UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Date of report (Date of earliest event reported)

January 28, 2016

SEACOAST BANKING CORPORATION

OF FLORIDA

(Exact Name of Registrant as Specified in

Charter)

|

Florida |

|

0-13660 |

|

59-2260678 |

|

(State or Other Jurisdiction

of Incorporation) |

|

(Commission

File Number |

|

(IRS Employer

Identification No.) |

|

815

Colorado Avenue, Stuart, FL |

|

34994 |

| (Address of Principal Executive Offices) |

|

(Zip Code) |

Registrant’s telephone number, including

area code (772) 287-4000

Check the appropriate box below if the

Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions

(see General Instruction A.2.)

| ¨ | Written communications pursuant to Rule

425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12

under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant

to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant

to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

SEACOAST BANKING CORPORATION OF FLORIDA

Item 2.02 Results of Operations and

Financial Condition

On January 28, 2016, the Seacoast Banking

Corporation of Florida (“Seacoast” or the “Company”) announced its financial results for the fourth quarter

and year ended December 31, 2015.

A copy of the press release announcing

Seacoast’s results for the fourth quarter and year ended December 31, 2015 is attached hereto as Exhibit 99.1 and incorporated

herein by reference.

Item 7.01 Regulation FD Disclosure

On January 29, 2016, Seacoast held an investor

conference call to discuss its financial results for the fourth quarter and year ended December 31, 2015. A transcript of this

conference call is attached hereto as Exhibit 99.2 and incorporated herein by reference. Also attached as Exhibit 99.3 are charts

(available on the Company’s website at www.seacoastbanking.net) containing information used in the conference call and incorporated

herein by reference. All information included in the transcript and the charts is presented as of December 31, 2015, and the Company

does not assume any obligation to correct or update said information in the future.

The information in Items 2.02 and 7.01,

as well as Exhibits 99.1, 99.2 and 99.3, is being furnished and shall not be deemed “filed” for purposes of Section

18 of the Securities Exchange Act of 1934, nor shall it be deemed incorporated by reference in any filing under the Securities

Act of 1933.

Item 9.01 Financial Statements and

Exhibits

(d) Exhibits

| Exhibit

No. |

|

Description |

| |

|

|

| 99.1 |

|

Press Release dated January 28, 2016 with respect to Seacoast’s

financial results for the fourth quarter and year ended December 31, 2015

|

| |

|

|

| 99.2 |

|

Transcript of Seacoast’s investor conference

call held on January 29, 2016 to discuss the Company’s financial results for the fourth quarter and year ended December

31, 2015 |

| |

|

|

| 99.3 |

|

Data on website containing information used in the

conference call held on January 29, 2016 |

Exhibits 99.1, 99.2 and 99.3 referenced

herein contain “forward-looking statements” within the meaning of Section 28A of the Securities Act of 1933 and Section

21E of the Securities Exchange Act of 1934, including, without limitation, statements about future financial and operating results,

ability to realized deferred tax assets, cost savings, enhanced revenues, economic and seasonal conditions in our markets, and

improvements to reported earnings that may be realized from cost controls and for integration of banks that we have acquired, as

well as statements with respect to Seacoast’s objectives, expectations and intentions and other statements that are not historical

facts. Actual results may differ from those set forth in the forward-looking statements.

Forward-looking statements include statements

with respect to our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions, and involve known

and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause the actual results, performance

or achievements of Seacoast to be materially different from future results, performance or achievements expressed or implied by

such forward-looking statements. You should not expect us to update any forward-looking statements.

You can identify these forward-looking

statements through our use of words such as “may,” “will,” “anticipate,” “assume,”

“should,” “support”, “indicate,” “would,” “believe,” “contemplate,”

“expect,” “estimate,” “continue,” “further”, “point to,” “project,”

“could,” “intend” or other similar words and expressions of the future. These forward-looking statements

may not be realized due to a variety of factors, including, without limitation: the effects of future economic and market conditions,

including seasonality; governmental monetary and fiscal policies, as well as legislative, tax and regulatory changes; changes in

accounting policies, rules and practices; the risks of changes in interest rates on the level and composition of deposits, loan

demand, liquidity and the values of loan collateral, securities, and interest sensitive assets and liabilities; interest rate risks,

sensitivities and the shape of the yield curve; the effects of competition from other commercial banks, thrifts, mortgage banking

firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual

funds and other financial institutions operating in our market areas and elsewhere, including institutions operating regionally,

nationally and internationally, together with such competitors offering banking products and services by mail, telephone, computer

and the Internet; and the failure of assumptions underlying the establishment of reserves for possible loan losses. The risks of

mergers and acquisitions, include, without limitation: unexpected transaction costs, including the costs of integrating operations;

the risks that the businesses will not be integrated successfully or that such integration may be more difficult, time-consuming

or costly than expected; the potential failure to fully or timely realize expected revenues and revenue synergies, including as

the result of revenues following the merger being lower than expected; the risk of deposit and customer attrition; any changes

in deposit mix; unexpected operating and other costs, which may differ or change from expectations; the risks of customer and employee

loss and business disruption, including, without limitation, as the result of difficulties in maintaining relationships with employees;

increased competitive pressures and solicitations of customers by competitors; as well as the difficulties and risks inherent with

entering new markets.

All written or oral forward-looking statements

attributable to us are expressly qualified in their entirety by this cautionary notice, including, without limitation, those risks

and uncertainties described in our annual report on Form 10-K for the year ended December 31, 2014 under “Special Cautionary

Notice Regarding Forward-Looking Statements” and “Risk Factors”, and otherwise in our SEC reports and filings.

Such reports are available upon request from the Company, or from the Securities and Exchange Commission, including through the

SEC’s Internet website at http://www.sec.gov.

SIGNATURES

Pursuant to the

requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the

undersigned hereunto duly authorized.

| |

SEACOAST BANKING CORPORATION OF FLORIDA |

| |

(Registrant) |

| Date: February 3, 2016 |

|

By: |

/s/ Stephen Fowle |

| |

|

|

Stephen Fowle |

| |

|

|

Executive Vice President and Chief Financial Officer |

EXHIBIT INDEX

| Exhibit No. |

|

Description |

| |

|

|

| 99.1 |

|

Press Release dated January 28, 2016 with respect to Seacoast’s

financial results for the fourth quarter and year ended December 31, 2015

|

| 99.2 |

|

Transcript of Seacoast’s investor conference call held

on January 29, 2016 to discuss the Company’s financial results for the fourth quarter and year ended December 31, 2015

|

| 99.3 |

|

Data on website containing information used in the conference

call held on January 29, 2016

|

EXHIBIT 99.1

To Form 8-K dated January 28, 2016

SEACOAST BANKING CORPORATION OF FLORIDA

NEWS RELEASE

CONTACTS:

Stephen

Fowle, EVP and CFO

(772) 463-8977

steve.fowle@seacoastbank.com

Seacoast

Reports Full Year and Fourth Quarter 2015 Results

Full

Year 2015 EPS Rose 214% to $0.66

Double-Digit

Loan Growth Drove Fourth Quarter Adjusted EPS1 to $0.19, Compared With $0.13 in Q4 2014

Fourth Quarter 2015 Earnings

Highlights

| · | Adjusted revenues increased $5.0 million

or 16% year-over-year to $36.9 million. |

| · | Net interest margin increased eleven basis

points year-over-year to 3.67%. |

| · | Net interest income improved $4.4 million

or 18% largely due to organic loan growth. |

| · | Adjusted

net income1 increased 56% to $6.5 million or $0.19 per diluted share, compared to $4.2 million or $0.13 per diluted

share in the fourth quarter 2014. |

| · | Adjusted return on tangible common equity

improved to 8.4% from 6.2% year-over-year. |

Fourth Quarter 2015 Growth

Highlights

| · | Loans increased $57 million or 3% not

annualized, compared to third quarter 2015 and rose 18% year-over-year. Excluding acquisitions, loans increased $218 million or

12% above year-ago levels. |

| · | Strategic initiatives continue to pay

off. Excluding acquisitions, households grew 5% year-over-year and consumer loans originated outside the branch hit a record 26%

during the fourth quarter. |

| · | Successful integration of Grand Bank and

BankFIRST franchises resulted in net household growth by the third month as opposed to net attrition typical for acquisitions. |

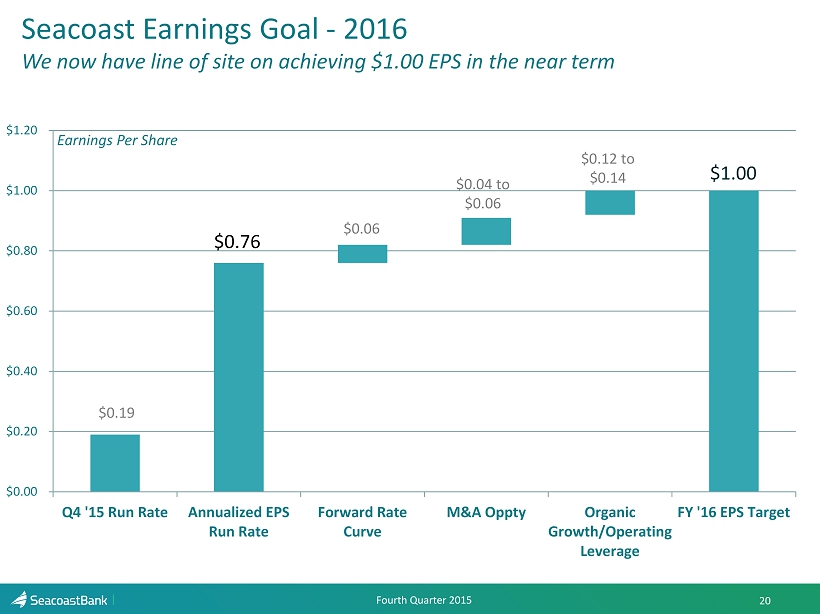

2016 Guidance

| · | Seacoast provided 2016 adjusted diluted

EPS target of $1.00. |

1 Non-GAAP

measure, see “Explanation of Certain Unaudited Non-GAAP Financial Measures”

STUART, Fla., January 28, 2016 /PRNewswire/

— Seacoast Banking Corporation of Florida (NASDAQ: SBCF) today reported results for the fourth quarter and full year 2015.

Fourth quarter 2015 net income increased

to $6.0 million compared to a net loss of $1.5 million reported in the same period of the prior year. Adjusted net income1

increased $2.3 million, or 56%, from year-ago levels. Diluted earnings per common share (EPS) were $0.18 and adjusted diluted

EPS1 were $0.19 in the fourth quarter, compared to adjusted diluted EPS of $0.13 in the fourth quarter of 2014 and

$0.19 in the third quarter of 2015.

Dennis S. Hudson, III, Chairman and CEO

said, “Our sustained execution of Seacoast’s balanced growth strategy produced another quarter of strong results, measured

by increases in loans, deposits and households. The combination of organic and acquired growth in 2015 and our significant operating

leverage led to nearly 60% growth in core EPS, reinforcing our conviction that our continued execution of Seacoast’s long-term

strategy positions us well to produce strong results for shareholders.”

Seacoast’s earnings improvement reflected

continued strong business growth and execution of digital and other strategic initiatives, supplemented by successful acquisitions.

Fourth quarter net income included a $416,000 bargain purchase gain from the acquisition of the Grand Bankshares, arising from

unanticipated recoveries and resulting valuation adjustments to loans and other real estate owned (OREO) realized in the fourth

quarter.

Full-year 2015 net income improved $16.4

million to $22.2 million and fully diluted earnings per share increased 214% to $0.66 compared with $0.21 per diluted common share

in 2014. Adjusted net income1 increased to $25.3 million, or $0.75 per diluted share, in 2015 from $13.0 million, or

$0.47 per diluted share, in 2014.

Hudson added, “We believe that community

banking is undergoing a revolution and we plan to be at the forefront of refining the user experience to the benefit of our customers.

Exiting the Great Recession, we recognized that a fundamental shift in community banking had taken place, and we began to invest

for a new future. We introduced Seacoast’s Accelerate commercial banking model in 2011, and in 2013 began to invest in analytics,

digital servicing capabilities and digital marketing talent and technology. These investments in our future drove our 16% revenue

growth in 2015, with loans increasing at a 12% organic rate and households rising 5% year-over-year.

“Seacoast is building a fully integrated

distribution platform across all channels to provide our customers with the ability to choose their path of convenience to satisfy

their banking needs. In 2015, we rolled out integrated digital marketing, automated cross sell, and deeper customer analytics

which are creating shareholder value as we move forward. Additionally, we are making trade-offs by reinvesting a portion

of the cost savings related to consolidating branch locations and more efficient business processes into new and innovative ways

to serve and grow our customer base. In 2015, we fully absorbed incremental costs needed to support better channel integration

including the expansion of our 24/7 call center, that now originates over 10% of our deposit relationships and almost 30% of our

consumer loan production. Looking forward, we expect our digital and phone based channels to expand dramatically.

“As our upgraded technology platform

enabled us to effectively adapt to changes in consumer banking behavior, we were able to close three branches during 2015 with

minimal customer impact; in fact household growth continued to accelerate during the year. We are currently in the process of consolidating

an additional four legacy locations in the first half of 2016.

“While we remained disciplined in

executing an organic-growth focused strategy, our recent acquisitions have boosted our growth trajectory. Our convenient service

model and enhanced product offerings, especially digital banking, allowed us to grow our acquired banks’ households and further

cross-sell additional products to our newly acquired customers. Specifically, our recently acquired BankFIRST (Orlando) and Grand

Bankshares (Palm Beach County) franchises attained net household growth within three months of acquisition, and Orlando increased

households at a rate above 7% in 2015.”

Hudson concluded, “We look to 2016

with confidence as we continue to execute on our long term strategy, investing in important initiatives, managing expenses and

executing on the right acquisition opportunities. As a result, we have provided an adjusted diluted EPS outlook target of $1.00

for the year. We look forward to discussing this goal with shareholders on our Q4 earnings call.”

FINANCIAL HIGHLIGHTS

(Dollars in thousands except per share data) | |

4Q15 | | |

3Q15 | | |

2Q15 | | |

1Q15 | | |

4Q14 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total Assets | |

$ | 3,534,780 | | |

$ | 3,378,108 | | |

$ | 3,233,588 | | |

$ | 3,231,956 | | |

$ | 3,093,335 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loans | |

| 2,156,330 | | |

| 2,099,447 | | |

| 1,937,399 | | |

| 1,854,487 | | |

| 1,821,885 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Deposits | |

| 2,844,387 | | |

| 2,742,296 | | |

| 2,605,177 | | |

| 2,609,825 | | |

| 2,416,534 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net Income (Loss) | |

| 6,036 | | |

| 4,441 | | |

| 5,805 | | |

| 5,859 | | |

| (1,517 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Diluted Earnings Per Share | |

| 0.18 | | |

| 0.13 | | |

| 0.18 | | |

| 0.18 | | |

| (0.05 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Return on Average Assets (ROA) | |

| 0.69 | % | |

| 0.52 | % | |

| 0.72 | % | |

| 0.75 | % | |

| (0.20 | )% |

| Return on Average Tangible Common Equity (ROTCE) | |

| 7.8 | | |

| 5.9 | | |

| 8.2 | | |

| 8.5 | | |

| (1.7 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net Interest Margin | |

| 3.67 | | |

| 3.75 | | |

| 3.50 | | |

| 3.62 | | |

| 3.56 | |

| Efficiency Ratio | |

| 72.6 | | |

| 76.3 | | |

| 68.6 | | |

| 68.3 | | |

| 104.5 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Pretax, Pre-provision Income (1) | |

$ | 10,130 | | |

$ | 8,126 | | |

$ | 10,224 | | |

$ | 9,832 | | |

$ | (2,029 | ) |

| Average Diluted Shares Outstanding (000) | |

| 34,395 | | |

| 34,194 | | |

| 33,234 | | |

| 33,136 | | |

| 33,124 | |

| Adjusted Net Income (1) | |

$ | 6,520 | | |

$ | 6,433 | | |

$ | 6,172 | | |

$ | 6,177 | | |

$ | 4,179 | |

| Adjusted Diluted Earnings Per Share (1) | |

| 0.19 | | |

| 0.19 | | |

| 0.19 | | |

| 0.19 | | |

| 0.13 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Adjusted ROA (1) | |

| 0.75 | % | |

| 0.76 | % | |

| 0.77 | % | |

| 0.79 | % | |

| 0.55 | % |

| Adjusted ROTCE (1) | |

| 8.4 | | |

| 8.5 | | |

| 8.7 | | |

| 9.0 | | |

| 6.2 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Adjusted Efficiency Ratio (1) | |

| 69.1 | | |

| 68.2 | | |

| 67.5 | | |

| 67.5 | | |

| 74.8 | |

| Adjusted Pretax, Pre-provision Income (1) | |

$ | 10,913 | | |

$ | 11,328 | | |

$ | 10,815 | | |

$ | 10,342 | | |

$ | 7,464 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Annualized Adjusted Operating Expenses as a Percent of Average Assets (1) | |

| 2.93 | % | |

| 3.03 | % | |

| 2.91 | % | |

| 2.88 | % | |

| 3.13 | % |

Acquisitions Update

Hudson noted, “We continue to be

encouraged by results from our recent acquisitions. In Orlando, we achieved growth levels in excess of our already-strong franchise

growth rate as we delivered our service and product offerings to the BankFIRST customer base. Acquisitions in the asset-based lending

space and in demographically-strong Palm Beach County have helped us further propel growth. We are pleased with our ability to

execute against our commitments.

“We look forward to welcoming more

than 5,000 customers of Floridian Bankshares and nearly 9,000 customers from BMO Harris’ Orlando banking operations in the

first part of 2016. We are pleased to announce that we have received regulatory approval for both of these transactions and expect

to close the Floridian acquisition late in the first quarter and the BMO Harris branch purchase late in the second quarter, subject

in both instances to customary closing conditions.”

Florida Economic Update

"The strong Florida economy continues

to amplify our success," said Hudson.

Wells Fargo Securities Group’s December

18, 2015 report titled, “Florida Employment Update: November 2015” stated, “Florida’s economy is firing

on all cylinders…Florida added a nation-leading 35,200 jobs in November, which marks the largest monthly job gain for the

Sunshine State since May 2010. On a year-to-date basis, nonfarm employment has risen 3.0 percent, resulting in a net gain of 239,600

jobs.”

Comerica Bank’s Comerica Economic

Insights report dated January 5, 2016 stated, “Our Florida Economic Activity Index increased again in October, for the 19th

consecutive month. Most components of the index were positive in October. Only state exports and housing starts were negative for

the month. The Florida economy is firmly re-established as a growth leader for the U.S….we see no reason for the positive

trend to change in the near term.”

Fourth Quarter 2015 Income Statement

Highlights

Balance Sheet Mix, Driven by Growth

in Relationship Customers and Improved Yields, Fuel Net Interest Income and Margin Expansion

Net interest income for the quarter totaled

$29.1 million, a $4.4 million or 18% increase from fourth quarter 2014 levels. Net interest margin expanded to 3.67%, an eleven

basis point increase from the prior year. Year-over-year net interest income and margin increases reflect improvement in rate and

balance sheet mix, largely due to growth in customer relationships.

Net interest income increased $0.1 million

and net interest margin decreased eight basis points from 3.75% in the prior quarter. Linked quarter results reflect an accelerated

level of purchase loan accretion in the third quarter of 2015 that contributed approximately 10 basis points of margin during that

quarter. Strong loan growth and improved core yields more than compensated for a decrease in purchased loan accretion. Fourth quarter

results included essentially no excess purchased loan accretion.

Noninterest Income Growth Reflects Increases

in Households

Noninterest income excluding securities

gains and the bargain purchase gain, totaled $7.8 million for the fourth quarter, an increase of $641,000 or 9% from a year ago.

Most categories of service fee income showed year-over-year growth with interchange income up a strong 24%, indicating continued

strength in customer acquisition and cross sell and benefits from acquisition activity.

Noninterest income, excluding securities

gains and the bargain purchase gain related to the Grand Bankshares acquisition, decreased $300,000 from third quarter 2015 levels.

Strength in interchange income and smaller increases in many other categories were offset by decreases in mortgage banking, brokerage

and marine income, which were negatively impacted by low activity during the holiday season.

As mentioned previously, fourth quarter

net income included a $416,000 bargain purchase gain from the acquisition of the Grand Bankshares, arising from unanticipated recoveries

and resulting valuation adjustments to loans and other real estate owned (OREO) realized in the fourth quarter.

Noninterest Expense Continues to Show

Strong Operating Leverage and Investment in Seacoast Strategy

Noninterest expense decreased $6.8 million

from the fourth quarter 2014. Prior year expenses reflected significant non-recurring costs related to the acquisition of The BANKshares

on October 1, 2014 and other one-time costs. Adjusted noninterest expense1 increased $1.6 million from prior-year levels.

The year-over-year increase in adjusted expense reflects ongoing costs related to the acquisitions of FGC and Grand Bankshares,

particularly in added salary and benefits, which increased $666,000 or 5%, and occupancy and furniture and equipment costs, which

increased $265,000 or 9%. Increases also reflect variable costs related to strong organic franchise growth, particularly in data

processing costs, which increased $588,000 or 31%, an investment made to further the company’s strategy.

Noninterest expense decreased $2.0 million

from the third quarter, 2015. Excluding merger related charges and other one-time items, adjusted noninterest expense1

grew $200,000, or less than 1%. Increases in occupancy ($108,000) and data processing costs ($178,000) were partially offset by

decreases in salary and benefits ($110,000). These fluctuations represent normal expense volatility.

Seacoast’s efficiency ratio was 72.6%

in fourth quarter of 2015, down from 104.5% in the fourth quarter of 2014 and below 76.3% in the third quarter of 2015. Adjusted1,

the efficiency ratio decreased to 69.3% in the fourth quarter of 2015 from 74.8% in the fourth quarter of 2014 and up slightly

from 68.2% in the third quarter of 2015. Linked-quarter increase was impacted by the significant amount of accelerated purchased

loan accretion recorded in the third quarter of 2015, whereas fourth quarter results included essentially no excess purchased loan

accretion.

Fourth Quarter 2015 Balance Sheet Highlights

Deposit Growth Reflects Success of Core

Customer Increase and Acquisitions

Total deposits increased 18% to $2.84 billion

at December 31, 2015, from year ago levels. Core customer funding increased to $2.72 billion at December 31, 2015, a $476 million,

or 21% increase from the fourth quarter of 2014. Excluding acquisitions, core customer funding increased by $286 million or 13%

from one year ago and total deposits increased $239 million or 10% from one year ago. Total deposits grew $102 million or 4% (not

annualized) and core customer funding increased $138 million or 5% (not annualized) compared to the prior quarter. Linked-quarter

increases were largely due to normal seasonal growth in public funds.

Noninterest demand deposits grew $129.2

million, or 18% from the fourth quarter of 2014 and remained at a strong 30.0% of total deposits.

| (Dollars in thousands) | |

Fourth

Quarter

2015 | | |

Third

Quarter

2015 | | |

Second

Quarter

2015 | | |

First

Quarter

2015 | | |

Fourth

Quarter

2014 | |

| Customer Relationship Funding | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest demand | |

$ | 854,447 | | |

$ | 869,877 | | |

$ | 808,429 | | |

$ | 793,336 | | |

$ | 725,238 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing demand | |

| 734,749 | | |

| 618,344 | | |

| 599,268 | | |

| 634,854 | | |

| 652,353 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Money market | |

| 665,353 | | |

| 660,632 | | |

| 621,973 | | |

| 596,600 | | |

| 450,172 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Savings | |

| 295,851 | | |

| 286,810 | | |

| 282,588 | | |

| 272,963 | | |

| 264,738 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Time certificates of deposit | |

| 293,987 | | |

| 306,633 | | |

| 292,919 | | |

| 312,072 | | |

| 324,033 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total deposits | |

$ | 2,844,387 | | |

$ | 2,742,296 | | |

$ | 2,605,177 | | |

$ | 2,609,825 | | |

$ | 2,416,534 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Customer sweep accounts | |

$ | 172,005 | | |

$ | 148,607 | | |

$ | 157,676 | | |

$ | 170,023 | | |

$ | 153,640 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total core customer funding (2) | |

$ | 2,722,405 | | |

$ | 2,584,270 | | |

$ | 2,469,934 | | |

$ | 2,467,776 | | |

$ | 2,246,141 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Demand deposit mix (noninterest bearing) | |

| 30.0 | % | |

| 31.7 | % | |

| 31.0 | % | |

| 30.4 | % | |

| 30.0 | % |

(2)Total deposits and customer

sweep accounts, excluding time certificates of deposit.

Loans Up Substantially from Acquisition

and Strong Core Growth

Total loans were $2.16 billion at December

31, 2015, an increase of $334 million or 18% from a year ago. Excluding acquired loans, loans increased $218 million or 12% from

the prior year’s fourth quarter. Loans increased a strong $57 million or 3% (not annualized) from third quarter levels.

Loan growth continued across all business

lines. Commercial loan originations for the quarter were $80 million with the commercial pipeline (in underwriting and approval

or approved and not yet closed) totaling a strong $106 million at December 31, 2015 increasing from prior quarter and well in excess

of recent history. Consumer loan and small business originations (inclusive of lines of credit) totaled $54 million in the fourth

quarter of 2015 compared to $28 million one year ago.

Closed residential production for the quarter

totaled $60.2 million compared with $57.9 million a year ago, with a total residential pipeline of $30.3 million at December 31,

2015 up from $21.4 million one year ago.

| (Dollars in thousands) | |

4Q15 | | |

3Q15 | | |

2Q15 | | |

1Q15 | | |

4Q14 | |

| | |

| | |

| | |

| | |

| | |

| |

| Commercial pipeline | |

$ | 105,556 | | |

$ | 104,915 | | |

$ | 108,538 | | |

$ | 82,143 | | |

$ | 60,136 | |

| Commercial loans closed | |

| 80,003 | | |

| 71,823 | | |

| 85,815 | | |

| 61,357 | | |

| 94,719 | |

| Total Commercial loan originations and pipeline | |

$ | 185,559 | | |

$ | 176,738 | | |

$ | 194,353 | | |

$ | 143,500 | | |

$ | 154,855 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Residential pipeline | |

$ | 30,340 | | |

$ | 37,958 | | |

$ | 53,902 | | |

$ | 48,485 | | |

$ | 21,351 | |

| Residential loans retained | |

| 24,905 | | |

| 36,027 | | |

| 45,596 | | |

| 23,951 | | |

| 31,598 | |

| Residential loans sold | |

| 35,278 | | |

| 37,996 | | |

| 36,182 | | |

| 31,896 | | |

| 26,336 | |

| Total Residential loan originations and pipeline | |

$ | 90,523 | | |

$ | 111,981 | | |

$ | 135,680 | | |

$ | 104,332 | | |

$ | 79,285 | |

Other Highlights

Credit Quality Remains Stable with Growth

Trends

The provision for loan losses was $369,000

for the fourth quarter of 2015, up from $118,000 in the fourth quarter 2014 and below $987,000 recorded in the third quarter 2015.

The fourth quarter provision reflects continued strong credit metrics, offset by continued loan growth. The third quarter provision

was also impacted by $655,000 related to a single purchased credit impaired loan performing below our initial expectations. The

allowance for loan losses for non-acquired loans was 1.03% of total loans, compared to 1.11% in the third quarter 2015.

Additional highlights include:

| · | Nonperforming loans to total loans outstanding

at the end of the fourth quarter remained at a clean 0.8%, down from 1.2% at year-end 2014; |

| · | Nonperforming assets to total assets declined

to 0.7%, compared to 0.9% a year ago. |

Capital Ratios Continue to Improve from

Earnings Momentum

Capital ratios remain healthy and well

above regulatory requirements for well-capitalized institutions. The common equity tier 1 capital ratio (CET1) is estimated at

13.3% and the total capital ratio is estimated at 16.0% at December 31, 2015. The tier 1 leverage ratio is estimated at 10.7% at

December 31, 2015.

Tangible book value per share increased

$0.13 to $9.31 and book value per share increased $0.09 to $10.29 at December 31, 2015, as earnings more than offset decreases

in AFS securities valuation at the end of the 2015 year. Average tangible common equity to assets was a strong 9.3% at December

31, 2015.

Conference Call Information

Seacoast will host a conference call on

Friday, January 29, 2016 at 10:00 a.m. (Eastern Time) to discuss the earnings results. Investors may call in (toll-free) by dialing

(888) 517-2513 (passcode: 7021 952; host: Dennis S. Hudson). Slides will be used during the conference call and may be accessed

at Seacoast's website at SeacoastBanking.com by selecting "Presentations" under the heading "Investor Services."

A replay of the call will be available for one month, beginning late afternoon of January 29, by dialing (888) 843-7419 (domestic),

using the passcode 7021 952.

Alternatively, individuals may listen to

the live webcast of the presentation by visiting Seacoast's website at SeacoastBanking.com. The link is located in the subsection

"Presentations" under the heading "Investor Services." Beginning the afternoon of January 29, an archived version

of the webcast can be accessed from this same subsection of the website. The archived webcast will be available for one year.

About Seacoast Banking Corporation of

Florida (NASDAQ: SBCF)

Seacoast Banking Corporation of Florida

is one of the largest community banks headquartered in Florida with approximately $3.5 billion in assets and $2.8 billion in deposits

as of December 31, 2015. The Company provides integrated financial services including commercial and retail banking, wealth management,

and mortgage services to customers through advanced banking solutions, 43 traditional branches of its locally-branded wholly-owned

subsidiary bank, Seacoast Bank, and five commercial banking centers. Offices stretch from Ft. Lauderdale, Boca Raton and West Palm

Beach north through the Space Coast of Florida, into Orlando and Central Florida, and west to Okeechobee and surrounding counties.

More information about the Company is available at SeacoastBanking.com.

Sources:

https://www08.wellsfargomedia.com/assets/pdf/commercial/insights/economics/regional-reports/fl-employment-20151218.pdf

http://blog.comerica.com/2016/01/05/comerica-banks-florida-index-continues-solid-gains/

Cautionary Notice Regarding Forward-Looking

Statements

This press release contains "forward-looking

statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act

of 1934, including, without limitation, statements about future financial and operating results, cost savings, enhanced revenues,

economic and seasonal conditions in our markets, and improvements to reported earnings that may be realized from cost controls

and for integration of banks that we have acquired, or expect to acquire, as well as statements with respect to Seacoast's objectives,

expectations and intentions and other statements that are not historical facts. Actual results may differ from those set forth

in the forward-looking statements.

Forward-looking statements include statements

with respect to our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions, and involve known

and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause the actual results, performance

or achievements of Seacoast to be materially different from future results, performance or achievements expressed or implied by

such forward-looking statements. You should not expect us to update any forward-looking statements.

You can identify these forward-looking

statements through our use of words such as "may," "will," "anticipate," "assume," "should,"

"support", "indicate," "would," "believe," "contemplate," "expect,"

"estimate," "continue," "further", "point to," "project," "could,"

"intend" or other similar words and expressions of the future. These forward-looking statements may not be realized due

to a variety of factors, including, without limitation: the effects of future economic and market conditions, including seasonality;

governmental monetary and fiscal policies, as well as legislative, tax and regulatory changes; changes in accounting policies,

rules and practices; the risks of changes in interest rates on the level and composition of deposits, loan demand, liquidity and

the values of loan collateral, securities, and interest sensitive assets and liabilities; interest rate risks, sensitivities and

the shape of the yield curve; the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer

finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other

financial institutions operating in our market areas and elsewhere, including institutions operating regionally, nationally and

internationally, together with such competitors offering banking products and services by mail, telephone, computer and the Internet;

and the failure of assumptions underlying the establishment of reserves for possible loan losses. The risks of mergers and acquisitions,

include, without limitation: unexpected transaction costs, including the costs of integrating operations; the risks that the businesses

will not be integrated successfully or that such integration may be more difficult, time-consuming or costly than expected; the

potential failure to fully or timely realize expected revenues and revenue synergies, including as the result of revenues following

the merger being lower than expected; the risk of deposit and customer attrition; any changes in deposit mix; unexpected operating

and other costs, which may differ or change from expectations; the risks of customer and employee loss and business disruption,

including, without limitation, as the result of difficulties in maintaining relationships with employees; increased competitive

pressures and solicitations of customers by competitors; as well as the difficulties and risks inherent with entering new markets.

All written or oral forward-looking

statements attributable to us are expressly qualified in their entirety by this cautionary notice, including, without limitation,

those risks and uncertainties described in our annual report on Form 10-K for the year ended December 31, 2014, under "Special

Cautionary Notice Regarding Forward-looking Statements" and "Risk Factors", and otherwise in our SEC reports and

filings. Such reports are available upon request from the Company, or from the Securities and Exchange Commission, including through

the SEC's Internet website at http://www.sec.gov.

Important information for Investors and Shareholders

Seacoast has filed a registration statement

on Form S-4 and amendments thereto containing a definitive Proxy Statement/Prospectus with the SEC regarding the proposed merger

with Floridian into Seacoast. On or about January 22, 2016, this Proxy Statement/Prospectus was mailed to Floridian shareholders.

INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS REGARDING THE PROPOSED MERGER AND OTHER DOCUMENTS

FILED BY SEACOAST WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS WHEN

THEY BECOME AVAILABLE, BECAUSE THEY DO OR WILL CONTAIN IMPORTANT INFORMATION.

Investors can obtain a free copy of

the Proxy Statement/Prospectus, as well as other filings containing information about Seacoast and Floridian, at the SEC’s

website (http://www.sec.gov), with respect to information about Seacoast, and Floridian’s website (www.floridianbank.com),

with respect to information about Floridian. Investors can also obtain these documents, free of charge, at http://www.seacoastbanking.com

under the tab “Investor Relations” and then under the tab “Financials/Regulatory Filings.” Copies

of the Proxy Statement/Prospectus and any other filing by Seacoast with the SEC can also be obtained, free of charge, by directing

a request to Investor Relations, 815 Colorado Avenue, P.O. Box 9012, Stuart, FL 34994, (772) 288-6085.

Seacoast, Floridian, their respective

directors and executive officers and other members of management and employees may be considered participants in the solicitation

of proxies in connection with the proposed transaction. Information about the directors and executive officers of Seacoast is set

forth in its proxy statement for its 2015 annual meeting of shareholders, which was filed with the SEC on April 7, 2015 and its

Current Reports on Form 8-K. Other information regarding the participants in the proxy solicitation and a description of their

direct and indirect interests, by security holdings or otherwise, is contained in the Proxy Statement/Prospectus. You may

obtain free copies of these documents as described in the preceding paragraph.

Explanation of Certain Unaudited Non-GAAP Financial Measures

This press release contains financial information

determined by methods other than Generally Accepted Accounting Principles ("GAAP"). The financial highlights provide

reconciliations between GAAP net income and adjusted net income, GAAP income and adjusted pretax, pre-provision income. Management

uses these non-GAAP financial measures in its analysis of the Company's performance and believes these presentations provide useful

supplemental information, and a clearer understanding of the Company's performance. The Company believes the non-GAAP measures

enhance investors' understanding of the Company's business and performance. These measures are also useful in understanding performance

trends and facilitate comparisons with the performance of other financial institutions. The limitations associated with operating

measures are the risk that persons might disagree as to the appropriateness of items comprising these measures and that different

companies might calculate these measures differently. The Company provides reconciliations between GAAP and these non-GAAP measures.

These disclosures should not be considered an alternative to GAAP.

To better evaluate its earnings, the Company

removes certain items to arrive at adjusted net income, adjusted pretax, pre-provision income and adjusted diluted earnings per

share (non-GAAP measures) as detailed in the table below:

| (Dollars in thousands except per share data) | |

Fourth

Quarter

2015 | | |

Third

Quarter

2015 | | |

Second

Quarter

2015 | | |

First

Quarter

2015 | | |

Fourth

Quarter

2014 | |

| | |

| | |

| | |

| | |

| | |

| |

| Net income | |

$ | 6,036 | | |

$ | 4,441 | | |

$ | 5,805 | | |

$ | 5,859 | | |

($ | 1,517 | ) |

| Severance | |

| 187 | | |

| 98 | | |

| 29 | | |

| 12 | | |

| 478 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Merger related charges | |

| 1,043 | | |

| 2,692 | | |

| 337 | | |

| 275 | | |

| 2,722 | |

| Bargain purchase gain | |

| (416 | ) | |

| 0 | | |

| 0 | | |

| 0 | | |

| 0 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Branch closure charges and costs related to expense initiatives | |

| 0 | | |

| 121 | | |

| 0 | | |

| 0 | | |

| 4,261 | |

| Marketing and brand refresh expense | |

| 0 | | |

| 0 | | |

| 0 | | |

| 0 | | |

| 697 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Stock compensation expense and other incentive costs related to improved outlook | |

| 0 | | |

| 0 | | |

| 0 | | |

| 0 | | |

| 1,213 | |

| Securities (gains) | |

| (1 | ) | |

| (160 | ) | |

| 0 | | |

| 0 | | |

| (108 | ) |

| Miscellaneous losses | |

| 48 | | |

| 112 | | |

| 0 | | |

| 0 | | |

| 119 | |

| Net loss on OREO and repossessed assets | |

| (157 | ) | |

| 262 | | |

| 53 | | |

| 81 | | |

| 9 | |

| Asset dispositions expense | |

| 79 | | |

| 77 | | |

| 173 | | |

| 143 | | |

| 103 | |

| Effective tax rate on adjustments | |

| (299 | ) | |

| (1,210 | ) | |

| (225 | ) | |

| (193 | ) | |

| (3,798 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Adjusted Net Income (1) | |

| 6,520 | | |

| 6,433 | | |

| 6,172 | | |

| 6,177 | | |

| 4,179 | |

| Provision for loan losses | |

| 369 | | |

| 987 | | |

| 855 | | |

| 433 | | |

| 118 | |

| Income taxes | |

| 4,024 | | |

| 3,908 | | |

| 3,788 | | |

| 3,732 | | |

| 3,167 | |

| Adjusted pretax, pre-provision income (1) | |

$ | 10,913 | | |

$ | 11,328 | | |

$ | 10,815 | | |

$ | 10,342 | | |

$ | 7,464 | |

| Adjusted earnings per diluted share (1) | |

$ | 0.19 | | |

$ | 0.19 | | |

$ | 0.19 | | |

$ | 0.19 | | |

$ | 0.13 | |

| Average shares outstanding (000) | |

| 34,395 | | |

| 34,194 | | |

| 33,234 | | |

| 33,136 | | |

| 33,124 | |

| FINANCIAL HIGHLIGHTS |

(Unaudited) |

02/02/16 |

| SEACOAST BANKING CORPORATION OF FLORIDA AND SUBSIDIARIES |

| (Dollars in thousands, except share data) | |

Three Months Ended | | |

Twelve Months Ended | |

| | |

December 31, | | |

September 30, | | |

December 31, | | |

December 31, | | |

December 31, | |

| | |

2015 | | |

2015 | | |

2014 | | |

2015 | | |

2014 | |

| Summary of Earnings | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income (loss) | |

$ | 6,036 | | |

$ | 4,441 | | |

$ | (1,517 | ) | |

$ | 22,141 | | |

$ | 5,696 | |

| Net interest income (1) | |

| 29,216 | | |

| 29,130 | | |

| 24,883 | | |

| 109,968 | | |

| 75,221 | |

| Net interest margin (1), (2) | |

| 3.67 | | |

| 3.75 | | |

| 3.56 | | |

| 3.64 | | |

| 3.25 | |

| | |

| | | |

| | | |

| | | |

| | | |

| . | |

| Performance Ratios | |

| | | |

| | | |

| | | |

| | | |

| | |

| Return on average assets-GAAP basis (2), (3) | |

| 0.69 | % | |

| 0.52 | % | |

| (0.20 | )% | |

| 0.67 | % | |

| 0.23 | % |

| Return on average shareholders' equity-GAAP basis (2), (3) | |

| 6.78 | | |

| 5.05 | | |

| (1.89 | ) | |

| 6.56 | | |

| 2.22 | |

| Return on average tangible shareholders' equity-GAAP basis (2), (3), (4) | |

| 7.83 | | |

| 5.94 | | |

| (1.71 | ) | |

| 7.59 | | |

| 2.57 | |

| Efficiency ratio (5) | |

| 72.57 | | |

| 76.29 | | |

| 104.46 | | |

| 71.58 | | |

| 91.57 | |

| Noninterest income to total revenue | |

| 21.10 | | |

| 21.79 | | |

| 22.40 | | |

| 22.63 | | |

| 24.83 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Per Share Data | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income (loss) diluted-GAAP basis | |

$ | 0.18 | | |

$ | 0.13 | | |

$ | (0.05 | ) | |

$ | 0.66 | | |

$ | 0.21 | |

| Net income (loss) basic-GAAP basis | |

| 0.18 | | |

| 0.13 | | |

| (0.05 | ) | |

| 0.66 | | |

| 0.21 | |

| Book value per share common | |

| 10.29 | | |

| 10.20 | | |

| 9.44 | | |

| 10.29 | | |

| 9.44 | |

| Tangible book value per share | |

| 9.31 | | |

| 9.18 | | |

| 8.51 | | |

| 9.31 | | |

| 8.51 | |

| Cash dividends declared | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | |

| (1) | Calculated on a fully taxable equivalent basis using

amortized cost. |

| (2) | These ratios are stated on an annualized basis and are

not necessarily indicative of future periods. |

| (3) | The calculation of ROA and ROE do not include the mark-to-market

unrealized gains (losses) because the unrealized gains (losses) are not included in net income. |

| (4) | The Company defines tangible common equity as total

shareholder's equity less intangible assets. |

| (5) | Defined as (noninterest expense less foreclosed property

expense and amortization of intangibles) divided by net operating revenue (net interest income on a fully taxable equivalent basis

plus noninterest income excluding securities gains and bargain purchase gain, net). |

| FINANCIAL HIGHLIGHTS |

| SEACOAST BANKING CORPORATION OF FLORIDA AND SUBSIDIARIES |

| | |

December 31, | | |

September 30, | | |

December 31, | |

| (Dollars in thousands, except share data) | |

2015 | | |

2015 | | |

2014 | |

| | |

| | |

| | |

| |

| Selected Financial Data | |

| | | |

| | | |

| | |

| Total assets | |

$ | 3,534,780 | | |

$ | 3,378,108 | | |

$ | 3,093,335 | |

| Securities available for sale (at fair value) | |

| 790,766 | | |

| 728,161 | | |

| 741,375 | |

| Securities held for investment (at amortized cost) | |

| 203,525 | | |

| 209,047 | | |

| 207,904 | |

| Net loans | |

| 2,137,202 | | |

| 2,080,119 | | |

| 1,804,814 | |

| Deposits | |

| 2,844,387 | | |

| 2,742,296 | | |

| 2,416,534 | |

| Total shareholders' equity | |

| 353,453 | | |

| 350,280 | | |

| 312,651 | |

| | |

| | | |

| | | |

| | |

| Average Balances (Year-to-Date) | |

| | | |

| | | |

| | |

| Total average assets | |

$ | 3,304,397 | | |

$ | 3,250,855 | | |

$ | 2,485,259 | |

| Less: intangible assets | |

| 33,277 | | |

| 32,879 | | |

| 8,840 | |

| Total average tangible assets | |

$ | 3,271,120 | | |

$ | 3,217,976 | | |

$ | 2,476,419 | |

| | |

| | | |

| | | |

| | |

| Total average equity | |

$ | 337,367 | | |

$ | 331,966 | | |

$ | 256,867 | |

| Less: intangible assets | |

| 33,277 | | |

| 32,879 | | |

| 8,840 | |

| Total average tangible equity | |

$ | 304,090 | | |

$ | 299,087 | | |

$ | 248,027 | |

| | |

| | | |

| | | |

| | |

| Credit Analysis | |

| | | |

| | | |

| | |

| Net charge-offs (recoveries) year-to-date - non-acquired loans | |

$ | (609 | ) | |

$ | (854 | ) | |

$ | (489 | ) |

| Net charge-offs year-to-date - acquired loans | |

| 1,196 | | |

| 872 | | |

| - | |

| Total net charge-offs (recoveries) year-to-date | |

$ | 587 | | |

$ | 18 | | |

$ | (489 | ) |

| | |

| | | |

| | | |

| | |

| Net charge-offs (recoveries) to average loans (annualized) - non-acquired loans | |

| (0.03 | )% | |

| (0.06 | )% | |

| (0.03 | )% |

| Net charge-offs to average loans (annualized) - acquired loans | |

| 0.06 | | |

| 0.06 | | |

| - | |

| Total net charge-offs (recoveries) to average loans (annualized) | |

| 0.03 | | |

| 0.00 | | |

| (0.03 | ) |

| | |

| | | |

| | | |

| | |

| Loan loss provision (recapture) year-to-date - non-acquired loans | |

$ | 1,375 | | |

$ | 1,415 | | |

$ | (3,550 | ) |

| Loan loss provision year-to-date - acquired loans | |

| 1,269 | | |

| 860 | | |

| 64 | |

| Total loan loss provision (recapture) year-to-date | |

$ | 2,644 | | |

$ | 2,275 | | |

$ | (3,486 | ) |

| | |

| | | |

| | | |

| | |

| Allowance to loans at end of period - non-acquired loans | |

| 1.03 | % | |

| 1.11 | % | |

| 1.14 | % |

| Discount for credit losses to acquired loans at end of period | |

| 4.24 | | |

| 4.13 | | |

| 3.56 | |

| | |

| | | |

| | | |

| | |

| Nonperforming loans - non-acquired loans | |

$ | 12,758 | | |

$ | 14,474 | | |

$ | 18,563 | |

| Nonperforming loans - acquired loans | |

| 4,628 | | |

| 2,636 | | |

| 2,577 | |

| Other real estate owned - non-acquired | |

| 3,699 | | |

| 4,183 | | |

| 5,567 | |

| Other real estate owned - acquired | |

| 3,340 | | |

| 3,250 | | |

| 1,895 | |

| Total nonperforming assets | |

$ | 24,425 | | |

$ | 24,543 | | |

$ | 28,602 | |

| | |

| | | |

| | | |

| | |

| Restructured loans (accruing) | |

$ | 19,970 | | |

$ | 20,543 | | |

$ | 24,997 | |

| | |

| | | |

| | | |

| | |

| Purchased noncredit impaired loans | |

$ | 308,737 | | |

$ | 347,262 | | |

$ | 332,508 | |

| Purchased credit impaired loans | |

| 12,109 | | |

| 12,673 | | |

| 7,814 | |

| Total acquired loans | |

$ | 320,846 | | |

$ | 359,935 | | |

$ | 340,322 | |

| | |

| | | |

| | | |

| | |

| Nonperforming loans to loans at end of period - non-acquired loans | |

| 0.59 | % | |

| 0.69 | % | |

| 1.02 | % |

| Nonperforming loans to loans at end of period - acquired loans | |

| 0.22 | | |

| 0.12 | | |

| 0.14 | |

| Total nonperforming loans to loans at end of period | |

| 0.81 | | |

| 0.81 | | |

| 1.16 | |

| | |

| | | |

| | | |

| | |

| Nonperforming assets to total assets - non-acquired | |

| 0.47 | % | |

| 0.55 | % | |

| 0.78 | % |

| Nonperforming assets to total assets - acquired | |

| 0.22 | | |

| 0.18 | | |

| 0.14 | |

| Total nonperforming assets to total assets | |

| 0.69 | | |

| 0.73 | | |

| 0.92 | |

| CONDENSED CONSOLIDATED STATEMENTS OF INCOME |

(Unaudited) |

| SEACOAST BANKING CORPORATION OF FLORIDA AND SUBSIDIARIES |

| | |

Three Months Ended | | |

Twelve Months Ended | |

| | |

December 31, | | |

December 31, | |

| (Dollars in thousands, except per share data) | |

2015 | | |

2014 | | |

2015 | | |

2014 | |

| | |

| | |

| | |

| | |

| |

| Interest on securities: | |

| | | |

| | | |

| | | |

| | |

| Taxable | |

$ | 5,312 | | |

$ | 4,728 | | |

$ | 20,341 | | |

$ | 15,448 | |

| Nontaxable | |

| 144 | | |

| 182 | | |

| 585 | | |

| 211 | |

| Interest and fees on loans | |

| 25,184 | | |

| 21,070 | | |

| 94,469 | | |

| 63,586 | |

| Interest on federal funds sold and other investments | |

| 275 | | |

| 292 | | |

| 1,022 | | |

| 1,017 | |

| Total Interest Income | |

| 30,915 | | |

| 26,272 | | |

| 116,417 | | |

| 80,262 | |

| | |

| | | |

| | | |

| | | |

| | |

| Interest on deposits | |

| 598 | | |

| 297 | | |

| 2,085 | | |

| 864 | |

| Interest on time certificates | |

| 265 | | |

| 375 | | |

| 1,228 | | |

| 1,538 | |

| Interest on borrowed money | |

| 952 | | |

| 867 | | |

| 3,617 | | |

| 2,953 | |

| Total Interest Expense | |

| 1,815 | | |

| 1,539 | | |

| 6,930 | | |

| 5,355 | |

| | |

| | | |

| | | |

| | | |

| | |

| Net Interest Income | |

| 29,100 | | |

| 24,733 | | |

| 109,487 | | |

| 74,907 | |

| Provision (recapture) for loan losses | |

| 369 | | |

| 118 | | |

| 2,644 | | |

| (3,486 | ) |

| Net Interest Income After Provision for Loan Losses | |

| 28,731 | | |

| 24,615 | | |

| 106,843 | | |

| 78,393 | |

| | |

| | | |

| | | |

| | | |

| | |

| Noninterest income: | |

| | | |

| | | |

| | | |

| | |

| Service charges on deposit accounts | |

| 2,229 | | |

| 2,208 | | |

| 8,563 | | |

| 6,952 | |

| Trust fees | |

| 791 | | |

| 795 | | |

| 3,132 | | |

| 2,986 | |

| Mortgage banking fees | |

| 955 | | |

| 716 | | |

| 4,252 | | |

| 3,057 | |

| Brokerage commissions and fees | |

| 511 | | |

| 417 | | |

| 2,132 | | |

| 1,614 | |

| Marine finance fees | |

| 205 | | |

| 445 | | |

| 1,152 | | |

| 1,320 | |

| Interchange income | |

| 1,989 | | |

| 1,603 | | |

| 7,684 | | |

| 5,972 | |

| Other deposit based EFT fees | |

| 99 | | |

| 92 | | |

| 397 | | |

| 343 | |

| BOLI income | |

| 396 | | |

| 252 | | |

| 1,426 | | |

| 252 | |

| Gain on participated loan | |

| 0 | | |

| 0 | | |

| 725 | | |

| 0 | |

| Other | |

| 607 | | |

| 613 | | |

| 2,555 | | |

| 2,248 | |

| | |

| 7,782 | | |

| 7,141 | | |

| 32,018 | | |

| 24,744 | |

| Securities gains, net | |

| 1 | | |

| 108 | | |

| 161 | | |

| 469 | |

| Bargain purchase gain, net | |

| 416 | | |

| 0 | | |

| 416 | | |

| 0 | |

| Total Noninterest Income | |

| 8,199 | | |

| 7,249 | | |

| 32,595 | | |

| 25,213 | |

| | |

| | | |

| | | |

| | | |

| | |

| Noninterest expenses: | |

| | | |

| | | |

| | | |

| | |

| Salaries and wages | |

| 11,135 | | |

| 11,676 | | |

| 41,075 | | |

| 35,132 | |

| Employee benefits | |

| 2,178 | | |

| 2,461 | | |

| 9,564 | | |

| 8,773 | |

| Outsourced data processing costs | |

| 2,455 | | |

| 3,506 | | |

| 10,150 | | |

| 8,781 | |

| Telephone / data lines | |

| 412 | | |

| 419 | | |

| 1,797 | | |

| 1,331 | |

| Occupancy | |

| 2,314 | | |

| 2,325 | | |

| 8,744 | | |

| 7,930 | |

| Furniture and equipment | |

| 1,000 | | |

| 732 | | |

| 3,434 | | |

| 2,535 | |

| Marketing | |

| 1,128 | | |

| 1,163 | | |

| 4,428 | | |

| 3,576 | |

| Legal and professional fees | |

| 2,580 | | |

| 2,555 | | |

| 8,022 | | |

| 6,871 | |

| FDIC assessments | |

| 551 | | |

| 476 | | |

| 2,212 | | |

| 1,660 | |

| Amortization of intangibles | |

| 397 | | |

| 446 | | |

| 1,424 | | |

| 1,033 | |

| Asset dispositions expense | |

| 79 | | |

| 103 | | |

| 472 | | |

| 488 | |

| Branch closures and branding | |

| 0 | | |

| 4,958 | | |

| 0 | | |

| 4,958 | |

| Net (gain)/loss on other real estate owned and repossessed assets | |

| (157 | ) | |

| 9 | | |

| 239 | | |

| 310 | |

| Other | |

| 3,097 | | |

| 3,182 | | |

| 12,209 | | |

| 9,988 | |

| Total Noninterest Expenses | |

| 27,169 | | |

| 34,011 | | |

| 103,770 | | |

| 93,366 | |

| | |

| | | |

| | | |

| | | |

| | |

| Income (Loss) Before Income Taxes | |

| 9,761 | | |

| (2,147 | ) | |

| 35,668 | | |

| 10,240 | |

| Income taxes | |

| 3,725 | | |

| (630 | ) | |

| 13,527 | | |

| 4,544 | |

| | |

| | | |

| | | |

| | | |

| | |

| Net Income (Loss) | |

$ | 6,036 | | |

$ | (1,517 | ) | |

$ | 22,141 | | |

$ | 5,696 | |

| | |

| | | |

| | | |

| | | |

| | |

| Per share of common stock: | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | |

| Net income (loss) diluted | |

$ | 0.18 | | |

$ | (0.05 | ) | |

$ | 0.66 | | |

$ | 0.21 | |

| Net income (loss) basic | |

| 0.18 | | |

| (0.05 | ) | |

| 0.66 | | |

| 0.21 | |

| Cash dividends declared | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | |

| | |

| | | |

| | | |

| | | |

| | |

| Average diluted shares outstanding | |

| 34,395,373 | | |

| 33,123,525 | | |

| 33,744,171 | | |

| 27,716,895 | |

| Average basic shares outstanding | |

| 34,115,697 | | |

| 32,888,612 | | |

| 33,495,827 | | |

| 27,538,955 | |

| CONDENSED CONSOLIDATED STATEMENTS OF INCOME |

(Unaudited) |

| SEACOAST BANKING CORPORATION OF FLORIDA AND SUBSIDIARIES |

| | |

QUARTER | |

| | |

2015 | | |

2014 | |

| (Dollars in thousands) | |

Fourth | | |

Third | | |

Second | | |

First | | |

Fourth | |

| | |

| | |

| | |

| | |

| | |

| |

| Interest on securities: | |

| | | |

| | | |

| | | |

| | | |

| | |

| Taxable | |

$ | 5,312 | | |

$ | 5,154 | | |

$ | 4,977 | | |

$ | 4,898 | | |

$ | 4,728 | |

| Nontaxable | |

| 144 | | |

| 144 | | |

| 147 | | |

| 150 | | |

| 182 | |

| Interest and fees on loans | |

| 25,184 | | |

| 25,276 | | |

| 21,988 | | |

| 22,021 | | |

| 21,070 | |

| Interest on federal funds sold and other investments | |

| 275 | | |

| 249 | | |

| 249 | | |

| 249 | | |

| 292 | |

| Total Interest Income | |

| 30,915 | | |

| 30,823 | | |

| 27,361 | | |

| 27,318 | | |

| 26,272 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest on deposits | |

| 598 | | |

| 562 | | |

| 524 | | |

| 401 | | |

| 297 | |

| Interest on time certificates | |

| 265 | | |

| 295 | | |

| 321 | | |

| 347 | | |

| 375 | |

| Interest on borrowed money | |

| 952 | | |

| 955 | | |

| 850 | | |

| 860 | | |

| 867 | |

| Total Interest Expense | |

| 1,815 | | |

| 1,812 | | |

| 1,695 | | |

| 1,608 | | |

| 1,539 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net Interest Income | |

| 29,100 | | |

| 29,011 | | |

| 25,666 | | |

| 25,710 | | |

| 24,733 | |

| Provision (recapture) for loan losses | |

| 369 | | |

| 987 | | |

| 855 | | |

| 433 | | |

| 118 | |

| Net Interest Income After Provision for Loan Losses | |

| 28,731 | | |

| 28,024 | | |

| 24,811 | | |

| 25,277 | | |

| 24,615 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest income: | |

| | | |

| | | |

| | | |

| | | |

| | |

| Service charges on deposit accounts | |

| 2,229 | | |

| 2,217 | | |

| 2,115 | | |

| 2,002 | | |

| 2,208 | |

| Trust fees | |

| 791 | | |

| 781 | | |

| 759 | | |

| 801 | | |

| 795 | |

| Mortgage banking fees | |

| 955 | | |

| 1,177 | | |

| 1,032 | | |

| 1,088 | | |

| 716 | |

| Brokerage commissions and fees | |

| 511 | | |

| 604 | | |

| 576 | | |

| 441 | | |

| 417 | |

| Marine finance fees | |

| 205 | | |

| 258 | | |

| 492 | | |

| 197 | | |

| 445 | |

| Interchange income | |

| 1,989 | | |

| 1,925 | | |

| 2,033 | | |

| 1,737 | | |

| 1,603 | |

| Other deposit based EFT fees | |

| 99 | | |

| 88 | | |

| 96 | | |

| 114 | | |

| 92 | |

| BOLI income | |

| 396 | | |

| 366 | | |

| 334 | | |

| 330 | | |

| 252 | |

| Gain on participated loan | |

| 0 | | |

| 0 | | |

| 725 | | |

| 0 | | |

| 0 | |

| Other | |

| 607 | | |

| 666 | | |

| 684 | | |

| 598 | | |

| 613 | |

| | |

| 7,782 | | |

| 8,082 | | |

| 8,846 | | |

| 7,308 | | |

| 7,141 | |

| Securities gains, net | |

| 1 | | |

| 160 | | |

| 0 | | |

| 0 | | |

| 108 | |

| Bargain purchase gain, net | |

| 416 | | |

| 0 | | |

| 0 | | |

| 0 | | |

| 0 | |

| Total Noninterest Income | |

| 8,199 | | |

| 8,242 | | |

| 8,846 | | |

| 7,308 | | |

| 7,249 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Noninterest expenses: | |

| | | |

| | | |

| | | |

| | | |

| | |

| Salaries and wages | |

| 11,135 | | |

| 11,850 | | |

| 9,301 | | |

| 8,789 | | |

| 11,676 | |

| Employee benefits | |

| 2,178 | | |

| 2,430 | | |

| 2,541 | | |

| 2,415 | | |

| 2,461 | |

| Outsourced data processing costs | |

| 2,455 | | |

| 3,277 | | |

| 2,234 | | |

| 2,184 | | |

| 3,506 | |

| Telephone / data lines | |

| 412 | | |

| 446 | | |

| 443 | | |

| 496 | | |

| 419 | |

| Occupancy | |

| 2,314 | | |

| 2,396 | | |

| 2,011 | | |

| 2,023 | | |

| 2,325 | |

| Furniture and equipment | |

| 1,000 | | |

| 883 | | |

| 819 | | |

| 732 | | |

| 732 | |

| Marketing | |

| 1,128 | | |

| 1,099 | | |

| 1,226 | | |

| 975 | | |

| 1,163 | |

| Legal and professional fees | |

| 2,580 | | |

| 2,189 | | |

| 1,590 | | |

| 1,663 | | |

| 2,555 | |

| FDIC assessments | |

| 551 | | |

| 552 | | |

| 520 | | |

| 589 | | |

| 476 | |

| Amortization of intangibles | |

| 397 | | |

| 397 | | |

| 315 | | |

| 315 | | |

| 446 | |

| Asset dispositions expense | |

| 79 | | |

| 77 | | |

| 173 | | |

| 143 | | |

| 103 | |

| Branch closures and branding | |

| 0 | | |

| 0 | | |

| 0 | | |

| 0 | | |

| 4,958 | |

| Net (gain)/loss on other real estate owned and repossessed assets | |

| (157 | ) | |

| 262 | | |

| 53 | | |

| 81 | | |

| 9 | |

| Other | |

| 3,097 | | |

| 3,269 | | |

| 3,062 | | |

| 2,781 | | |

| 3,182 | |

| Total Noninterest Expenses | |

| 27,169 | | |

| 29,127 | | |

| 24,288 | | |

| 23,186 | | |

| 34,011 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Income (Loss) Before Income Taxes | |

| 9,761 | | |

| 7,139 | | |

| 9,369 | | |

| 9,399 | | |

| (2,147 | ) |

| Income taxes | |

| 3,725 | | |

| 2,698 | | |

| 3,564 | | |

| 3,540 | | |

| (630 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net Income (Loss) | |

$ | 6,036 | | |

$ | 4,441 | | |

$ | 5,805 | | |

$ | 5,859 | | |

$ | (1,517 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Per share of common stock: | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income (loss) diluted | |

$ | 0.18 | | |

$ | 0.13 | | |

$ | 0.18 | | |

$ | 0.18 | | |

$ | (0.05 | ) |

| Net income (loss) basic | |

| 0.18 | | |

| 0.13 | | |

| 0.18 | | |

| 0.18 | | |

| (0.05 | ) |

| Cash dividends declared | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | | |

| 0.00 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Average diluted shares outstanding | |

| 34,395,373 | | |

| 34,193,540 | | |

| 33,233,508 | | |

| 33,135,618 | | |

| 33,123,525 | |

| Average basic shares outstanding | |

| 34,115,697 | | |

| 33,907,178 | | |

| 32,978,006 | | |

| 32,971,444 | | |

| 32,888,612 | |

| CONDENSED CONSOLIDATED BALANCE SHEETS |

(Unaudited) |

| SEACOAST BANKING CORPORATION OF FLORIDA AND SUBSIDIARIES |

| | |

December 31, | | |

December 31, | |

| (Dollars in thousands, except share data) | |

2015 | | |

2014 | |

| | |

| | |

| |

| Assets | |

| | | |

| | |

| Cash and due from banks | |

$ | 81,216 | | |

$ | 64,411 | |

| Interest bearing deposits with other banks | |

| 54,851 | | |

| 36,128 | |

| Total Cash and Cash Equivalents | |

| 136,067 | | |

| 100,539 | |

| | |

| | | |

| | |

| Securities: | |

| | | |

| | |

| Available for sale (at fair value) | |

| 790,766 | | |

| 741,375 | |

| Held for investment (at amortized cost) | |

| 203,525 | | |

| 207,904 | |

| Total Securities | |

| 994,291 | | |

| 949,279 | |

| | |

| | | |

| | |

| Loans available for sale | |

| 23,998 | | |

| 12,078 | |

| | |

| | | |

| | |

| Loans, net of deferred costs | |

| 2,156,330 | | |

| 1,821,885 | |

| Less: Allowance for loan losses | |

| (19,128 | ) | |

| (17,071 | ) |

| Net Loans | |

| 2,137,202 | | |

| 1,804,814 | |

| | |

| | | |

| | |

| Bank premises and equipment, net | |

| 54,579 | | |

| 45,086 | |

| Other real estate owned | |

| 7,039 | | |

| 7,462 | |

| Other intangible assets | |

| 8,594 | | |

| 7,454 | |

| Goodwill | |

| 25,211 | | |

| 25,309 | |

| Bank owned life insurance | |

| 43,579 | | |

| 35,679 | |

| Other assets | |

| 104,220 | | |

| 105,635 | |

| | |

$ | 3,534,780 | | |

$ | 3,093,335 | |

| | |

| | | |

| | |

| Liabilities and Shareholders' Equity | |

| | | |

| | |

| Liabilities | |

| | | |

| | |

| Deposits | |

| | | |

| | |

| Noninterest demand | |

$ | 854,447 | | |

$ | 725,238 | |

| Interest-bearing demand | |

| 734,749 | | |

| 652,353 | |

| Savings | |

| 295,851 | | |

| 264,738 | |

| Money market | |

| 665,353 | | |

| 450,172 | |

| Other time certificates | |

| 153,318 | | |

| 173,247 | |

| Brokered time certificates | |

| 9,403 | | |

| 7,034 | |

| Time certificates of $100,000 or more | |

| 131,266 | | |

| 143,752 | |

| Total Deposits | |

| 2,844,387 | | |

| 2,416,534 | |

| | |

| | | |

| | |

| Federal funds purchased and securities sold under agreements to repurchase, maturing within 30 days | |

| 172,005 | | |

| 233,640 | |

| Borrowed funds | |

| 50,000 | | |

| 50,000 | |

| Subordinated debt | |

| 69,961 | | |

| 64,583 | |

| Other liabilities | |

| 44,974 | | |

| 15,927 | |

| | |

| 3,181,327 | | |

| 2,780,684 | |

| | |

| | | |

| | |

| Shareholders' Equity | |

| | | |

| | |

| Common stock | |

| 3,435 | | |

| 3,300 | |

| Additional paid in capital | |

| 399,162 | | |

| 379,249 | |

| Accumulated deficit | |

| (42,858 | ) | |

| (65,000 | ) |

| Treasury stock | |

| (73 | ) | |

| (71 | ) |

| | |

| 359,666 | | |

| 317,478 | |

| Accumulated other comprehensive (loss), net | |

| (6,213 | ) | |

| (4,827 | ) |

| Total Shareholders' Equity | |

| 353,453 | | |

| 312,651 | |

| | |

$ | 3,534,780 | | |

$ | 3,093,335 | |

| | |

| | | |

| | |

| Common Shares Outstanding | |

| 34,351,409 | | |

| 33,136,592 | |

Note: The balance sheet at December 31, 2014 has been derived

from the audited financial statements at that date.

| CONSOLIDATED QUARTERLY FINANCIAL DATA |

(Unaudited) |

| SEACOAST BANKING CORPORATION OF FLORIDA AND SUBSIDIARIES |

| | |

QUARTERS | |

| | |

2015 | | |

2014 | |

| (Dollars in thousands, except per share data) | |

Fourth | | |

Third | | |

Second | | |

First | | |

Fourth | |

| Net income (loss) | |

$ | 6,036 | | |

$ | 4,441 | | |

$ | 5,805 | | |

$ | 5,859 | | |

$ | (1,517 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Operating Ratios | |

| | | |

| | | |

| | | |

| | | |

| | |

| Return on average assets-GAAP basis (2),(3) | |

| 0.69 | % | |

| 0.52 | % | |

| 0.72 | % | |

| 0.75 | % | |

| (0.20 | )% |

| Return on average tangible assets (2),(3),(4) | |

| 0.73 | | |

| 0.56 | | |

| 0.75 | | |

| 0.79 | | |

| (0.16 | ) |

| Return on average shareholders' equity-GAAP basis (2),(3) | |

| 6.78 | | |

| 5.05 | | |

| 7.13 | | |

| 7.42 | | |

| (1.89 | ) |

| Efficiency ratio (5) | |

| 72.57 | | |

| 76.29 | | |

| 68.57 | | |

| 68.33 | | |

| 104.46 | |

| Noninterest income to total revenue | |

| 21.10 | | |

| 21.79 | | |

| 25.63 | | |

| 22.13 | | |

| 22.40 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest margin (1),(2) | |

| 3.67 | | |

| 3.75 | | |

| 3.50 | | |

| 3.62 | | |

| 3.56 | |

| Average equity to average assets | |

| 10.20 | | |

| 10.34 | | |

| 10.12 | | |

| 10.17 | | |

| 10.51 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Credit Analysis Excluding Acquired Loans | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net charge-offs (recoveries) - non-acquired loans | |

$ | 245 | | |

$ | (233 | ) | |

$ | (358 | ) | |

$ | (263 | ) | |

$ | 618 | |

| Net charge-offs - acquired loans | |

| 324 | | |

| 683 | | |

| 143 | | |

| 46 | | |

| - | |