UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

Date: March 10, 2016

Commission File Number: 001-33414

Denison Mines Corp.

(Translation of registrant’s name into English)

1100-40 University Avenue,

Toronto Ontario, M5J 1T1 Canada

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form

20-F ¨ Form 40-F x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T

Rule 101(b)(7): ¨

Signatures

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned,

thereunto duly authorized.

|

|

|

|

|

|

|

|

|

Denison Mines Corp. |

|

|

|

|

|

|

|

/s/ Amanda Willett |

| Date: March 10, 2016 |

|

|

|

Amanda Willett |

|

|

|

|

Corporate Counsel and Corporate Secretary |

EXHIBIT INDEX

|

|

|

| Exhibit Number |

|

Description |

|

|

| 99.1 |

|

Press Release dated March 9, 2016 |

| 99.2 |

|

Audited Financial Statements for the financial year ended December 31, 2015 |

| 99.3 |

|

Management’s Discussion and Analysis for the financial year ended December 31, 2015 |

Exhibit 99.1

|

|

|

|

|

Denison Mines Corp. 1100

– 40 University Ave Toronto, ON M5J 1T1

www.denisonmines.com |

PRESS RELEASE

DENISON MINES CORP. REPORTS HIGHLIGHTS OF 2015 RESULTS

Toronto, ON – March 9, 2016. Denison Mines Corp. (“Denison” or the “Company”) (DML: TSX, DNN: NYSE MKT) today filed

its Consolidated Financial Statements and Management’s Discussion & Analysis (“MD&A”) for the financial year ended December 31, 2015. Both documents can be found on the Company’s website at www.denisonmines.com or on SEDAR (at www.sedar.com) and

EDGAR (at www.sec.gov/edgar.shtml). The highlights provided below are derived from these documents and should be read in conjunction with them.

All amounts in this release are in U.S. dollars unless otherwise stated.

David Cates, President and CEO of Denison commented “In 2015,

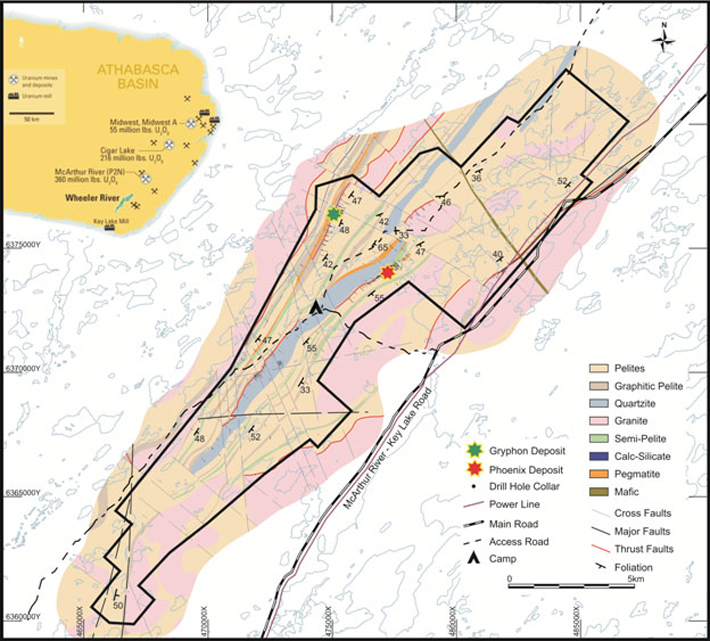

Denison achieved a key milestone with the completion of a maiden resource estimate for our Gryphon deposit on the Wheeler River property – which was already host to the exceptionally high-grade Phoenix deposit. The addition of the Gryphon

deposit represents a significant increase in the estimated mineral resources at Denison’s 60% owned Wheeler River property, and establishes the project as one of the largest and highest grade undeveloped uranium projects in the Athabasca Basin

region.”

2015 HIGHLIGHTS

| ¡ |

|

Reported a significant increase in estimated mineral resources at the Wheeler River property |

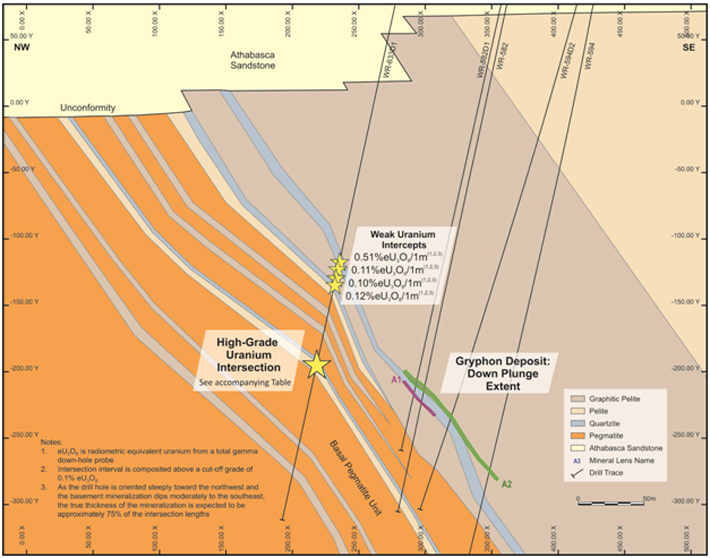

The Company completed an initial mineral resource estimate for the basement hosted Gryphon uranium deposit, which is located three

kilometres to the northwest of the high-grade unconformity hosted Phoenix deposit. The Gryphon deposit is estimated to contain an inferred mineral resource of 43.0 million pounds U3O8 at an average grade of 2.3% U3O8. Together with the high-grade Phoenix deposit,

Wheeler River is now estimated to contain indicated mineral resources of 70.2 million pounds U3O8 at an average grade of 19.1% U3O8 and inferred mineral resources totaling 44.1 million pounds U3O8 at a combined grade of 2.34% U3O8 (see Denison news release dated November 3, 2015).

| ¡ |

|

Moving ahead at the Wheeler River Property |

A Preliminary Economic Analysis (“PEA”) was initiated in 2015 to evaluate the economic merit of the co-development of the

Gryphon and Phoenix deposits and is expected to be completed in the first half of 2016. Subject to a positive outcome from the PEA, the Company plans to initiate work on a Prefeasibility Study and environmental assessment work as part of a 2016

evaluation budget of CAD$2,600,000 (CAD$1,600,000 Denison’s share).

| ¡ |

|

Experienced continued exploration success at the Wheeler River property |

Exploration drilling results for the area in the vicinity of the Gryphon deposit continued to highlight the mineralization potential of

this area. During 2015, a total of 16 drill holes were completed up plunge and along the sub-Athabasca unconformity to the southwest of the Gryphon deposit along the K-North trend. The drilling successfully identified approximately 2.3 kilometres of

mineralized strike. The mineralization occurs both at the unconformity and immediately below within the basement, indicating further potential along the unconformity to the southwest and within the basement below. The best result to date occurs

at the unconformity, 800 metres to the south of Gryphon, with drill hole WR-597 intersecting 4.5% U3O8 over 4.5 metres (see Denison news

release dated June 4, 2015). In February 2016 Denison reported a new intersection of high-grade uranium within the basement roughly 100 metres to the north of the Gryphon deposit, (see Denison news release dated February 9, 2016).

| ¡ |

|

Generated positive 2015 exploration results at other exploration pipeline properties in the infrastructure rich eastern Athabasca Basin

|

At the 68.85% owned Murphy Lake property, Denison intersected a new zone of uranium mineralization, highlighted

by drill hole MP-15-03, which returned a mineralized interval of 0.25% U3O8 over 6.0 metres at the sub-Athabasca unconformity (see

Denison news release dated July 29, 2015). At the 61.55% owned Waterbury Lake property, the Company intersected weak uranium mineralization and strong alteration and/or structure at the Oban target area. At the 100% owned Crawford

Lake property, the Company extended a large zone of significant sandstone alteration along the CR-2 and CR-5 conductors, which is now confirmed over a strike length of 2.9 kilometres.

| ¡ |

|

Exceeded initial 2015 guidance for toll milling revenue at McClean Lake |

The McClean Lake mill, in which Denison owns a 22.5% interest, packaged approximately 11.3 million pounds U3O8 during the year (initially targeted at six to eight million packaged pounds) for the Cigar Lake Joint Venture (“CLJV”),

generating toll milling revenues for Denison of $3.2 million.

| ¡ |

|

Completed the sale of the Company’s Mongolian interests for consideration of up to $13.25 million |

Denison received $1.25 million in initial payments on the closing of the sale of its Mongolian interests. Denison has the rights to

receive additional proceeds of up to $12 million, conditional on achieving certain milestones associated with the Mongolian projects.

ABOUT DENISON

Denison is a uranium exploration and development company with interests focused in the Athabasca Basin region of northern Saskatchewan, Canada.

In addition to its 60% owned Wheeler River project, which hosts the high grade Phoenix and Gryphon uranium deposits, Denison’s exploration portfolio consists of numerous projects covering over 390,000 hectares in the eastern Athabasca Basin.

Denison’s interests in Saskatchewan also include a 22.5% ownership interest in the McClean Lake joint venture (“MLJV”), which includes several uranium deposits and the McClean Lake uranium mill, plus a 25.17% interest in the Midwest

deposit and a 61.55% interest in the J Zone deposit on the Waterbury Lake property. Both the Midwest and J Zone deposits are located within 20 kilometres of the McClean Lake mill. Internationally, Denison owns 100% of the Mutanga uranium

project in Zambia, 100% of the uranium-silver-copper Falea project in Mali and a 90% interest in the Dome uranium project in Namibia.

Denison is

engaged in mine decommissioning and environmental services through its Denison Environmental Services (“DES”).

Denison is also the manager

of Uranium Participation Corporation (“UPC”), a publicly traded company listed on the TSX under the symbol “U”, which invests in uranium oxide in concentrates (“U3O8”) and uranium hexafluoride

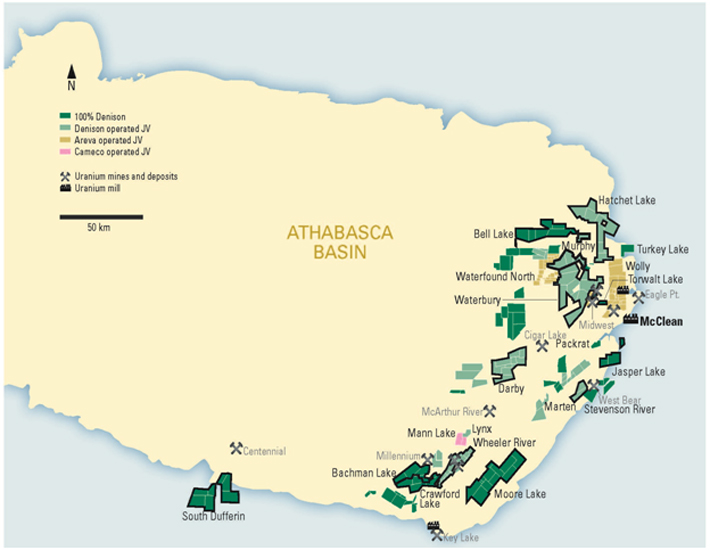

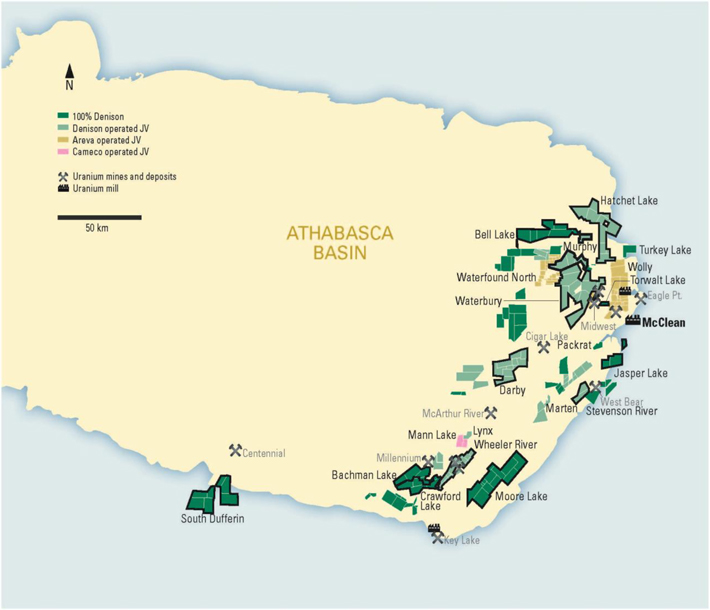

EASTERN ATHABASCA LAND POSITION

The Company’s land position in the infrastructure rich eastern Athabasca Basin, as of December 31, 2015, is illustrated below. Denison’s

active exploration properties are outlined in bold.

2

|

|

|

|

|

|

|

|

|

|

|

|

|

| SELECTED ANNUAL FINANCIAL INFORMATION |

|

|

|

|

|

|

|

|

|

|

| (in thousands, except for per share amounts) |

|

|

|

Year Ended

December 31, 2015 |

|

|

|

|

Year Ended

December 31,

2014 |

|

|

|

|

|

|

| Results of Continuing Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

| Total revenues |

|

$ |

|

|

12,670 |

|

|

$ |

|

|

9,619 |

|

| Mineral property exploration |

|

$ |

|

|

(14,257) |

|

|

$ |

|

|

(14,401) |

|

| Impairment of mineral properties |

|

$ |

|

|

(27,767) |

|

|

$ |

|

|

(1,745) |

|

| Net loss |

|

$ |

|

|

(61,737) |

|

|

$ |

|

|

(28,266) |

|

| Basic and diluted loss per share |

|

$ |

|

|

(0.12) |

|

|

$ |

|

|

(0.06) |

|

|

|

|

|

|

| Results from Mongolian Discontinued Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

| Net income (loss) |

|

$ |

|

|

10,177 |

|

|

$ |

|

|

(3,437) |

|

| Basic and diluted income per share |

|

$ |

|

|

0.02 |

|

|

$ |

|

|

(0.01) |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| (in thousands) |

|

|

|

As at

December 31,

2015 |

|

|

|

|

As at

December 31,

2014 |

|

|

|

|

|

|

| Financial Position: |

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents |

|

$ |

|

|

5,367 |

|

|

$ |

|

|

18,640 |

|

| Short term investments |

|

|

|

|

7,282 |

|

|

|

|

|

4,381 |

|

| Long term investments |

|

|

|

|

496 |

|

|

|

|

|

954 |

|

| Cash, cash equivalents and investments |

|

$ |

|

|

13,145 |

|

|

$ |

|

|

23,975 |

|

|

|

|

|

|

| Working capital |

|

$ |

|

|

12,772 |

|

|

$ |

|

|

22,542 |

|

| Property, plant and equipment |

|

$ |

|

|

188,250 |

|

|

$ |

|

|

270,388 |

|

| Total assets |

|

$ |

|

|

212,758 |

|

|

$ |

|

|

311,330 |

|

| Total long-term liabilities |

|

$ |

|

|

38,125 |

|

|

$ |

|

|

42,291 |

|

RESULTS OF OPERATIONS

Revenues

The McClean Lake mill continued to process ore received from the Cigar Lake mine. The mill packaged approximately 11.3 million pounds U3O8 for the CLJV. The Company’s share of toll milling revenue during 2015 totaled $3,155,000. Revenue from Denison Environmental Services

(“DES”) during 2015 was $7,607,000, improving on 2014 due to increased activity at certain care and maintenance sites.

Revenue from the

Company’s management contract with UPC was $1,822,000 during 2015.

Operating expenses

Canadian mining segment operating expenses include depreciation, development and standby costs, as well as certain adjustments to the estimates of future

reclamation liabilities at McClean Lake, Midwest and Elliot Lake. Operating expenses in 2015 were $4,554,000, including depreciation of the McClean Lake mill of $1,627,000.

DES operating expenses during 2015 totaled $6,875,000, related primarily to the construction and consulting services provided to clients and includes

labour and other costs.

General and administrative expenses

Total general and administrative expenses were $6,463,000 during 2015. These costs are mainly comprised of head office salaries and benefits, office costs

in multiple regions, audit and regulatory costs, legal fees, investor relations expenses, project costs and all other costs related to operating a public company with listings in Canada and the United States. Also included was $1,461,000 related to

the failed transaction with Fission Uranium Corp.

Impairment – Mineral Properties

During 2015, the Company recognized a non-cash impairment of $25,164,000 against the value of its African mining segment, which included significant

carrying values for the Falea, Mutanga and Dome projects, and also recognized non-cash impairment charges of $2,603,000, to fully impair the carrying value of three of its non-core Canadian exploration properties.

3

Foreign exchange income and expense

During 2015, a foreign exchange loss of $16.0 million was recognized due to unfavourable fluctuations in foreign exchange rates impacting the revaluation

of intercompany debt for the Company’s African related operations.

Mongolian Discontinued Operations

Income from discontinued operations was $10,177,000, which mainly comprised of the gain on disposal of $8,374,000 and transactional foreign exchange

income of $2,873,000, partly offset by exploration, operating and administrative expenses of $1,091,000. The gain on the disposal consisted of $1,250,000 in cash consideration, less transaction costs of $337,000, a favourable cumulative translation

adjustment of $13,680,000, offset by the carrying value of the net assets of $6,219,000. Denison is entitled to up to $12,000,000 in additional proceeds that are contingent on the approval of certain mining licenses and other milestones.

LIQUIDITY AND CAPITAL RESOURCES

Cash, cash equivalents, GICs

and other investments were $13,145,000 at December 31, 2015. The Company holds a large majority of its cash, cash equivalents, and investments in Canadian dollars. As at December 31, 2015, the Company’s cash, cash equivalents and

current investments amount to CAD$17.5 million. The Company’s CAD$24 million credit facility available for non-financial letters of credit was extended in January 2016 to January 2017. The facility contains a covenant that

requires the Company to maintain a minimum cash balance of CAD$5 million on deposit with the Bank of Nova Scotia.

OUTLOOK FOR 2016

In 2016, the Company will focus on increasing its mineral resource base in the Athabasca Basin and advancing the Wheeler River project. The 2016 winter

exploration program commenced in January with a focus on the Company’s Wheeler River project and other high priority properties located in the infrastructure rich eastern Athabasca Basin.

|

|

|

|

|

| |

|

| (in thousands) |

|

2016 BUDGET (1) |

|

| |

|

| Canada |

|

|

|

|

| Toll Milling Revenue & Mineral Sales

|

|

$ |

5,450 |

|

| Development & Operations |

|

|

(2,450) |

|

| Mineral Property Exploration & Evaluation |

|

|

(13,000) |

|

| |

|

|

|

|

(10,000) |

|

| Africa |

|

|

|

|

| Zambia, Mali and Namibia |

|

|

(1,290) |

|

| |

|

|

|

|

(1,290) |

|

| Other |

|

|

|

|

| UPC Management Services |

|

|

1,520 |

|

| DES Environmental Services |

|

|

920 |

|

| Corporate Administration & Other |

|

|

(4,200) |

|

| |

|

|

|

|

(1,760) |

|

| |

|

| Total |

|

$ |

(13,050) |

|

| |

|

| (1) Budget figures have been converted using a US$ to CAD$

exchange rate of 1.30. |

|

CANADA

Toll Milling Revenue & Mineral

Sales

Provided regulatory approvals are secured to increase the annual license limit, the McClean Lake mill is expected to produce 16 million

pounds U3O8 during 2016. Denison’s share of revenue from toll milling of the Cigar Lake ore and the sale of approximately 25,000

pounds U3O8, currently held by Denison in inventory, is budgeted to be $5.4 million (CAD$7.1 million).

4

Development & Operations

In 2016, Denison’s share of operating and capital expenditures at McClean Lake and Midwest are budgeted to be $1.6 million (CAD$2.1 million).

Operating expenditures include $797,000 (CAD$1.04 million) in respect of Denison’s share of the planned 2016 budget for the Surface Access Borehole Resource Extraction (“SABRE”) program.

Reclamation expenditures at Elliot Lake are budgeted to be $665,000 (CAD$864,000).

Mineral Property Exploration & Evaluation

Denison expects

to operate and/or participate in a total of 15 exploration programs (including 13 drilling programs totaling approximately 75,000 metres), of which Wheeler River will continue to be the primary focus. The total budget for all of these programs,

inclusive of the evaluation work planned for Wheeler River, is budgeted to be CAD$24.6 million (Denison’s share, CAD$16.9 million).

Wheeler River –

Exploration

A total of 47,000 metres of exploration drilling is planned at Wheeler River between the winter and summer drill programs, along with

geophysical surveys at a total cost of CAD$10.0 million (Denison’s share, CAD$6.0 million).

Exploration drilling planned for 2016 will continue

to test the unconformity to the southwest of Gryphon as well as numerous basement targets near Gryphon.

Wheeler River - Evaluation

The PEA is expected to be completed during the first half of 2016. Subject to a positive outcome from the PEA, the Company plans to initiate work on a

Prefeasibility Study and environmental assessment work with an approximate budget for 2016 of CAD$2.6 million (Denison’s share, CAD$1.6 million).

Other High

Priority Exploration Properties

Drilling at the Company’s high priority exploration properties is planned to continue at Murphy Lake,

Crawford Lake and Waterbury Lake during 2016. Drill programs are also planned for Denison’s non-operated joint venture projects, including Mann Lake, Wolly and McClean Lake.

Environmental services

Revenue from operations at DES during

2016 is budgeted to be $7.2 million (CAD$9.4 million) and operating and overhead expenses are budgeted to be $6.1 million (CAD$7.9 million). Capital expenditures at DES are budgeted to be $230,000 (CAD$300,000).

Corporate administration and other

Budgeted at $3.85 million

(CAD$5.0 million) in 2016, corporate administration costs include all head office salaries and benefits, office costs, audit and regulatory costs, legal fees, investor relations expenses and all other costs related to operating a public company with

listings in Canada and the United States.

Net management fees earned during 2016 from UPC are budgeted at $1.5 million (CAD$1.95 million).

Letter of credit and standby fees relating to the 2016 Credit Facility are budgeted to be $400,000 (CAD$520,000).

TECHNICAL INFORMATION

Further details regarding the Gryphon

deposit and the current mineral resources estimated at Wheeler River are provided in the report titled “Technical Report on a Mineral Resource Estimate For The Wheeler River Property, Eastern Athabasca Basin, Northern Saskatchewan,

Canada.”, dated Nov. 25, 2015, authored by William E. Roscoe Ph.D, P.Eng. and Mark B. Mathisen C.P.G of RPA Inc. A copy of this report is available under Denison’s profile on SEDAR (www.sedar.com).

The disclosure of a scientific or technical nature contained in this news release was prepared by Dale Verran, MSc, Pr.Sci.Nat., Denison’s Vice

President, Exploration, who is a Qualified Person in accordance with the requirements of NI 3-101. For a description of the quality assurance program and quality control measures applied by Denison, please see Denison’s Annual Information

Form dated March 5, 2015 filed under the Company’s profile on SEDAR at www.sedar.com.

For more information, please contact

|

|

|

| David Cates |

|

(416) 979 – 1991 ext 362 |

| President and Chief Executive Officer |

|

|

|

|

| Sophia Shane |

|

(604) 689 - 7842 |

| Investor Relations |

|

|

5

Cautionary Statement Regarding Forward-Looking Statements

Certain information contained in this press release constitutes “forward-looking information”, within the meaning of the United States Private

Securities Litigation Reform Act of 1995 and similar Canadian legislation concerning the business, operations and financial performance and condition of Denison.

Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects”,

“budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, or “believes”, or the negatives and/or variations of such words and phrases, or state that certain

actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur”, “be achieved” or “has the potential to”.

In particular, this press release contains forward-looking information pertaining to the following: the likelihood of completing and benefits to be

derived from corporate transactions, including the potential for receipt of any contingent payments; the estimates of Denison’s mineral reserves and mineral resources; completion of the PEA; expectations regarding the toll milling of Cigar Lake

ores; expectations regarding revenues and expenditure from operations at DES; capital expenditure programs, estimated exploration and development expenditures and reclamation costs and Denison’s share of same; exploration, development and

expansion plans and objectives; and statements regarding anticipated budgets, fees and expenditures. Statements relating to “mineral reserves” or “mineral resources” are deemed to be forward-looking information, as they involve

the implied assessment, based on certain estimates and assumptions that the mineral reserves and mineral resources described can be profitably produced in the future.

Forward looking statements are based on the opinions and estimates of management as of the date such statements are made, and they are subject to known

and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Denison to be materially different from those expressed or implied by such forward-looking

statements. Denison believes that the expectations reflected in this forward-looking information are reasonable but no assurance can be given that these expectations will prove to be accurate and may differ materially from those anticipated in

this forward looking information. For a discussion in respect of risks and other factors that could influence forward-looking events, please refer to the factors discussed in the MD&A under the heading “Risk Factors”. These

factors are not, and should not be construed as being exhaustive.

Accordingly, readers should not place undue reliance on forward-looking

statements. The forward-looking information contained in this press release is expressly qualified by this cautionary statement. Any forward-looking information and the assumptions made with respect thereto speaks only as of the date of

this press release. Denison does not undertake any obligation to publicly update or revise any forward-looking information after the date of this press release to conform such information to actual results or to changes in Denison’s

expectations except as otherwise required by applicable legislation.

Cautionary Note to United States Investors Concerning Estimates of Measured,

Indicated and Inferred Mineral Resources: This press release may use the terms “measured”, “indicated” and “inferred” mineral resources. United States investors are advised that while such terms are recognized and

required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and as to their economic and legal

feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or other economic

studies. United States investors are cautioned not to assume that all or any part of measured or indicated mineral resources will ever be converted into mineral reserves. United States investors are also cautioned not to assume

that all or any part of an inferred mineral resource exists, or is economically or legally mineable.

6

Exhibit 99.2

ANNUAL CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2015

Responsibility for Financial Statements

The Company’s management is responsible for the integrity and fairness of presentation of these consolidated financial statements. The consolidated

financial statements have been prepared by management, in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, for review by the Audit Committee and approval by the Board of

Directors.

The preparation of financial statements requires the selection of appropriate accounting policies in accordance with International

Financial Reporting Standards and the use of estimates and judgements by management to present fairly and consistently the consolidated financial position of the Company. Estimates are necessary when transactions affecting the current period cannot

be finalized with certainty until future information becomes available. In making certain material estimates, the Company’s management has relied on the judgement of independent specialists.

The Company’s management has developed and maintains a system of internal accounting controls to ensure, on a reasonable and cost-effective basis,

that the financial information is timely reported and is accurate and reliable in all material respects and that the Company’s assets are appropriately accounted for and adequately safeguarded.

The consolidated financial statements have been audited by PricewaterhouseCoopers LLP, our independent auditor. Its report outlines the scope of its

examination and expresses its opinions on the consolidated financial statements and internal control over financial reporting.

|

|

|

| Original signed by “David D.Cates” |

|

Original signed by “Gabriel (Mac) McDonald” |

|

|

| David D. Cates |

|

Gabriel (Mac) McDonald |

| President and Chief Executive Officer |

|

Vice-President Finance and Chief Financial Officer |

March 9, 2016

Management’s Report on Internal Control over Financial Reporting

The Company’s management is responsible for establishing and maintaining an adequate system of internal control over financial reporting. Management

conducted an evaluation of the effectiveness of internal control over financial reporting based on the Internal Control – Integrated Framework, 2013 issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on

this evaluation, management concluded that the Company’s internal control over financial reporting was effective as of December 31, 2015.

The effectiveness of the Company’s internal control over financial reporting as at December 31, 2015 has been audited by PricewaterhouseCoopers

LLP, our independent auditor, as stated in its report which appears herein.

Changes to Internal Control over Financial Reporting

There has not been any change in the Company’s internal control over financial reporting that occurred during 2015 that has

materially affected, or is reasonably likely to materially affect, the Company’s internal control over financial reporting.

2

March 9, 2016

Independent Auditor’s Report

To the Shareholders of

Denison Mines Corp.

We

have completed the integrated audits of the consolidated financial statements of Denison Mines Corp. and its subsidiaries for the years ending December 31, 2015 and December 31, 2014 and their internal control over financial reporting as

at December 31, 2015. Our opinions based on our audits are presented below.

Report on the consolidated financial statements

We have audited the accompanying consolidated financial statements of Denison Mines Corp. and its subsidiaries, which comprise the

consolidated statements of financial position as at December 31, 2015 and 2014 and the consolidated statements of income (loss) and comprehensive income (loss), changes in equity and cash flow for the years then ended, and the related notes,

which comprise a summary of significant accounting policies and other explanatory information.

Management’s responsibility for

the consolidated financial statements

Management is responsible for the preparation and fair presentation of these consolidated

financial statements in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB) and for such internal control as management determines is necessary to enable the preparation

of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s

responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We

conducted our audits in accordance with Canadian generally accepted auditing standards and the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the consolidated financial statements are free from material misstatement. Canadian generally accepted auditing standards also require that we comply with ethical requirements.

An audit involves performing procedures to obtain audit evidence, on a test basis, about the amounts and disclosures in the consolidated

financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the company’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances. An audit

also includes evaluating the appropriateness of accounting principles and policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

|

|

|

| |

|

|

|

|

PricewaterhouseCoopers LLP PwC Tower,

18 York Street, Suite 2600, Toronto, Ontario, Canada M5J 0B2 T: +1 416 863 1133, F: +1 416 365 8215, www.pwc.com/ca

“PwC” refers to PricewaterhouseCoopers LLP, an Ontario limited liability

partnership. |

3

We believe that the audit evidence we have obtained in our audits is sufficient and

appropriate to provide a basis for our audit opinion on the consolidated financial statements.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of Denison Mines Corp.

and its subsidiaries as at December 31, 2015 and 2014 and their financial performance and their cash flows for the years then ended in accordance with IFRS as issued by the IASB.

Emphasis of matter

Without qualifying our opinion, we draw attention to Note 2 in the consolidated financial statements which describe matters and conditions that

indicate the existence of material uncertainties that raise substantial doubt about the company’s ability to continue as a going concern.

Report on internal control over financial reporting

We have also audited Denison Mines Corp. and its subsidiaries’ internal control over financial reporting as at December 31, 2015,

based on criteria established in Internal Control - Integrated Framework (2013), issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

Management’s responsibility for internal control over financial reporting

Management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of

internal control over financial reporting included in the accompanying Management’s Report on Internal Control over Financial Reporting.

Auditor’s responsibility

Our responsibility is to express an opinion on the company’s internal control over financial reporting based on our audit. We conducted

our audit of internal control over financial reporting in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about

whether effective internal control over financial reporting was maintained in all material respects.

An audit of internal control over

financial reporting includes obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, testing and evaluating the design and operating effectiveness of internal control, based on the

assessed risk, and performing such other procedures as we consider necessary in the circumstances.

We believe that our audit provides a

reasonable basis for our audit opinion on the company’s internal control over financial reporting.

Definition of internal control

over financial reporting

A company’s internal control over financial reporting is a process designed to provide reasonable

assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

4

A company’s internal control over financial reporting includes those policies and

procedures that: (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as

necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors

of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Inherent limitations

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of

any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions or that the degree of compliance with the policies or procedures may deteriorate.

Opinion

In our opinion,

Denison Mines Corp. and its subsidiaries maintained, in all material respects, effective internal control over financial reporting as at December 31, 2015, based on criteria established in Internal Control - Integrated Framework (2013) issued

by COSO.

(Signed) “PricewaterhouseCoopers LLP”

Chartered Professional Accountants, Licensed Public Accountants

Toronto, Ontario, Canada

5

Consolidated Statements of Financial Position

|

|

|

|

|

|

|

|

|

|

|

| |

|

| (Expressed in thousands of U.S. dollars except for share amounts) |

|

|

|

At December 31

2015 |

|

|

At December 31

2014 |

|

| |

|

|

|

|

|

| ASSETS |

|

|

|

|

|

|

|

|

|

|

| Current |

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents (note 7) |

|

$ |

|

|

5,367 |

|

|

$ |

18,640 |

|

| Investments (note 10) |

|

|

|

|

7,282 |

|

|

|

4,381 |

|

| Trade and other receivables (note 8) |

|

|

|

|

4,826 |

|

|

|

9,411 |

|

| Inventories (note 9) |

|

|

|

|

2,256 |

|

|

|

2,240 |

|

| Prepaid expenses and other |

|

|

|

|

619 |

|

|

|

850 |

|

| |

|

|

|

|

|

|

20,350 |

|

|

|

35,522 |

|

| Non-Current |

|

|

|

|

|

|

|

|

|

|

| Inventories-ore in stockpiles (note 9) |

|

|

|

|

1,515 |

|

|

|

1,760 |

|

| Investments (note 10) |

|

|

|

|

496 |

|

|

|

954 |

|

| Restricted cash and investments (note 11) |

|

|

|

|

2,040 |

|

|

|

2,068 |

|

| Property, plant and equipment (note 12) |

|

|

|

|

188,250 |

|

|

|

270,388 |

|

| Intangibles (note 13) |

|

|

|

|

107 |

|

|

|

638 |

|

| |

|

| Total assets |

|

$ |

|

|

212,758 |

|

|

$ |

311,330 |

|

| |

|

|

|

|

|

| LIABILITIES |

|

|

|

|

|

|

|

|

|

|

| Current |

|

|

|

|

|

|

|

|

|

|

| Accounts payable and accrued liabilities |

|

$ |

|

|

4,574 |

|

|

$ |

10,050 |

|

| Current portion of long-term liabilities: |

|

|

|

|

|

|

|

|

|

|

| Post-employment benefits (note 14) |

|

|

|

|

217 |

|

|

|

259 |

|

| Reclamation obligations (note 15) |

|

|

|

|

624 |

|

|

|

706 |

|

| Debt obligations (note 16) |

|

|

|

|

300 |

|

|

|

30 |

|

| Other liabilities (note 17) |

|

|

|

|

1,863 |

|

|

|

1,935 |

|

| |

|

|

|

|

|

|

7,578 |

|

|

|

12,980 |

|

| Non-Current |

|

|

|

|

|

|

|

|

|

|

| Post-employment benefits (note 14) |

|

|

|

|

2,172 |

|

|

|

2,662 |

|

| Reclamation obligations (note 15) |

|

|

|

|

18,836 |

|

|

|

16,953 |

|

| Debt obligations (note 16) |

|

|

|

|

- |

|

|

|

9 |

|

| Other liabilities (note 17) |

|

|

|

|

652 |

|

|

|

841 |

|

| Deferred income tax liability (note 18) |

|

|

|

|

16,465 |

|

|

|

21,826 |

|

| |

|

| Total liabilities |

|

|

|

|

45,703 |

|

|

|

55,271 |

|

| |

|

|

|

|

|

| EQUITY |

|

|

|

|

|

|

|

|

|

|

| Share capital (note 19) |

|

|

|

|

1,130,779 |

|

|

|

1,120,758 |

|

| Share purchase warrants (note 20) |

|

|

|

|

- |

|

|

|

376 |

|

| Contributed surplus (note 21) |

|

|

|

|

53,965 |

|

|

|

53,321 |

|

| Deficit |

|

|

|

|

(944,097) |

|

|

|

(892,537) |

|

| Accumulated other comprehensive loss (note 22) |

|

|

|

|

(73,592) |

|

|

|

(25,859) |

|

| |

|

| Total equity |

|

|

|

|

167,055 |

|

|

|

256,059 |

|

| |

|

| Total liabilities and equity |

|

$ |

|

|

212,758 |

|

|

$ |

311,330 |

|

| |

|

|

|

|

|

| Issued and outstanding common shares (note 19) |

|

|

|

|

518,438,669 |

|

|

|

505,868,894 |

|

| |

|

| Going concern basis of accounting (note 2) |

|

|

|

|

|

|

|

|

|

|

| Commitments and contingencies (note 27) |

|

|

|

|

|

|

|

|

|

|

| Subsequent events (note 29) |

|

|

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of the consolidated financial statements

On behalf of the Board of Directors:

|

|

|

| (Signed) “William A. Rand” |

|

(Signed) “Catherine J.G. Stefan” |

| Director |

|

Director |

6

Consolidated Statements of Income (Loss) and

Comprehensive Income (Loss)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| |

|

|

|

Year Ended |

|

| (Expressed in thousands of U.S. dollars except for share and per share amounts) |

|

|

|

December 31

2015 |

|

|

|

|

December 31

2014 |

|

| |

|

|

|

|

|

|

| REVENUES (note 24) |

|

$ |

|

|

12,670 |

|

|

$ |

|

|

9,619 |

|

| |

|

|

|

|

|

|

| EXPENSES |

|

|

|

|

|

|

|

|

|

|

|

|

| Operating expenses (note 23, 24) |

|

|

|

|

(12,408) |

|

|

|

|

|

(11,651) |

|

| Mineral property exploration (note 24) |

|

|

|

|

(14,257) |

|

|

|

|

|

(14,401) |

|

| General and administrative (note 24) |

|

|

|

|

(6,463) |

|

|

|

|

|

(6,636) |

|

| Impairment of mineral properties (note 12) |

|

|

|

|

(27,767) |

|

|

|

|

|

(1,745) |

|

| Foreign exchange |

|

|

|

|

(16,042) |

|

|

|

|

|

(5,893) |

|

| Other income (expense) (note 23) |

|

|

|

|

(525) |

|

|

|

|

|

425 |

|

| |

|

|

|

|

|

|

(77,462) |

|

|

|

|

|

(39,901) |

|

| |

|

| Loss before finance charges |

|

|

|

|

(64,792) |

|

|

|

|

|

(30,282) |

|

|

|

|

|

|

| Finance expense (note 23) |

|

|

|

|

(714) |

|

|

|

|

|

(283) |

|

| |

|

| Loss before taxes |

|

|

|

|

(65,506) |

|

|

|

|

|

(30,565) |

|

| Income tax recovery (expense) (note 18): |

|

|

|

|

|

|

|

|

|

|

|

|

| Current |

|

|

|

|

- |

|

|

|

|

|

(5) |

|

| Deferred |

|

|

|

|

3,769 |

|

|

|

|

|

2,304 |

|

| |

|

| Loss from continuing operations |

|

|

|

|

(61,737) |

|

|

|

|

|

(28,266) |

|

| Net income (loss) from discontinued operations, net of tax (note 6) |

|

|

|

|

10,177 |

|

|

|

|

|

(3,437) |

|

| |

|

| Net loss for the period |

|

$ |

|

|

(51,560) |

|

|

$ |

|

|

(31,703) |

|

| |

|

|

|

|

|

|

| Other comprehensive income (loss): |

|

|

|

|

|

|

|

|

|

|

|

|

| Items that may be reclassified to loss: |

|

|

|

|

|

|

|

|

|

|

|

|

| Unrealized gain (loss) on investments-net of tax |

|

|

|

|

|

|

|

|

|

|

|

|

| Continuing operations |

|

|

|

|

(4) |

|

|

|

|

|

7 |

|

| Discontinued operations |

|

|

|

|

- |

|

|

|

|

|

- |

|

| Foreign currency translation change |

|

|

|

|

|

|

|

|

|

|

|

|

| Continuing operations |

|

|

|

|

(59,653) |

|

|

|

|

|

(22,813) |

|

| Discontinued operations |

|

|

|

|

11,924 |

|

|

|

|

|

4,676 |

|

| |

|

| Comprehensive loss for the period |

|

$ |

|

|

(99,293) |

|

|

$ |

|

|

(49,833) |

|

| |

|

|

|

|

|

|

| Basic and diluted net income (loss) per share: |

|

|

|

|

|

|

|

|

|

|

|

|

| Continuing operations |

|

$ |

|

|

(0.12) |

|

|

$ |

|

|

(0.06) |

|

| Discontinued operations |

|

$ |

|

|

0.02 |

|

|

$ |

|

|

(0.01) |

|

| All operations |

|

$ |

|

|

(0.10) |

|

|

$ |

|

|

(0.06) |

|

| |

|

|

|

|

|

|

| Weighted-average number of shares outstanding (in thousands): |

|

|

|

|

|

|

|

|

|

|

|

|

| Basic and diluted |

|

|

|

|

513,415 |

|

|

|

|

|

494,510 |

|

| |

|

The accompanying notes are an integral part of the consolidated financial statements

7

Consolidated Statements of Changes in Equity

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| |

|

|

|

Year Ended |

|

| (Expressed in thousands of U.S. dollars) |

|

|

|

December 31

2015 |

|

|

|

|

December 31

2014 |

|

| |

|

|

|

|

|

|

| Share capital |

|

|

|

|

|

|

|

|

|

|

|

|

| Balance-beginning of period |

|

$ |

|

|

1,120,758 |

|

|

$ |

|

|

1,092,144 |

|

| Share issues-net of issue costs |

|

|

|

|

11,318 |

|

|

|

|

|

12,845 |

|

| Flow-through share premium |

|

|

|

|

(2,028) |

|

|

|

|

|

(2,030) |

|

| Shares issued on acquisition of Rockgate Capital Corp (note 6) |

|

|

|

|

- |

|

|

|

|

|

3,034 |

|

| Shares issued on acquisition of International Enexco Limited (note 6) |

|

|

|

|

- |

|

|

|

|

|

11,979 |

|

| Shares issued to settle payable and accrued liability obligations (note 19) |

|

|

|

|

- |

|

|

|

|

|

610 |

|

| Share options exercised-cash |

|

|

|

|

5 |

|

|

|

|

|

946 |

|

| Share options exercised-non cash |

|

|

|

|

4 |

|

|

|

|

|

525 |

|

| Share purchase warrants exercised-cash |

|

|

|

|

406 |

|

|

|

|

|

405 |

|

| Share purchase warrants exercised–non-cash |

|

|

|

|

316 |

|

|

|

|

|

300 |

|

| |

|

| Balance-end of period |

|

|

|

|

1,130,779 |

|

|

|

|

|

1,120,758 |

|

| |

|

|

|

|

|

|

| Share purchase warrants |

|

|

|

|

|

|

|

|

|

|

|

|

| Balance-beginning of period |

|

|

|

|

376 |

|

|

|

|

|

616 |

|

| Warrants issued on acquisition of International Enexco Limited (note 6) |

|

|

|

|

- |

|

|

|

|

|

61 |

|

| Warrants exercised |

|

|

|

|

(316) |

|

|

|

|

|

(300) |

|

| Warrants expired |

|

|

|

|

(60) |

|

|

|

|

|

(1) |

|

| |

|

| Balance-end of period |

|

|

|

|

- |

|

|

|

|

|

376 |

|

| |

|

|

|

|

|

|

| Contributed surplus |

|

|

|

|

|

|

|

|

|

|

|

|

| Balance-beginning of period |

|

|

|

|

53,321 |

|

|

|

|

|

52,943 |

|

| Stock-based compensation expense |

|

|

|

|

588 |

|

|

|

|

|

800 |

|

| Share options issued on acquisition of International Enexco Limited (note 6) |

|

|

|

|

- |

|

|

|

|

|

102 |

|

| Share options exercised-non-cash |

|

|

|

|

(4) |

|

|

|

|

|

(525) |

|

| Warrants expired |

|

|

|

|

60 |

|

|

|

|

|

1 |

|

| |

|

| Balance-end of period |

|

|

|

|

53,965 |

|

|

|

|

|

53,321 |

|

| |

|

|

|

|

|

|

| Deficit |

|

|

|

|

|

|

|

|

|

|

|

|

| Balance-beginning of period |

|

|

|

|

(892,537) |

|

|

|

|

|

(860,834) |

|

| Net loss |

|

|

|

|

(51,560) |

|

|

|

|

|

(31,703) |

|

| |

|

| Balance-end of period |

|

|

|

|

(944,097) |

|

|

|

|

|

(892,537) |

|

| |

|

|

|

|

|

|

| Accumulated other comprehensive loss |

|

|

|

|

|

|

|

|

|

|

|

|

| Balance-beginning of period |

|

|

|

|

(25,859) |

|

|

|

|

|

(7,729) |

|

| Unrealized gain (loss) on investments |

|

|

|

|

(4) |

|

|

|

|

|

7 |

|

| Foreign currency translation |

|

|

|

|

(61,399) |

|

|

|

|

|

(18,137) |

|

| Foreign currency translation realized in net income |

|

|

|

|

13,670 |

|

|

|

|

|

- |

|

| |

|

| Balance-end of period |

|

|

|

|

(73,592) |

|

|

|

|

|

(25,859) |

|

| |

|

|

|

|

|

|

| Total Equity |

|

|

|

|

|

|

|

|

|

|

|

|

| Balance-beginning of period |

|

$ |

|

|

256,059 |

|

|

$ |

|

|

277,140 |

|

| |

|

| Balance-end of period |

|

$ |

|

|

167,055 |

|

|

$ |

|

|

256,059 |

|

| |

|

The accompanying notes are an integral part of the consolidated financial statements

8

Consolidated Statements of Cash Flow

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| |

|

|

|

Year Ended |

|

| (Expressed in thousands of U.S. dollars) |

|

|

|

December 31

2015 |

|

|

|

|

December 31

2014 |

|

| |

|

|

|

|

|

|

| CASH PROVIDED BY (USED IN): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| OPERATING ACTIVITIES |

|

|

|

|

|

|

|

|

|

|

|

|

| Net loss for the period |

|

$ |

|

|

(51,560) |

|

|

$ |

|

|

(31,703) |

|

| Items not affecting cash: |

|

|

|

|

|

|

|

|

|

|

|

|

| Depletion, depreciation, amortization and accretion |

|

|

|

|

3,626 |

|

|

|

|

|

2,095 |

|

| Impairment-mineral properties (note 12) |

|

|

|

|

27,767 |

|

|

|

|

|

1,745 |

|

| Impairment-investments |

|

|

|

|

- |

|

|

|

|

|

22 |

|

| Stock-based compensation |

|

|

|

|

588 |

|

|

|

|

|

800 |

|

| Gain on divestiture of Mongolia Mining Division (note 6) |

|

|

|

|

(8,374) |

|

|

|

|

|

- |

|

| Gains on asset disposals |

|

|

|

|

(85) |

|

|

|

|

|

(449) |

|

| Losses on investments and restricted investments |

|

|

|

|

346 |

|

|

|

|

|

59 |

|

| Losses on reclamation obligation revisions |

|

|

|

|

2,262 |

|

|

|

|

|

2,086 |

|

| Non-cash inventory adjustments |

|

|

|

|

169 |

|

|

|

|

|

- |

|

| Deferred income tax recovery |

|

|

|

|

(3,769) |

|

|

|

|

|

(2,304) |

|

| Foreign exchange losses |

|

|

|

|

13,169 |

|

|

|

|

|

7,983 |

|

| Change in non-cash working capital items (note 23) |

|

|

|

|

(1,872) |

|

|

|

|

|

(3,834) |

|

| |

|

| Net cash used in operating activities |

|

|

|

|

(17,733) |

|

|

|

|

|

(23,500) |

|

| |

|

|

|

|

|

|

| INVESTING ACTIVITIES |

|

|

|

|

|

|

|

|

|

|

|

|

| Acquisition of asset group, net of cash and cash equivalents acquired: |

|

|

|

|

|

|

|

|

|

|

|

|

| Rockgate Capital Corp (note 6) |

|

|

|

|

- |

|

|

|

|

|

(57) |

|

| International Enexco Limited (note 6) |

|

|

|

|

- |

|

|

|

|

|

(141) |

|

| Divestiture of asset group, net of cash and cash equivalents divested: |

|

|

|

|

|

|

|

|

|

|

|

|

| Mongolia Mining Division (note 6) |

|

|

|

|

897 |

|

|

|

|

|

- |

|

| Sale of investments |

|

|

|

|

4,033 |

|

|

|

|

|

9,529 |

|

| Purchase of investments |

|

|

|

|

(8,134) |

|

|

|

|

|

(569) |

|

| Expenditures on property, plant and equipment |

|

|

|

|

(1,987) |

|

|

|

|

|

(859) |

|

| Proceeds on sale of property, plant and equipment |

|

|

|

|

115 |

|

|

|

|

|

265 |

|

| Decrease (increase) in restricted cash and investments |

|

|

|

|

(346) |

|

|

|

|

|

44 |

|

| |

|

| Net cash provided by (used in) investing activities |

|

|

|

|

(5,422) |

|

|

|

|

|

8,212 |

|

| |

|

|

|

|

|

|

| FINANCING ACTIVITIES |

|

|

|

|

|

|

|

|

|

|

|

|

| Increase (decrease) in debt obligations |

|

|

|

|

276 |

|

|

|

|

|

(53) |

|

| Issuance of common shares for: |

|

|

|

|

|

|

|

|

|

|

|

|

| New share issues-net of issue costs (note 19) |

|

|

|

|

11,318 |

|

|

|

|

|

12,845 |

|

| Share options exercised (note 19) |

|

|

|

|

5 |

|

|

|

|

|

946 |

|

| Share purchase warrants exercised (note 19) |

|

|

|

|

406 |

|

|

|

|

|

405 |

|

| |

|

| Net cash provided by financing activities |

|

|

|

|

12,005 |

|

|

|

|

|

14,143 |

|

| |

|

|

|

|

|

|

| Decrease in cash and cash equivalents |

|

|

|

|

(11,150) |

|

|

|

|

|

(1,145) |

|

| Foreign exchange effect on cash and cash equivalents |

|

|

|

|

(2,123) |

|

|

|

|

|

(2,001) |

|

| Cash and cash equivalents, beginning of period |

|

|

|

|

18,640 |

|

|

|

|

|

21,786 |

|

| |

|

| Cash and cash equivalents, end of period |

|

$ |

|

|

5,367 |

|

|

$ |

|

|

18,640 |

|

| |

|

|

|

|

|

|

| Supplemental cash flow disclosure: |

|

|

|

|

|

|

|

|

|

|

|

|

| Interest paid |

|

$ |

|

|

2 |

|

|

$ |

|

|

2 |

|

| Income taxes paid |

|

|

|

|

- |

|

|

|

|

|

- |

|

|

| |

|

The accompanying notes are an integral part of the consolidated financial statements

9

Notes to the consolidated financial statements for the years ended

December 31, 2015 and 2014

(Expressed in U.S. dollars except for shares and per share amounts)

Denison Mines Corp. and its subsidiary companies and joint arrangements (collectively, the “Company”) are engaged in uranium

mining related activities, including acquisition, exploration and development of uranium properties, extraction, processing and selling of uranium.

The Company has a 22.5% interest in the McClean Lake Joint Venture (“MLJV”) (which includes the McClean Lake mill) and a 25.17%

interest in the Midwest Joint Venture (“MWJV”), both of which are located in the Athabasca Basin of Saskatchewan, Canada. The McClean Lake mill provides toll milling services to the Cigar Lake Joint Venture (“CLJV”) under the

terms of a toll milling agreement between the parties. In addition, the Company has varying ownership interests in a number of evaluation and exploration projects located in Canada, Mali, Namibia and Zambia.

The Company provides mine decommissioning and decommissioned site monitoring services to third parties through its Denison Environmental

Services (“DES”) division and is also the manager of Uranium Participation Corporation (“UPC”), a publicly-listed investment holding company formed to invest substantially all of its assets in uranium oxide concentrates (“U3O8“) and uranium hexafluoride (“UF6”). The Company has no ownership

interest in UPC but receives fees for management services and commissions from the purchase and sale of U3O8 and UF6 by UPC.

Denison Mines Corp. (“DMC”) is incorporated under the

Business Corporations Act (Ontario) and domiciled in Canada. The address of its registered head office is 40 University Avenue, Suite 1100, Toronto, Ontario, Canada, M5J 1T1.

References to “2015” and “2014” refer to the year ended December 31, 2015 and the year ended December 31,

2014 respectively.

| 2. |

GOING CONCERN BASIS OF ACCOUNTING |

These consolidated financial statements have been prepared using International Financial Reporting Standards, as issued by the

International Accounting Standards Board, on a going concern basis, which assumes that the Company will be able to meet its obligations and continue its operations for the next twelve months.

At December 31, 2015, the Company has sufficient liquidity on hand to fund its planned operations for the fiscal 2016 year. However,

in the absence of additional funding, the Company anticipates that it will become non-compliant with the minimum cash covenant requirement of its letters of credit facility in 2016 and, as a result, there is substantial doubt upon the Company’s

ability to realize its assets and discharge its liabilities in the normal course of business, and accordingly, the appropriateness of the use of accounting principles applicable to a going concern. In order to both fund operations and maintain

rights under existing agreements, the Company must secure sufficient future funding. The Company is actively pursuing access to different sources of funding and while it has been successful in the past in obtaining financing for its activities,

there is no assurance that it will be able to obtain adequate financing in the future.

These financial statements do not reflect the

adjustments to the carrying values of assets and liabilities and the reported expenses and balance sheet classifications that would be necessary if the Company ceases to exist as a going concern in the normal course of operations. Such adjustments

could be material.

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards

(“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

The Company’s presentation

currency is U.S dollars.

These financial statements were approved by the board of directors for issue on March 9, 2016.

10

| 4. |

ACCOUNTING POLICIES AND COMPARATIVE NUMBERS |

Significant Accounting Policies

The significant accounting policies used in the preparation of these consolidated financial statements are described below:

The financial statements of the Company include the accounts of DMC and its subsidiaries and joint operations. Subsidiaries are all

entities (including structured entities) over which the group has control. The group controls an entity where the group is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those

returns through its power to direct the activities of the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the group and are deconsolidated from the date that control ceases. Intercompany

transactions, balances and unrealized gains and losses from intercompany transactions are eliminated.

Joint operations include

various mineral property interests which are held through option or contractual agreements. These arrangements involve joint control of one or more of the assets acquired or contributed for the purpose of the joint operation. The

consolidated financial statements of the Company include its share of the assets in such joint operations, together with its share of the liabilities, revenues and expenses arising jointly or otherwise from those operations. All such amounts

are measured in accordance with the terms of each arrangement.

| |

(b) |

Foreign currency translation |

| |

(i) |

Functional and presentation currency |

Items included in the financial statements of each entity in the DMC group are measured using the currency of the primary economic

environment in which the entity operates (“the functional currency”). Primary and secondary indicators are used to determine the functional currency. Primary indicators include the currency that mainly influences sales prices, labour,

material and other costs. Secondary indicators include the currency in which funds from financing activities are generated and in which receipts from operating activities are usually retained. For our entities located in Canada, Mali, Namibia and

Zambia, the local currency has been determined to be the functional currency.

The consolidated financial statements are presented

in U.S. dollars, unless otherwise stated.

The financial statements of entities that have a functional currency different from the

presentation currency of DMC (“foreign operations”) are translated into U.S. dollars as follows: assets and liabilities-at the closing rate at the date of the statement of financial position, and income and expenses-at the average rate of

the period (as this is considered a reasonable approximation to actual rates). All resulting changes are recognized in other comprehensive income or loss as cumulative foreign currency translation adjustments.

When the Company disposes of its entire interest in a foreign operation, or loses control, joint control, or significant influence over

a foreign operation, the foreign currency gains or losses accumulated in other comprehensive income or loss related to the foreign operation are recognized in the statement of income or loss as translational foreign exchange gains or losses.

| |

(ii) |

Transactions and balances |

Foreign currency transactions are translated into an entity’s functional currency using the exchange rates prevailing at the dates

of the transactions. Foreign exchange gains and losses resulting from the settlement of foreign currency transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in currencies other than an

operation’s functional currency are recognized in the statement of income or loss as transactional foreign exchange gains or losses.

| |

(c) |

Cash and cash equivalents |

Cash and cash equivalents include cash on hand, deposits held with banks, and other short-term highly liquid investments with original

maturities of three months or less which are subject to an insignificant risk of changes in value.

11

| |

(d) |

Financial instruments |

Financial assets and financial liabilities are recognized when the Company becomes a party to the contractual provisions of the financial

instrument. Financial assets are derecognized when the rights to receive cash flows from the assets have expired or have been transferred and the Company has transferred substantially all risks and rewards of ownership. Financial liabilities

are derecognized when the obligations specified in the contract is discharged, cancelled or expires.

At initial recognition, the

Company classifies its financial instruments in the following categories:

| |

(i) |

Financial assets and liabilities at fair value through profit or loss (“FVPL”) |

A financial asset or liability is classified in this category if acquired principally for the purpose of selling or repurchasing in the

short-term. Financial instruments in this category are recognized initially and subsequently at fair value. Transaction costs are expensed in the statement of income or loss. Gains and losses arising from changes in fair value are

presented in the statement of income or loss in the period in which they arise.

| |

(ii) |

Available-for-sale investments |

Available-for-sale investments are recognized initially at fair value plus transaction costs and are subsequently carried at fair

value. Gains or losses arising from re-measurement are recognized in other comprehensive income or loss. When an available-for-sale investment is sold or impaired, the accumulated gains or losses are moved from accumulated other

comprehensive income or loss to the statement of income or loss.

| |

(iii) |

Held-to-maturity investments |

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities that are

intended to be held to maturity. Held-to-maturity investments are initially recognized at fair value plus transaction costs and subsequently measured at amortized cost using the effective interest method less a provision for impairment.

| |

(iv) |

Loans and receivables |

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active

market. Loans and receivables are initially recognized at the amount expected to be received, less a discount (when material) to reduce the loans and receivables to fair value. Subsequently, loans and receivables are measured at amortized

cost using the effective interest method less a provision for impairment.

| |

(v) |

Financial liabilities at amortized cost |

Financial liabilities are initially recognized at the amount required to be paid, less a discount (when material) to reduce the

financial liabilities to fair value. Subsequently, financial liabilities are measured at amortized cost using the effective interest method.

The Company has designated its financial assets and liabilities as follows:

| |

(i) |

“Cash and cash equivalents” and “Trade and other receivables” are classified as loans and receivables and are measured at amortized cost

using the effective interest rate method, with the exception of contingent consideration which is classified as a financial asset at fair value through profit and loss (note 4(s)). Interest income is recorded in net income through finance income

(expense), as applicable; |

| |

(ii) |

A portion of “Investments” are classified as FVPL and any period change in fair value is recorded in net income within other income (expense). The

remaining amount is classified as available-for-sale and any period change in fair value is recorded in other comprehensive income. When the investment’s value becomes impaired, the loss is recognized in net income within other income (expense)

in the period of impairment; |

| |

(iii) |

“Restricted cash and investments” is classified as held-to-maturity investments; and |

| |

(iv) |

“Accounts payable and accrued liabilities” and “Debt obligations” are classified as other financial liabilities and are measured at