |

|

| Development costs capitalised |

|

3 |

|

|

306 |

|

|

|

274 |

|

|

|

621 |

|

|

|

547 |

|

| Other income |

|

|

|

|

33 |

|

|

|

32 |

|

|

|

129 |

|

|

|

56 |

|

| Depreciation and amortisation |

|

|

|

|

(365 |

) |

|

|

(244 |

) |

|

|

(683 |

) |

|

|

(478 |

) |

| Foreign exchange (loss)/gain |

|

|

|

|

(142 |

) |

|

|

45 |

|

|

|

(64 |

) |

|

|

192 |

|

| Finance income |

|

4 |

|

|

8 |

|

|

|

12 |

|

|

|

18 |

|

|

|

23 |

|

| Finance expense (net) |

|

4 |

|

|

(29 |

) |

|

|

(1 |

) |

|

|

(47 |

) |

|

|

(5 |

) |

| Share of loss from equity accounted investees |

|

|

|

|

(1 |

) |

|

|

(4 |

) |

|

|

(7 |

) |

|

|

(10 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Loss)/profit before tax |

|

|

|

|

(157 |

) |

|

|

609 |

|

|

|

481 |

|

|

|

1,533 |

|

| Income tax credit/ (expense) excluding tax on exceptional item |

|

|

|

|

4 |

|

|

|

(159 |

) |

|

|

(142 |

) |

|

|

(390 |

) |

| Tax on exceptional item |

|

9 |

|

|

61 |

|

|

|

— |

|

|

|

61 |

|

|

|

— |

|

| Income tax credit/(expense) |

|

9 |

|

|

65 |

|

|

|

(159 |

) |

|

|

(81 |

) |

|

|

(390 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Loss)/profit for the period |

|

|

|

|

(92 |

) |

|

|

450 |

|

|

|

400 |

|

|

|

1,143 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condensed Consolidated Statement of Comprehensive Income

For the three and six months ended 30 September 2015 (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Three months ended |

|

|

Six months ended |

|

| |

|

30 September |

|

|

30 September |

|

|

30 September |

|

|

30 September |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| (£ millions) |

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

| (Loss)/profit for the period |

|

|

(92 |

) |

|

|

450 |

|

|

|

400 |

|

|

|

1,143 |

|

| Items that will not be reclassified subsequently to profit or loss: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Remeasurement of defined benefit obligation |

|

|

261 |

|

|

|

(80 |

) |

|

|

435 |

|

|

|

(194 |

) |

| Income tax related to items that will not be reclassified |

|

|

(52 |

) |

|

|

16 |

|

|

|

(87 |

) |

|

|

39 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

209 |

|

|

|

(64 |

) |

|

|

348 |

|

|

|

(155 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Items that may be reclassified subsequently to profit or loss: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Loss)/gain on effective cash flow hedges |

|

|

(136 |

) |

|

|

(475 |

) |

|

|

669 |

|

|

|

(412 |

) |

| Cash flow hedges reclassified to foreign exchange gain in profit or loss |

|

|

15 |

|

|

|

(69 |

) |

|

|

118 |

|

|

|

(158 |

) |

| Currency translation differences |

|

|

2 |

|

|

|

11 |

|

|

|

(14 |

) |

|

|

— |

|

| Income tax related to items that may be reclassified |

|

|

25 |

|

|

|

109 |

|

|

|

(157 |

) |

|

|

114 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(94 |

) |

|

|

(424 |

) |

|

|

616 |

|

|

|

(456 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Other comprehensive income / (expense) net of tax |

|

|

115 |

|

|

|

(488 |

) |

|

|

964 |

|

|

|

(611 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total comprehensive income / (expense) attributable to shareholders |

|

|

23 |

|

|

|

(38 |

) |

|

|

1,364 |

|

|

|

532 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7

Condensed Consolidated Balance Sheet

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

Note |

|

(unaudited) |

|

|

(audited) |

|

| Non-current assets |

|

|

|

|

|

|

|

|

|

|

| Equity accounted investees |

|

|

|

|

259 |

|

|

|

280 |

|

| Other financial assets |

|

|

|

|

127 |

|

|

|

49 |

|

| Property, plant and equipment |

|

|

|

|

4,878 |

|

|

|

4,474 |

|

| Intangible assets |

|

|

|

|

5,239 |

|

|

|

4,952 |

|

| Other assets |

|

|

|

|

71 |

|

|

|

26 |

|

| Deferred tax assets |

|

|

|

|

407 |

|

|

|

372 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total non-current assets |

|

|

|

|

10,981 |

|

|

|

10,153 |

|

|

|

|

|

|

|

|

|

|

|

|

| Current assets |

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

|

|

|

2,104 |

|

|

|

3,208 |

|

| Short term deposits |

|

|

|

|

856 |

|

|

|

1,055 |

|

| Trade receivables |

|

|

|

|

974 |

|

|

|

1,112 |

|

| Other financial assets |

|

6 |

|

|

245 |

|

|

|

214 |

|

| Inventories |

|

7 |

|

|

2,799 |

|

|

|

2,416 |

|

| Other current assets |

|

8 |

|

|

393 |

|

|

|

396 |

|

| Current tax assets |

|

|

|

|

60 |

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total current assets |

|

|

|

|

7,431 |

|

|

|

8,410 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total assets |

|

|

|

|

18,412 |

|

|

|

18,563 |

|

|

|

|

|

|

|

|

|

|

|

|

| Current liabilities |

|

|

|

|

|

|

|

|

|

|

| Accounts payable |

|

|

|

|

4,785 |

|

|

|

5,450 |

|

| Short term borrowings |

|

14 |

|

|

136 |

|

|

|

156 |

|

| Other financial liabilities |

|

11 |

|

|

696 |

|

|

|

923 |

|

| Provisions |

|

12 |

|

|

471 |

|

|

|

485 |

|

| Other current liabilities |

|

13 |

|

|

351 |

|

|

|

374 |

|

| Current tax liabilities |

|

|

|

|

36 |

|

|

|

69 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total current liabilities |

|

|

|

|

6,475 |

|

|

|

7,457 |

|

|

|

|

|

|

|

|

|

|

|

|

| Non-current liabilities |

|

|

|

|

|

|

|

|

|

|

| Long term debt |

|

14 |

|

|

2,345 |

|

|

|

2,381 |

|

| Other financial liabilities |

|

11 |

|

|

470 |

|

|

|

842 |

|

| Provisions |

|

12 |

|

|

615 |

|

|

|

639 |

|

| Retirement benefit obligation |

|

17 |

|

|

572 |

|

|

|

887 |

|

| Other non-current liabilities |

|

|

|

|

139 |

|

|

|

118 |

|

| Deferred tax liabilities |

|

|

|

|

542 |

|

|

|

199 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total non-current liabilities |

|

|

|

|

4,683 |

|

|

|

5,066 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities |

|

|

|

|

11,158 |

|

|

|

12,523 |

|

|

|

|

|

|

|

|

|

|

|

|

| Equity attributable to shareholders |

|

|

|

|

|

|

|

|

|

|

| Ordinary shares |

|

|

|

|

1,501 |

|

|

|

1,501 |

|

| Capital redemption reserve |

|

|

|

|

167 |

|

|

|

167 |

|

| Reserves |

|

15 |

|

|

5,586 |

|

|

|

4,372 |

|

|

|

|

|

|

|

|

|

|

|

|

| Equity attributable to shareholders |

|

|

|

|

7,254 |

|

|

|

6,040 |

|

|

|

|

|

|

|

|

|

|

|

|

| Total liabilities and equity |

|

|

|

|

18,412 |

|

|

|

18,563 |

|

|

|

|

|

|

|

|

|

|

|

|

These condensed consolidated interim financial statements were approved by the board of directors.

Company registered number: 6477691

8

Condensed Consolidated Statement of Changes in Equity

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (£ millions) |

|

Ordinary share

capital |

|

|

Capital redemption

reserve |

|

|

Other reserves |

|

|

Total equity |

|

| Balance at 1 April 2015 (audited) |

|

|

1,501 |

|

|

|

167 |

|

|

|

4,372 |

|

|

|

6,040 |

|

| Profit for the period |

|

|

— |

|

|

|

— |

|

|

|

400 |

|

|

|

400 |

|

| Other comprehensive income for the period |

|

|

— |

|

|

|

— |

|

|

|

964 |

|

|

|

964 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total comprehensive income |

|

|

— |

|

|

|

— |

|

|

|

1,364 |

|

|

|

1,364 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Dividend paid |

|

|

— |

|

|

|

— |

|

|

|

(150 |

) |

|

|

(150 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Balance at 30 September 2015 (unaudited) |

|

|

1,501 |

|

|

|

167 |

|

|

|

5,586 |

|

|

|

7,254 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (£ millions) |

|

Ordinary share

capital |

|

|

Capital redemption

reserve |

|

|

Other reserves |

|

|

Total equity |

|

| Balance at 1 April 2014 (audited) |

|

|

1,501 |

|

|

|

167 |

|

|

|

4,196 |

|

|

|

5,864 |

|

| Profit for the period |

|

|

— |

|

|

|

— |

|

|

|

1,143 |

|

|

|

1,143 |

|

| Other comprehensive expense for the period |

|

|

— |

|

|

|

— |

|

|

|

(611 |

) |

|

|

(611 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total comprehensive income |

|

|

— |

|

|

|

— |

|

|

|

532 |

|

|

|

532 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Dividend paid |

|

|

— |

|

|

|

— |

|

|

|

(150 |

) |

|

|

(150 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Balance at 30 September 2014 (unaudited) |

|

|

1,501 |

|

|

|

167 |

|

|

|

4,578 |

|

|

|

6,246 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9

Condensed Consolidated Cash Flow Statement

For the three and six months ended 30 September 2015 (unaudited)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Three months ended |

|

|

Six months ended |

|

| |

|

30 September |

|

|

30 September |

|

|

30 September |

|

|

30 September |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| (£ millions) |

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

| Cash flows from operating activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (Loss)/profit for the period |

|

|

(92 |

) |

|

|

450 |

|

|

|

400 |

|

|

|

1,143 |

|

| Adjustments for: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Depreciation and amortisation |

|

|

365 |

|

|

|

244 |

|

|

|

683 |

|

|

|

478 |

|

| Loss on sale of assets |

|

|

— |

|

|

|

— |

|

|

|

3 |

|

|

|

1 |

|

| Foreign exchange gain on loans |

|

|

59 |

|

|

|

53 |

|

|

|

(40 |

) |

|

|

26 |

|

| Income tax (credit)/expense |

|

|

(65 |

) |

|

|

159 |

|

|

|

81 |

|

|

|

390 |

|

| Finance expense (net) |

|

|

29 |

|

|

|

1 |

|

|

|

47 |

|

|

|

5 |

|

| Finance income |

|

|

(8 |

) |

|

|

(12 |

) |

|

|

(18 |

) |

|

|

(23 |

) |

| Foreign exchange loss/(gain) on derivatives |

|

|

20 |

|

|

|

24 |

|

|

|

(51 |

) |

|

|

— |

|

| Foreign exchange loss/(gain) on short term deposits |

|

|

(5 |

) |

|

|

(11 |

) |

|

|

13 |

|

|

|

(20 |

) |

| Share of loss from equity accounted investees |

|

|

1 |

|

|

|

4 |

|

|

|

7 |

|

|

|

10 |

|

| Exceptional item |

|

|

245 |

|

|

|

— |

|

|

|

245 |

|

|

|

— |

|

| Other non-cash adjustments |

|

|

(1 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash flows from operating activities before changes in assets and liabilities |

|

|

548 |

|

|

|

912 |

|

|

|

1,370 |

|

|

|

2,010 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Trade receivables |

|

|

(68 |

) |

|

|

61 |

|

|

|

138 |

|

|

|

84 |

|

| Other financial assets |

|

|

9 |

|

|

|

— |

|

|

|

7 |

|

|

|

(12 |

) |

| Other current assets |

|

|

14 |

|

|

|

153 |

|

|

|

(2 |

) |

|

|

119 |

|

| Inventories |

|

|

(50 |

) |

|

|

(148 |

) |

|

|

(628 |

) |

|

|

(102 |

) |

| Other non-current assets |

|

|

(12 |

) |

|

|

(9 |

) |

|

|

(14 |

) |

|

|

(9 |

) |

| Accounts payable |

|

|

(61 |

) |

|

|

160 |

|

|

|

(613 |

) |

|

|

(254 |

) |

| Other current liabilities |

|

|

18 |

|

|

|

98 |

|

|

|

(18 |

) |

|

|

31 |

|

| Other financial liabilities |

|

|

59 |

|

|

|

7 |

|

|

|

118 |

|

|

|

(4 |

) |

| Other non-current liabilities and retirement benefit obligations |

|

|

78 |

|

|

|

34 |

|

|

|

141 |

|

|

|

80 |

|

| Provisions |

|

|

(21 |

) |

|

|

(8 |

) |

|

|

(49 |

) |

|

|

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash generated from operations |

|

|

514 |

|

|

|

1,260 |

|

|

|

450 |

|

|

|

1,981 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income tax paid |

|

|

(48 |

) |

|

|

(71 |

) |

|

|

(105 |

) |

|

|

(172 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash generated from operating activities |

|

|

466 |

|

|

|

1,189 |

|

|

|

345 |

|

|

|

1,809 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash flows used in investing activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Investment in joint ventures |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

(72 |

) |

| Movements in other restricted deposits |

|

|

— |

|

|

|

(1 |

) |

|

|

4 |

|

|

|

1 |

|

| Investment in short term deposits |

|

|

(680 |

) |

|

|

(789 |

) |

|

|

(1,488 |

) |

|

|

(1,505 |

) |

| Redemption of short term deposits |

|

|

1,065 |

|

|

|

741 |

|

|

|

1,674 |

|

|

|

1,232 |

|

| Movements in short term deposits |

|

|

385 |

|

|

|

(48 |

) |

|

|

186 |

|

|

|

(273 |

) |

| Purchases of property, plant and equipment |

|

|

(378 |

) |

|

|

(367 |

) |

|

|

(727 |

) |

|

|

(655 |

) |

| Proceeds from sale of property, plant and equipment |

|

|

— |

|

|

|

1 |

|

|

|

— |

|

|

|

1 |

|

| Cash paid for intangible assets |

|

|

(322 |

) |

|

|

(335 |

) |

|

|

(685 |

) |

|

|

(604 |

) |

| Finance income received |

|

|

9 |

|

|

|

10 |

|

|

|

20 |

|

|

|

22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash used in investing activities |

|

|

(306 |

) |

|

|

(740 |

) |

|

|

(1,202 |

) |

|

|

(1,580 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash flows from financing activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Finance expenses and fees paid |

|

|

(50 |

) |

|

|

(41 |

) |

|

|

(75 |

) |

|

|

(67 |

) |

| Proceeds from issuance of short term borrowings |

|

|

— |

|

|

|

— |

|

|

|

6 |

|

|

|

— |

|

| Repayment of short term borrowings |

|

|

(25 |

) |

|

|

(11 |

) |

|

|

(25 |

) |

|

|

(6 |

) |

| Payments of lease obligations |

|

|

(2 |

) |

|

|

(2 |

) |

|

|

(3 |

) |

|

|

(3 |

) |

| Dividends paid |

|

|

— |

|

|

|

— |

|

|

|

(150 |

) |

|

|

(150 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash used in financing activities |

|

|

(77 |

) |

|

|

(54 |

) |

|

|

(247 |

) |

|

|

(226 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net change in cash and cash equivalents |

|

|

83 |

|

|

|

395 |

|

|

|

(1,104 |

) |

|

|

3 |

|

| Cash and cash equivalents at beginning of period |

|

|

2,021 |

|

|

|

1,868 |

|

|

|

3,208 |

|

|

|

2,260 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents at end of period |

|

|

2,104 |

|

|

|

2,263 |

|

|

|

2,104 |

|

|

|

2,263 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10

Notes (forming part of the condensed consolidated financial statements)

Basis of preparation

The information for the three and six months ended 30 September 2015 is unaudited and does not constitute statutory accounts as defined in

Section 435 of the Companies Act 2006. The condensed consolidated interim financial statements of Jaguar Land Rover Automotive plc have been prepared in accordance with International Accounting Standard 34, “Interim Financial

Reporting” under IFRS as adopted by the European Union (‘EU’).

The condensed consolidated interim financial statements have been prepared

on a historical cost basis except for certain financial instruments held at fair value. These financial instrument valuations are classified as level 2 fair value measurements, as defined by IFRS 13, being those derived from inputs other than quoted

prices which are observable. There have been no changes in the valuation techniques used or transfers between fair value levels from those set out in the annual consolidated financial statements for the year ended 31 March 2015.

The condensed consolidated interim financial statements should be read in conjunction with the annual consolidated financial statements for the year ended

31 March 2015, which were prepared in accordance with IFRS as adopted by the EU. There were no differences between those financial statements and the financial statements for the group prepared under IFRS as adopted by the International

Accounting Standards Board.

The condensed consolidated interim financial statements have been prepared on the going concern basis as set out within the

directors’ statement of responsibilities section of the group’s annual report for the year ended 31 March 2015.

The accounting policies

applied are consistent with those of the annual consolidated financial statements for the year ended 31 March 2015, as described in those financial statements.

A provision against the carrying value of inventory of £245 million has

been recorded following the group’s assessment of the physical condition of the vehicles involved in the Tianjin explosion in August 2015. The process for finalising an insurance claim may take some months to conclude, so insurance and other

potential recoveries will only be recognised in future periods when paid or confirmed and have not been recognised in this period.

Due to the size of the

provision recorded the charge together with the associated tax impact has been disclosed as an exceptional item.

| 3 |

Research and development |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Three months ended |

|

|

Six months ended |

|

| |

|

30 September |

|

|

30 September |

|

|

30 September |

|

|

30 September |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| (£ millions) |

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

| Total research and development costs incurred |

|

|

381 |

|

|

|

336 |

|

|

|

760 |

|

|

|

662 |

|

| Research and development expensed |

|

|

(75 |

) |

|

|

(62 |

) |

|

|

(139 |

) |

|

|

(115 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Development costs capitalised |

|

|

306 |

|

|

|

274 |

|

|

|

621 |

|

|

|

547 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Interest capitalised |

|

|

16 |

|

|

|

29 |

|

|

|

36 |

|

|

|

59 |

|

| Research and development expenditure credit |

|

|

(18 |

) |

|

|

(13 |

) |

|

|

(36 |

) |

|

|

(26 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total internally developed intangible additions |

|

|

304 |

|

|

|

290 |

|

|

|

621 |

|

|

|

580 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11

Notes (continued)

| 4 |

Finance income and expense |

Recognised in net income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Three months ended |

|

|

Six months ended |

|

| |

|

30 September |

|

|

30 September |

|

|

30 September |

|

|

30 September |

|

| |

|

2015 |

|

|

2014 |

|

|

2015 |

|

|

2014 |

|

| (£ millions) |

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

|

(unaudited) |

|

| Finance income |

|

|

8 |

|

|

|

12 |

|

|

|

18 |

|

|

|

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total finance income |

|

|

8 |

|

|

|

12 |

|

|

|

18 |

|

|

|

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total interest expense on financial liabilities measured at amortised cost |

|

|

(40 |

) |

|

|

(33 |

) |

|

|

(74 |

) |

|

|

(71 |

) |

| Unwind of discount on provisions |

|

|

(5 |

) |

|

|

2 |

|

|

|

(10 |

) |

|

|

6 |

|

| Interest capitalised |

|

|

16 |

|

|

|

30 |

|

|

|

37 |

|

|

|

60 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total finance expense (net) |

|

|

(29 |

) |

|

|

(1 |

) |

|

|

(47 |

) |

|

|

(5 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The capitalisation rate used to calculate borrowing costs eligible for capitalisation was 4.6% (six months ended

30 September 2014: 6.0%).

| 5 |

Allowances for trade and other receivables |

Changes in the allowances for trade and other receivables

are as follows:

|

|

|

|

|

|

|

|

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| At beginning of period |

|

|

11 |

|

|

|

8 |

|

| Change in allowance during the period |

|

|

— |

|

|

|

3 |

|

| Written off |

|

|

(1 |

) |

|

|

— |

|

|

|

|

|

|

|

|

|

|

| At end of period |

|

|

10 |

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

| 6 |

Other financial assets - current |

|

|

|

|

|

|

|

|

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| Advances and other receivables recoverable in cash |

|

|

7 |

|

|

|

19 |

|

| Derivative financial instruments |

|

|

214 |

|

|

|

176 |

|

| Accrued income |

|

|

9 |

|

|

|

5 |

|

| Other |

|

|

15 |

|

|

|

14 |

|

|

|

|

|

|

|

|

|

|

| Total current other financial assets |

|

|

245 |

|

|

|

214 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| Raw materials and consumables |

|

|

89 |

|

|

|

80 |

|

| Work in progress |

|

|

379 |

|

|

|

298 |

|

| Finished goods |

|

|

2,331 |

|

|

|

2,038 |

|

|

|

|

|

|

|

|

|

|

| Total inventories |

|

|

2,799 |

|

|

|

2,416 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| Recoverable VAT |

|

|

205 |

|

|

|

221 |

|

| Prepaid expenses |

|

|

120 |

|

|

|

106 |

|

| Other |

|

|

68 |

|

|

|

69 |

|

|

|

|

|

|

|

|

|

|

| Total current other assets |

|

|

393 |

|

|

|

396 |

|

|

|

|

|

|

|

|

|

|

12

Notes (continued)

Recognised in the income statement

The income tax for the three and six month periods ended 30 September 2015 and 30 September 2014 is charged at the estimated effective tax rate

expected to apply for the applicable financial year ends.

The income tax credit/(expense) for the three and six month periods ended 30 September

2015 includes a tax credit on the exceptional item as highlighted in note 2 of £61 million.

Capital expenditure in the period was £704 million (6 month period to

30 September 2014: £755 million) on fixed assets and £705 million (6 month period to 30 September 2014: £641 million) was capitalised as intangible engineering assets (excluding the R&D tax credit). There were no

impairments, material disposals or changes in use of assets.

| 11 |

Other financial liabilities |

|

|

|

|

|

|

|

|

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| Current |

|

|

|

|

|

|

|

|

| Finance lease obligations |

|

|

6 |

|

|

|

4 |

|

| Interest accrued |

|

|

22 |

|

|

|

25 |

|

| Derivative financial instruments |

|

|

402 |

|

|

|

697 |

|

| Liability for vehicles sold under a repurchase arrangement |

|

|

260 |

|

|

|

197 |

|

| Other payables |

|

|

6 |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

696 |

|

|

|

923 |

|

|

|

|

|

|

|

|

|

|

| Non-current |

|

|

|

|

|

|

|

|

| Finance lease obligations |

|

|

4 |

|

|

|

9 |

|

| Derivative financial instruments |

|

|

465 |

|

|

|

832 |

|

| Other payables |

|

|

1 |

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

470 |

|

|

|

842 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| As at (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| Current |

|

|

|

|

|

|

|

|

| Product warranty |

|

|

409 |

|

|

|

426 |

|

| Legal and product liability |

|

|

52 |

|

|

|

50 |

|

| Provisions for residual risk |

|

|

5 |

|

|

|

4 |

|

| Provision for environmental liability |

|

|

5 |

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

| Total current provisions |

|

|

471 |

|

|

|

485 |

|

|

|

|

|

|

|

|

|

|

| Non-current |

|

|

|

|

|

|

|

|

| Product warranty |

|

|

572 |

|

|

|

585 |

|

| Provision for residual risk |

|

|

12 |

|

|

|

16 |

|

| Provision for environmental liability |

|

|

26 |

|

|

|

26 |

|

| Other employee benefits obligations |

|

|

5 |

|

|

|

12 |

|

|

|

|

|

|

|

|

|

|

| Total non-current provisions |

|

|

615 |

|

|

|

639 |

|

|

|

|

|

|

|

|

|

|

13

Notes (continued)

| 12 |

Provisions (continued) |

|

|

|

|

|

|

|

|

|

| |

|

Six months ended |

|

|

Year ended |

|

| |

|

30 September 2015 |

|

|

31 March 2015 |

|

| (£ millions) |

|

(unaudited) |

|

|

(audited) |

|

| Product warranty |

|

|

|

|

|

|

|

|

| Opening balance |

|

|

1,011 |

|

|

|

881 |

|

| Provision made during the period |

|

|

200 |

|

|

|

562 |

|

| Provision used during the period |

|

|

(237 |

) |

|

|

(430 |

) |

| Impact of discounting |

|

|

10 |

|

|

|

17 |

|

| Foreign currency translation |

|

|

(3 |

) |

|

|

(19 |

) |

|

|

|

|

|

|

|

|

|

| Closing balance |

|

|

981 |

|

|

|

1,011 |

|

|

|

|

|

|

|

|

|

|

| Legal and product liability |

|

|

|

|

|

|

|

|

| Opening balance |

|

|

50 |

|

|

|

49 |

|

| Provision made during the period |

|

|

18 |

|

|

|

18 |

|

| Provision used during the period |

|

|

(15 |

) |

|

|

(17 |

) |

| Foreign currency translation |

|

|

(1 |

) |

|

|

— |

|

|

|

|

|

|

|

|

|

|

| Closing balance |

|

|

52 |

|

|

|

50 |

|

|

|

|

|

|

|

|

|

|

| Residual risk |

|

|

|

|

|

|

|

|

| Opening balance |

|

|